Allegion Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

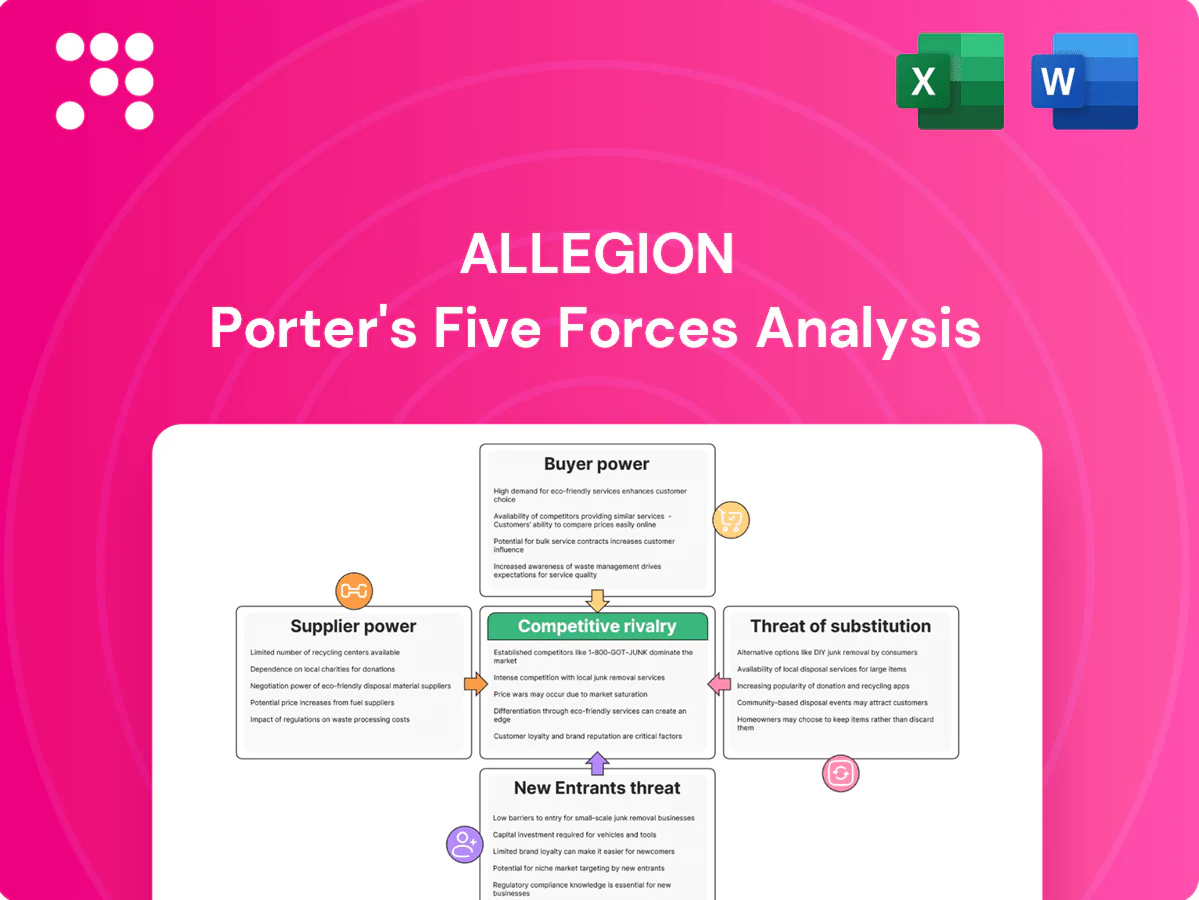

Allegion faces moderate supplier leverage, steady buyer bargaining, and niche threat from substitutes while regulatory and new-entrant barriers shape its margins; this snapshot highlights competitive intensity and strategic levers. Want deeper, force-by-force ratings, visuals and actionable implications? Unlock the full Porter’s Five Forces Analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Specialized component reliance

Allegion (NYSE: ALLE) relies on precision electromechanical actuators, semiconductors and high-grade alloys for safety-critical locks, where a limited pool of qualified suppliers raises switching costs and leads to longer lead times. Supplier concentration can give niche vendors pricing and allocation leverage, squeezing margins and production schedules. Dual-sourcing and design standardization reduce exposure but do not fully eliminate supply risk.

Commodity metals and input volatility

Steel, zinc, brass, and aluminum price swings directly raise costs for locks, closers and exit devices. While hedging and scale purchasing blunt volatility, 2024 saw LME copper up ~22%, aluminum +13%, zinc +18% and U.S. hot‑rolled coil swings near ±20%, limiting offset. Suppliers have passed through surcharges in tight cycles; value engineering and long‑term contracts dampen but do not eliminate exposure.

Electronics and firmware supply constraints

Smart locks and access systems tie Allegion to cyclical semiconductor supply, with allocation events in 2021–23 producing lead times reported up to 52 weeks and prioritizing larger consumer and auto buyers over industrials. Firmware security and certification add 3–9 months to supplier qualification, limiting rapid substitution. Strategic partnerships and buffer inventory mitigate but do not eliminate supplier bargaining power.

Logistics, regionalization, and compliance

Global supply chains for Allegion face shipping costs, tariffs (eg, US steel tariffs of 25%), and regional compliance regimes (UL, ANSI/BHMA, CE), strengthening suppliers with localized certified capacity. Reshoring and nearshoring diversify risk but typically raise unit costs and reduce scale advantages. Increasing supplier ESG and cybersecurity requirements further narrow the pool of qualified vendors in 2024.

- Localized certified suppliers = higher negotiating power

- 25% steel tariffs raise input cost pressure

- Reshoring/nearshoring tradeoff: lower risk, higher unit cost

- ESG/cyber rules shrink qualified supplier pool

Tooling, molds, and co-development lock-in

Custom tooling and co-engineered parts create meaningful switching frictions for Allegion, where legacy-platform lock‑in is amplified by the need to recover NRE and re‑qualify safety products; Allegion reported roughly $3.0B in net sales in 2023, making legacy platform continuity financially material to margins. Industry cases show NRE often exceeds $1M and requalification can span 6–18 months, elevating supplier leverage on older platforms.

- Tooling lock-in raises supplier power

- NRE > $1M; requalification 6–18 months

- Embedded parts boost legacy supplier leverage

- Modular design and common parts libraries preserve optionality

Supplier concentration, 2024 metals +22%/+13%/+18% and semis lead times up to 52w

Allegion depends on specialized electromechanical and alloy suppliers, creating high switching costs and niche vendor leverage. 2024 commodity swings (LME copper +22%, aluminum +13%, zinc +18%, US HRC ±20%) and 25% US steel tariffs increased input pressure. Semiconductor allocation (lead times up to 52 weeks in 2021–23) and NRE/requalification (>$1M, 6–18 months) sustain supplier bargaining power.

| Metric | 2023–24 Data |

|---|---|

| Allegion net sales | $3.0B (2023) |

| Copper/Al/ZN moves (2024) | +22% / +13% / +18% |

| US HRC volatility | ±20% |

| Lead times (semis) | up to 52 weeks |

| NRE / requal | >$1M / 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Allegion uncovering competitive drivers, customer influence, supplier bargaining power, and barriers to entry within the security and access solutions market. Identifies disruptive substitutes, emerging threats, and strategic levers to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for Allegion that instantly highlights competitive pressures and relieves strategic uncertainty for faster decisions. Customize pressure levels, swap in your own data, and drop the clean layout straight into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated channels and large projects

Distributors, large contractors and institutional buyers aggregate volume and negotiate pricing against Allegion’s scale; Allegion reported roughly $3.0 billion in 2024 revenue, concentrating bargaining leverage. Multi-site rollouts and specification packages often drive competitive tendering and pressure margins through standardized SKUs. Buyers solicit cross-brand bids and secure volume rebates and service SLAs to retain accounts and reduce total cost of ownership.

Specification-driven demand

Architects and security consultants often spec-in Allegion products to meet codes and standards, creating design-phase lock-in that makes mid-project switching costly and reduces buyer leverage. Buyers retain influence by shaping specs early to allow approved alternatives, but once a strong spec position is established Allegion regains pricing and approval power. Specification control thus materially centralizes bargaining power with Allegion.

Total cost of ownership focus

Commercial customers prioritize total cost of ownership—lifecycle costs, reliability, and downtime—over unit price; Allegion reported roughly $3.8 billion in 2024 sales, underscoring scale in service and spare parts. High durability and bundled support reduce perceived switching gains, yet buyers with internal maintenance still negotiate parts pricing. Warranty length and rapid service response remain decisive levers in procurement decisions.

Interoperability and open standards

Enterprise buyers in 2024 increasingly prioritize open protocols and API-first access control; if competitors plug into existing IT stacks more easily, buyer leverage grows and can pressure pricing and service terms. Certified interoperability and clear software roadmaps with backward compatibility neutralize this power by reducing switching risk and protecting recurring revenue.

- Integration-first buying: raises buyer power

- Certified interoperability: reduces switching

- Roadmaps/backward compatibility: key bargaining chips

Residential price sensitivity

Consumers compare smart locks across retail and e-commerce, raising price transparency; average retail prices in 2024 clustered around $120–$250, compressing margins at value tiers. Promotions and feature parity heighten bargaining power in low-to-mid segments, while brand trust and app experience can command a modest premium of roughly 10–15%. Reviews and ecosystem fit (Alexa/Google/Apple) frequently tip final decisions.

- Price transparency: cross-channel comparisons

- Promo pressure: low-mid tier bargaining

- Brand/app premium: ~10–15%

- Ecosystem/reviews: decisive purchase factors

Scale vs buyers: distributor rebates compress margins; smart-lock retail transparency

Large distributors and enterprise buyers exert strong price and rebate pressure against Allegion’s scale (roughly $3.0 billion revenue in 2024), while spec-driven projects and certified interoperability reduce switching and boost Allegion’s negotiating position. Retail smart-lock price transparency compresses margins at $120–$250 average, though brand/app can command ~10–15% premium.

| Metric | 2024 Value |

|---|---|

| Allegion revenue | $3.0 billion |

| Smart-lock avg retail | $120–$250 |

| Brand/app premium | ~10–15% |

Full Version Awaits

Allegion Porter's Five Forces Analysis

This preview shows the exact Allegion Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the complete deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Allegion faces moderate supplier leverage, steady buyer bargaining, and niche threat from substitutes while regulatory and new-entrant barriers shape its margins; this snapshot highlights competitive intensity and strategic levers. Want deeper, force-by-force ratings, visuals and actionable implications? Unlock the full Porter’s Five Forces Analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Specialized component reliance

Allegion (NYSE: ALLE) relies on precision electromechanical actuators, semiconductors and high-grade alloys for safety-critical locks, where a limited pool of qualified suppliers raises switching costs and leads to longer lead times. Supplier concentration can give niche vendors pricing and allocation leverage, squeezing margins and production schedules. Dual-sourcing and design standardization reduce exposure but do not fully eliminate supply risk.

Commodity metals and input volatility

Steel, zinc, brass, and aluminum price swings directly raise costs for locks, closers and exit devices. While hedging and scale purchasing blunt volatility, 2024 saw LME copper up ~22%, aluminum +13%, zinc +18% and U.S. hot‑rolled coil swings near ±20%, limiting offset. Suppliers have passed through surcharges in tight cycles; value engineering and long‑term contracts dampen but do not eliminate exposure.

Electronics and firmware supply constraints

Smart locks and access systems tie Allegion to cyclical semiconductor supply, with allocation events in 2021–23 producing lead times reported up to 52 weeks and prioritizing larger consumer and auto buyers over industrials. Firmware security and certification add 3–9 months to supplier qualification, limiting rapid substitution. Strategic partnerships and buffer inventory mitigate but do not eliminate supplier bargaining power.

Logistics, regionalization, and compliance

Global supply chains for Allegion face shipping costs, tariffs (eg, US steel tariffs of 25%), and regional compliance regimes (UL, ANSI/BHMA, CE), strengthening suppliers with localized certified capacity. Reshoring and nearshoring diversify risk but typically raise unit costs and reduce scale advantages. Increasing supplier ESG and cybersecurity requirements further narrow the pool of qualified vendors in 2024.

- Localized certified suppliers = higher negotiating power

- 25% steel tariffs raise input cost pressure

- Reshoring/nearshoring tradeoff: lower risk, higher unit cost

- ESG/cyber rules shrink qualified supplier pool

Tooling, molds, and co-development lock-in

Custom tooling and co-engineered parts create meaningful switching frictions for Allegion, where legacy-platform lock‑in is amplified by the need to recover NRE and re‑qualify safety products; Allegion reported roughly $3.0B in net sales in 2023, making legacy platform continuity financially material to margins. Industry cases show NRE often exceeds $1M and requalification can span 6–18 months, elevating supplier leverage on older platforms.

- Tooling lock-in raises supplier power

- NRE > $1M; requalification 6–18 months

- Embedded parts boost legacy supplier leverage

- Modular design and common parts libraries preserve optionality

Supplier concentration, 2024 metals +22%/+13%/+18% and semis lead times up to 52w

Allegion depends on specialized electromechanical and alloy suppliers, creating high switching costs and niche vendor leverage. 2024 commodity swings (LME copper +22%, aluminum +13%, zinc +18%, US HRC ±20%) and 25% US steel tariffs increased input pressure. Semiconductor allocation (lead times up to 52 weeks in 2021–23) and NRE/requalification (>$1M, 6–18 months) sustain supplier bargaining power.

| Metric | 2023–24 Data |

|---|---|

| Allegion net sales | $3.0B (2023) |

| Copper/Al/ZN moves (2024) | +22% / +13% / +18% |

| US HRC volatility | ±20% |

| Lead times (semis) | up to 52 weeks |

| NRE / requal | >$1M / 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Allegion uncovering competitive drivers, customer influence, supplier bargaining power, and barriers to entry within the security and access solutions market. Identifies disruptive substitutes, emerging threats, and strategic levers to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for Allegion that instantly highlights competitive pressures and relieves strategic uncertainty for faster decisions. Customize pressure levels, swap in your own data, and drop the clean layout straight into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated channels and large projects

Distributors, large contractors and institutional buyers aggregate volume and negotiate pricing against Allegion’s scale; Allegion reported roughly $3.0 billion in 2024 revenue, concentrating bargaining leverage. Multi-site rollouts and specification packages often drive competitive tendering and pressure margins through standardized SKUs. Buyers solicit cross-brand bids and secure volume rebates and service SLAs to retain accounts and reduce total cost of ownership.

Specification-driven demand

Architects and security consultants often spec-in Allegion products to meet codes and standards, creating design-phase lock-in that makes mid-project switching costly and reduces buyer leverage. Buyers retain influence by shaping specs early to allow approved alternatives, but once a strong spec position is established Allegion regains pricing and approval power. Specification control thus materially centralizes bargaining power with Allegion.

Total cost of ownership focus

Commercial customers prioritize total cost of ownership—lifecycle costs, reliability, and downtime—over unit price; Allegion reported roughly $3.8 billion in 2024 sales, underscoring scale in service and spare parts. High durability and bundled support reduce perceived switching gains, yet buyers with internal maintenance still negotiate parts pricing. Warranty length and rapid service response remain decisive levers in procurement decisions.

Interoperability and open standards

Enterprise buyers in 2024 increasingly prioritize open protocols and API-first access control; if competitors plug into existing IT stacks more easily, buyer leverage grows and can pressure pricing and service terms. Certified interoperability and clear software roadmaps with backward compatibility neutralize this power by reducing switching risk and protecting recurring revenue.

- Integration-first buying: raises buyer power

- Certified interoperability: reduces switching

- Roadmaps/backward compatibility: key bargaining chips

Residential price sensitivity

Consumers compare smart locks across retail and e-commerce, raising price transparency; average retail prices in 2024 clustered around $120–$250, compressing margins at value tiers. Promotions and feature parity heighten bargaining power in low-to-mid segments, while brand trust and app experience can command a modest premium of roughly 10–15%. Reviews and ecosystem fit (Alexa/Google/Apple) frequently tip final decisions.

- Price transparency: cross-channel comparisons

- Promo pressure: low-mid tier bargaining

- Brand/app premium: ~10–15%

- Ecosystem/reviews: decisive purchase factors

Scale vs buyers: distributor rebates compress margins; smart-lock retail transparency

Large distributors and enterprise buyers exert strong price and rebate pressure against Allegion’s scale (roughly $3.0 billion revenue in 2024), while spec-driven projects and certified interoperability reduce switching and boost Allegion’s negotiating position. Retail smart-lock price transparency compresses margins at $120–$250 average, though brand/app can command ~10–15% premium.

| Metric | 2024 Value |

|---|---|

| Allegion revenue | $3.0 billion |

| Smart-lock avg retail | $120–$250 |

| Brand/app premium | ~10–15% |

Full Version Awaits

Allegion Porter's Five Forces Analysis

This preview shows the exact Allegion Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the complete deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Allegion faces moderate supplier leverage, steady buyer bargaining, and niche threat from substitutes while regulatory and new-entrant barriers shape its margins; this snapshot highlights competitive intensity and strategic levers. Want deeper, force-by-force ratings, visuals and actionable implications? Unlock the full Porter’s Five Forces Analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Specialized component reliance

Allegion (NYSE: ALLE) relies on precision electromechanical actuators, semiconductors and high-grade alloys for safety-critical locks, where a limited pool of qualified suppliers raises switching costs and leads to longer lead times. Supplier concentration can give niche vendors pricing and allocation leverage, squeezing margins and production schedules. Dual-sourcing and design standardization reduce exposure but do not fully eliminate supply risk.

Commodity metals and input volatility

Steel, zinc, brass, and aluminum price swings directly raise costs for locks, closers and exit devices. While hedging and scale purchasing blunt volatility, 2024 saw LME copper up ~22%, aluminum +13%, zinc +18% and U.S. hot‑rolled coil swings near ±20%, limiting offset. Suppliers have passed through surcharges in tight cycles; value engineering and long‑term contracts dampen but do not eliminate exposure.

Electronics and firmware supply constraints

Smart locks and access systems tie Allegion to cyclical semiconductor supply, with allocation events in 2021–23 producing lead times reported up to 52 weeks and prioritizing larger consumer and auto buyers over industrials. Firmware security and certification add 3–9 months to supplier qualification, limiting rapid substitution. Strategic partnerships and buffer inventory mitigate but do not eliminate supplier bargaining power.

Logistics, regionalization, and compliance

Global supply chains for Allegion face shipping costs, tariffs (eg, US steel tariffs of 25%), and regional compliance regimes (UL, ANSI/BHMA, CE), strengthening suppliers with localized certified capacity. Reshoring and nearshoring diversify risk but typically raise unit costs and reduce scale advantages. Increasing supplier ESG and cybersecurity requirements further narrow the pool of qualified vendors in 2024.

- Localized certified suppliers = higher negotiating power

- 25% steel tariffs raise input cost pressure

- Reshoring/nearshoring tradeoff: lower risk, higher unit cost

- ESG/cyber rules shrink qualified supplier pool

Tooling, molds, and co-development lock-in

Custom tooling and co-engineered parts create meaningful switching frictions for Allegion, where legacy-platform lock‑in is amplified by the need to recover NRE and re‑qualify safety products; Allegion reported roughly $3.0B in net sales in 2023, making legacy platform continuity financially material to margins. Industry cases show NRE often exceeds $1M and requalification can span 6–18 months, elevating supplier leverage on older platforms.

- Tooling lock-in raises supplier power

- NRE > $1M; requalification 6–18 months

- Embedded parts boost legacy supplier leverage

- Modular design and common parts libraries preserve optionality

Supplier concentration, 2024 metals +22%/+13%/+18% and semis lead times up to 52w

Allegion depends on specialized electromechanical and alloy suppliers, creating high switching costs and niche vendor leverage. 2024 commodity swings (LME copper +22%, aluminum +13%, zinc +18%, US HRC ±20%) and 25% US steel tariffs increased input pressure. Semiconductor allocation (lead times up to 52 weeks in 2021–23) and NRE/requalification (>$1M, 6–18 months) sustain supplier bargaining power.

| Metric | 2023–24 Data |

|---|---|

| Allegion net sales | $3.0B (2023) |

| Copper/Al/ZN moves (2024) | +22% / +13% / +18% |

| US HRC volatility | ±20% |

| Lead times (semis) | up to 52 weeks |

| NRE / requal | >$1M / 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Allegion uncovering competitive drivers, customer influence, supplier bargaining power, and barriers to entry within the security and access solutions market. Identifies disruptive substitutes, emerging threats, and strategic levers to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for Allegion that instantly highlights competitive pressures and relieves strategic uncertainty for faster decisions. Customize pressure levels, swap in your own data, and drop the clean layout straight into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated channels and large projects

Distributors, large contractors and institutional buyers aggregate volume and negotiate pricing against Allegion’s scale; Allegion reported roughly $3.0 billion in 2024 revenue, concentrating bargaining leverage. Multi-site rollouts and specification packages often drive competitive tendering and pressure margins through standardized SKUs. Buyers solicit cross-brand bids and secure volume rebates and service SLAs to retain accounts and reduce total cost of ownership.

Specification-driven demand

Architects and security consultants often spec-in Allegion products to meet codes and standards, creating design-phase lock-in that makes mid-project switching costly and reduces buyer leverage. Buyers retain influence by shaping specs early to allow approved alternatives, but once a strong spec position is established Allegion regains pricing and approval power. Specification control thus materially centralizes bargaining power with Allegion.

Total cost of ownership focus

Commercial customers prioritize total cost of ownership—lifecycle costs, reliability, and downtime—over unit price; Allegion reported roughly $3.8 billion in 2024 sales, underscoring scale in service and spare parts. High durability and bundled support reduce perceived switching gains, yet buyers with internal maintenance still negotiate parts pricing. Warranty length and rapid service response remain decisive levers in procurement decisions.

Interoperability and open standards

Enterprise buyers in 2024 increasingly prioritize open protocols and API-first access control; if competitors plug into existing IT stacks more easily, buyer leverage grows and can pressure pricing and service terms. Certified interoperability and clear software roadmaps with backward compatibility neutralize this power by reducing switching risk and protecting recurring revenue.

- Integration-first buying: raises buyer power

- Certified interoperability: reduces switching

- Roadmaps/backward compatibility: key bargaining chips

Residential price sensitivity

Consumers compare smart locks across retail and e-commerce, raising price transparency; average retail prices in 2024 clustered around $120–$250, compressing margins at value tiers. Promotions and feature parity heighten bargaining power in low-to-mid segments, while brand trust and app experience can command a modest premium of roughly 10–15%. Reviews and ecosystem fit (Alexa/Google/Apple) frequently tip final decisions.

- Price transparency: cross-channel comparisons

- Promo pressure: low-mid tier bargaining

- Brand/app premium: ~10–15%

- Ecosystem/reviews: decisive purchase factors

Scale vs buyers: distributor rebates compress margins; smart-lock retail transparency

Large distributors and enterprise buyers exert strong price and rebate pressure against Allegion’s scale (roughly $3.0 billion revenue in 2024), while spec-driven projects and certified interoperability reduce switching and boost Allegion’s negotiating position. Retail smart-lock price transparency compresses margins at $120–$250 average, though brand/app can command ~10–15% premium.

| Metric | 2024 Value |

|---|---|

| Allegion revenue | $3.0 billion |

| Smart-lock avg retail | $120–$250 |

| Brand/app premium | ~10–15% |

Full Version Awaits

Allegion Porter's Five Forces Analysis

This preview shows the exact Allegion Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the complete deliverable.