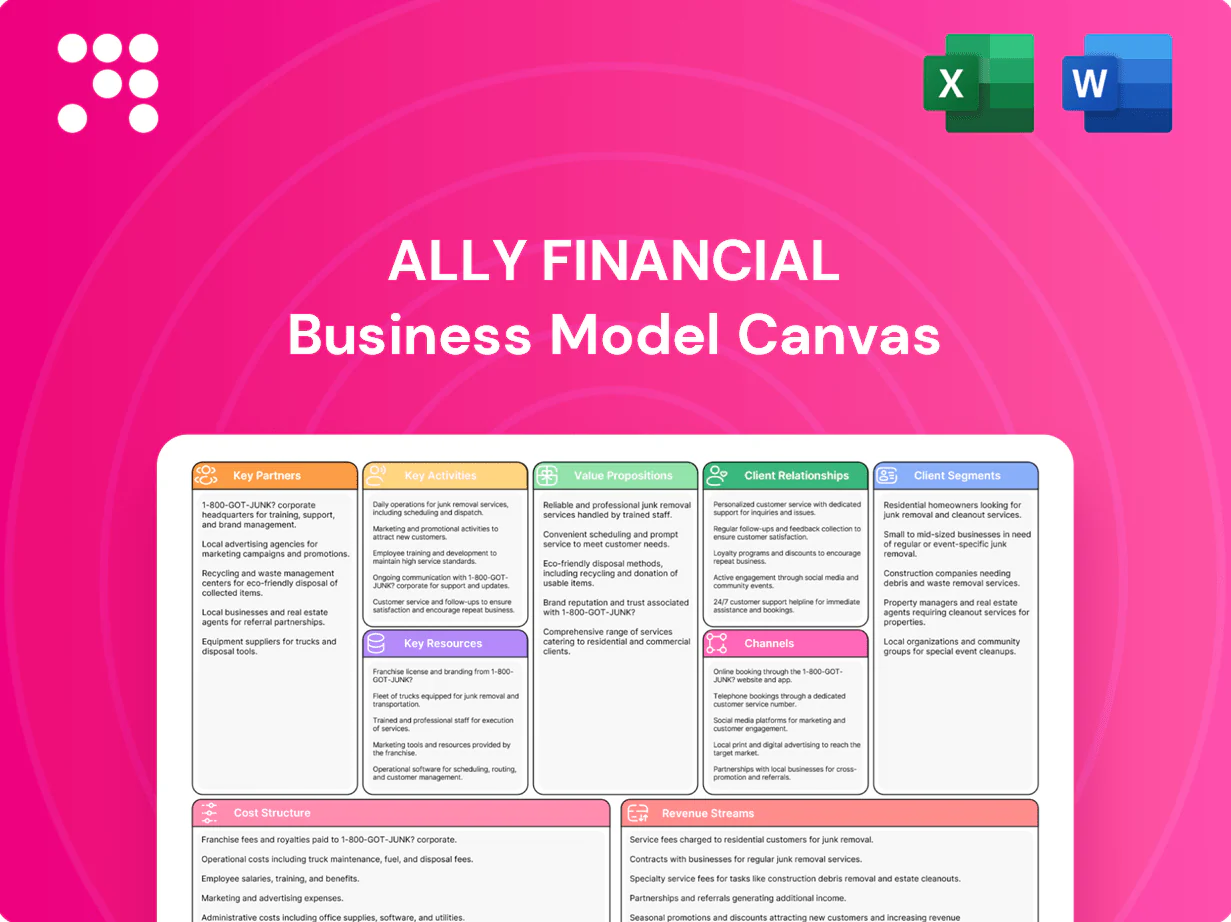

Ally Financial Business Model Canvas

Unlock the strategic playbook: 3-5 Business Model Canvas insights on digital banking & auto finance

Unlock Ally Financial’s strategic playbook with our concise Business Model Canvas—three to five clear insights on how it creates value, scales customer relationships, and monetizes digital banking and auto finance. Purchase the full, editable canvas for a section-by-section breakdown, financial implications, and ready-to-use templates for benchmarking or investor decks.

Partnerships

Auto OEMs and Dealer Networks

Ally partners with automakers and franchised dealers to originate retail and lease financing at the point of sale, driving customer acquisition and scale; its vehicle financing portfolio topped roughly $170 billion in 2024. Co-branded and captive-like programs lift approval rates and allow differentiated pricing, with dealer networks supplying the bulk of new originations. Data sharing enables tailored offers, improved risk management and loss mitigation.

Card Networks and Payment Processors

Alliances with Visa and Mastercard (each operating in 200+ countries and territories) and major processors enable Ally to issue cards, route payments and access settlement rails; networks provide fraud tools such as Visa Advanced Authorization and Mastercard Decision Intelligence plus tokenization. These partners help optimize interchange economics and authorization performance, and joint marketing programs historically boost card activation and spend.

Mortgage Secondary Market and Servicers

Relationships with agencies and institutional investors enable Ally to sell loans and securitize origination pools into the roughly $8.5 trillion agency MBS market in 2024, providing exit channels and price discovery. Third-party servicers and sub-servicers expand capacity and handle special servicing, supporting scale during peak origination windows. Warehouse lenders and custodians provide short-term funding and custody, reducing funding friction. Together this ecosystem boosts liquidity and capital efficiency for Ally.

Insurance Underwriters and Reinsurers

Underwriting partners supply auto-related protection products and transfer risk to reinsurers, while reinsurance structures manage loss volatility and optimize capital usage. Distribution agreements with brokers and dealer networks expand Ally’s reach, and collaboration between claims teams and actuaries improves pricing accuracy and product performance.

- Underwriting partners: product supply and risk transfer

- Reinsurance: loss volatility and capital efficiency

- Distribution: brokers and dealers extend reach

- Claims/actuarial: improves pricing and performance

Cloud, Fintech, and Data Providers

Cloud hyperscalers (AWS, Microsoft Azure, Google Cloud), core platforms, and API vendors power Ally’s digital stack. Credit bureaus (Experian, TransUnion, Equifax), identity verification, and fraud analytics firms shore up underwriting and KYC. Fintech partnerships accelerate feature delivery and innovation, enhancing scalability, resilience, and speed to market.

- Cloud partners: AWS, Azure, GCP

- Data partners: 3 major credit bureaus + ID/fraud vendors

- Fintechs: rapid feature delivery and co-innovation

Auto finance: $170B, 200+ countries, $8.5T securitization

Ally partners with automakers and dealers to originate retail and lease loans at point of sale; vehicle finance portfolio ~$170B in 2024. Card network partners (Visa, Mastercard) enable issuance, routing and fraud tools across 200+ countries, boosting interchange and spend. Capital markets, agencies and warehouse lenders enable securitization into the $8.5T agency MBS market while reinsurers and fintechs improve capital efficiency and delivery.

| Partner type | Examples | 2024 metric |

|---|---|---|

| Auto OEMs/Dealers | Captive-like programs | $170B vehicle portfolio |

| Card Networks | Visa, Mastercard | 200+ countries |

| Capital Markets | Agencies, investors, warehouses | $8.5T agency MBS market |

| Cloud/Data | AWS, Azure, GCP; Experian, TU, EQ | Digital ops & credit data |

What is included in the product

A comprehensive Business Model Canvas for Ally Financial detailing its nine core blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, activities, partners, and cost structure—aligned with real-world retail and commercial finance operations. Ideal for investors and analysts, it includes competitive advantages, SWOT-linked insights, and polished narratives for presentations and strategic validation.

High-level view of Ally Financial’s business model with editable cells to quickly surface and solve pain points across lending, digital banking, and auto finance. Clean, shareable snapshot ideal for teams to align on customer pain relievers, operational fixes, and strategic priorities.

Activities

Digital Lending and Underwriting

Origination across auto, mortgage, credit cards and personal loans is central to Ally's digital lending, with automated decisioning and pricing models used to assess risk and optimize yield. E-contracting and e-sign capabilities streamline funding cycles and reduce time-to-fund. Continuous portfolio monitoring and analytics maintain credit quality and inform loss mitigation post-origination.

Deposit Gathering and Treasury Management

Direct-to-consumer deposits fund lending and investments, supporting over $150 billion in retail deposits at Ally in 2024 and reducing wholesale funding dependence. Active rate setting, liquidity management, and ALM target stable net interest spreads and balance-sheet resilience. Comprehensive hedging programs mitigate interest-rate and basis risks. Robust cash operations and payment rails process billions monthly to keep the platform reliable.

Risk, Compliance, and Security

Ally’s credit, market, and operational risk frameworks protect the franchise with enterprise-wide limits, portfolio stress monitoring, and hedging programs aligned to 2024 regulatory expectations. Regulatory compliance covers banking supervision, fair lending oversight, and consumer privacy under federal statutes and Fed/OCIE guidance. Cybersecurity and fraud prevention combine multi-layer detection, identity verification, and incident response to safeguard customers and systems. Stress testing and capital planning support resilience through periodic scenario analyses and contingency capital actions.

Technology Development and Operations

Building and maintaining Ally's web, mobile, and API platforms is continuous, supporting digital-first banking with industry-standard uptime targets of 99.99% and multi-week agile sprints for releases.

Data engineering and analytics drive personalization and risk scoring, while reliability engineering and cloud ops ensure scalability and low-latency performance.

- Continuous platform delivery

- 99.99% uptime target

- Data-driven personalization & risk

- Agile 2-week sprints

Servicing, Collections, and Customer Care

Loan servicing at Ally manages billing, escrow, and customer inquiries for a servicing portfolio exceeding $100 billion as of 2024, ensuring accurate statements and escrow administration. Early-stage collections and loss mitigation focus on cure strategies and workout options to preserve asset value and limit charge-offs. Claims processing underpins Ally Insurance offerings, while omnichannel support (phone, app, chat) drives satisfaction and retention.

- Servicing: billing, escrow, inquiries — portfolio >$100B (2024)

- Collections: early-stage loss mitigation to reduce charge-offs

- Claims: insurance product support and adjudication

- Customer care: omnichannel support to sustain retention

Automated multi-product lending — deposits $150B, servicing > $100B, uptime 99.99%

Origination across auto, mortgage, cards and personal loans with automated underwriting; retail deposits $150B (2024) fund lending; servicing portfolio >$100B (2024) with collections and claims; platform uptime target 99.99% and agile 2-week sprints; analytics, hedging, compliance and cybersecurity underpin operations.

| Activity | 2024 metric |

|---|---|

| Deposits | $150B |

| Servicing | >$100B |

| Uptime target | 99.99% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Ally Financial Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview matches the final editable Word and Excel files, including structure, content, and formatting. Buy with confidence: the full, downloadable document will be identical and ready to edit, present, or share.

Unlock the strategic playbook: 3-5 Business Model Canvas insights on digital banking & auto finance

Unlock Ally Financial’s strategic playbook with our concise Business Model Canvas—three to five clear insights on how it creates value, scales customer relationships, and monetizes digital banking and auto finance. Purchase the full, editable canvas for a section-by-section breakdown, financial implications, and ready-to-use templates for benchmarking or investor decks.

Partnerships

Auto OEMs and Dealer Networks

Ally partners with automakers and franchised dealers to originate retail and lease financing at the point of sale, driving customer acquisition and scale; its vehicle financing portfolio topped roughly $170 billion in 2024. Co-branded and captive-like programs lift approval rates and allow differentiated pricing, with dealer networks supplying the bulk of new originations. Data sharing enables tailored offers, improved risk management and loss mitigation.

Card Networks and Payment Processors

Alliances with Visa and Mastercard (each operating in 200+ countries and territories) and major processors enable Ally to issue cards, route payments and access settlement rails; networks provide fraud tools such as Visa Advanced Authorization and Mastercard Decision Intelligence plus tokenization. These partners help optimize interchange economics and authorization performance, and joint marketing programs historically boost card activation and spend.

Mortgage Secondary Market and Servicers

Relationships with agencies and institutional investors enable Ally to sell loans and securitize origination pools into the roughly $8.5 trillion agency MBS market in 2024, providing exit channels and price discovery. Third-party servicers and sub-servicers expand capacity and handle special servicing, supporting scale during peak origination windows. Warehouse lenders and custodians provide short-term funding and custody, reducing funding friction. Together this ecosystem boosts liquidity and capital efficiency for Ally.

Insurance Underwriters and Reinsurers

Underwriting partners supply auto-related protection products and transfer risk to reinsurers, while reinsurance structures manage loss volatility and optimize capital usage. Distribution agreements with brokers and dealer networks expand Ally’s reach, and collaboration between claims teams and actuaries improves pricing accuracy and product performance.

- Underwriting partners: product supply and risk transfer

- Reinsurance: loss volatility and capital efficiency

- Distribution: brokers and dealers extend reach

- Claims/actuarial: improves pricing and performance

Cloud, Fintech, and Data Providers

Cloud hyperscalers (AWS, Microsoft Azure, Google Cloud), core platforms, and API vendors power Ally’s digital stack. Credit bureaus (Experian, TransUnion, Equifax), identity verification, and fraud analytics firms shore up underwriting and KYC. Fintech partnerships accelerate feature delivery and innovation, enhancing scalability, resilience, and speed to market.

- Cloud partners: AWS, Azure, GCP

- Data partners: 3 major credit bureaus + ID/fraud vendors

- Fintechs: rapid feature delivery and co-innovation

Auto finance: $170B, 200+ countries, $8.5T securitization

Ally partners with automakers and dealers to originate retail and lease loans at point of sale; vehicle finance portfolio ~$170B in 2024. Card network partners (Visa, Mastercard) enable issuance, routing and fraud tools across 200+ countries, boosting interchange and spend. Capital markets, agencies and warehouse lenders enable securitization into the $8.5T agency MBS market while reinsurers and fintechs improve capital efficiency and delivery.

| Partner type | Examples | 2024 metric |

|---|---|---|

| Auto OEMs/Dealers | Captive-like programs | $170B vehicle portfolio |

| Card Networks | Visa, Mastercard | 200+ countries |

| Capital Markets | Agencies, investors, warehouses | $8.5T agency MBS market |

| Cloud/Data | AWS, Azure, GCP; Experian, TU, EQ | Digital ops & credit data |

What is included in the product

A comprehensive Business Model Canvas for Ally Financial detailing its nine core blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, activities, partners, and cost structure—aligned with real-world retail and commercial finance operations. Ideal for investors and analysts, it includes competitive advantages, SWOT-linked insights, and polished narratives for presentations and strategic validation.

High-level view of Ally Financial’s business model with editable cells to quickly surface and solve pain points across lending, digital banking, and auto finance. Clean, shareable snapshot ideal for teams to align on customer pain relievers, operational fixes, and strategic priorities.

Activities

Digital Lending and Underwriting

Origination across auto, mortgage, credit cards and personal loans is central to Ally's digital lending, with automated decisioning and pricing models used to assess risk and optimize yield. E-contracting and e-sign capabilities streamline funding cycles and reduce time-to-fund. Continuous portfolio monitoring and analytics maintain credit quality and inform loss mitigation post-origination.

Deposit Gathering and Treasury Management

Direct-to-consumer deposits fund lending and investments, supporting over $150 billion in retail deposits at Ally in 2024 and reducing wholesale funding dependence. Active rate setting, liquidity management, and ALM target stable net interest spreads and balance-sheet resilience. Comprehensive hedging programs mitigate interest-rate and basis risks. Robust cash operations and payment rails process billions monthly to keep the platform reliable.

Risk, Compliance, and Security

Ally’s credit, market, and operational risk frameworks protect the franchise with enterprise-wide limits, portfolio stress monitoring, and hedging programs aligned to 2024 regulatory expectations. Regulatory compliance covers banking supervision, fair lending oversight, and consumer privacy under federal statutes and Fed/OCIE guidance. Cybersecurity and fraud prevention combine multi-layer detection, identity verification, and incident response to safeguard customers and systems. Stress testing and capital planning support resilience through periodic scenario analyses and contingency capital actions.

Technology Development and Operations

Building and maintaining Ally's web, mobile, and API platforms is continuous, supporting digital-first banking with industry-standard uptime targets of 99.99% and multi-week agile sprints for releases.

Data engineering and analytics drive personalization and risk scoring, while reliability engineering and cloud ops ensure scalability and low-latency performance.

- Continuous platform delivery

- 99.99% uptime target

- Data-driven personalization & risk

- Agile 2-week sprints

Servicing, Collections, and Customer Care

Loan servicing at Ally manages billing, escrow, and customer inquiries for a servicing portfolio exceeding $100 billion as of 2024, ensuring accurate statements and escrow administration. Early-stage collections and loss mitigation focus on cure strategies and workout options to preserve asset value and limit charge-offs. Claims processing underpins Ally Insurance offerings, while omnichannel support (phone, app, chat) drives satisfaction and retention.

- Servicing: billing, escrow, inquiries — portfolio >$100B (2024)

- Collections: early-stage loss mitigation to reduce charge-offs

- Claims: insurance product support and adjudication

- Customer care: omnichannel support to sustain retention

Automated multi-product lending — deposits $150B, servicing > $100B, uptime 99.99%

Origination across auto, mortgage, cards and personal loans with automated underwriting; retail deposits $150B (2024) fund lending; servicing portfolio >$100B (2024) with collections and claims; platform uptime target 99.99% and agile 2-week sprints; analytics, hedging, compliance and cybersecurity underpin operations.

| Activity | 2024 metric |

|---|---|

| Deposits | $150B |

| Servicing | >$100B |

| Uptime target | 99.99% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Ally Financial Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview matches the final editable Word and Excel files, including structure, content, and formatting. Buy with confidence: the full, downloadable document will be identical and ready to edit, present, or share.

Description

Unlock the strategic playbook: 3-5 Business Model Canvas insights on digital banking & auto finance

Unlock Ally Financial’s strategic playbook with our concise Business Model Canvas—three to five clear insights on how it creates value, scales customer relationships, and monetizes digital banking and auto finance. Purchase the full, editable canvas for a section-by-section breakdown, financial implications, and ready-to-use templates for benchmarking or investor decks.

Partnerships

Auto OEMs and Dealer Networks

Ally partners with automakers and franchised dealers to originate retail and lease financing at the point of sale, driving customer acquisition and scale; its vehicle financing portfolio topped roughly $170 billion in 2024. Co-branded and captive-like programs lift approval rates and allow differentiated pricing, with dealer networks supplying the bulk of new originations. Data sharing enables tailored offers, improved risk management and loss mitigation.

Card Networks and Payment Processors

Alliances with Visa and Mastercard (each operating in 200+ countries and territories) and major processors enable Ally to issue cards, route payments and access settlement rails; networks provide fraud tools such as Visa Advanced Authorization and Mastercard Decision Intelligence plus tokenization. These partners help optimize interchange economics and authorization performance, and joint marketing programs historically boost card activation and spend.

Mortgage Secondary Market and Servicers

Relationships with agencies and institutional investors enable Ally to sell loans and securitize origination pools into the roughly $8.5 trillion agency MBS market in 2024, providing exit channels and price discovery. Third-party servicers and sub-servicers expand capacity and handle special servicing, supporting scale during peak origination windows. Warehouse lenders and custodians provide short-term funding and custody, reducing funding friction. Together this ecosystem boosts liquidity and capital efficiency for Ally.

Insurance Underwriters and Reinsurers

Underwriting partners supply auto-related protection products and transfer risk to reinsurers, while reinsurance structures manage loss volatility and optimize capital usage. Distribution agreements with brokers and dealer networks expand Ally’s reach, and collaboration between claims teams and actuaries improves pricing accuracy and product performance.

- Underwriting partners: product supply and risk transfer

- Reinsurance: loss volatility and capital efficiency

- Distribution: brokers and dealers extend reach

- Claims/actuarial: improves pricing and performance

Cloud, Fintech, and Data Providers

Cloud hyperscalers (AWS, Microsoft Azure, Google Cloud), core platforms, and API vendors power Ally’s digital stack. Credit bureaus (Experian, TransUnion, Equifax), identity verification, and fraud analytics firms shore up underwriting and KYC. Fintech partnerships accelerate feature delivery and innovation, enhancing scalability, resilience, and speed to market.

- Cloud partners: AWS, Azure, GCP

- Data partners: 3 major credit bureaus + ID/fraud vendors

- Fintechs: rapid feature delivery and co-innovation

Auto finance: $170B, 200+ countries, $8.5T securitization

Ally partners with automakers and dealers to originate retail and lease loans at point of sale; vehicle finance portfolio ~$170B in 2024. Card network partners (Visa, Mastercard) enable issuance, routing and fraud tools across 200+ countries, boosting interchange and spend. Capital markets, agencies and warehouse lenders enable securitization into the $8.5T agency MBS market while reinsurers and fintechs improve capital efficiency and delivery.

| Partner type | Examples | 2024 metric |

|---|---|---|

| Auto OEMs/Dealers | Captive-like programs | $170B vehicle portfolio |

| Card Networks | Visa, Mastercard | 200+ countries |

| Capital Markets | Agencies, investors, warehouses | $8.5T agency MBS market |

| Cloud/Data | AWS, Azure, GCP; Experian, TU, EQ | Digital ops & credit data |

What is included in the product

A comprehensive Business Model Canvas for Ally Financial detailing its nine core blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, activities, partners, and cost structure—aligned with real-world retail and commercial finance operations. Ideal for investors and analysts, it includes competitive advantages, SWOT-linked insights, and polished narratives for presentations and strategic validation.

High-level view of Ally Financial’s business model with editable cells to quickly surface and solve pain points across lending, digital banking, and auto finance. Clean, shareable snapshot ideal for teams to align on customer pain relievers, operational fixes, and strategic priorities.

Activities

Digital Lending and Underwriting

Origination across auto, mortgage, credit cards and personal loans is central to Ally's digital lending, with automated decisioning and pricing models used to assess risk and optimize yield. E-contracting and e-sign capabilities streamline funding cycles and reduce time-to-fund. Continuous portfolio monitoring and analytics maintain credit quality and inform loss mitigation post-origination.

Deposit Gathering and Treasury Management

Direct-to-consumer deposits fund lending and investments, supporting over $150 billion in retail deposits at Ally in 2024 and reducing wholesale funding dependence. Active rate setting, liquidity management, and ALM target stable net interest spreads and balance-sheet resilience. Comprehensive hedging programs mitigate interest-rate and basis risks. Robust cash operations and payment rails process billions monthly to keep the platform reliable.

Risk, Compliance, and Security

Ally’s credit, market, and operational risk frameworks protect the franchise with enterprise-wide limits, portfolio stress monitoring, and hedging programs aligned to 2024 regulatory expectations. Regulatory compliance covers banking supervision, fair lending oversight, and consumer privacy under federal statutes and Fed/OCIE guidance. Cybersecurity and fraud prevention combine multi-layer detection, identity verification, and incident response to safeguard customers and systems. Stress testing and capital planning support resilience through periodic scenario analyses and contingency capital actions.

Technology Development and Operations

Building and maintaining Ally's web, mobile, and API platforms is continuous, supporting digital-first banking with industry-standard uptime targets of 99.99% and multi-week agile sprints for releases.

Data engineering and analytics drive personalization and risk scoring, while reliability engineering and cloud ops ensure scalability and low-latency performance.

- Continuous platform delivery

- 99.99% uptime target

- Data-driven personalization & risk

- Agile 2-week sprints

Servicing, Collections, and Customer Care

Loan servicing at Ally manages billing, escrow, and customer inquiries for a servicing portfolio exceeding $100 billion as of 2024, ensuring accurate statements and escrow administration. Early-stage collections and loss mitigation focus on cure strategies and workout options to preserve asset value and limit charge-offs. Claims processing underpins Ally Insurance offerings, while omnichannel support (phone, app, chat) drives satisfaction and retention.

- Servicing: billing, escrow, inquiries — portfolio >$100B (2024)

- Collections: early-stage loss mitigation to reduce charge-offs

- Claims: insurance product support and adjudication

- Customer care: omnichannel support to sustain retention

Automated multi-product lending — deposits $150B, servicing > $100B, uptime 99.99%

Origination across auto, mortgage, cards and personal loans with automated underwriting; retail deposits $150B (2024) fund lending; servicing portfolio >$100B (2024) with collections and claims; platform uptime target 99.99% and agile 2-week sprints; analytics, hedging, compliance and cybersecurity underpin operations.

| Activity | 2024 metric |

|---|---|

| Deposits | $150B |

| Servicing | >$100B |

| Uptime target | 99.99% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Ally Financial Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview matches the final editable Word and Excel files, including structure, content, and formatting. Buy with confidence: the full, downloadable document will be identical and ready to edit, present, or share.