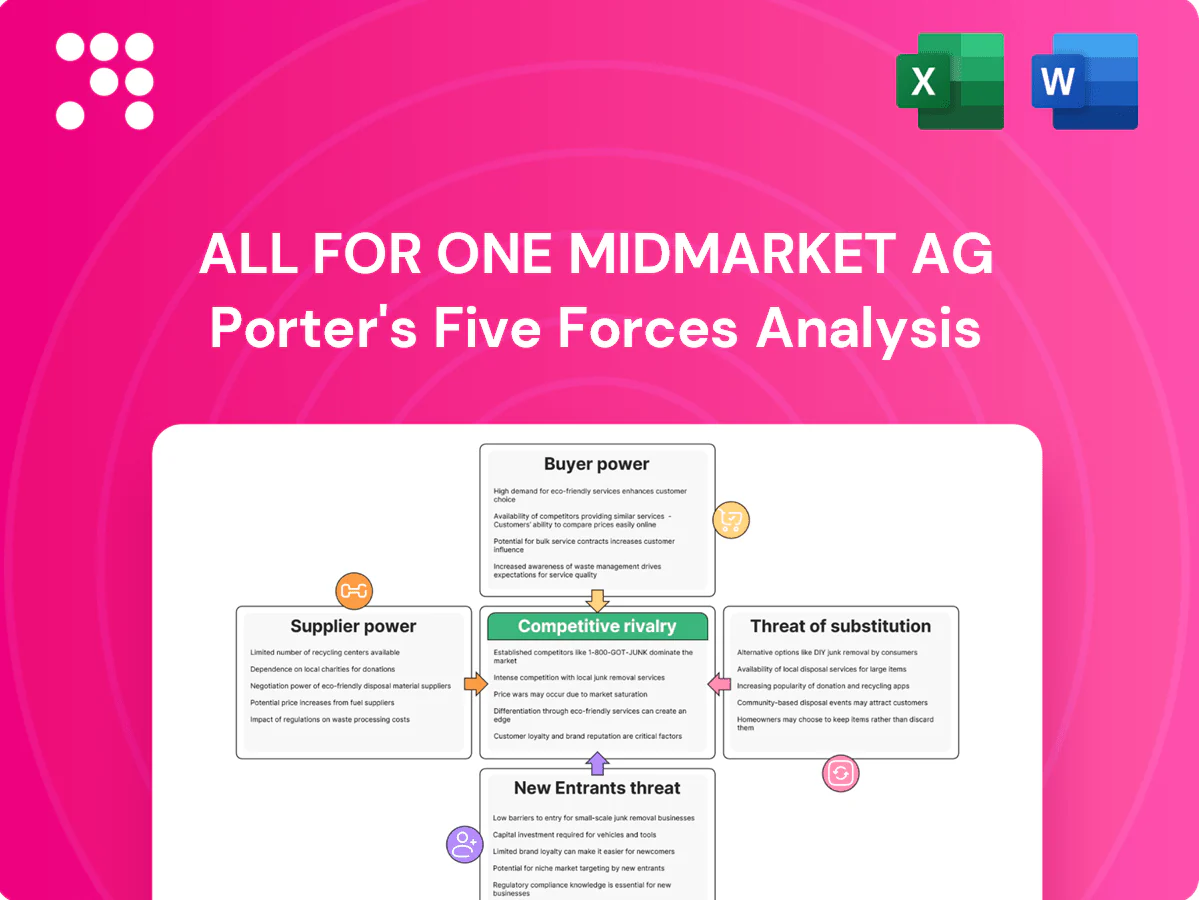

All for One Midmarket AG Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

All for One Midmarket AG faces moderate buyer power, strong supplier specialization, and intense rivalry across midmarket ERP and IT services, with technological shifts raising substitute risks. Regulatory and scale barriers temper new entrants but industry consolidation increases competitive pressure. Unlock the full Porter's Five Forces Analysis to explore All for One Midmarket AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Core tech vendors' leverage

All for One depends on SAP, Microsoft and IBM for core platforms, licenses and roadmap access; Microsoft reported FY2024 revenue of $211.9B and IBM $60.5B, underscoring their market leverage. These vendors can alter partner margins, certification rules and pricing, directly squeezing project economics. Dependency raises exposure to program tiering and incentive realignments seen in 2023–24 partner updates, and few viable alternatives for Tier‑1 stacks amplify supplier power.

Hyperscaler and cloud terms

Azure, AWS and GCP collectively control roughly 67-70% of global cloud IaaS/PaaS (2024 estimates), letting hyperscalers set consumption pricing, reserved-capacity discounts (up to ~70%) and egress fees that can shave 1–5pp off managed-services margins. Changes to egress or committed-use discounts and marketplace rules shift deal economics; partner-led cloud credits and resale policies further shape pricing. Consolidation among top providers concentrates supplier power.

Talent and subcontractor scarcity

Certified SAP and Microsoft engineers remain scarce, driving upward wage pressure and higher project margins for suppliers. Specialist subcontractors command premium rates on peak projects, especially for cloud and S/4HANA migrations. Visa, remote-work rules and compliance restrict alternative talent pools, while concentration of experts in urban hubs amplifies bargaining power of key individuals.

Tooling, IP, and security vendors

Monitoring, cybersecurity, and DevOps tool vendors are highly sticky once embedded, with 2024 surveys showing over 60% of enterprises citing tool lock-in as a procurement risk; per-user or per-host price escalators (commonly 5–10% annually) drive operating-cost creep. Switching carries real service-disruption and retraining burdens, while bundled suites create soft lock-in that weakens negotiation leverage.

- Stickiness: >60% firms cite lock-in (2024)

- Price pressure: 5–10% annual escalators

- Switch cost: disruption + retraining

- Bundling: reduces bargaining flexibility

Data center and colocation dependencies

For hybrid setups, colocation and network providers control critical capacity and connectivity SLAs, and the global colocation market reached about $70 billion in 2024, reinforcing supplier pricing power. Power and rack price volatility — rack rates rose roughly 10% in 2023–24 — compress hosting margins. Data residency rules in EU/APAC force onsite choices for an estimated 38% of enterprises, limiting switching, and long-term contracts can lock in unfavorable terms during demand spikes.

- Capacity concentration: high

- Rack pricing volatility: ≈10% (2023–24)

- Market size 2024: ~$70B

- Compliance-driven lock-in: ≈38% of enterprises

Hyperscaler dominance, talent scarcity and rising colocation costs squeeze margins for IT integrators

All for One faces high supplier power from Tier‑1 software/hyperscalers (Microsoft FY2024 revenue $211.9B; IBM $60.5B) and cloud share ~67–70% (2024), squeezing margins via pricing, incentives and egress fees. Talent scarcity and tool lock‑in (≥60% firms, 2024) raise costs; colocation market ~$70B (2024) and ~10% rack price rise further constrain flexibility.

| Metric | 2024 Value |

|---|---|

| Microsoft rev | $211.9B |

| IBM rev | $60.5B |

| Hyperscaler share | 67–70% |

| Tool lock‑in | >=60% |

| Colocation market | ~$70B |

| Rack price change | ~10% |

What is included in the product

Tailored exclusively for All for One Midmarket AG, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threats from entrants and substitutes, and highlights disruptive forces and market dynamics that influence pricing, profitability, and strategic positioning.

A concise one-sheet Porter's Five Forces for All for One Midmarket AG that translates competitive pressure into actionable priorities—editable radar chart, copy-ready layout for decks, and no-complex tools so teams instantly spot and mitigate strategic threats.

Customers Bargaining Power

SME price sensitivity

Midmarket clients for All for One Midmarket AG are highly price-sensitive: EU SMEs, which represent about 99.8% of firms and roughly 66% of employment, routinely compare proposals and demand fixed-price engagements and transparent T&M rates. Economic uncertainty in 2024 increases discounting and phased rollouts, while procurement often anchors bids to prior projects or market benchmarks.

High switching costs

Deep ERP customizations and AMS integrations at All for One create strong technical lock-in: ERP migrations typically take 12–18 months and often run into multi-million euro projects, deterring switches and moderating buyer power after go-live. Buyers still exploit renewal windows to renegotiate pricing, and multi-year contracts can be reopened around performance issues or SLA breaches.

Multi-sourcing and tenders

In 2024 clients run competitive RFPs across local boutiques and global SIs, deliberately splitting work between strategy, build and run to keep vendors competing. Framework agreements increasingly standardize rates and terms, compressing fee variability. Benchmarking clauses and periodic reviews — often annual — sustain continuous price pressure on All for One Midmarket AG. This multi-sourcing dynamic elevates buyer leverage and tightens margins.

Outcome-based expectations

Buyers now insist on SLAs, KPIs and outcome commitments, pushing All for One Midmarket AG toward risk-sharing contracts with milestone-based payments and penalties; market surveys in 2024 indicated outcome-based terms in roughly 60% of midmarket ERP engagements and accelerating demand for faster time-to-value via packaged accelerators.

- SLAs/KPIs required

- Risk-sharing: milestones & penalties

- References/templates prerequisite

- Time-to-value pressure: accelerators

Platform consolidation choices

Platform consolidation choices let customers shift scope between vendor and partner when adopting SAP RISE, Microsoft Dynamics, or mixed estates; SAP RISE had over 2,000 customers by 2023 while Azure held ~23% IaaS market share in 2023, increasing partner-vendor competition. Direct vendor services and marketplace procurement (AWS/Azure marketplaces) simplify switching and price transparency; standardized cloud offerings make comparisons easier across quotes.

- Vendor share: Azure ~23% (2023)

- SAP RISE: >2,000 customers (2023)

- Marketplaces: faster procurement/switching

- Standardized cloud = higher comparability

Midmarket ERP renewals drive outcome-based renegotiations, compressing margins

Midmarket buyers are price-sensitive and benchmark aggressively (EU SMEs = 99.8% of firms; ~66% employment). ERP lock-in (12–18 months; multi‑€m) reduces churn but renewals spark renegotiation; ~60% of 2024 ERP deals include outcome-based terms. Multi-sourcing, cloud marketplaces and SAP RISE/Azure adoption raise comparability and compress margins.

| Metric | Value | Year |

|---|---|---|

| EU SMEs (% firms) | 99.8% | 2024 |

| Employment share | ~66% | 2024 |

| Outcome-based deals | ~60% | 2024 |

| ERP migration time | 12–18 months | typical |

Preview Before You Purchase

All for One Midmarket AG Porter's Five Forces Analysis

This Porter's Five Forces analysis of All for One Midmarket AG provides a thorough assessment of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products, with practical implications for strategy. This preview is the exact, fully formatted document you will receive immediately after purchase. Use it as-is for decision-making and presentations.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

All for One Midmarket AG faces moderate buyer power, strong supplier specialization, and intense rivalry across midmarket ERP and IT services, with technological shifts raising substitute risks. Regulatory and scale barriers temper new entrants but industry consolidation increases competitive pressure. Unlock the full Porter's Five Forces Analysis to explore All for One Midmarket AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Core tech vendors' leverage

All for One depends on SAP, Microsoft and IBM for core platforms, licenses and roadmap access; Microsoft reported FY2024 revenue of $211.9B and IBM $60.5B, underscoring their market leverage. These vendors can alter partner margins, certification rules and pricing, directly squeezing project economics. Dependency raises exposure to program tiering and incentive realignments seen in 2023–24 partner updates, and few viable alternatives for Tier‑1 stacks amplify supplier power.

Hyperscaler and cloud terms

Azure, AWS and GCP collectively control roughly 67-70% of global cloud IaaS/PaaS (2024 estimates), letting hyperscalers set consumption pricing, reserved-capacity discounts (up to ~70%) and egress fees that can shave 1–5pp off managed-services margins. Changes to egress or committed-use discounts and marketplace rules shift deal economics; partner-led cloud credits and resale policies further shape pricing. Consolidation among top providers concentrates supplier power.

Talent and subcontractor scarcity

Certified SAP and Microsoft engineers remain scarce, driving upward wage pressure and higher project margins for suppliers. Specialist subcontractors command premium rates on peak projects, especially for cloud and S/4HANA migrations. Visa, remote-work rules and compliance restrict alternative talent pools, while concentration of experts in urban hubs amplifies bargaining power of key individuals.

Tooling, IP, and security vendors

Monitoring, cybersecurity, and DevOps tool vendors are highly sticky once embedded, with 2024 surveys showing over 60% of enterprises citing tool lock-in as a procurement risk; per-user or per-host price escalators (commonly 5–10% annually) drive operating-cost creep. Switching carries real service-disruption and retraining burdens, while bundled suites create soft lock-in that weakens negotiation leverage.

- Stickiness: >60% firms cite lock-in (2024)

- Price pressure: 5–10% annual escalators

- Switch cost: disruption + retraining

- Bundling: reduces bargaining flexibility

Data center and colocation dependencies

For hybrid setups, colocation and network providers control critical capacity and connectivity SLAs, and the global colocation market reached about $70 billion in 2024, reinforcing supplier pricing power. Power and rack price volatility — rack rates rose roughly 10% in 2023–24 — compress hosting margins. Data residency rules in EU/APAC force onsite choices for an estimated 38% of enterprises, limiting switching, and long-term contracts can lock in unfavorable terms during demand spikes.

- Capacity concentration: high

- Rack pricing volatility: ≈10% (2023–24)

- Market size 2024: ~$70B

- Compliance-driven lock-in: ≈38% of enterprises

Hyperscaler dominance, talent scarcity and rising colocation costs squeeze margins for IT integrators

All for One faces high supplier power from Tier‑1 software/hyperscalers (Microsoft FY2024 revenue $211.9B; IBM $60.5B) and cloud share ~67–70% (2024), squeezing margins via pricing, incentives and egress fees. Talent scarcity and tool lock‑in (≥60% firms, 2024) raise costs; colocation market ~$70B (2024) and ~10% rack price rise further constrain flexibility.

| Metric | 2024 Value |

|---|---|

| Microsoft rev | $211.9B |

| IBM rev | $60.5B |

| Hyperscaler share | 67–70% |

| Tool lock‑in | >=60% |

| Colocation market | ~$70B |

| Rack price change | ~10% |

What is included in the product

Tailored exclusively for All for One Midmarket AG, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threats from entrants and substitutes, and highlights disruptive forces and market dynamics that influence pricing, profitability, and strategic positioning.

A concise one-sheet Porter's Five Forces for All for One Midmarket AG that translates competitive pressure into actionable priorities—editable radar chart, copy-ready layout for decks, and no-complex tools so teams instantly spot and mitigate strategic threats.

Customers Bargaining Power

SME price sensitivity

Midmarket clients for All for One Midmarket AG are highly price-sensitive: EU SMEs, which represent about 99.8% of firms and roughly 66% of employment, routinely compare proposals and demand fixed-price engagements and transparent T&M rates. Economic uncertainty in 2024 increases discounting and phased rollouts, while procurement often anchors bids to prior projects or market benchmarks.

High switching costs

Deep ERP customizations and AMS integrations at All for One create strong technical lock-in: ERP migrations typically take 12–18 months and often run into multi-million euro projects, deterring switches and moderating buyer power after go-live. Buyers still exploit renewal windows to renegotiate pricing, and multi-year contracts can be reopened around performance issues or SLA breaches.

Multi-sourcing and tenders

In 2024 clients run competitive RFPs across local boutiques and global SIs, deliberately splitting work between strategy, build and run to keep vendors competing. Framework agreements increasingly standardize rates and terms, compressing fee variability. Benchmarking clauses and periodic reviews — often annual — sustain continuous price pressure on All for One Midmarket AG. This multi-sourcing dynamic elevates buyer leverage and tightens margins.

Outcome-based expectations

Buyers now insist on SLAs, KPIs and outcome commitments, pushing All for One Midmarket AG toward risk-sharing contracts with milestone-based payments and penalties; market surveys in 2024 indicated outcome-based terms in roughly 60% of midmarket ERP engagements and accelerating demand for faster time-to-value via packaged accelerators.

- SLAs/KPIs required

- Risk-sharing: milestones & penalties

- References/templates prerequisite

- Time-to-value pressure: accelerators

Platform consolidation choices

Platform consolidation choices let customers shift scope between vendor and partner when adopting SAP RISE, Microsoft Dynamics, or mixed estates; SAP RISE had over 2,000 customers by 2023 while Azure held ~23% IaaS market share in 2023, increasing partner-vendor competition. Direct vendor services and marketplace procurement (AWS/Azure marketplaces) simplify switching and price transparency; standardized cloud offerings make comparisons easier across quotes.

- Vendor share: Azure ~23% (2023)

- SAP RISE: >2,000 customers (2023)

- Marketplaces: faster procurement/switching

- Standardized cloud = higher comparability

Midmarket ERP renewals drive outcome-based renegotiations, compressing margins

Midmarket buyers are price-sensitive and benchmark aggressively (EU SMEs = 99.8% of firms; ~66% employment). ERP lock-in (12–18 months; multi‑€m) reduces churn but renewals spark renegotiation; ~60% of 2024 ERP deals include outcome-based terms. Multi-sourcing, cloud marketplaces and SAP RISE/Azure adoption raise comparability and compress margins.

| Metric | Value | Year |

|---|---|---|

| EU SMEs (% firms) | 99.8% | 2024 |

| Employment share | ~66% | 2024 |

| Outcome-based deals | ~60% | 2024 |

| ERP migration time | 12–18 months | typical |

Preview Before You Purchase

All for One Midmarket AG Porter's Five Forces Analysis

This Porter's Five Forces analysis of All for One Midmarket AG provides a thorough assessment of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products, with practical implications for strategy. This preview is the exact, fully formatted document you will receive immediately after purchase. Use it as-is for decision-making and presentations.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

All for One Midmarket AG faces moderate buyer power, strong supplier specialization, and intense rivalry across midmarket ERP and IT services, with technological shifts raising substitute risks. Regulatory and scale barriers temper new entrants but industry consolidation increases competitive pressure. Unlock the full Porter's Five Forces Analysis to explore All for One Midmarket AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Core tech vendors' leverage

All for One depends on SAP, Microsoft and IBM for core platforms, licenses and roadmap access; Microsoft reported FY2024 revenue of $211.9B and IBM $60.5B, underscoring their market leverage. These vendors can alter partner margins, certification rules and pricing, directly squeezing project economics. Dependency raises exposure to program tiering and incentive realignments seen in 2023–24 partner updates, and few viable alternatives for Tier‑1 stacks amplify supplier power.

Hyperscaler and cloud terms

Azure, AWS and GCP collectively control roughly 67-70% of global cloud IaaS/PaaS (2024 estimates), letting hyperscalers set consumption pricing, reserved-capacity discounts (up to ~70%) and egress fees that can shave 1–5pp off managed-services margins. Changes to egress or committed-use discounts and marketplace rules shift deal economics; partner-led cloud credits and resale policies further shape pricing. Consolidation among top providers concentrates supplier power.

Talent and subcontractor scarcity

Certified SAP and Microsoft engineers remain scarce, driving upward wage pressure and higher project margins for suppliers. Specialist subcontractors command premium rates on peak projects, especially for cloud and S/4HANA migrations. Visa, remote-work rules and compliance restrict alternative talent pools, while concentration of experts in urban hubs amplifies bargaining power of key individuals.

Tooling, IP, and security vendors

Monitoring, cybersecurity, and DevOps tool vendors are highly sticky once embedded, with 2024 surveys showing over 60% of enterprises citing tool lock-in as a procurement risk; per-user or per-host price escalators (commonly 5–10% annually) drive operating-cost creep. Switching carries real service-disruption and retraining burdens, while bundled suites create soft lock-in that weakens negotiation leverage.

- Stickiness: >60% firms cite lock-in (2024)

- Price pressure: 5–10% annual escalators

- Switch cost: disruption + retraining

- Bundling: reduces bargaining flexibility

Data center and colocation dependencies

For hybrid setups, colocation and network providers control critical capacity and connectivity SLAs, and the global colocation market reached about $70 billion in 2024, reinforcing supplier pricing power. Power and rack price volatility — rack rates rose roughly 10% in 2023–24 — compress hosting margins. Data residency rules in EU/APAC force onsite choices for an estimated 38% of enterprises, limiting switching, and long-term contracts can lock in unfavorable terms during demand spikes.

- Capacity concentration: high

- Rack pricing volatility: ≈10% (2023–24)

- Market size 2024: ~$70B

- Compliance-driven lock-in: ≈38% of enterprises

Hyperscaler dominance, talent scarcity and rising colocation costs squeeze margins for IT integrators

All for One faces high supplier power from Tier‑1 software/hyperscalers (Microsoft FY2024 revenue $211.9B; IBM $60.5B) and cloud share ~67–70% (2024), squeezing margins via pricing, incentives and egress fees. Talent scarcity and tool lock‑in (≥60% firms, 2024) raise costs; colocation market ~$70B (2024) and ~10% rack price rise further constrain flexibility.

| Metric | 2024 Value |

|---|---|

| Microsoft rev | $211.9B |

| IBM rev | $60.5B |

| Hyperscaler share | 67–70% |

| Tool lock‑in | >=60% |

| Colocation market | ~$70B |

| Rack price change | ~10% |

What is included in the product

Tailored exclusively for All for One Midmarket AG, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, threats from entrants and substitutes, and highlights disruptive forces and market dynamics that influence pricing, profitability, and strategic positioning.

A concise one-sheet Porter's Five Forces for All for One Midmarket AG that translates competitive pressure into actionable priorities—editable radar chart, copy-ready layout for decks, and no-complex tools so teams instantly spot and mitigate strategic threats.

Customers Bargaining Power

SME price sensitivity

Midmarket clients for All for One Midmarket AG are highly price-sensitive: EU SMEs, which represent about 99.8% of firms and roughly 66% of employment, routinely compare proposals and demand fixed-price engagements and transparent T&M rates. Economic uncertainty in 2024 increases discounting and phased rollouts, while procurement often anchors bids to prior projects or market benchmarks.

High switching costs

Deep ERP customizations and AMS integrations at All for One create strong technical lock-in: ERP migrations typically take 12–18 months and often run into multi-million euro projects, deterring switches and moderating buyer power after go-live. Buyers still exploit renewal windows to renegotiate pricing, and multi-year contracts can be reopened around performance issues or SLA breaches.

Multi-sourcing and tenders

In 2024 clients run competitive RFPs across local boutiques and global SIs, deliberately splitting work between strategy, build and run to keep vendors competing. Framework agreements increasingly standardize rates and terms, compressing fee variability. Benchmarking clauses and periodic reviews — often annual — sustain continuous price pressure on All for One Midmarket AG. This multi-sourcing dynamic elevates buyer leverage and tightens margins.

Outcome-based expectations

Buyers now insist on SLAs, KPIs and outcome commitments, pushing All for One Midmarket AG toward risk-sharing contracts with milestone-based payments and penalties; market surveys in 2024 indicated outcome-based terms in roughly 60% of midmarket ERP engagements and accelerating demand for faster time-to-value via packaged accelerators.

- SLAs/KPIs required

- Risk-sharing: milestones & penalties

- References/templates prerequisite

- Time-to-value pressure: accelerators

Platform consolidation choices

Platform consolidation choices let customers shift scope between vendor and partner when adopting SAP RISE, Microsoft Dynamics, or mixed estates; SAP RISE had over 2,000 customers by 2023 while Azure held ~23% IaaS market share in 2023, increasing partner-vendor competition. Direct vendor services and marketplace procurement (AWS/Azure marketplaces) simplify switching and price transparency; standardized cloud offerings make comparisons easier across quotes.

- Vendor share: Azure ~23% (2023)

- SAP RISE: >2,000 customers (2023)

- Marketplaces: faster procurement/switching

- Standardized cloud = higher comparability

Midmarket ERP renewals drive outcome-based renegotiations, compressing margins

Midmarket buyers are price-sensitive and benchmark aggressively (EU SMEs = 99.8% of firms; ~66% employment). ERP lock-in (12–18 months; multi‑€m) reduces churn but renewals spark renegotiation; ~60% of 2024 ERP deals include outcome-based terms. Multi-sourcing, cloud marketplaces and SAP RISE/Azure adoption raise comparability and compress margins.

| Metric | Value | Year |

|---|---|---|

| EU SMEs (% firms) | 99.8% | 2024 |

| Employment share | ~66% | 2024 |

| Outcome-based deals | ~60% | 2024 |

| ERP migration time | 12–18 months | typical |

Preview Before You Purchase

All for One Midmarket AG Porter's Five Forces Analysis

This Porter's Five Forces analysis of All for One Midmarket AG provides a thorough assessment of competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products, with practical implications for strategy. This preview is the exact, fully formatted document you will receive immediately after purchase. Use it as-is for decision-making and presentations.