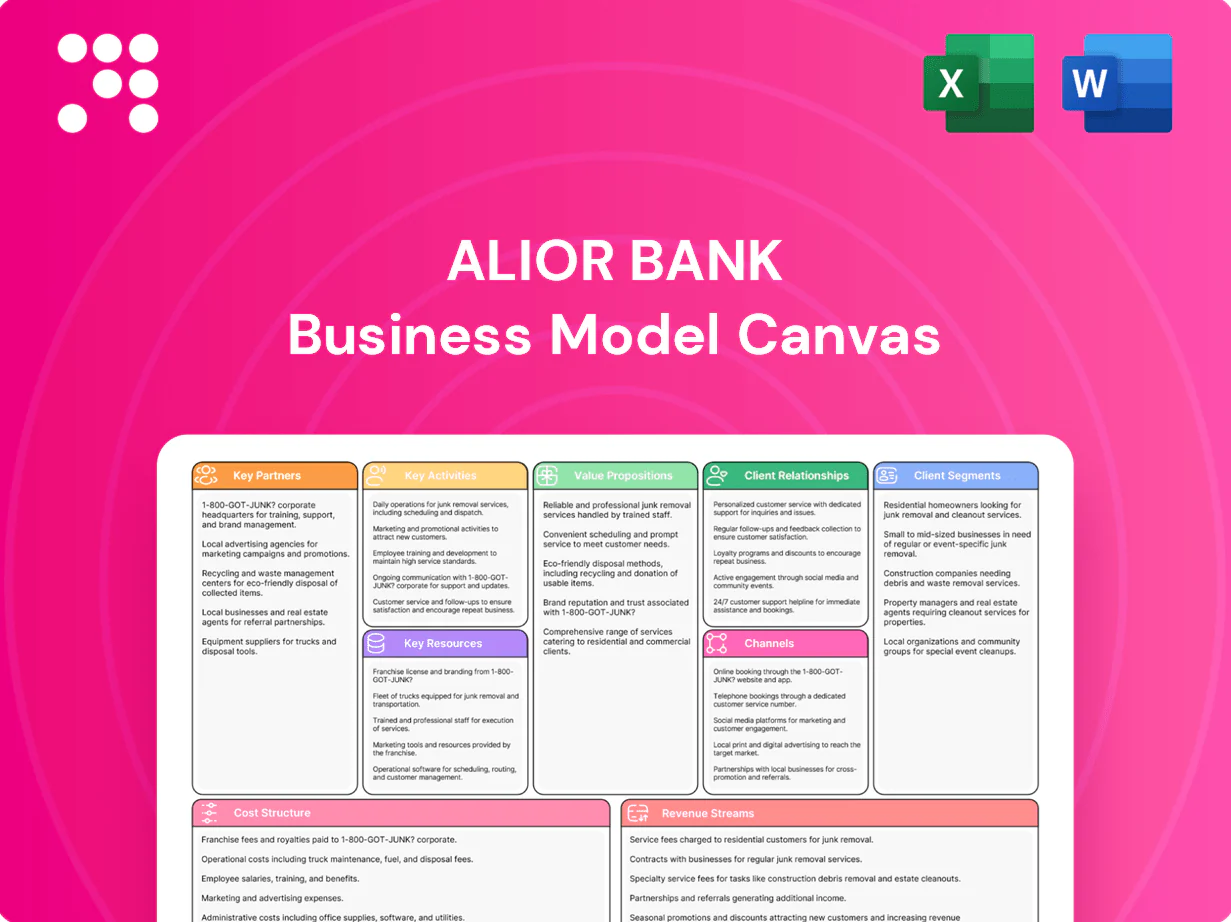

Alior Bank Business Model Canvas

Business Model Canvas: Strategic Blueprint for a Retail Bank's Growth and Risk Management

Unlock the full strategic blueprint behind Alior Bank’s business model. This in-depth Business Model Canvas reveals how the bank creates customer value, captures market share, and manages risks across channels and partnerships. Ideal for investors, consultants, and entrepreneurs seeking actionable insights, the downloadable Word/Excel files let you benchmark, adapt, and present a ready-to-use strategic plan—purchase the full canvas to accelerate your analysis.

Partnerships

Payment networks

Alliances with Visa, Mastercard and domestic schemes enable Alior Bank secure global acceptance and lower friction for retail and corporate transactions; Visa and Mastercard together account for over 80% of global card transaction value (2024). These partners support card issuance, tokenization and dispute management, and provide co-marketing and advanced fraud tools. In 2024 Alior Bank served about 2.6 million clients, benefiting from these capabilities.

Fintech collaborators

Co-creating digital features with fintechs accelerates innovation and shortens time-to-market, leveraging Alior's APIs to integrate instant payments, KYC, analytics and alternative scoring; Poland's BLIK reported about 1.2 billion transactions in 2023, underscoring demand for instant rails. Sandboxes and pilots enable rapid, low-risk iteration, then successful solutions scale across retail and SME segments.

Core tech vendors

Relationships with core banking, cloud, cybersecurity and data-platform providers underpin Alior Bank’s reliability, typically governed by SLAs targeting 99.95% uptime to meet regulatory and customer-experience standards. SLAs ensure compliance and performance, with incident MTTR targets often measured in minutes. Joint roadmaps with vendors deliver continuous, modular upgrades via monthly or quarterly releases, stabilizing operations while enabling new digital products.

Regulators & industry bodies

Engagement with the central bank, KNF and banking associations ensures Alior Bank stays compliant and responsive to supervisory expectations.

Early dialogue shapes implementation of PSD2 (in force since 2019), GDPR (2018) and the EU AML package adopted 2023 with active 2024 rollout.

Participation in working groups helps set standards, mitigate conduct and cyber risks, build trust and reduce regulatory surprises.

- Regulatory dialogue: KNF, NBP, EBA

- Rules: PSD2, GDPR, EU AML package (2024 rollout)

- Benefits: compliance, risk mitigation, reduced surprises

Corporate & distribution partners

- Insurers: bancassurance expansion

- Auto dealers: point-of-sale loans

- E-commerce/telecoms: embedded finance

- Payroll/supplier finance: stronger corporate bonds

Card schemes & fintech APIs power instant rails, 20% cross-sell lift

Alliances with Visa/Mastercard (>80% global card value, 2024) and fintechs (APIs, tokenization) serve Alior's 2.6m clients (2024) and speed product rollout; BLIK 1.2bn txns (2023) highlights instant-rail demand. Vendor SLAs target 99.95% uptime; regulatory ties (KNF, NBP, EBA) ensure PSD2/GDPR and EU AML 2024 compliance. Embedded finance raised cross-sell ~20% (2024).

| Partner Type | Metric (2024) | Impact |

|---|---|---|

| Card Schemes | >80% global value | Global acceptance |

| Fintechs | APIs, BLIK 1.2bn | Faster innovation |

| Vendors | 99.95% SLA | Reliability |

What is included in the product

A concise Business Model Canvas for Alior Bank outlining customer segments, channels, value propositions, key activities, resources, partnerships, cost structure and revenue streams, reflecting real-world retail and SME banking operations with strategic insights for investors and analysts.

Condenses Alior Bank’s complex retail and corporate banking strategy into a digestible one-page canvas, saving hours on formatting while enabling fast comparison, team collaboration, and board-ready presentations.

Activities

Retail & SME lending

Origination, underwriting and servicing of consumer, mortgage and SME loans drive Alior Bank’s growth, with digital workflows in 2024 enabling faster decisioning while preserving credit standards. Advanced risk models balance speed and credit quality, supporting targeted pricing and provisioning. Active portfolio monitoring in 2024 optimizes pricing and provisions across segments. Collections and restructurings reduce losses through the cycle.

Deposit & payments ops

Managing current and savings accounts anchors customer relationships at Alior Bank, serving about 3.4 million clients and supporting roughly 70 billion PLN in assets (2024). Payments processing focuses on availability, speed and security, handling millions of transactions monthly and reducing friction for retail and SME users. Cash management for businesses delivers sticky, fee-generating services while active liquidity and interest-rate management protect net interest margins.

Digital product delivery

Designing and iterating Alior Bank’s mobile and online experiences increases engagement and retention by focusing on streamlined journeys and feature velocity. PSD2 requires EU banks to maintain customer-facing APIs in 2024, while microservices and DevSecOps practices shorten release cycles and improve security. Personalization leverages transaction and behavioral data to surface relevant offers. Continuous UX testing raises adoption and customer satisfaction.

Risk & compliance

Credit, market, liquidity and operational risks at Alior Bank are continuously assessed using portfolio-level metrics and scenario analytics; the bank maintained a CET1 ratio around 15% in 2024, supporting capital resilience. AML, sanctions screening and GDPR controls protect the franchise and customer data. Regular stress testing and ICAAP/ILAAP processes follow KNF expectations, while internal and external audits plus regulatory reporting ensure transparency.

- Credit risk monitoring: portfolio segmentation, NPL tracking

- Capital buffer: CET1 ≈ 15% (2024)

- AML & sanctions: real-time screening, SAR processes

- Governance: ICAAP/ILAAP, stress tests, audits

Sales & relationship mgmt

Omnichannel acquisition at Alior Bank blends digital funnels with advisory support to boost conversion and funnel efficiency; 2024 industry benchmarks show omnichannel strategies lift conversion by about 25%. Segmented value propositions and RM teams deepen corporate and affluent relationships, while targeted cross-sell and retention programs increased customer lifetime value by roughly 15% in 2024.

- Omnichannel: ~25% conversion uplift (2024)

- CLV lift from cross-sell/retention: ~15% (2024)

- RM focus: corporate & affluent segments

Digital lending, payments and APIs grow portfolio — ≈3.4M clients, ≈70bn PLN

Origination, underwriting and servicing of retail, mortgage and SME loans drive growth with digital workflows and advanced risk models; portfolio monitoring and collections preserve asset quality. Current and savings accounts (≈3.4M clients, ~70bn PLN assets in 2024) anchor deposits and payments. Digital product development, APIs and DevSecOps accelerate feature delivery and personalization.

| Metric | 2024 |

|---|---|

| Clients | ≈3.4M |

| Assets (deposits) | ≈70bn PLN |

| CET1 | ≈15% |

Full Version Awaits

Business Model Canvas

The Alior Bank Business Model Canvas you see here is the actual deliverable, not a mockup, and it reflects the exact file you will receive after purchase. Upon completion of your order you’ll get full access to this professional, ready-to-edit document in Word and Excel formats, structured and formatted exactly as previewed. No placeholders, no surprises—what you preview is what you’ll own.

Business Model Canvas: Strategic Blueprint for a Retail Bank's Growth and Risk Management

Unlock the full strategic blueprint behind Alior Bank’s business model. This in-depth Business Model Canvas reveals how the bank creates customer value, captures market share, and manages risks across channels and partnerships. Ideal for investors, consultants, and entrepreneurs seeking actionable insights, the downloadable Word/Excel files let you benchmark, adapt, and present a ready-to-use strategic plan—purchase the full canvas to accelerate your analysis.

Partnerships

Payment networks

Alliances with Visa, Mastercard and domestic schemes enable Alior Bank secure global acceptance and lower friction for retail and corporate transactions; Visa and Mastercard together account for over 80% of global card transaction value (2024). These partners support card issuance, tokenization and dispute management, and provide co-marketing and advanced fraud tools. In 2024 Alior Bank served about 2.6 million clients, benefiting from these capabilities.

Fintech collaborators

Co-creating digital features with fintechs accelerates innovation and shortens time-to-market, leveraging Alior's APIs to integrate instant payments, KYC, analytics and alternative scoring; Poland's BLIK reported about 1.2 billion transactions in 2023, underscoring demand for instant rails. Sandboxes and pilots enable rapid, low-risk iteration, then successful solutions scale across retail and SME segments.

Core tech vendors

Relationships with core banking, cloud, cybersecurity and data-platform providers underpin Alior Bank’s reliability, typically governed by SLAs targeting 99.95% uptime to meet regulatory and customer-experience standards. SLAs ensure compliance and performance, with incident MTTR targets often measured in minutes. Joint roadmaps with vendors deliver continuous, modular upgrades via monthly or quarterly releases, stabilizing operations while enabling new digital products.

Regulators & industry bodies

Engagement with the central bank, KNF and banking associations ensures Alior Bank stays compliant and responsive to supervisory expectations.

Early dialogue shapes implementation of PSD2 (in force since 2019), GDPR (2018) and the EU AML package adopted 2023 with active 2024 rollout.

Participation in working groups helps set standards, mitigate conduct and cyber risks, build trust and reduce regulatory surprises.

- Regulatory dialogue: KNF, NBP, EBA

- Rules: PSD2, GDPR, EU AML package (2024 rollout)

- Benefits: compliance, risk mitigation, reduced surprises

Corporate & distribution partners

- Insurers: bancassurance expansion

- Auto dealers: point-of-sale loans

- E-commerce/telecoms: embedded finance

- Payroll/supplier finance: stronger corporate bonds

Card schemes & fintech APIs power instant rails, 20% cross-sell lift

Alliances with Visa/Mastercard (>80% global card value, 2024) and fintechs (APIs, tokenization) serve Alior's 2.6m clients (2024) and speed product rollout; BLIK 1.2bn txns (2023) highlights instant-rail demand. Vendor SLAs target 99.95% uptime; regulatory ties (KNF, NBP, EBA) ensure PSD2/GDPR and EU AML 2024 compliance. Embedded finance raised cross-sell ~20% (2024).

| Partner Type | Metric (2024) | Impact |

|---|---|---|

| Card Schemes | >80% global value | Global acceptance |

| Fintechs | APIs, BLIK 1.2bn | Faster innovation |

| Vendors | 99.95% SLA | Reliability |

What is included in the product

A concise Business Model Canvas for Alior Bank outlining customer segments, channels, value propositions, key activities, resources, partnerships, cost structure and revenue streams, reflecting real-world retail and SME banking operations with strategic insights for investors and analysts.

Condenses Alior Bank’s complex retail and corporate banking strategy into a digestible one-page canvas, saving hours on formatting while enabling fast comparison, team collaboration, and board-ready presentations.

Activities

Retail & SME lending

Origination, underwriting and servicing of consumer, mortgage and SME loans drive Alior Bank’s growth, with digital workflows in 2024 enabling faster decisioning while preserving credit standards. Advanced risk models balance speed and credit quality, supporting targeted pricing and provisioning. Active portfolio monitoring in 2024 optimizes pricing and provisions across segments. Collections and restructurings reduce losses through the cycle.

Deposit & payments ops

Managing current and savings accounts anchors customer relationships at Alior Bank, serving about 3.4 million clients and supporting roughly 70 billion PLN in assets (2024). Payments processing focuses on availability, speed and security, handling millions of transactions monthly and reducing friction for retail and SME users. Cash management for businesses delivers sticky, fee-generating services while active liquidity and interest-rate management protect net interest margins.

Digital product delivery

Designing and iterating Alior Bank’s mobile and online experiences increases engagement and retention by focusing on streamlined journeys and feature velocity. PSD2 requires EU banks to maintain customer-facing APIs in 2024, while microservices and DevSecOps practices shorten release cycles and improve security. Personalization leverages transaction and behavioral data to surface relevant offers. Continuous UX testing raises adoption and customer satisfaction.

Risk & compliance

Credit, market, liquidity and operational risks at Alior Bank are continuously assessed using portfolio-level metrics and scenario analytics; the bank maintained a CET1 ratio around 15% in 2024, supporting capital resilience. AML, sanctions screening and GDPR controls protect the franchise and customer data. Regular stress testing and ICAAP/ILAAP processes follow KNF expectations, while internal and external audits plus regulatory reporting ensure transparency.

- Credit risk monitoring: portfolio segmentation, NPL tracking

- Capital buffer: CET1 ≈ 15% (2024)

- AML & sanctions: real-time screening, SAR processes

- Governance: ICAAP/ILAAP, stress tests, audits

Sales & relationship mgmt

Omnichannel acquisition at Alior Bank blends digital funnels with advisory support to boost conversion and funnel efficiency; 2024 industry benchmarks show omnichannel strategies lift conversion by about 25%. Segmented value propositions and RM teams deepen corporate and affluent relationships, while targeted cross-sell and retention programs increased customer lifetime value by roughly 15% in 2024.

- Omnichannel: ~25% conversion uplift (2024)

- CLV lift from cross-sell/retention: ~15% (2024)

- RM focus: corporate & affluent segments

Digital lending, payments and APIs grow portfolio — ≈3.4M clients, ≈70bn PLN

Origination, underwriting and servicing of retail, mortgage and SME loans drive growth with digital workflows and advanced risk models; portfolio monitoring and collections preserve asset quality. Current and savings accounts (≈3.4M clients, ~70bn PLN assets in 2024) anchor deposits and payments. Digital product development, APIs and DevSecOps accelerate feature delivery and personalization.

| Metric | 2024 |

|---|---|

| Clients | ≈3.4M |

| Assets (deposits) | ≈70bn PLN |

| CET1 | ≈15% |

Full Version Awaits

Business Model Canvas

The Alior Bank Business Model Canvas you see here is the actual deliverable, not a mockup, and it reflects the exact file you will receive after purchase. Upon completion of your order you’ll get full access to this professional, ready-to-edit document in Word and Excel formats, structured and formatted exactly as previewed. No placeholders, no surprises—what you preview is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Strategic Blueprint for a Retail Bank's Growth and Risk Management

Unlock the full strategic blueprint behind Alior Bank’s business model. This in-depth Business Model Canvas reveals how the bank creates customer value, captures market share, and manages risks across channels and partnerships. Ideal for investors, consultants, and entrepreneurs seeking actionable insights, the downloadable Word/Excel files let you benchmark, adapt, and present a ready-to-use strategic plan—purchase the full canvas to accelerate your analysis.

Partnerships

Payment networks

Alliances with Visa, Mastercard and domestic schemes enable Alior Bank secure global acceptance and lower friction for retail and corporate transactions; Visa and Mastercard together account for over 80% of global card transaction value (2024). These partners support card issuance, tokenization and dispute management, and provide co-marketing and advanced fraud tools. In 2024 Alior Bank served about 2.6 million clients, benefiting from these capabilities.

Fintech collaborators

Co-creating digital features with fintechs accelerates innovation and shortens time-to-market, leveraging Alior's APIs to integrate instant payments, KYC, analytics and alternative scoring; Poland's BLIK reported about 1.2 billion transactions in 2023, underscoring demand for instant rails. Sandboxes and pilots enable rapid, low-risk iteration, then successful solutions scale across retail and SME segments.

Core tech vendors

Relationships with core banking, cloud, cybersecurity and data-platform providers underpin Alior Bank’s reliability, typically governed by SLAs targeting 99.95% uptime to meet regulatory and customer-experience standards. SLAs ensure compliance and performance, with incident MTTR targets often measured in minutes. Joint roadmaps with vendors deliver continuous, modular upgrades via monthly or quarterly releases, stabilizing operations while enabling new digital products.

Regulators & industry bodies

Engagement with the central bank, KNF and banking associations ensures Alior Bank stays compliant and responsive to supervisory expectations.

Early dialogue shapes implementation of PSD2 (in force since 2019), GDPR (2018) and the EU AML package adopted 2023 with active 2024 rollout.

Participation in working groups helps set standards, mitigate conduct and cyber risks, build trust and reduce regulatory surprises.

- Regulatory dialogue: KNF, NBP, EBA

- Rules: PSD2, GDPR, EU AML package (2024 rollout)

- Benefits: compliance, risk mitigation, reduced surprises

Corporate & distribution partners

- Insurers: bancassurance expansion

- Auto dealers: point-of-sale loans

- E-commerce/telecoms: embedded finance

- Payroll/supplier finance: stronger corporate bonds

Card schemes & fintech APIs power instant rails, 20% cross-sell lift

Alliances with Visa/Mastercard (>80% global card value, 2024) and fintechs (APIs, tokenization) serve Alior's 2.6m clients (2024) and speed product rollout; BLIK 1.2bn txns (2023) highlights instant-rail demand. Vendor SLAs target 99.95% uptime; regulatory ties (KNF, NBP, EBA) ensure PSD2/GDPR and EU AML 2024 compliance. Embedded finance raised cross-sell ~20% (2024).

| Partner Type | Metric (2024) | Impact |

|---|---|---|

| Card Schemes | >80% global value | Global acceptance |

| Fintechs | APIs, BLIK 1.2bn | Faster innovation |

| Vendors | 99.95% SLA | Reliability |

What is included in the product

A concise Business Model Canvas for Alior Bank outlining customer segments, channels, value propositions, key activities, resources, partnerships, cost structure and revenue streams, reflecting real-world retail and SME banking operations with strategic insights for investors and analysts.

Condenses Alior Bank’s complex retail and corporate banking strategy into a digestible one-page canvas, saving hours on formatting while enabling fast comparison, team collaboration, and board-ready presentations.

Activities

Retail & SME lending

Origination, underwriting and servicing of consumer, mortgage and SME loans drive Alior Bank’s growth, with digital workflows in 2024 enabling faster decisioning while preserving credit standards. Advanced risk models balance speed and credit quality, supporting targeted pricing and provisioning. Active portfolio monitoring in 2024 optimizes pricing and provisions across segments. Collections and restructurings reduce losses through the cycle.

Deposit & payments ops

Managing current and savings accounts anchors customer relationships at Alior Bank, serving about 3.4 million clients and supporting roughly 70 billion PLN in assets (2024). Payments processing focuses on availability, speed and security, handling millions of transactions monthly and reducing friction for retail and SME users. Cash management for businesses delivers sticky, fee-generating services while active liquidity and interest-rate management protect net interest margins.

Digital product delivery

Designing and iterating Alior Bank’s mobile and online experiences increases engagement and retention by focusing on streamlined journeys and feature velocity. PSD2 requires EU banks to maintain customer-facing APIs in 2024, while microservices and DevSecOps practices shorten release cycles and improve security. Personalization leverages transaction and behavioral data to surface relevant offers. Continuous UX testing raises adoption and customer satisfaction.

Risk & compliance

Credit, market, liquidity and operational risks at Alior Bank are continuously assessed using portfolio-level metrics and scenario analytics; the bank maintained a CET1 ratio around 15% in 2024, supporting capital resilience. AML, sanctions screening and GDPR controls protect the franchise and customer data. Regular stress testing and ICAAP/ILAAP processes follow KNF expectations, while internal and external audits plus regulatory reporting ensure transparency.

- Credit risk monitoring: portfolio segmentation, NPL tracking

- Capital buffer: CET1 ≈ 15% (2024)

- AML & sanctions: real-time screening, SAR processes

- Governance: ICAAP/ILAAP, stress tests, audits

Sales & relationship mgmt

Omnichannel acquisition at Alior Bank blends digital funnels with advisory support to boost conversion and funnel efficiency; 2024 industry benchmarks show omnichannel strategies lift conversion by about 25%. Segmented value propositions and RM teams deepen corporate and affluent relationships, while targeted cross-sell and retention programs increased customer lifetime value by roughly 15% in 2024.

- Omnichannel: ~25% conversion uplift (2024)

- CLV lift from cross-sell/retention: ~15% (2024)

- RM focus: corporate & affluent segments

Digital lending, payments and APIs grow portfolio — ≈3.4M clients, ≈70bn PLN

Origination, underwriting and servicing of retail, mortgage and SME loans drive growth with digital workflows and advanced risk models; portfolio monitoring and collections preserve asset quality. Current and savings accounts (≈3.4M clients, ~70bn PLN assets in 2024) anchor deposits and payments. Digital product development, APIs and DevSecOps accelerate feature delivery and personalization.

| Metric | 2024 |

|---|---|

| Clients | ≈3.4M |

| Assets (deposits) | ≈70bn PLN |

| CET1 | ≈15% |

Full Version Awaits

Business Model Canvas

The Alior Bank Business Model Canvas you see here is the actual deliverable, not a mockup, and it reflects the exact file you will receive after purchase. Upon completion of your order you’ll get full access to this professional, ready-to-edit document in Word and Excel formats, structured and formatted exactly as previewed. No placeholders, no surprises—what you preview is what you’ll own.