Alpha Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

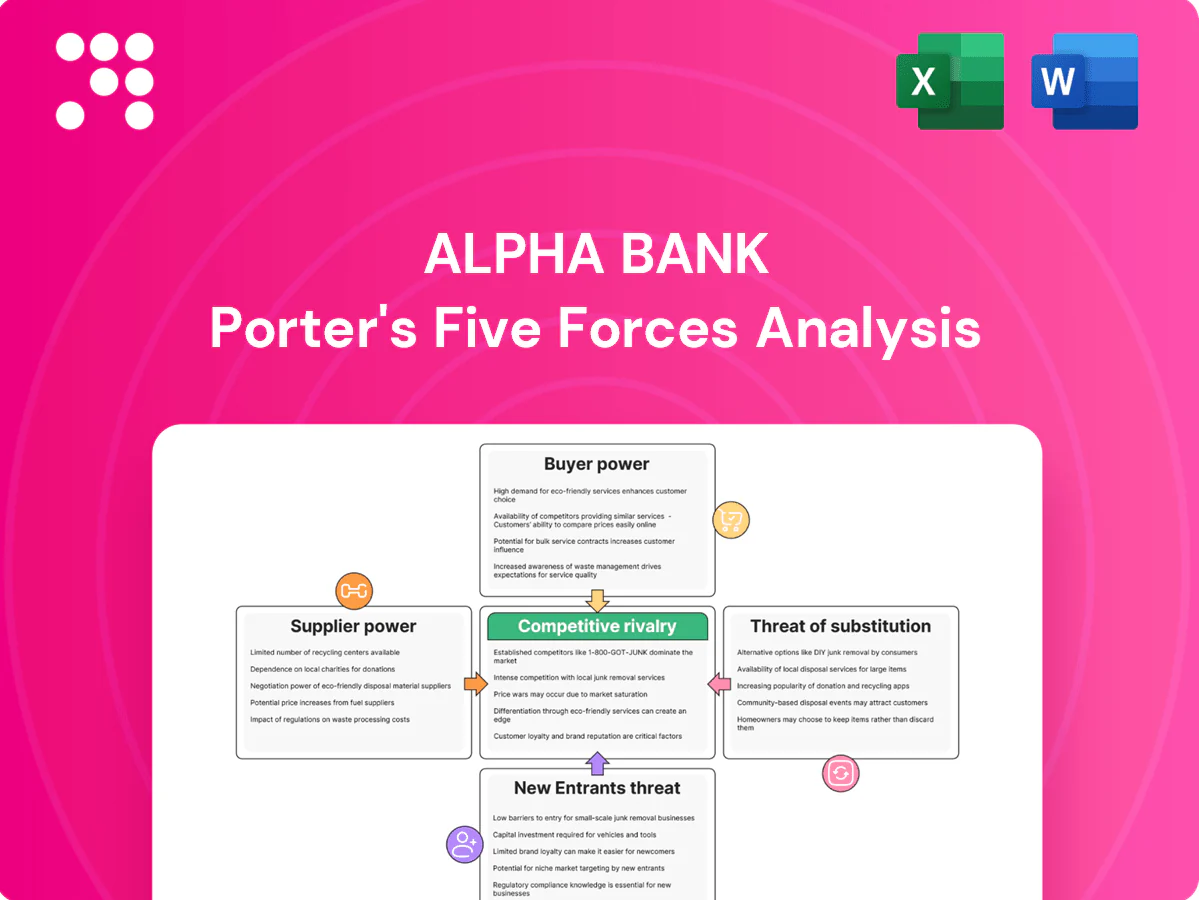

Alpha Bank faces intense competitive pressure from domestic banks, fintech entrants and shifting regulatory demands, while customer bargaining and digital disruption reshape margins and growth prospects. This snapshot highlights key tensions but stops short of force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get detailed scores, strategic implications, and ready-to-use charts for decision-making.

Suppliers Bargaining Power

Concentrated core-tech vendors

Alpha Bank relies on a small set of core-banking, cards and cloud vendors, giving suppliers leverage on pricing and contract terms; industry estimates put large core replacement projects at roughly €50–150m and 2–4 years, reinforcing vendor lock-in. Modular architectures and open APIs in 2024 are slowly widening alternatives, while multi-vendor strategies can meaningfully temper single-supplier power.

Wholesale and central bank funding

Market funding, covered bonds and ECB facilities remain key liquidity sources beyond deposits for Alpha Bank; reliance on ECB windows fell after 2023 deleveraging but can re-emerge in stress. In tight markets spreads widen—ECB deposit rate near 4.00% in mid-2024 and Greek 10y yield fell to about 3.2% by mid-2024—raising supplier power and squeezing NIMs. Strong liquidity buffers limit dependence on volatile funding windows.

Payment networks and processors

Card schemes and processors (Visa/Mastercard >80% share in Europe) set fees and technical standards, limiting Alpha Bank’s negotiating room. EU Interchange Fee Regulation caps consumer debit at 0.2% and credit at 0.3%, partly curbing supplier rents. Alpha’s volume scale gives marginal leverage on tiered pricing, and growth of SEPA Instant and alternative rails in 2024 is diversifying dependencies.

Data, cybersecurity, and regtech providers

Specialized data, AML/KYC and cybersecurity vendors are few and mission-critical for Alpha Bank, raising switching costs; the global regtech market was estimated at about $12.3 billion in 2024 (Statista) and vendor consolidation concentrates leverage.

EU rules such as DORA (effective 2025) and heightened AML supervision increase compliance intensity, strengthening supplier bargaining power and justifying premium pricing.

Multiyear contracts often lock in cost escalators and service dependencies, while selective in-house builds for data ingestion and KYC orchestration can partially rebalance power.

- DORA (effective 2025): raises supplier importance

- Regtech market 2024: ~$12.3bn (Statista)

- Few mission-critical vendors: high switching costs

- Long-term contracts: locked cost escalators

- In-house selective build: reduces reliance

Skilled talent and advisory services

Demand for risk, quant, tech and compliance talent in Greece and CEE outstrips local supply, fueling wage pressure; the 2024 global cybersecurity workforce gap remained about 3.4 million, highlighting scarcity in security and compliance skills. Global consultancies command pricing power on large transformation projects as the consulting market exceeded $330 billion in 2023–24. Hybrid work and nearshoring expand access to talent pools, while Alpha Bank's upskilling initiatives cut external-advisor reliance.

- Supply gap: cybersecurity workforce gap ~3.4M (2024)

- Consulting market: >$330B (2023–24)

- Mitigation: hybrid/nearshore hiring

- Strategy: internal upskilling reduces advisor spend

Supplier power strains Greek bank: core rebuild, card fees, cyber gaps

Alpha Bank faces strong supplier bargaining from core-banking, cards and cloud vendors (core replacement ~€50–150m, 2–4 yrs) and card schemes (Visa/Mastercard >80%; IFR caps debit 0.2% credit 0.3%). Market funding and ECB windows (deposit rate ~4.0% mid-2024; Greek 10y ~3.2% mid-2024) raise supplier leverage in stress. Regtech (~$12.3bn 2024), cybersecurity gap ~3.4M and consulting >$330bn (2023–24) concentrate vendor power; selective insourcing and multi-vendor/API strategies mitigate it.

| Metric | Value (2024) |

|---|---|

| Core replacement | €50–150m; 2–4 yrs |

| ECB deposit rate | ~4.0% |

| Greek 10y | ~3.2% |

| Regtech market | $12.3bn |

| Cyber workforce gap | ~3.4M |

| Consulting market | >$330bn |

| Visa/Mastercard share | >80% |

| IFR caps | Debit 0.2% / Credit 0.3% |

| DORA | Effective 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Alpha Bank that uncovers key drivers of competition, buyer/supplier power, entry risks and substitutes, identifies disruptive threats and protective market dynamics, and is ready for use in investor materials or strategy decks.

Clear, one-sheet Porter's Five Forces for Alpha Bank—instantly highlights competitive pressures and relief points for strategy decisions. Customize force levels, swap in your data, and drop the chart into decks or dashboards without macros for fast boardroom-ready insights.

Customers Bargaining Power

Rate-sensitive retail depositors

Rising euro-area rates in 2024 have heightened savers' price sensitivity, increasing deposit betas as customers chase yields.

Improved digital comparability and mobile banking reduce switching frictions across Greek banks, accelerating balance outflows to higher-yield offers.

Loyalty programs and bundled services partially damp churn, while EU deposit insurance of €100,000 limits panic-driven flight but cannot prevent yield-motivated moves.

Large corporates and institutions

Large corporates and institutions extract tighter spreads and fee waivers from Alpha Bank thanks to ticket size and multi-banking, and they can reallocate wallet share across lending, cash management and markets services. Deep relationships and ancillary flows—trade, FX and transaction volumes—are critical to defend margins. Syndication and capital markets alternatives further amplify their bargaining leverage.

SMEs with multi-banking options

SMEs with multi-banking options increasingly compare working capital, POS acquiring and fee packages via brokers and platforms, pressuring Alpha Bank on pricing and features. API-enabled onboarding, highlighted in 2024 Open Banking reports, lowers switching costs to hours for many clients, making churn easier. Bundled POS, payroll and digital tools can shift competition from price to stickiness, but access to credit remains the decisive factor for most SMEs.

Retail borrowers in a digital journey

PSD2 (effective 2018) and proliferating price-comparison platforms have raised mortgage and consumer-loan transparency; 78% of EU individuals used internet banking in 2023 (Eurostat), increasing digital shopping for loan offers. Rapid pre-approval and superior UX drive choice beyond headline APR, while cross-sell of cards and insurance can offset margin pressure; the bank's credit-risk appetite ultimately limits pricing concessions.

- PSD2: 2018 enables account-data portability

- 78% EU internet banking users (Eurostat 2023)

- Pre-approval speed and UX influence conversion

- Cross-sell offsets headline-rate pressure

- Credit-risk appetite caps pricing flexibility

Asset management and insurance clients

Asset management and insurance clients push Alpha Bank on fees as 2024 ETF average expense ratios fell to about 0.18% and global ETF AUM reached roughly 12.5 trillion USD, intensifying margin pressure. Bancassurance buyers rigorously compare coverage and claims service across carriers; strong performance and high-quality advice remain key pricing justifications. Enhanced PRIIPs/MiFID II disclosures in 2024 amplify buyer awareness and bargaining power.

- fees vs ETFs: 0.18% (2024)

- ETF AUM: ~12.5T USD (2024)

- claims & service: key switch drivers

- PRIIPs/MiFID II: higher transparency

Customers gain pricing power as EU digital banking 78% boosts switching

Customers' bargaining power is rising as 2024 euro-area rate increases and widespread internet banking (78% EU users, Eurostat 2023) make deposit switching yield-driven. Digital comparability, PSD2 and Open Banking lower friction, empowering SMEs and retail to demand better rates, fees and UX. Large corporates and asset clients push spreads and fees down, amplified by ETF fee compression (avg ER ~0.18%, AUM ~12.5T USD, 2024).

| Metric | Value |

|---|---|

| EU internet banking (2023) | 78% |

| EU deposit insurance | €100,000 |

| ETF avg ER (2024) | ~0.18% |

| Global ETF AUM (2024) | ~12.5T USD |

Preview the Actual Deliverable

Alpha Bank Porter's Five Forces Analysis

This Alpha Bank Porter's Five Forces Analysis preview is the exact document you'll receive immediately after purchase—no surprises or placeholders. It contains the full, professionally formatted assessment ready for download and use. Instant access is provided upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Alpha Bank faces intense competitive pressure from domestic banks, fintech entrants and shifting regulatory demands, while customer bargaining and digital disruption reshape margins and growth prospects. This snapshot highlights key tensions but stops short of force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get detailed scores, strategic implications, and ready-to-use charts for decision-making.

Suppliers Bargaining Power

Concentrated core-tech vendors

Alpha Bank relies on a small set of core-banking, cards and cloud vendors, giving suppliers leverage on pricing and contract terms; industry estimates put large core replacement projects at roughly €50–150m and 2–4 years, reinforcing vendor lock-in. Modular architectures and open APIs in 2024 are slowly widening alternatives, while multi-vendor strategies can meaningfully temper single-supplier power.

Wholesale and central bank funding

Market funding, covered bonds and ECB facilities remain key liquidity sources beyond deposits for Alpha Bank; reliance on ECB windows fell after 2023 deleveraging but can re-emerge in stress. In tight markets spreads widen—ECB deposit rate near 4.00% in mid-2024 and Greek 10y yield fell to about 3.2% by mid-2024—raising supplier power and squeezing NIMs. Strong liquidity buffers limit dependence on volatile funding windows.

Payment networks and processors

Card schemes and processors (Visa/Mastercard >80% share in Europe) set fees and technical standards, limiting Alpha Bank’s negotiating room. EU Interchange Fee Regulation caps consumer debit at 0.2% and credit at 0.3%, partly curbing supplier rents. Alpha’s volume scale gives marginal leverage on tiered pricing, and growth of SEPA Instant and alternative rails in 2024 is diversifying dependencies.

Data, cybersecurity, and regtech providers

Specialized data, AML/KYC and cybersecurity vendors are few and mission-critical for Alpha Bank, raising switching costs; the global regtech market was estimated at about $12.3 billion in 2024 (Statista) and vendor consolidation concentrates leverage.

EU rules such as DORA (effective 2025) and heightened AML supervision increase compliance intensity, strengthening supplier bargaining power and justifying premium pricing.

Multiyear contracts often lock in cost escalators and service dependencies, while selective in-house builds for data ingestion and KYC orchestration can partially rebalance power.

- DORA (effective 2025): raises supplier importance

- Regtech market 2024: ~$12.3bn (Statista)

- Few mission-critical vendors: high switching costs

- Long-term contracts: locked cost escalators

- In-house selective build: reduces reliance

Skilled talent and advisory services

Demand for risk, quant, tech and compliance talent in Greece and CEE outstrips local supply, fueling wage pressure; the 2024 global cybersecurity workforce gap remained about 3.4 million, highlighting scarcity in security and compliance skills. Global consultancies command pricing power on large transformation projects as the consulting market exceeded $330 billion in 2023–24. Hybrid work and nearshoring expand access to talent pools, while Alpha Bank's upskilling initiatives cut external-advisor reliance.

- Supply gap: cybersecurity workforce gap ~3.4M (2024)

- Consulting market: >$330B (2023–24)

- Mitigation: hybrid/nearshore hiring

- Strategy: internal upskilling reduces advisor spend

Supplier power strains Greek bank: core rebuild, card fees, cyber gaps

Alpha Bank faces strong supplier bargaining from core-banking, cards and cloud vendors (core replacement ~€50–150m, 2–4 yrs) and card schemes (Visa/Mastercard >80%; IFR caps debit 0.2% credit 0.3%). Market funding and ECB windows (deposit rate ~4.0% mid-2024; Greek 10y ~3.2% mid-2024) raise supplier leverage in stress. Regtech (~$12.3bn 2024), cybersecurity gap ~3.4M and consulting >$330bn (2023–24) concentrate vendor power; selective insourcing and multi-vendor/API strategies mitigate it.

| Metric | Value (2024) |

|---|---|

| Core replacement | €50–150m; 2–4 yrs |

| ECB deposit rate | ~4.0% |

| Greek 10y | ~3.2% |

| Regtech market | $12.3bn |

| Cyber workforce gap | ~3.4M |

| Consulting market | >$330bn |

| Visa/Mastercard share | >80% |

| IFR caps | Debit 0.2% / Credit 0.3% |

| DORA | Effective 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Alpha Bank that uncovers key drivers of competition, buyer/supplier power, entry risks and substitutes, identifies disruptive threats and protective market dynamics, and is ready for use in investor materials or strategy decks.

Clear, one-sheet Porter's Five Forces for Alpha Bank—instantly highlights competitive pressures and relief points for strategy decisions. Customize force levels, swap in your data, and drop the chart into decks or dashboards without macros for fast boardroom-ready insights.

Customers Bargaining Power

Rate-sensitive retail depositors

Rising euro-area rates in 2024 have heightened savers' price sensitivity, increasing deposit betas as customers chase yields.

Improved digital comparability and mobile banking reduce switching frictions across Greek banks, accelerating balance outflows to higher-yield offers.

Loyalty programs and bundled services partially damp churn, while EU deposit insurance of €100,000 limits panic-driven flight but cannot prevent yield-motivated moves.

Large corporates and institutions

Large corporates and institutions extract tighter spreads and fee waivers from Alpha Bank thanks to ticket size and multi-banking, and they can reallocate wallet share across lending, cash management and markets services. Deep relationships and ancillary flows—trade, FX and transaction volumes—are critical to defend margins. Syndication and capital markets alternatives further amplify their bargaining leverage.

SMEs with multi-banking options

SMEs with multi-banking options increasingly compare working capital, POS acquiring and fee packages via brokers and platforms, pressuring Alpha Bank on pricing and features. API-enabled onboarding, highlighted in 2024 Open Banking reports, lowers switching costs to hours for many clients, making churn easier. Bundled POS, payroll and digital tools can shift competition from price to stickiness, but access to credit remains the decisive factor for most SMEs.

Retail borrowers in a digital journey

PSD2 (effective 2018) and proliferating price-comparison platforms have raised mortgage and consumer-loan transparency; 78% of EU individuals used internet banking in 2023 (Eurostat), increasing digital shopping for loan offers. Rapid pre-approval and superior UX drive choice beyond headline APR, while cross-sell of cards and insurance can offset margin pressure; the bank's credit-risk appetite ultimately limits pricing concessions.

- PSD2: 2018 enables account-data portability

- 78% EU internet banking users (Eurostat 2023)

- Pre-approval speed and UX influence conversion

- Cross-sell offsets headline-rate pressure

- Credit-risk appetite caps pricing flexibility

Asset management and insurance clients

Asset management and insurance clients push Alpha Bank on fees as 2024 ETF average expense ratios fell to about 0.18% and global ETF AUM reached roughly 12.5 trillion USD, intensifying margin pressure. Bancassurance buyers rigorously compare coverage and claims service across carriers; strong performance and high-quality advice remain key pricing justifications. Enhanced PRIIPs/MiFID II disclosures in 2024 amplify buyer awareness and bargaining power.

- fees vs ETFs: 0.18% (2024)

- ETF AUM: ~12.5T USD (2024)

- claims & service: key switch drivers

- PRIIPs/MiFID II: higher transparency

Customers gain pricing power as EU digital banking 78% boosts switching

Customers' bargaining power is rising as 2024 euro-area rate increases and widespread internet banking (78% EU users, Eurostat 2023) make deposit switching yield-driven. Digital comparability, PSD2 and Open Banking lower friction, empowering SMEs and retail to demand better rates, fees and UX. Large corporates and asset clients push spreads and fees down, amplified by ETF fee compression (avg ER ~0.18%, AUM ~12.5T USD, 2024).

| Metric | Value |

|---|---|

| EU internet banking (2023) | 78% |

| EU deposit insurance | €100,000 |

| ETF avg ER (2024) | ~0.18% |

| Global ETF AUM (2024) | ~12.5T USD |

Preview the Actual Deliverable

Alpha Bank Porter's Five Forces Analysis

This Alpha Bank Porter's Five Forces Analysis preview is the exact document you'll receive immediately after purchase—no surprises or placeholders. It contains the full, professionally formatted assessment ready for download and use. Instant access is provided upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Alpha Bank faces intense competitive pressure from domestic banks, fintech entrants and shifting regulatory demands, while customer bargaining and digital disruption reshape margins and growth prospects. This snapshot highlights key tensions but stops short of force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get detailed scores, strategic implications, and ready-to-use charts for decision-making.

Suppliers Bargaining Power

Concentrated core-tech vendors

Alpha Bank relies on a small set of core-banking, cards and cloud vendors, giving suppliers leverage on pricing and contract terms; industry estimates put large core replacement projects at roughly €50–150m and 2–4 years, reinforcing vendor lock-in. Modular architectures and open APIs in 2024 are slowly widening alternatives, while multi-vendor strategies can meaningfully temper single-supplier power.

Wholesale and central bank funding

Market funding, covered bonds and ECB facilities remain key liquidity sources beyond deposits for Alpha Bank; reliance on ECB windows fell after 2023 deleveraging but can re-emerge in stress. In tight markets spreads widen—ECB deposit rate near 4.00% in mid-2024 and Greek 10y yield fell to about 3.2% by mid-2024—raising supplier power and squeezing NIMs. Strong liquidity buffers limit dependence on volatile funding windows.

Payment networks and processors

Card schemes and processors (Visa/Mastercard >80% share in Europe) set fees and technical standards, limiting Alpha Bank’s negotiating room. EU Interchange Fee Regulation caps consumer debit at 0.2% and credit at 0.3%, partly curbing supplier rents. Alpha’s volume scale gives marginal leverage on tiered pricing, and growth of SEPA Instant and alternative rails in 2024 is diversifying dependencies.

Data, cybersecurity, and regtech providers

Specialized data, AML/KYC and cybersecurity vendors are few and mission-critical for Alpha Bank, raising switching costs; the global regtech market was estimated at about $12.3 billion in 2024 (Statista) and vendor consolidation concentrates leverage.

EU rules such as DORA (effective 2025) and heightened AML supervision increase compliance intensity, strengthening supplier bargaining power and justifying premium pricing.

Multiyear contracts often lock in cost escalators and service dependencies, while selective in-house builds for data ingestion and KYC orchestration can partially rebalance power.

- DORA (effective 2025): raises supplier importance

- Regtech market 2024: ~$12.3bn (Statista)

- Few mission-critical vendors: high switching costs

- Long-term contracts: locked cost escalators

- In-house selective build: reduces reliance

Skilled talent and advisory services

Demand for risk, quant, tech and compliance talent in Greece and CEE outstrips local supply, fueling wage pressure; the 2024 global cybersecurity workforce gap remained about 3.4 million, highlighting scarcity in security and compliance skills. Global consultancies command pricing power on large transformation projects as the consulting market exceeded $330 billion in 2023–24. Hybrid work and nearshoring expand access to talent pools, while Alpha Bank's upskilling initiatives cut external-advisor reliance.

- Supply gap: cybersecurity workforce gap ~3.4M (2024)

- Consulting market: >$330B (2023–24)

- Mitigation: hybrid/nearshore hiring

- Strategy: internal upskilling reduces advisor spend

Supplier power strains Greek bank: core rebuild, card fees, cyber gaps

Alpha Bank faces strong supplier bargaining from core-banking, cards and cloud vendors (core replacement ~€50–150m, 2–4 yrs) and card schemes (Visa/Mastercard >80%; IFR caps debit 0.2% credit 0.3%). Market funding and ECB windows (deposit rate ~4.0% mid-2024; Greek 10y ~3.2% mid-2024) raise supplier leverage in stress. Regtech (~$12.3bn 2024), cybersecurity gap ~3.4M and consulting >$330bn (2023–24) concentrate vendor power; selective insourcing and multi-vendor/API strategies mitigate it.

| Metric | Value (2024) |

|---|---|

| Core replacement | €50–150m; 2–4 yrs |

| ECB deposit rate | ~4.0% |

| Greek 10y | ~3.2% |

| Regtech market | $12.3bn |

| Cyber workforce gap | ~3.4M |

| Consulting market | >$330bn |

| Visa/Mastercard share | >80% |

| IFR caps | Debit 0.2% / Credit 0.3% |

| DORA | Effective 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Alpha Bank that uncovers key drivers of competition, buyer/supplier power, entry risks and substitutes, identifies disruptive threats and protective market dynamics, and is ready for use in investor materials or strategy decks.

Clear, one-sheet Porter's Five Forces for Alpha Bank—instantly highlights competitive pressures and relief points for strategy decisions. Customize force levels, swap in your data, and drop the chart into decks or dashboards without macros for fast boardroom-ready insights.

Customers Bargaining Power

Rate-sensitive retail depositors

Rising euro-area rates in 2024 have heightened savers' price sensitivity, increasing deposit betas as customers chase yields.

Improved digital comparability and mobile banking reduce switching frictions across Greek banks, accelerating balance outflows to higher-yield offers.

Loyalty programs and bundled services partially damp churn, while EU deposit insurance of €100,000 limits panic-driven flight but cannot prevent yield-motivated moves.

Large corporates and institutions

Large corporates and institutions extract tighter spreads and fee waivers from Alpha Bank thanks to ticket size and multi-banking, and they can reallocate wallet share across lending, cash management and markets services. Deep relationships and ancillary flows—trade, FX and transaction volumes—are critical to defend margins. Syndication and capital markets alternatives further amplify their bargaining leverage.

SMEs with multi-banking options

SMEs with multi-banking options increasingly compare working capital, POS acquiring and fee packages via brokers and platforms, pressuring Alpha Bank on pricing and features. API-enabled onboarding, highlighted in 2024 Open Banking reports, lowers switching costs to hours for many clients, making churn easier. Bundled POS, payroll and digital tools can shift competition from price to stickiness, but access to credit remains the decisive factor for most SMEs.

Retail borrowers in a digital journey

PSD2 (effective 2018) and proliferating price-comparison platforms have raised mortgage and consumer-loan transparency; 78% of EU individuals used internet banking in 2023 (Eurostat), increasing digital shopping for loan offers. Rapid pre-approval and superior UX drive choice beyond headline APR, while cross-sell of cards and insurance can offset margin pressure; the bank's credit-risk appetite ultimately limits pricing concessions.

- PSD2: 2018 enables account-data portability

- 78% EU internet banking users (Eurostat 2023)

- Pre-approval speed and UX influence conversion

- Cross-sell offsets headline-rate pressure

- Credit-risk appetite caps pricing flexibility

Asset management and insurance clients

Asset management and insurance clients push Alpha Bank on fees as 2024 ETF average expense ratios fell to about 0.18% and global ETF AUM reached roughly 12.5 trillion USD, intensifying margin pressure. Bancassurance buyers rigorously compare coverage and claims service across carriers; strong performance and high-quality advice remain key pricing justifications. Enhanced PRIIPs/MiFID II disclosures in 2024 amplify buyer awareness and bargaining power.

- fees vs ETFs: 0.18% (2024)

- ETF AUM: ~12.5T USD (2024)

- claims & service: key switch drivers

- PRIIPs/MiFID II: higher transparency

Customers gain pricing power as EU digital banking 78% boosts switching

Customers' bargaining power is rising as 2024 euro-area rate increases and widespread internet banking (78% EU users, Eurostat 2023) make deposit switching yield-driven. Digital comparability, PSD2 and Open Banking lower friction, empowering SMEs and retail to demand better rates, fees and UX. Large corporates and asset clients push spreads and fees down, amplified by ETF fee compression (avg ER ~0.18%, AUM ~12.5T USD, 2024).

| Metric | Value |

|---|---|

| EU internet banking (2023) | 78% |

| EU deposit insurance | €100,000 |

| ETF avg ER (2024) | ~0.18% |

| Global ETF AUM (2024) | ~12.5T USD |

Preview the Actual Deliverable

Alpha Bank Porter's Five Forces Analysis

This Alpha Bank Porter's Five Forces Analysis preview is the exact document you'll receive immediately after purchase—no surprises or placeholders. It contains the full, professionally formatted assessment ready for download and use. Instant access is provided upon payment.