Alsea SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Alsea’s SWOT analysis highlights strong brand portfolios and regional scale but also exposes margin pressure from commodity costs and competitive retail dynamics; we unpack how these forces shape growth and risk. Want the full story behind its strengths, weaknesses, opportunities, and threats? Purchase the complete SWOT analysis to get a research-backed, editable Word report and Excel matrix—ideal for investors, strategists, and advisors.

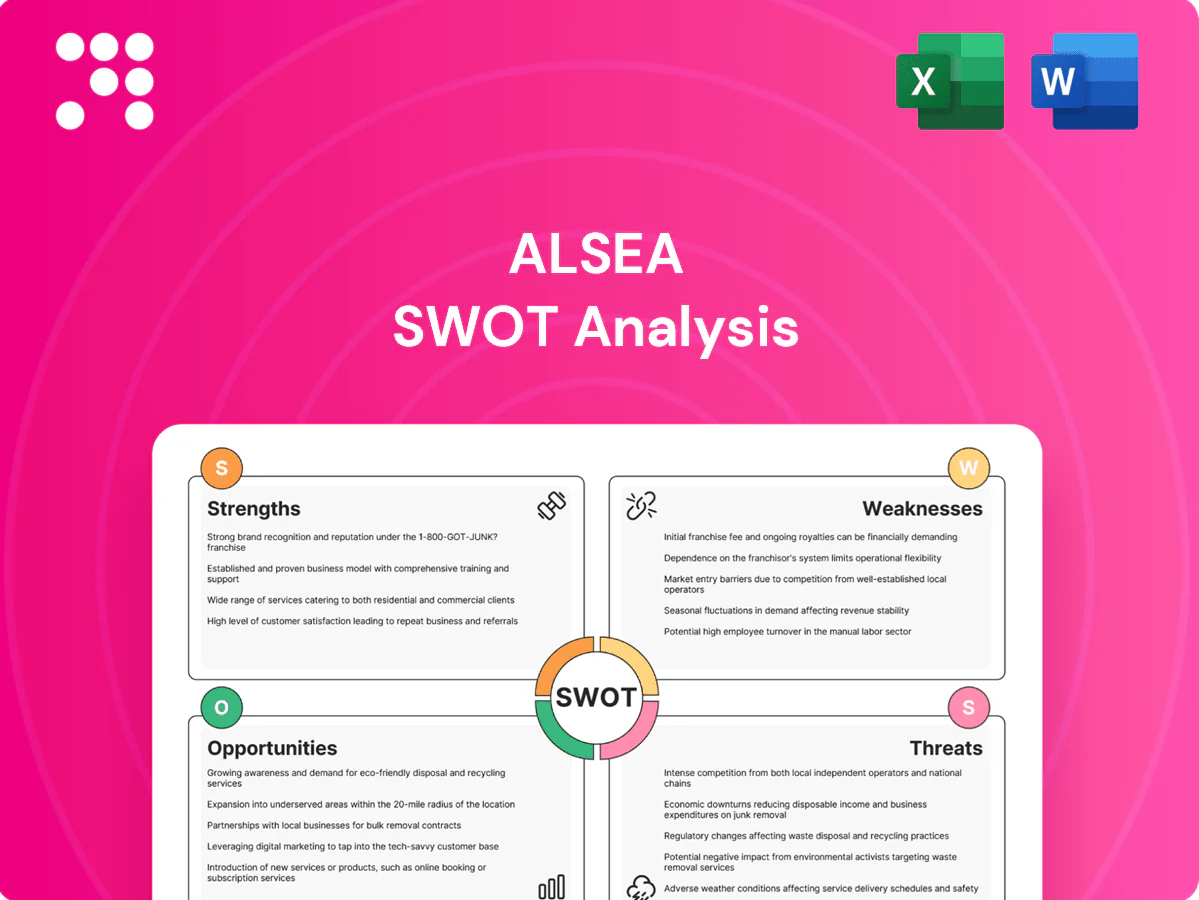

Strengths

Diversified brands

Operating Starbucks, Domino's, Burger King and Chili's lets Alsea spread demand across coffee, delivery, quick‑service and casual dining, reducing reliance on any single concept; with over 4,300 restaurants across 9 countries in 2024 this portfolio enabled rapid rollouts and adoption. Cross-learning of QSR and casual dining best practices improves unit economics and same‑store performance.

Scale in core regions

Alsea's scale—over 4,800 restaurants across 10 countries—drives purchasing power and marketing efficiency, lowering input costs and boosting ROI on promotions. Centralized supply, technology platforms and training hubs support consistent operations and unit economics, helping margins withstand localized shocks. Broad regional presence strengthens bargaining with landlords and delivery aggregators, improving rent and commission terms.

Operational playbooks

Alsea’s operational playbooks support rapid rollouts and turnarounds across its 4,000+ restaurants in 9 countries, accelerating openings and fixes. Standardized processes deliver consistent customer experiences across brands and formats. Data-driven labor and inventory management raises throughput and improves margins. Continuous improvement programs tighten cost control and boost service quality.

Mixed ownership model

Alsea's mixed ownership model combines company-operated and franchised stores to balance growth and returns, with ~5,800 stores and MXN 88.1 billion revenue in 2023 supporting scale and cash generation. Company-owned units demonstrate execution and pilot innovations across markets, while franchising accelerates expansion with lower capital intensity and franchisees funding local rollouts. The mix diversifies cash flows and risk profiles across countries and brands.

- Scale: ~5,800 stores (2023)

- Revenue: MXN 88.1 billion (2023)

- Franchise-led expansion: lower capex, faster openings

- Cash-flow diversification across ownership types

Digital and delivery

Alsea leverages strong delivery, mobile ordering and cross-brand loyalty to lift visit frequency and tickets, while shared tech stacks reduce friction and enable personalized offers. Partnerships with aggregators expand reach as first-party channels preserve margins, and centralized data analytics inform pricing, promotions and site selection.

- Delivery + mobile ordering drive frequency

- Shared tech stacks enable personalization

- Aggregator partnerships widen reach; first-party protects margins

- Data guides pricing, promos, site selection

Multi-brand restaurant operator: MXN 88.1 bn revenue, ~5,800 stores (2023)

Alsea’s diversified portfolio (Starbucks, Domino’s, Burger King, Chili’s) and omni‑channel delivery reduce concept risk and boost throughput, supporting MXN 88.1 billion revenue and ~5,800 stores in 2023 across 10 countries. Scale lowers input costs and improves marketing ROI, while mixed company/franchise model accelerates low‑capex growth and steady cash flows.

| Metric | Value (2023) |

|---|---|

| Stores | ~5,800 |

| Revenue | MXN 88.1 bn |

| Countries | 10 |

What is included in the product

Provides a clear SWOT framework for analyzing Alsea’s business strategy, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and growth prospects.

Provides a concise Alsea SWOT matrix for fast alignment of franchise and portfolio strategies, highlighting strengths, weaknesses, opportunities and threats to quickly relieve decision-making bottlenecks and support executive prioritization.

Weaknesses

Licensor dependence

Alsea relies on franchise and license agreements for global names such as Starbucks, Domino's and Burger King, exposing margins to changes in royalty rates, territory fees and contract terms. With operations across 10+ countries and over 4,000 restaurants managing 20+ brands, limited control over brand strategy can restrict local adaptation. Renewal and renegotiation risk creates uncertainty for long‑term planning and profitability.

FX and macro exposure

Revenue and costs span multiple currencies and inflation regimes across Mexico, Spain and several Latin American markets, making margins sensitive to devaluations and rising prices. Currency devaluations and high local inflation have historically compressed retail margins and distorted cross-country comparables. Hedging programs mitigate but are imperfect and can incur significant costs. Consumer downturns in key markets reduce same-store sales and slow new openings.

Thin unit margins

Alsea faces thin unit margins as restaurants operate under tight labor, rent and commodity cost structures that leave little room for error; small execution lapses can materially cut profitability. High delivery mix exposes units to platform commissions, often running 15–30% per order, diluting margins. Raising prices risks negative demand elasticity and potential damage to premium brand perception, limiting pass-through ability.

Capital and leases

Expansion and remodels require sustained capital expenditure, pressuring cash flow and constraining free cash for other initiatives.

Long-term lease commitments elevate fixed costs and operational leverage, while underperforming sites are expensive to exit or restructure due to breakage and contractual penalties.

Balance sheet flexibility can tighten in downturns, increasing refinancing and liquidity risk for the group.

- Capex intensity

- High fixed lease obligations

- Costly site exits/restructures

- Liquidity/refinancing risk

Complex operations

- 9 countries footprint

- thousands of outlets

- integration delays → reporting lag

- execution variability → inconsistent guest experience

Franchise-focused chain faces margin squeeze from royalties, FX volatility, commissions and leases

Alsea's reliance on franchise and licence deals across ~9 countries and ~4,000 outlets managing 20+ brands concentrates margin risk to royalties and renewals. Currency volatility and high inflation in key markets compress margins; delivery commissions (15–30%) and tight labor/rent costs leave thin unit margins. High capex and long leases raise leverage and refinancing risk, while integration strain causes execution variability.

| Metric | Value |

|---|---|

| Countries | ~9 |

| Outlets | ~4,000 |

| Brands | 20+ |

| Delivery commissions | 15–30% |

| Key risks | Capex, leases, FX, renewals |

What You See Is What You Get

Alsea SWOT Analysis

This is the actual SWOT analysis document for Alsea that you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report. Buy now to unlock the complete, editable version with in-depth strengths, weaknesses, opportunities and threats.

Dive Deeper Into the Company’s Strategic Blueprint

Alsea’s SWOT analysis highlights strong brand portfolios and regional scale but also exposes margin pressure from commodity costs and competitive retail dynamics; we unpack how these forces shape growth and risk. Want the full story behind its strengths, weaknesses, opportunities, and threats? Purchase the complete SWOT analysis to get a research-backed, editable Word report and Excel matrix—ideal for investors, strategists, and advisors.

Strengths

Diversified brands

Operating Starbucks, Domino's, Burger King and Chili's lets Alsea spread demand across coffee, delivery, quick‑service and casual dining, reducing reliance on any single concept; with over 4,300 restaurants across 9 countries in 2024 this portfolio enabled rapid rollouts and adoption. Cross-learning of QSR and casual dining best practices improves unit economics and same‑store performance.

Scale in core regions

Alsea's scale—over 4,800 restaurants across 10 countries—drives purchasing power and marketing efficiency, lowering input costs and boosting ROI on promotions. Centralized supply, technology platforms and training hubs support consistent operations and unit economics, helping margins withstand localized shocks. Broad regional presence strengthens bargaining with landlords and delivery aggregators, improving rent and commission terms.

Operational playbooks

Alsea’s operational playbooks support rapid rollouts and turnarounds across its 4,000+ restaurants in 9 countries, accelerating openings and fixes. Standardized processes deliver consistent customer experiences across brands and formats. Data-driven labor and inventory management raises throughput and improves margins. Continuous improvement programs tighten cost control and boost service quality.

Mixed ownership model

Alsea's mixed ownership model combines company-operated and franchised stores to balance growth and returns, with ~5,800 stores and MXN 88.1 billion revenue in 2023 supporting scale and cash generation. Company-owned units demonstrate execution and pilot innovations across markets, while franchising accelerates expansion with lower capital intensity and franchisees funding local rollouts. The mix diversifies cash flows and risk profiles across countries and brands.

- Scale: ~5,800 stores (2023)

- Revenue: MXN 88.1 billion (2023)

- Franchise-led expansion: lower capex, faster openings

- Cash-flow diversification across ownership types

Digital and delivery

Alsea leverages strong delivery, mobile ordering and cross-brand loyalty to lift visit frequency and tickets, while shared tech stacks reduce friction and enable personalized offers. Partnerships with aggregators expand reach as first-party channels preserve margins, and centralized data analytics inform pricing, promotions and site selection.

- Delivery + mobile ordering drive frequency

- Shared tech stacks enable personalization

- Aggregator partnerships widen reach; first-party protects margins

- Data guides pricing, promos, site selection

Multi-brand restaurant operator: MXN 88.1 bn revenue, ~5,800 stores (2023)

Alsea’s diversified portfolio (Starbucks, Domino’s, Burger King, Chili’s) and omni‑channel delivery reduce concept risk and boost throughput, supporting MXN 88.1 billion revenue and ~5,800 stores in 2023 across 10 countries. Scale lowers input costs and improves marketing ROI, while mixed company/franchise model accelerates low‑capex growth and steady cash flows.

| Metric | Value (2023) |

|---|---|

| Stores | ~5,800 |

| Revenue | MXN 88.1 bn |

| Countries | 10 |

What is included in the product

Provides a clear SWOT framework for analyzing Alsea’s business strategy, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and growth prospects.

Provides a concise Alsea SWOT matrix for fast alignment of franchise and portfolio strategies, highlighting strengths, weaknesses, opportunities and threats to quickly relieve decision-making bottlenecks and support executive prioritization.

Weaknesses

Licensor dependence

Alsea relies on franchise and license agreements for global names such as Starbucks, Domino's and Burger King, exposing margins to changes in royalty rates, territory fees and contract terms. With operations across 10+ countries and over 4,000 restaurants managing 20+ brands, limited control over brand strategy can restrict local adaptation. Renewal and renegotiation risk creates uncertainty for long‑term planning and profitability.

FX and macro exposure

Revenue and costs span multiple currencies and inflation regimes across Mexico, Spain and several Latin American markets, making margins sensitive to devaluations and rising prices. Currency devaluations and high local inflation have historically compressed retail margins and distorted cross-country comparables. Hedging programs mitigate but are imperfect and can incur significant costs. Consumer downturns in key markets reduce same-store sales and slow new openings.

Thin unit margins

Alsea faces thin unit margins as restaurants operate under tight labor, rent and commodity cost structures that leave little room for error; small execution lapses can materially cut profitability. High delivery mix exposes units to platform commissions, often running 15–30% per order, diluting margins. Raising prices risks negative demand elasticity and potential damage to premium brand perception, limiting pass-through ability.

Capital and leases

Expansion and remodels require sustained capital expenditure, pressuring cash flow and constraining free cash for other initiatives.

Long-term lease commitments elevate fixed costs and operational leverage, while underperforming sites are expensive to exit or restructure due to breakage and contractual penalties.

Balance sheet flexibility can tighten in downturns, increasing refinancing and liquidity risk for the group.

- Capex intensity

- High fixed lease obligations

- Costly site exits/restructures

- Liquidity/refinancing risk

Complex operations

- 9 countries footprint

- thousands of outlets

- integration delays → reporting lag

- execution variability → inconsistent guest experience

Franchise-focused chain faces margin squeeze from royalties, FX volatility, commissions and leases

Alsea's reliance on franchise and licence deals across ~9 countries and ~4,000 outlets managing 20+ brands concentrates margin risk to royalties and renewals. Currency volatility and high inflation in key markets compress margins; delivery commissions (15–30%) and tight labor/rent costs leave thin unit margins. High capex and long leases raise leverage and refinancing risk, while integration strain causes execution variability.

| Metric | Value |

|---|---|

| Countries | ~9 |

| Outlets | ~4,000 |

| Brands | 20+ |

| Delivery commissions | 15–30% |

| Key risks | Capex, leases, FX, renewals |

What You See Is What You Get

Alsea SWOT Analysis

This is the actual SWOT analysis document for Alsea that you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report. Buy now to unlock the complete, editable version with in-depth strengths, weaknesses, opportunities and threats.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Alsea’s SWOT analysis highlights strong brand portfolios and regional scale but also exposes margin pressure from commodity costs and competitive retail dynamics; we unpack how these forces shape growth and risk. Want the full story behind its strengths, weaknesses, opportunities, and threats? Purchase the complete SWOT analysis to get a research-backed, editable Word report and Excel matrix—ideal for investors, strategists, and advisors.

Strengths

Diversified brands

Operating Starbucks, Domino's, Burger King and Chili's lets Alsea spread demand across coffee, delivery, quick‑service and casual dining, reducing reliance on any single concept; with over 4,300 restaurants across 9 countries in 2024 this portfolio enabled rapid rollouts and adoption. Cross-learning of QSR and casual dining best practices improves unit economics and same‑store performance.

Scale in core regions

Alsea's scale—over 4,800 restaurants across 10 countries—drives purchasing power and marketing efficiency, lowering input costs and boosting ROI on promotions. Centralized supply, technology platforms and training hubs support consistent operations and unit economics, helping margins withstand localized shocks. Broad regional presence strengthens bargaining with landlords and delivery aggregators, improving rent and commission terms.

Operational playbooks

Alsea’s operational playbooks support rapid rollouts and turnarounds across its 4,000+ restaurants in 9 countries, accelerating openings and fixes. Standardized processes deliver consistent customer experiences across brands and formats. Data-driven labor and inventory management raises throughput and improves margins. Continuous improvement programs tighten cost control and boost service quality.

Mixed ownership model

Alsea's mixed ownership model combines company-operated and franchised stores to balance growth and returns, with ~5,800 stores and MXN 88.1 billion revenue in 2023 supporting scale and cash generation. Company-owned units demonstrate execution and pilot innovations across markets, while franchising accelerates expansion with lower capital intensity and franchisees funding local rollouts. The mix diversifies cash flows and risk profiles across countries and brands.

- Scale: ~5,800 stores (2023)

- Revenue: MXN 88.1 billion (2023)

- Franchise-led expansion: lower capex, faster openings

- Cash-flow diversification across ownership types

Digital and delivery

Alsea leverages strong delivery, mobile ordering and cross-brand loyalty to lift visit frequency and tickets, while shared tech stacks reduce friction and enable personalized offers. Partnerships with aggregators expand reach as first-party channels preserve margins, and centralized data analytics inform pricing, promotions and site selection.

- Delivery + mobile ordering drive frequency

- Shared tech stacks enable personalization

- Aggregator partnerships widen reach; first-party protects margins

- Data guides pricing, promos, site selection

Multi-brand restaurant operator: MXN 88.1 bn revenue, ~5,800 stores (2023)

Alsea’s diversified portfolio (Starbucks, Domino’s, Burger King, Chili’s) and omni‑channel delivery reduce concept risk and boost throughput, supporting MXN 88.1 billion revenue and ~5,800 stores in 2023 across 10 countries. Scale lowers input costs and improves marketing ROI, while mixed company/franchise model accelerates low‑capex growth and steady cash flows.

| Metric | Value (2023) |

|---|---|

| Stores | ~5,800 |

| Revenue | MXN 88.1 bn |

| Countries | 10 |

What is included in the product

Provides a clear SWOT framework for analyzing Alsea’s business strategy, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and growth prospects.

Provides a concise Alsea SWOT matrix for fast alignment of franchise and portfolio strategies, highlighting strengths, weaknesses, opportunities and threats to quickly relieve decision-making bottlenecks and support executive prioritization.

Weaknesses

Licensor dependence

Alsea relies on franchise and license agreements for global names such as Starbucks, Domino's and Burger King, exposing margins to changes in royalty rates, territory fees and contract terms. With operations across 10+ countries and over 4,000 restaurants managing 20+ brands, limited control over brand strategy can restrict local adaptation. Renewal and renegotiation risk creates uncertainty for long‑term planning and profitability.

FX and macro exposure

Revenue and costs span multiple currencies and inflation regimes across Mexico, Spain and several Latin American markets, making margins sensitive to devaluations and rising prices. Currency devaluations and high local inflation have historically compressed retail margins and distorted cross-country comparables. Hedging programs mitigate but are imperfect and can incur significant costs. Consumer downturns in key markets reduce same-store sales and slow new openings.

Thin unit margins

Alsea faces thin unit margins as restaurants operate under tight labor, rent and commodity cost structures that leave little room for error; small execution lapses can materially cut profitability. High delivery mix exposes units to platform commissions, often running 15–30% per order, diluting margins. Raising prices risks negative demand elasticity and potential damage to premium brand perception, limiting pass-through ability.

Capital and leases

Expansion and remodels require sustained capital expenditure, pressuring cash flow and constraining free cash for other initiatives.

Long-term lease commitments elevate fixed costs and operational leverage, while underperforming sites are expensive to exit or restructure due to breakage and contractual penalties.

Balance sheet flexibility can tighten in downturns, increasing refinancing and liquidity risk for the group.

- Capex intensity

- High fixed lease obligations

- Costly site exits/restructures

- Liquidity/refinancing risk

Complex operations

- 9 countries footprint

- thousands of outlets

- integration delays → reporting lag

- execution variability → inconsistent guest experience

Franchise-focused chain faces margin squeeze from royalties, FX volatility, commissions and leases

Alsea's reliance on franchise and licence deals across ~9 countries and ~4,000 outlets managing 20+ brands concentrates margin risk to royalties and renewals. Currency volatility and high inflation in key markets compress margins; delivery commissions (15–30%) and tight labor/rent costs leave thin unit margins. High capex and long leases raise leverage and refinancing risk, while integration strain causes execution variability.

| Metric | Value |

|---|---|

| Countries | ~9 |

| Outlets | ~4,000 |

| Brands | 20+ |

| Delivery commissions | 15–30% |

| Key risks | Capex, leases, FX, renewals |

What You See Is What You Get

Alsea SWOT Analysis

This is the actual SWOT analysis document for Alsea that you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report. Buy now to unlock the complete, editable version with in-depth strengths, weaknesses, opportunities and threats.