Alm. Brand Business Model Canvas

Unlock the Business Model Canvas for this insurer: value, risk, and revenue insights

Unlock the full Business Model Canvas for Alm. Brand and see exactly how the insurer creates value, manages risk, and monetizes customer relationships. This concise, company-specific canvas reveals partnerships, revenue streams, and cost drivers. Perfect for investors, strategists, or founders seeking actionable insights—download the full template to apply these lessons to your own strategy.

Partnerships

Global reinsurers

Global reinsurers absorb Alm. Brand’s peak and catastrophe risks to stabilize loss ratios and protect the balance sheet, enabling underwriting of larger corporate policies; structured treaty and facultative arrangements are used to optimize capital efficiency and transfer volatility; long-term reinsurance relationships support pricing discipline and back joint product innovation and tailored coverage solutions.

Brokers and agents

Independent brokers extend Alm. Brand’s reach into SME and corporate segments, crucial given that SMEs account for about 99% of Danish enterprises (EU Commission data). Brokers provide market insight and place complex risks that direct channels often cannot. Commissioned distribution complements Alm. Brand’s digital and bancassurance channels, while co-marketing and structured training programs ensure a consistent customer experience.

Auto dealers and repair networks

Alm. Brand relies on preferred garages and parts suppliers to streamline motor claims, leveraging Denmark’s ~2.7 million passenger cars (2024) to scale network efficiencies. These partnerships speed repairs, control parts and labor costs, and lift claims satisfaction metrics. Data sharing enables accurate digital estimates and stronger fraud controls—reducing cycle times by ~30% and lowering fraud loss exposure. OEM and dealer collaborations enable embedded point-of-sale insurance.

Data, tech, and telematics providers

- Data enrichment: better risk scoring, lower loss ratios

- Telematics/IoT: usage-based pricing, -25% accident risk in pilots

- Cloud & analytics: faster deployment, scalable ML

- Cybersecurity: encryption, incident response for PII

Regulators and industry bodies

Close engagement with Finanstilsynet and EU authorities ensures Alm. Brand meets Danish and EU insurance requirements, anchored in the Solvency II framework implemented in 2016, and informs product design and capital planning through ongoing regulatory dialogue.

- Regulators: Finanstilsynet — compliance and supervision

- EU rules: Solvency II (2016) — capital and reporting framework

- Industry bodies: Insurance Europe — standards and best practice

- Outcome: stronger consumer trust and market stability

Reinsurance, brokers and telematics unlock scalable SME underwriting and 30% faster claims

Alm. Brand leverages global reinsurers to cap peak losses and optimize capital, enabling larger commercial underwriting. Independent brokers and bancassurance extend SME reach (SMEs ~99% of Danish firms) and place complex risks. Telematics, preferred garages and cloud partners cut claims cycle ~30% and support +25% Nordic telematics growth in 2024.

| Metric | Value (2024) |

|---|---|

| SME share | ~99% |

| Passenger cars DK | 2.7M |

| Telematics growth | +25% |

What is included in the product

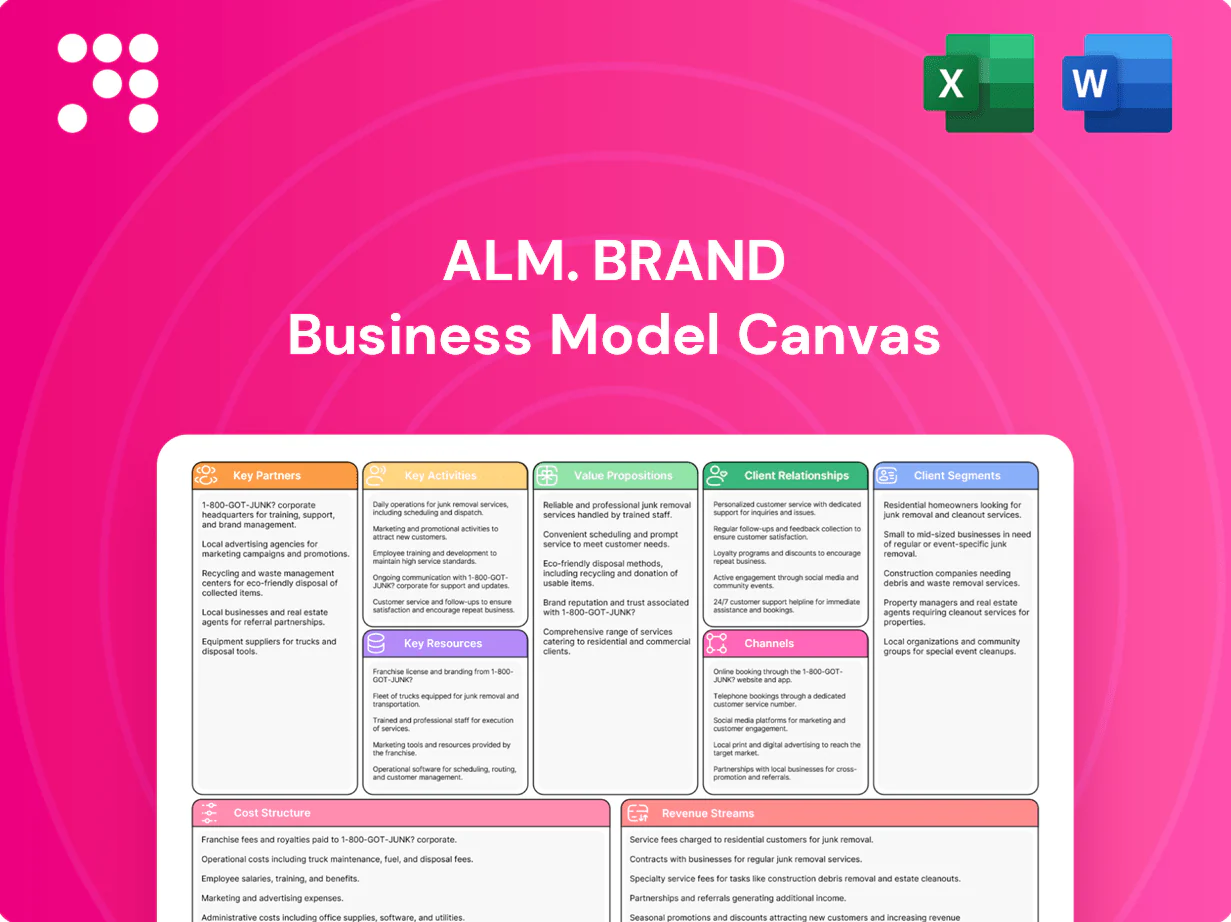

A ready-made Business Model Canvas for Alm. Brand detailing customer segments, value propositions, channels, revenue streams and operations across the 9 BMC blocks. Designed for presentations and investor discussions, it includes competitive advantages, SWOT-linked insights and actionable strategic recommendations based on real-world company data.

High-level view of Alm. Brand’s insurance business model with editable cells, streamlining analysis of distribution, underwriting and claims as a pain-point reliever. Shareable and editable for teams—saves hours of structuring strategy and creates a clean one-page snapshot for boardrooms or quick comparisons.

Activities

Risk underwriting

Assess, price and selectively underwrite property, casualty and motor risks using granular segmentations and exposure maps to limit tail concentration.

Actuarial models, catastrophe and telematics inputs plus external data sources calibrate risk-based premiums and reserve assumptions.

Guidelines are continuously refined by segment and exposure to improve hit-rate and reduce adverse selection while balancing growth against portfolio profitability in the Danish market (population c. 5.9 million in 2024).

Claims management

Handle FNOL, assessment and settlement efficiently to shorten cycle times and improve customer satisfaction. Prevent leakage through triage, fraud analytics and strict vendor controls to protect underwriting results. Prioritize customer empathy in every interaction while driving fast resolution. Aggressively pursue subrogation where applicable to reduce net claims costs.

Product development

Design modular covers and add-ons for retail and SME needs, enabling tailored bundles and cross-sell across motor, home and business lines. Align terms with evolving risks such as cyber—global cyber premiums grew strongly into 2024 after ~40% growth in 2023—and climate-driven exposures. Simplify wording to improve transparency and compliance. Pilot and iterate using customer feedback and loss experience to refine pricing and cover limits.

Risk and capital management

Risk and capital management monitors solvency under Solvency II (minimum 100%), reinsurance programs and asset-liability matching, while stress-testing catastrophe and market scenarios to quantify tail-risk. Capital is optimized across lines and channels to support profitable growth and meet regulatory ratios and ratings expectations, maintaining available capital buffers and contingency plans.

- Monitor Solvency II >=100%

- Reinsurance optimization

- ALM and stress tests

- Capital allocation across lines/channels

- Regulatory ratios and rating alignment

Digital distribution and service

Alm. Brand operates web, app and API-enabled journeys to automate quotes, policy issuance and endorsements, integrating payments and e-signatures via Danish MitID and PSD2 rails to enable frictionless onboarding; Denmark population ~5.9 million (2024) supports high digital uptake. Analytics-driven personalization tailors offers and service using real-time data.

- Operate web, app, API journeys

- Automate quotes, issuance, endorsements

- Integrate payments & e-signatures (MitID/PSD2)

- Use analytics for personalized offers

Underwrite motor, property & commercial risks with telematics and Solvency II capital

Assess, price and underwrite motor, property and commercial risks using granular segmentations and telematics to limit tail concentration.

Calibrate premiums/reserves with actuarial, catastrophe and external data; Denmark population c. 5.9m (2024).

Fast FNOL, fraud analytics, subrogation and vendor controls shorten cycles and reduce leakage.

Manage capital via Solvency II monitoring, reinsurance and ALM stress tests to protect ratings.

| Metric | 2024 |

|---|---|

| Denmark pop. | 5.9m |

| Solvency II | >=100% |

What You See Is What You Get

Business Model Canvas

The Alm. Brand Business Model Canvas previewed here is the exact deliverable—not a mockup—and reflects the full document you will receive after purchase. Upon completing your order you’ll download the same professionally formatted file, ready to edit, present, and share. No placeholders, no surprises.

Unlock the Business Model Canvas for this insurer: value, risk, and revenue insights

Unlock the full Business Model Canvas for Alm. Brand and see exactly how the insurer creates value, manages risk, and monetizes customer relationships. This concise, company-specific canvas reveals partnerships, revenue streams, and cost drivers. Perfect for investors, strategists, or founders seeking actionable insights—download the full template to apply these lessons to your own strategy.

Partnerships

Global reinsurers

Global reinsurers absorb Alm. Brand’s peak and catastrophe risks to stabilize loss ratios and protect the balance sheet, enabling underwriting of larger corporate policies; structured treaty and facultative arrangements are used to optimize capital efficiency and transfer volatility; long-term reinsurance relationships support pricing discipline and back joint product innovation and tailored coverage solutions.

Brokers and agents

Independent brokers extend Alm. Brand’s reach into SME and corporate segments, crucial given that SMEs account for about 99% of Danish enterprises (EU Commission data). Brokers provide market insight and place complex risks that direct channels often cannot. Commissioned distribution complements Alm. Brand’s digital and bancassurance channels, while co-marketing and structured training programs ensure a consistent customer experience.

Auto dealers and repair networks

Alm. Brand relies on preferred garages and parts suppliers to streamline motor claims, leveraging Denmark’s ~2.7 million passenger cars (2024) to scale network efficiencies. These partnerships speed repairs, control parts and labor costs, and lift claims satisfaction metrics. Data sharing enables accurate digital estimates and stronger fraud controls—reducing cycle times by ~30% and lowering fraud loss exposure. OEM and dealer collaborations enable embedded point-of-sale insurance.

Data, tech, and telematics providers

- Data enrichment: better risk scoring, lower loss ratios

- Telematics/IoT: usage-based pricing, -25% accident risk in pilots

- Cloud & analytics: faster deployment, scalable ML

- Cybersecurity: encryption, incident response for PII

Regulators and industry bodies

Close engagement with Finanstilsynet and EU authorities ensures Alm. Brand meets Danish and EU insurance requirements, anchored in the Solvency II framework implemented in 2016, and informs product design and capital planning through ongoing regulatory dialogue.

- Regulators: Finanstilsynet — compliance and supervision

- EU rules: Solvency II (2016) — capital and reporting framework

- Industry bodies: Insurance Europe — standards and best practice

- Outcome: stronger consumer trust and market stability

Reinsurance, brokers and telematics unlock scalable SME underwriting and 30% faster claims

Alm. Brand leverages global reinsurers to cap peak losses and optimize capital, enabling larger commercial underwriting. Independent brokers and bancassurance extend SME reach (SMEs ~99% of Danish firms) and place complex risks. Telematics, preferred garages and cloud partners cut claims cycle ~30% and support +25% Nordic telematics growth in 2024.

| Metric | Value (2024) |

|---|---|

| SME share | ~99% |

| Passenger cars DK | 2.7M |

| Telematics growth | +25% |

What is included in the product

A ready-made Business Model Canvas for Alm. Brand detailing customer segments, value propositions, channels, revenue streams and operations across the 9 BMC blocks. Designed for presentations and investor discussions, it includes competitive advantages, SWOT-linked insights and actionable strategic recommendations based on real-world company data.

High-level view of Alm. Brand’s insurance business model with editable cells, streamlining analysis of distribution, underwriting and claims as a pain-point reliever. Shareable and editable for teams—saves hours of structuring strategy and creates a clean one-page snapshot for boardrooms or quick comparisons.

Activities

Risk underwriting

Assess, price and selectively underwrite property, casualty and motor risks using granular segmentations and exposure maps to limit tail concentration.

Actuarial models, catastrophe and telematics inputs plus external data sources calibrate risk-based premiums and reserve assumptions.

Guidelines are continuously refined by segment and exposure to improve hit-rate and reduce adverse selection while balancing growth against portfolio profitability in the Danish market (population c. 5.9 million in 2024).

Claims management

Handle FNOL, assessment and settlement efficiently to shorten cycle times and improve customer satisfaction. Prevent leakage through triage, fraud analytics and strict vendor controls to protect underwriting results. Prioritize customer empathy in every interaction while driving fast resolution. Aggressively pursue subrogation where applicable to reduce net claims costs.

Product development

Design modular covers and add-ons for retail and SME needs, enabling tailored bundles and cross-sell across motor, home and business lines. Align terms with evolving risks such as cyber—global cyber premiums grew strongly into 2024 after ~40% growth in 2023—and climate-driven exposures. Simplify wording to improve transparency and compliance. Pilot and iterate using customer feedback and loss experience to refine pricing and cover limits.

Risk and capital management

Risk and capital management monitors solvency under Solvency II (minimum 100%), reinsurance programs and asset-liability matching, while stress-testing catastrophe and market scenarios to quantify tail-risk. Capital is optimized across lines and channels to support profitable growth and meet regulatory ratios and ratings expectations, maintaining available capital buffers and contingency plans.

- Monitor Solvency II >=100%

- Reinsurance optimization

- ALM and stress tests

- Capital allocation across lines/channels

- Regulatory ratios and rating alignment

Digital distribution and service

Alm. Brand operates web, app and API-enabled journeys to automate quotes, policy issuance and endorsements, integrating payments and e-signatures via Danish MitID and PSD2 rails to enable frictionless onboarding; Denmark population ~5.9 million (2024) supports high digital uptake. Analytics-driven personalization tailors offers and service using real-time data.

- Operate web, app, API journeys

- Automate quotes, issuance, endorsements

- Integrate payments & e-signatures (MitID/PSD2)

- Use analytics for personalized offers

Underwrite motor, property & commercial risks with telematics and Solvency II capital

Assess, price and underwrite motor, property and commercial risks using granular segmentations and telematics to limit tail concentration.

Calibrate premiums/reserves with actuarial, catastrophe and external data; Denmark population c. 5.9m (2024).

Fast FNOL, fraud analytics, subrogation and vendor controls shorten cycles and reduce leakage.

Manage capital via Solvency II monitoring, reinsurance and ALM stress tests to protect ratings.

| Metric | 2024 |

|---|---|

| Denmark pop. | 5.9m |

| Solvency II | >=100% |

What You See Is What You Get

Business Model Canvas

The Alm. Brand Business Model Canvas previewed here is the exact deliverable—not a mockup—and reflects the full document you will receive after purchase. Upon completing your order you’ll download the same professionally formatted file, ready to edit, present, and share. No placeholders, no surprises.

Description

Unlock the Business Model Canvas for this insurer: value, risk, and revenue insights

Unlock the full Business Model Canvas for Alm. Brand and see exactly how the insurer creates value, manages risk, and monetizes customer relationships. This concise, company-specific canvas reveals partnerships, revenue streams, and cost drivers. Perfect for investors, strategists, or founders seeking actionable insights—download the full template to apply these lessons to your own strategy.

Partnerships

Global reinsurers

Global reinsurers absorb Alm. Brand’s peak and catastrophe risks to stabilize loss ratios and protect the balance sheet, enabling underwriting of larger corporate policies; structured treaty and facultative arrangements are used to optimize capital efficiency and transfer volatility; long-term reinsurance relationships support pricing discipline and back joint product innovation and tailored coverage solutions.

Brokers and agents

Independent brokers extend Alm. Brand’s reach into SME and corporate segments, crucial given that SMEs account for about 99% of Danish enterprises (EU Commission data). Brokers provide market insight and place complex risks that direct channels often cannot. Commissioned distribution complements Alm. Brand’s digital and bancassurance channels, while co-marketing and structured training programs ensure a consistent customer experience.

Auto dealers and repair networks

Alm. Brand relies on preferred garages and parts suppliers to streamline motor claims, leveraging Denmark’s ~2.7 million passenger cars (2024) to scale network efficiencies. These partnerships speed repairs, control parts and labor costs, and lift claims satisfaction metrics. Data sharing enables accurate digital estimates and stronger fraud controls—reducing cycle times by ~30% and lowering fraud loss exposure. OEM and dealer collaborations enable embedded point-of-sale insurance.

Data, tech, and telematics providers

- Data enrichment: better risk scoring, lower loss ratios

- Telematics/IoT: usage-based pricing, -25% accident risk in pilots

- Cloud & analytics: faster deployment, scalable ML

- Cybersecurity: encryption, incident response for PII

Regulators and industry bodies

Close engagement with Finanstilsynet and EU authorities ensures Alm. Brand meets Danish and EU insurance requirements, anchored in the Solvency II framework implemented in 2016, and informs product design and capital planning through ongoing regulatory dialogue.

- Regulators: Finanstilsynet — compliance and supervision

- EU rules: Solvency II (2016) — capital and reporting framework

- Industry bodies: Insurance Europe — standards and best practice

- Outcome: stronger consumer trust and market stability

Reinsurance, brokers and telematics unlock scalable SME underwriting and 30% faster claims

Alm. Brand leverages global reinsurers to cap peak losses and optimize capital, enabling larger commercial underwriting. Independent brokers and bancassurance extend SME reach (SMEs ~99% of Danish firms) and place complex risks. Telematics, preferred garages and cloud partners cut claims cycle ~30% and support +25% Nordic telematics growth in 2024.

| Metric | Value (2024) |

|---|---|

| SME share | ~99% |

| Passenger cars DK | 2.7M |

| Telematics growth | +25% |

What is included in the product

A ready-made Business Model Canvas for Alm. Brand detailing customer segments, value propositions, channels, revenue streams and operations across the 9 BMC blocks. Designed for presentations and investor discussions, it includes competitive advantages, SWOT-linked insights and actionable strategic recommendations based on real-world company data.

High-level view of Alm. Brand’s insurance business model with editable cells, streamlining analysis of distribution, underwriting and claims as a pain-point reliever. Shareable and editable for teams—saves hours of structuring strategy and creates a clean one-page snapshot for boardrooms or quick comparisons.

Activities

Risk underwriting

Assess, price and selectively underwrite property, casualty and motor risks using granular segmentations and exposure maps to limit tail concentration.

Actuarial models, catastrophe and telematics inputs plus external data sources calibrate risk-based premiums and reserve assumptions.

Guidelines are continuously refined by segment and exposure to improve hit-rate and reduce adverse selection while balancing growth against portfolio profitability in the Danish market (population c. 5.9 million in 2024).

Claims management

Handle FNOL, assessment and settlement efficiently to shorten cycle times and improve customer satisfaction. Prevent leakage through triage, fraud analytics and strict vendor controls to protect underwriting results. Prioritize customer empathy in every interaction while driving fast resolution. Aggressively pursue subrogation where applicable to reduce net claims costs.

Product development

Design modular covers and add-ons for retail and SME needs, enabling tailored bundles and cross-sell across motor, home and business lines. Align terms with evolving risks such as cyber—global cyber premiums grew strongly into 2024 after ~40% growth in 2023—and climate-driven exposures. Simplify wording to improve transparency and compliance. Pilot and iterate using customer feedback and loss experience to refine pricing and cover limits.

Risk and capital management

Risk and capital management monitors solvency under Solvency II (minimum 100%), reinsurance programs and asset-liability matching, while stress-testing catastrophe and market scenarios to quantify tail-risk. Capital is optimized across lines and channels to support profitable growth and meet regulatory ratios and ratings expectations, maintaining available capital buffers and contingency plans.

- Monitor Solvency II >=100%

- Reinsurance optimization

- ALM and stress tests

- Capital allocation across lines/channels

- Regulatory ratios and rating alignment

Digital distribution and service

Alm. Brand operates web, app and API-enabled journeys to automate quotes, policy issuance and endorsements, integrating payments and e-signatures via Danish MitID and PSD2 rails to enable frictionless onboarding; Denmark population ~5.9 million (2024) supports high digital uptake. Analytics-driven personalization tailors offers and service using real-time data.

- Operate web, app, API journeys

- Automate quotes, issuance, endorsements

- Integrate payments & e-signatures (MitID/PSD2)

- Use analytics for personalized offers

Underwrite motor, property & commercial risks with telematics and Solvency II capital

Assess, price and underwrite motor, property and commercial risks using granular segmentations and telematics to limit tail concentration.

Calibrate premiums/reserves with actuarial, catastrophe and external data; Denmark population c. 5.9m (2024).

Fast FNOL, fraud analytics, subrogation and vendor controls shorten cycles and reduce leakage.

Manage capital via Solvency II monitoring, reinsurance and ALM stress tests to protect ratings.

| Metric | 2024 |

|---|---|

| Denmark pop. | 5.9m |

| Solvency II | >=100% |

What You See Is What You Get

Business Model Canvas

The Alm. Brand Business Model Canvas previewed here is the exact deliverable—not a mockup—and reflects the full document you will receive after purchase. Upon completing your order you’ll download the same professionally formatted file, ready to edit, present, and share. No placeholders, no surprises.