Alkermes Boston Consulting Group Matrix

See the Bigger Picture

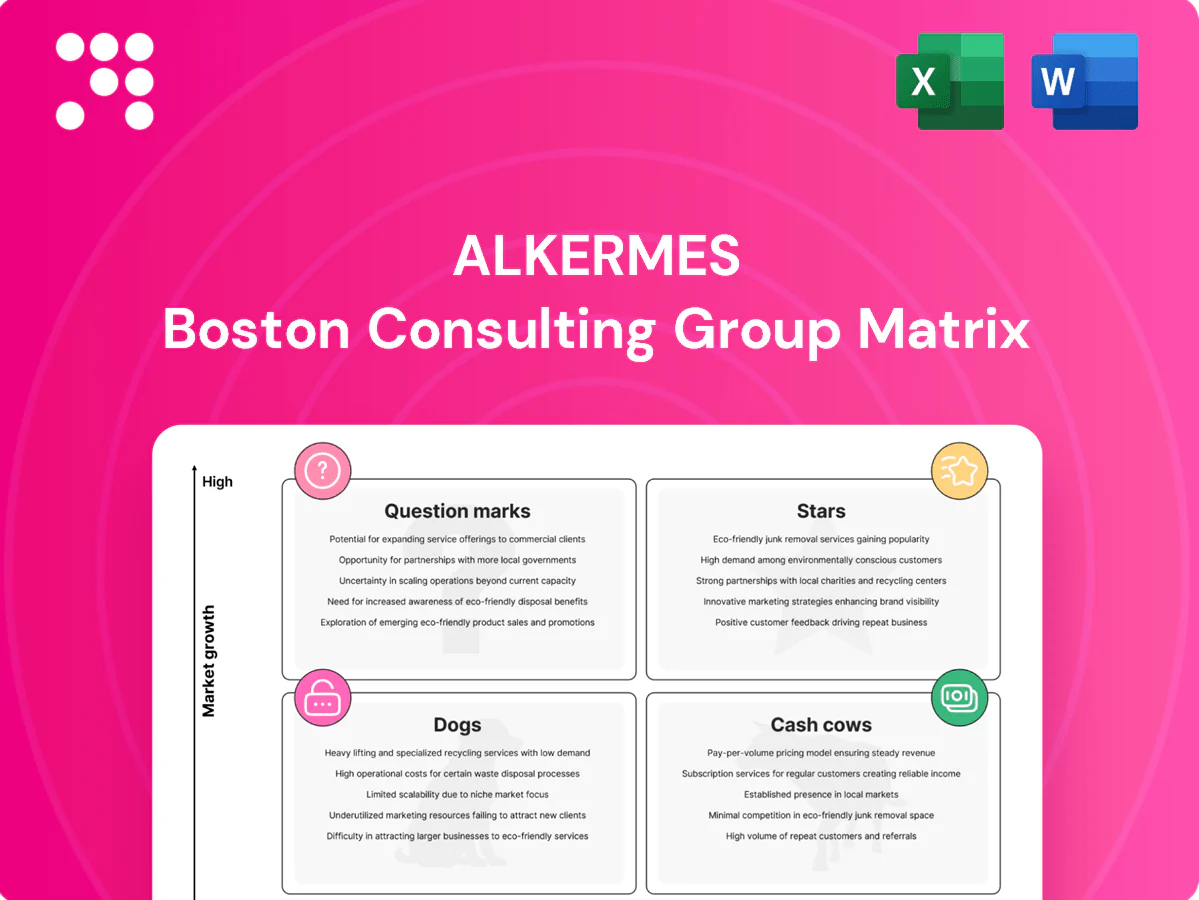

Curious where Alkermes’ products sit—Stars, Cash Cows, Dogs, or Question Marks? This compact BCG preview teases the strategic picture; buy the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word + Excel deliverables. Get the clarity to reallocate capital, prioritize R&D, and act fast.

Stars

Lybalvi momentum

Lybalvi momentum: fast uptake in schizophrenia and bipolar I since FDA approval in December 2021, driven by strong physician interest in weight-sparing antipsychotics. Promotion remains heavy while scripts compound and payer wins are stacking. Keep the foot down — this can graduate to Cash Cow as the category matures. It’s Alkermes’ growth engine to defend.

Aristada LAI franchise

Aristada LAI sits in a long-acting antipsychotic market growing ~8% CAGR (2024–28) with LAIs showing ~30–40% lower relapse/hospitalization versus orals; where access exists Aristada holds double-digit specialty-clinic share (~15–20%) and INITIO shortens onboarding; it consumes promotion but drives scale—strategy: defend share, expand site footprint, and it will compound revenue.

CNS platform leadership

Alkermes’ hard-won capabilities in psychiatric formulations and delivery create a defensible platform edge, underpinning repeatable product differentiation rather than a single SKU; Alkermes reported 2024 revenue of about $1.09 billion, driven largely by CNS franchises. The platform enables faster launches and more effective lifecycle tactics, shortening time-to-peak vs peers. Continued investment is required to keep the commercialization and formulation flywheel spinning.

Payer/access execution

Payer/access execution is converting market-access wins into measurable clinic conversion as hub-enabled territories show clear pull-through and refill adherence improvements. Priority remains reducing prior authorization latency and accelerating reimbursement to sustain share gains in high-growth pockets. Frictionless access drives physician prescribing and patient uptake when hub services perform consistently.

- Market-access wins → clinic conversion via hub support

- Reduce prior auth and reimbursement delays

- Frictionless access increases share and pull-through

Real-world outcomes story

Real-world outcomes show health-econ signals on adherence and improved metabolic profiles are driving system interest; real-world adherence for serious mental illness often hovers around 50%, and reducing relapses materially lowers total cost of care. Systems want fewer relapses and better tolerability—Alkermes can demonstrate this through outcomes data. Publish, present, repeat to build prescriber confidence and sales growth.

- Adherence ~50% baseline

- Relapse reduction = lower total cost of care

- Better tolerability → higher prescribing confidence

CNS growth fuels uptake — 2024 revenue 1.09B; LAI market 8%

Alkermes Stars: Lybalvi driving rapid uptake in schizophrenia/bipolar since Dec 2021 approval; 2024 Alkermes revenue ~$1.09B with CNS growth engine. Aristada LAI in an ~8% CAGR LAI market (2024–28), holding ~15–20% specialty-clinic share and reducing relapse 30–40%; adherence baseline ~50%. Prior-auth and hub scale are key to converting access wins into sustained share.

| Metric | Value (2024) |

|---|---|

| Alkermes revenue | $1.09B |

| LAI market CAGR (2024–28) | ~8% |

| Aristada share | 15–20% |

| Relapse reduction | 30–40% |

| Adherence baseline | ~50% |

What is included in the product

BCG Matrix review of Alkermes products: Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page Alkermes BCG Matrix that maps units into quadrants to cut analysis time and simplify exec decisions.

Cash Cows

Vivitrol

Vivitrol sits in a mature MAT market estimated at >$2.5B in 2024 and delivers roughly $400M in annual revenue, reflecting durable brand recognition and steady demand across alcohol and opioid dependence indications. Promotion is efficient and distribution channels are well-worn, producing reliable cash flow that funds Alkermes’ pipeline and field force. Focus on optimizing manufacturing throughput and keeping patient churn below industry levels to sustain margins.

Vumerity royalties

Vumerity (diroximel fumarate), FDA-approved in 2019, generates a royalty stream for Alkermes that delivers predictable, high-margin cash with minimal operating burden and little promotional spend. This royalty acts as dependable ballast on the P&L, supporting R&D and debt servicing. Management must protect the license and monitor generic entry and patent expiry timelines closely to sustain cash flow.

Aristada base business

As of 2024 Aristada base business delivers recurring monthly and multi‑month injections across core accounts, producing predictable inventory turns and steady clinic throughput.

Incremental investments in field support and patient access remain modest relative to output, preserving healthy per‑unit economics through 2024.

Gross margins strengthen with scale, so Alkermes continues to milk Aristada while selectively expanding high‑yield sites in 2024.

Established provider networks

Established provider networks drive repeatable, efficient detailing to long-standing psych prescribers, lowering cost per script and converting clinical engagement into steady cash flow; maintaining cadence without overspending preserves margin. In 2024 these networks remained Alkermes’ operational cash cows, enabling predictable prescription refill economics and faster cash conversion cycles.

- Repeatable detailing

- Lower cost per script

- Predictable cash conversion

- Maintain cadence, cap spend

Manufacturing know-how

Manufacturing know-how at Alkermes drove 2024 margin stability as process yields and tech-transfer skills cut COGS by an estimated 5–8% and stabilized supply across sites; small capex tweaks in a mature footprint lifted gross margins by roughly 200–300 bps. Line uptime targets >95% and scrap <1% keep this cash generator humming behind the curtain.

- COGS reduction: 5–8% (2024)

- Margin lift: ~200–300 bps from small capex

- Line uptime: >95%

- Scrap: <1%

Steady cash: $400M, royalties, recurring injections, +200–300bps

Vivitrol: $400M revenue in a >$2.5B MAT market (2024), steady cash flow; Vumerity: high‑margin royalty stream with minimal opex; Aristada: recurring injections driving predictable clinic throughput; manufacturing efficiency cut COGS 5–8% and lifted gross margins ~200–300 bps in 2024.

| Asset | 2024 metric | Role |

|---|---|---|

| Vivitrol | $400M | Primary cash cow |

| Vumerity | Royalty stream | Low‑cost cash |

| Aristada | Recurring injections | Stable cash |

| Manufacturing | COGS -5–8% | Margin support |

What You’re Viewing Is Included

Alkermes BCG Matrix

The Alkermes BCG Matrix you're previewing here is the exact file you'll receive after purchase — no watermarks, no placeholders, just the finished, analysis-ready report. It's built for strategic clarity and formatted for immediate use: edit, print, or present straight away. One purchase, one download, no surprises.

See the Bigger Picture

Curious where Alkermes’ products sit—Stars, Cash Cows, Dogs, or Question Marks? This compact BCG preview teases the strategic picture; buy the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word + Excel deliverables. Get the clarity to reallocate capital, prioritize R&D, and act fast.

Stars

Lybalvi momentum

Lybalvi momentum: fast uptake in schizophrenia and bipolar I since FDA approval in December 2021, driven by strong physician interest in weight-sparing antipsychotics. Promotion remains heavy while scripts compound and payer wins are stacking. Keep the foot down — this can graduate to Cash Cow as the category matures. It’s Alkermes’ growth engine to defend.

Aristada LAI franchise

Aristada LAI sits in a long-acting antipsychotic market growing ~8% CAGR (2024–28) with LAIs showing ~30–40% lower relapse/hospitalization versus orals; where access exists Aristada holds double-digit specialty-clinic share (~15–20%) and INITIO shortens onboarding; it consumes promotion but drives scale—strategy: defend share, expand site footprint, and it will compound revenue.

CNS platform leadership

Alkermes’ hard-won capabilities in psychiatric formulations and delivery create a defensible platform edge, underpinning repeatable product differentiation rather than a single SKU; Alkermes reported 2024 revenue of about $1.09 billion, driven largely by CNS franchises. The platform enables faster launches and more effective lifecycle tactics, shortening time-to-peak vs peers. Continued investment is required to keep the commercialization and formulation flywheel spinning.

Payer/access execution

Payer/access execution is converting market-access wins into measurable clinic conversion as hub-enabled territories show clear pull-through and refill adherence improvements. Priority remains reducing prior authorization latency and accelerating reimbursement to sustain share gains in high-growth pockets. Frictionless access drives physician prescribing and patient uptake when hub services perform consistently.

- Market-access wins → clinic conversion via hub support

- Reduce prior auth and reimbursement delays

- Frictionless access increases share and pull-through

Real-world outcomes story

Real-world outcomes show health-econ signals on adherence and improved metabolic profiles are driving system interest; real-world adherence for serious mental illness often hovers around 50%, and reducing relapses materially lowers total cost of care. Systems want fewer relapses and better tolerability—Alkermes can demonstrate this through outcomes data. Publish, present, repeat to build prescriber confidence and sales growth.

- Adherence ~50% baseline

- Relapse reduction = lower total cost of care

- Better tolerability → higher prescribing confidence

CNS growth fuels uptake — 2024 revenue 1.09B; LAI market 8%

Alkermes Stars: Lybalvi driving rapid uptake in schizophrenia/bipolar since Dec 2021 approval; 2024 Alkermes revenue ~$1.09B with CNS growth engine. Aristada LAI in an ~8% CAGR LAI market (2024–28), holding ~15–20% specialty-clinic share and reducing relapse 30–40%; adherence baseline ~50%. Prior-auth and hub scale are key to converting access wins into sustained share.

| Metric | Value (2024) |

|---|---|

| Alkermes revenue | $1.09B |

| LAI market CAGR (2024–28) | ~8% |

| Aristada share | 15–20% |

| Relapse reduction | 30–40% |

| Adherence baseline | ~50% |

What is included in the product

BCG Matrix review of Alkermes products: Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page Alkermes BCG Matrix that maps units into quadrants to cut analysis time and simplify exec decisions.

Cash Cows

Vivitrol

Vivitrol sits in a mature MAT market estimated at >$2.5B in 2024 and delivers roughly $400M in annual revenue, reflecting durable brand recognition and steady demand across alcohol and opioid dependence indications. Promotion is efficient and distribution channels are well-worn, producing reliable cash flow that funds Alkermes’ pipeline and field force. Focus on optimizing manufacturing throughput and keeping patient churn below industry levels to sustain margins.

Vumerity royalties

Vumerity (diroximel fumarate), FDA-approved in 2019, generates a royalty stream for Alkermes that delivers predictable, high-margin cash with minimal operating burden and little promotional spend. This royalty acts as dependable ballast on the P&L, supporting R&D and debt servicing. Management must protect the license and monitor generic entry and patent expiry timelines closely to sustain cash flow.

Aristada base business

As of 2024 Aristada base business delivers recurring monthly and multi‑month injections across core accounts, producing predictable inventory turns and steady clinic throughput.

Incremental investments in field support and patient access remain modest relative to output, preserving healthy per‑unit economics through 2024.

Gross margins strengthen with scale, so Alkermes continues to milk Aristada while selectively expanding high‑yield sites in 2024.

Established provider networks

Established provider networks drive repeatable, efficient detailing to long-standing psych prescribers, lowering cost per script and converting clinical engagement into steady cash flow; maintaining cadence without overspending preserves margin. In 2024 these networks remained Alkermes’ operational cash cows, enabling predictable prescription refill economics and faster cash conversion cycles.

- Repeatable detailing

- Lower cost per script

- Predictable cash conversion

- Maintain cadence, cap spend

Manufacturing know-how

Manufacturing know-how at Alkermes drove 2024 margin stability as process yields and tech-transfer skills cut COGS by an estimated 5–8% and stabilized supply across sites; small capex tweaks in a mature footprint lifted gross margins by roughly 200–300 bps. Line uptime targets >95% and scrap <1% keep this cash generator humming behind the curtain.

- COGS reduction: 5–8% (2024)

- Margin lift: ~200–300 bps from small capex

- Line uptime: >95%

- Scrap: <1%

Steady cash: $400M, royalties, recurring injections, +200–300bps

Vivitrol: $400M revenue in a >$2.5B MAT market (2024), steady cash flow; Vumerity: high‑margin royalty stream with minimal opex; Aristada: recurring injections driving predictable clinic throughput; manufacturing efficiency cut COGS 5–8% and lifted gross margins ~200–300 bps in 2024.

| Asset | 2024 metric | Role |

|---|---|---|

| Vivitrol | $400M | Primary cash cow |

| Vumerity | Royalty stream | Low‑cost cash |

| Aristada | Recurring injections | Stable cash |

| Manufacturing | COGS -5–8% | Margin support |

What You’re Viewing Is Included

Alkermes BCG Matrix

The Alkermes BCG Matrix you're previewing here is the exact file you'll receive after purchase — no watermarks, no placeholders, just the finished, analysis-ready report. It's built for strategic clarity and formatted for immediate use: edit, print, or present straight away. One purchase, one download, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Curious where Alkermes’ products sit—Stars, Cash Cows, Dogs, or Question Marks? This compact BCG preview teases the strategic picture; buy the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and ready-to-use Word + Excel deliverables. Get the clarity to reallocate capital, prioritize R&D, and act fast.

Stars

Lybalvi momentum

Lybalvi momentum: fast uptake in schizophrenia and bipolar I since FDA approval in December 2021, driven by strong physician interest in weight-sparing antipsychotics. Promotion remains heavy while scripts compound and payer wins are stacking. Keep the foot down — this can graduate to Cash Cow as the category matures. It’s Alkermes’ growth engine to defend.

Aristada LAI franchise

Aristada LAI sits in a long-acting antipsychotic market growing ~8% CAGR (2024–28) with LAIs showing ~30–40% lower relapse/hospitalization versus orals; where access exists Aristada holds double-digit specialty-clinic share (~15–20%) and INITIO shortens onboarding; it consumes promotion but drives scale—strategy: defend share, expand site footprint, and it will compound revenue.

CNS platform leadership

Alkermes’ hard-won capabilities in psychiatric formulations and delivery create a defensible platform edge, underpinning repeatable product differentiation rather than a single SKU; Alkermes reported 2024 revenue of about $1.09 billion, driven largely by CNS franchises. The platform enables faster launches and more effective lifecycle tactics, shortening time-to-peak vs peers. Continued investment is required to keep the commercialization and formulation flywheel spinning.

Payer/access execution

Payer/access execution is converting market-access wins into measurable clinic conversion as hub-enabled territories show clear pull-through and refill adherence improvements. Priority remains reducing prior authorization latency and accelerating reimbursement to sustain share gains in high-growth pockets. Frictionless access drives physician prescribing and patient uptake when hub services perform consistently.

- Market-access wins → clinic conversion via hub support

- Reduce prior auth and reimbursement delays

- Frictionless access increases share and pull-through

Real-world outcomes story

Real-world outcomes show health-econ signals on adherence and improved metabolic profiles are driving system interest; real-world adherence for serious mental illness often hovers around 50%, and reducing relapses materially lowers total cost of care. Systems want fewer relapses and better tolerability—Alkermes can demonstrate this through outcomes data. Publish, present, repeat to build prescriber confidence and sales growth.

- Adherence ~50% baseline

- Relapse reduction = lower total cost of care

- Better tolerability → higher prescribing confidence

CNS growth fuels uptake — 2024 revenue 1.09B; LAI market 8%

Alkermes Stars: Lybalvi driving rapid uptake in schizophrenia/bipolar since Dec 2021 approval; 2024 Alkermes revenue ~$1.09B with CNS growth engine. Aristada LAI in an ~8% CAGR LAI market (2024–28), holding ~15–20% specialty-clinic share and reducing relapse 30–40%; adherence baseline ~50%. Prior-auth and hub scale are key to converting access wins into sustained share.

| Metric | Value (2024) |

|---|---|

| Alkermes revenue | $1.09B |

| LAI market CAGR (2024–28) | ~8% |

| Aristada share | 15–20% |

| Relapse reduction | 30–40% |

| Adherence baseline | ~50% |

What is included in the product

BCG Matrix review of Alkermes products: Stars, Cash Cows, Question Marks, Dogs with investment and divestment guidance.

One-page Alkermes BCG Matrix that maps units into quadrants to cut analysis time and simplify exec decisions.

Cash Cows

Vivitrol

Vivitrol sits in a mature MAT market estimated at >$2.5B in 2024 and delivers roughly $400M in annual revenue, reflecting durable brand recognition and steady demand across alcohol and opioid dependence indications. Promotion is efficient and distribution channels are well-worn, producing reliable cash flow that funds Alkermes’ pipeline and field force. Focus on optimizing manufacturing throughput and keeping patient churn below industry levels to sustain margins.

Vumerity royalties

Vumerity (diroximel fumarate), FDA-approved in 2019, generates a royalty stream for Alkermes that delivers predictable, high-margin cash with minimal operating burden and little promotional spend. This royalty acts as dependable ballast on the P&L, supporting R&D and debt servicing. Management must protect the license and monitor generic entry and patent expiry timelines closely to sustain cash flow.

Aristada base business

As of 2024 Aristada base business delivers recurring monthly and multi‑month injections across core accounts, producing predictable inventory turns and steady clinic throughput.

Incremental investments in field support and patient access remain modest relative to output, preserving healthy per‑unit economics through 2024.

Gross margins strengthen with scale, so Alkermes continues to milk Aristada while selectively expanding high‑yield sites in 2024.

Established provider networks

Established provider networks drive repeatable, efficient detailing to long-standing psych prescribers, lowering cost per script and converting clinical engagement into steady cash flow; maintaining cadence without overspending preserves margin. In 2024 these networks remained Alkermes’ operational cash cows, enabling predictable prescription refill economics and faster cash conversion cycles.

- Repeatable detailing

- Lower cost per script

- Predictable cash conversion

- Maintain cadence, cap spend

Manufacturing know-how

Manufacturing know-how at Alkermes drove 2024 margin stability as process yields and tech-transfer skills cut COGS by an estimated 5–8% and stabilized supply across sites; small capex tweaks in a mature footprint lifted gross margins by roughly 200–300 bps. Line uptime targets >95% and scrap <1% keep this cash generator humming behind the curtain.

- COGS reduction: 5–8% (2024)

- Margin lift: ~200–300 bps from small capex

- Line uptime: >95%

- Scrap: <1%

Steady cash: $400M, royalties, recurring injections, +200–300bps

Vivitrol: $400M revenue in a >$2.5B MAT market (2024), steady cash flow; Vumerity: high‑margin royalty stream with minimal opex; Aristada: recurring injections driving predictable clinic throughput; manufacturing efficiency cut COGS 5–8% and lifted gross margins ~200–300 bps in 2024.

| Asset | 2024 metric | Role |

|---|---|---|

| Vivitrol | $400M | Primary cash cow |

| Vumerity | Royalty stream | Low‑cost cash |

| Aristada | Recurring injections | Stable cash |

| Manufacturing | COGS -5–8% | Margin support |

What You’re Viewing Is Included

Alkermes BCG Matrix

The Alkermes BCG Matrix you're previewing here is the exact file you'll receive after purchase — no watermarks, no placeholders, just the finished, analysis-ready report. It's built for strategic clarity and formatted for immediate use: edit, print, or present straight away. One purchase, one download, no surprises.