Altron Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Altron faces moderate buyer power, supplier concentration in tech inputs, and rising competitive intensity from local and global IT services firms; substitutes and regulatory shifts also shape margins. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore Altron’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on global OEMs

Altron depends on major OEMs like Microsoft, Cisco and hyperscalers for core licenses and hardware, leaving it exposed to supplier pricing power and roadmap control. Microsoft and AWS held roughly 23% and 32% global cloud market share in 2024, underscoring hyperscaler influence. Partner tiering and certification rules constrain discounting, and losing a top OEM badge would materially raise procurement costs and weaken competitive bids.

Specialist talent and subcontractors

Scarce skills in cybersecurity, cloud and data engineering drove a 2024 estimated global cyber workforce gap of ~3.5 million, pushing niche partner rates and reported premiums up to 40% versus general IT suppliers. Limited subcontractor pools lengthen delivery lead times and raise SLA breach risk, with 60%+ of firms citing resource constraints in 2024 surveys. Concentration in a few boutiques raises switching costs; building internal bench reduces supplier leverage but increases fixed payroll and training expense.

Hardware and semiconductor exposure

Global supply volatility continues to delay infrastructure rollouts and inflate hardware costs, with lead times for networking, servers and endpoints running about 12–16 weeks in 2024, shifting bargaining power toward upstream suppliers. Currency swings in South Africa amplify import pricing pressure, and buffer inventory plus multi-vendor designs mitigate but do not fully neutralize supplier leverage.

Carrier and data center dependencies

Carrier and colocation providers (notably large operators in 2024) drive service quality and bundled pricing for Altron, with limited regional alternatives amplifying supplier leverage; cross-connect and egress fees remain recurring cost drivers and can be sticky. Long-term carrier contracts mitigate short-term price shocks but lock Altron into fixed terms and capacity commitments.

- Regional scarcity increases supplier leverage

- Cross-connect/egress fees = recurring cost pressure

- Long-term contracts = price stability but reduced flexibility

Standards and interoperability

Open standards lower supplier power by easing vendor switching and reducing integration costs; in 2024 firms with API-first strategies cut average integration time by roughly 30%, tightening competitive sourcing. Proprietary ecosystems and vendor certifications can re-tighten lock-in, raising renewal margins and switching costs. Mature APIs reduce Altron's integration expense, while enterprise-wide agreements across portfolios can rebalance supplier bargaining.

- Open standards: lower switching costs

- Proprietary ecosystems: increase lock-in

- API maturity: cuts integration time ~30% (2024)

- Enterprise agreements: rebalance supplier leverage

Hyperscaler dominance, cyber skills gap and long hardware lead times squeeze margins

Altron faces strong supplier power from OEMs and hyperscalers (Microsoft ~23%, AWS ~32% global cloud share in 2024), raising price and roadmap exposure. Cyber skills gap (~3.5M global in 2024) and 12–16 week hardware lead times boost niche supplier premiums and delivery risk. Carrier egress fees and long contracts create recurring cost stickiness.

| Metric | 2024 |

|---|---|

| Hyperscaler share | MS 23% / AWS 32% |

| Cyber workforce gap | ~3.5M |

| Hardware lead times | 12–16 weeks |

What is included in the product

Concise Porter's Five Forces assessment of Altron that uncovers competitive drivers, supplier and buyer power, barriers to entry, substitution risks, and strategic implications for market positioning.

A concise one-sheet Porter's Five Forces for Altron that maps supplier, buyer, rivalry, substitutes and entrant pressures—delivering slide-ready clarity for fast strategic decisions and stakeholder briefings.

Customers Bargaining Power

Enterprise and public-sector procurement

Enterprise and public-sector procurement runs competitive RFPs that push Altron to offer volume discounts and tiered pricing, with framework agreements and rate cards intensifying price pressure. In 2024, public-sector demand remained a primary IT-services driver, and compliance and localization clauses are routinely leveraged to extract concessions. Multi-year deals are used to trade margin for revenue stability and predictable cash flow.

Switching costs versus integration lock-in

Deeply integrated managed services raise exit costs and can blunt buyer power—with the global managed services market exceeding $250 billion in 2024 many contracts embed proprietary integrations that increase switching friction. Yet standard cloud stacks and multi-cloud strategies (92% of enterprises in Flexera 2024) make components more swappable, encouraging unbundling to best-of-breed. Clear SLAs, runbooks and data portability clauses lower perceived switching risk and shift leverage back to buyers.

Outcome-based and SLA penalties

By 2024 clients increasingly demand outcome-based fees and SLA credits, often tying 5–10% of contract value to performance, shifting risk to Altron and compressing margins when delivery slips. High-visibility KPIs give buyers leverage in renegotiations, enabling clawbacks or rate resets. Strong governance, contract clauses and automation of delivery and monitoring can protect Altron’s economics and limit downside.

Insourcing and captive centers

Larger organisations increasingly insource digital capability as an alternative to vendors; Gartner 2024 reports worldwide IT spending near 4.7 trillion USD, underpinning internal build investments. Talent availability and local cost differentials dictate feasibility and bargaining stance. Hybrid models retain external leverage while capping spend growth; Altron must demonstrate superior time-to-value to defend pricing.

- Insourcing trend: internal teams vs vendors

- Resource cost and availability drive leverage

- Hybrid model: preserves vendor leverage, limits spend

- Altron must prove faster time-to-value

Demand for end-to-end solutions

Buyers increasingly favor consolidated partners that bundle infrastructure, software and services, which can lift deal sizes while concentrating negotiating leverage with large enterprise clients. Successful cross-selling depends on clear, demonstrable integration benefits and measurable ROI to overcome switching risk. Strong referenceability and vertical expertise often tip procurement decisions in favor of integrated providers.

- Consolidation boosts deal size

- Concentrates buyer power

- Cross-sell needs measurable integration ROI

- Referenceability and vertical expertise decisive

Price squeeze: $250B+ managed services lock-in, 92% multi-cloud, 5–10% SLA fees

Public RFPs and framework discounts tightened price pressure in 2024. Managed services scale (>250B market 2024) raises switching costs but 92% multi-cloud adoption enables unbundling. Buyers tie 5–10% of fees to SLAs, shifting risk and compressing margins.

| Metric | 2024 |

|---|---|

| Managed services market | $250B+ |

| Multi-cloud adoption (Flexera) | 92% |

| SLA-linked fees | 5–10% |

Same Document Delivered

Altron Porter's Five Forces Analysis

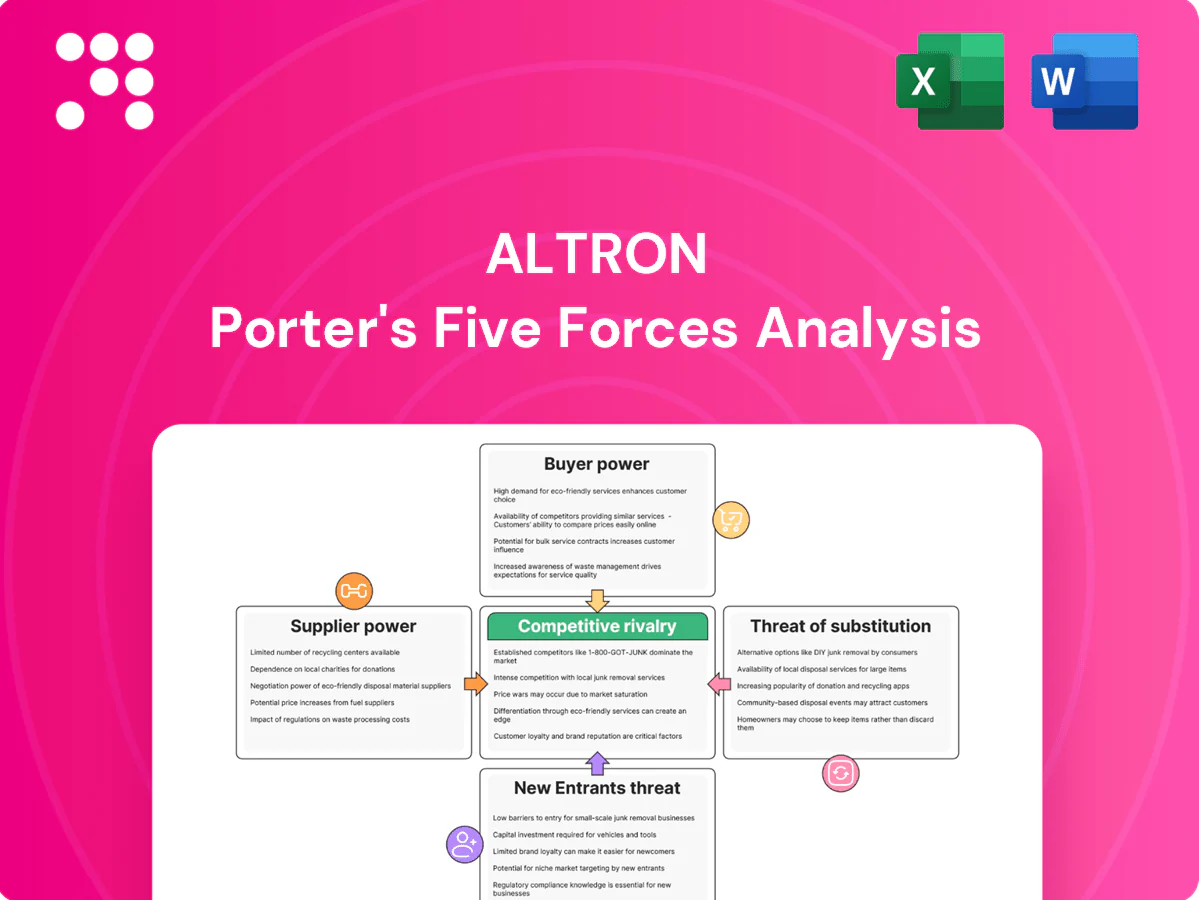

This preview shows the exact Altron Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The file is fully formatted and ready for use, containing supplier and buyer power, competitive rivalry, threat of entry, and substitutes insights. You'll get instant access to this exact document upon payment.

A Must-Have Tool for Decision-Makers

Altron faces moderate buyer power, supplier concentration in tech inputs, and rising competitive intensity from local and global IT services firms; substitutes and regulatory shifts also shape margins. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore Altron’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on global OEMs

Altron depends on major OEMs like Microsoft, Cisco and hyperscalers for core licenses and hardware, leaving it exposed to supplier pricing power and roadmap control. Microsoft and AWS held roughly 23% and 32% global cloud market share in 2024, underscoring hyperscaler influence. Partner tiering and certification rules constrain discounting, and losing a top OEM badge would materially raise procurement costs and weaken competitive bids.

Specialist talent and subcontractors

Scarce skills in cybersecurity, cloud and data engineering drove a 2024 estimated global cyber workforce gap of ~3.5 million, pushing niche partner rates and reported premiums up to 40% versus general IT suppliers. Limited subcontractor pools lengthen delivery lead times and raise SLA breach risk, with 60%+ of firms citing resource constraints in 2024 surveys. Concentration in a few boutiques raises switching costs; building internal bench reduces supplier leverage but increases fixed payroll and training expense.

Hardware and semiconductor exposure

Global supply volatility continues to delay infrastructure rollouts and inflate hardware costs, with lead times for networking, servers and endpoints running about 12–16 weeks in 2024, shifting bargaining power toward upstream suppliers. Currency swings in South Africa amplify import pricing pressure, and buffer inventory plus multi-vendor designs mitigate but do not fully neutralize supplier leverage.

Carrier and data center dependencies

Carrier and colocation providers (notably large operators in 2024) drive service quality and bundled pricing for Altron, with limited regional alternatives amplifying supplier leverage; cross-connect and egress fees remain recurring cost drivers and can be sticky. Long-term carrier contracts mitigate short-term price shocks but lock Altron into fixed terms and capacity commitments.

- Regional scarcity increases supplier leverage

- Cross-connect/egress fees = recurring cost pressure

- Long-term contracts = price stability but reduced flexibility

Standards and interoperability

Open standards lower supplier power by easing vendor switching and reducing integration costs; in 2024 firms with API-first strategies cut average integration time by roughly 30%, tightening competitive sourcing. Proprietary ecosystems and vendor certifications can re-tighten lock-in, raising renewal margins and switching costs. Mature APIs reduce Altron's integration expense, while enterprise-wide agreements across portfolios can rebalance supplier bargaining.

- Open standards: lower switching costs

- Proprietary ecosystems: increase lock-in

- API maturity: cuts integration time ~30% (2024)

- Enterprise agreements: rebalance supplier leverage

Hyperscaler dominance, cyber skills gap and long hardware lead times squeeze margins

Altron faces strong supplier power from OEMs and hyperscalers (Microsoft ~23%, AWS ~32% global cloud share in 2024), raising price and roadmap exposure. Cyber skills gap (~3.5M global in 2024) and 12–16 week hardware lead times boost niche supplier premiums and delivery risk. Carrier egress fees and long contracts create recurring cost stickiness.

| Metric | 2024 |

|---|---|

| Hyperscaler share | MS 23% / AWS 32% |

| Cyber workforce gap | ~3.5M |

| Hardware lead times | 12–16 weeks |

What is included in the product

Concise Porter's Five Forces assessment of Altron that uncovers competitive drivers, supplier and buyer power, barriers to entry, substitution risks, and strategic implications for market positioning.

A concise one-sheet Porter's Five Forces for Altron that maps supplier, buyer, rivalry, substitutes and entrant pressures—delivering slide-ready clarity for fast strategic decisions and stakeholder briefings.

Customers Bargaining Power

Enterprise and public-sector procurement

Enterprise and public-sector procurement runs competitive RFPs that push Altron to offer volume discounts and tiered pricing, with framework agreements and rate cards intensifying price pressure. In 2024, public-sector demand remained a primary IT-services driver, and compliance and localization clauses are routinely leveraged to extract concessions. Multi-year deals are used to trade margin for revenue stability and predictable cash flow.

Switching costs versus integration lock-in

Deeply integrated managed services raise exit costs and can blunt buyer power—with the global managed services market exceeding $250 billion in 2024 many contracts embed proprietary integrations that increase switching friction. Yet standard cloud stacks and multi-cloud strategies (92% of enterprises in Flexera 2024) make components more swappable, encouraging unbundling to best-of-breed. Clear SLAs, runbooks and data portability clauses lower perceived switching risk and shift leverage back to buyers.

Outcome-based and SLA penalties

By 2024 clients increasingly demand outcome-based fees and SLA credits, often tying 5–10% of contract value to performance, shifting risk to Altron and compressing margins when delivery slips. High-visibility KPIs give buyers leverage in renegotiations, enabling clawbacks or rate resets. Strong governance, contract clauses and automation of delivery and monitoring can protect Altron’s economics and limit downside.

Insourcing and captive centers

Larger organisations increasingly insource digital capability as an alternative to vendors; Gartner 2024 reports worldwide IT spending near 4.7 trillion USD, underpinning internal build investments. Talent availability and local cost differentials dictate feasibility and bargaining stance. Hybrid models retain external leverage while capping spend growth; Altron must demonstrate superior time-to-value to defend pricing.

- Insourcing trend: internal teams vs vendors

- Resource cost and availability drive leverage

- Hybrid model: preserves vendor leverage, limits spend

- Altron must prove faster time-to-value

Demand for end-to-end solutions

Buyers increasingly favor consolidated partners that bundle infrastructure, software and services, which can lift deal sizes while concentrating negotiating leverage with large enterprise clients. Successful cross-selling depends on clear, demonstrable integration benefits and measurable ROI to overcome switching risk. Strong referenceability and vertical expertise often tip procurement decisions in favor of integrated providers.

- Consolidation boosts deal size

- Concentrates buyer power

- Cross-sell needs measurable integration ROI

- Referenceability and vertical expertise decisive

Price squeeze: $250B+ managed services lock-in, 92% multi-cloud, 5–10% SLA fees

Public RFPs and framework discounts tightened price pressure in 2024. Managed services scale (>250B market 2024) raises switching costs but 92% multi-cloud adoption enables unbundling. Buyers tie 5–10% of fees to SLAs, shifting risk and compressing margins.

| Metric | 2024 |

|---|---|

| Managed services market | $250B+ |

| Multi-cloud adoption (Flexera) | 92% |

| SLA-linked fees | 5–10% |

Same Document Delivered

Altron Porter's Five Forces Analysis

This preview shows the exact Altron Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The file is fully formatted and ready for use, containing supplier and buyer power, competitive rivalry, threat of entry, and substitutes insights. You'll get instant access to this exact document upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Altron faces moderate buyer power, supplier concentration in tech inputs, and rising competitive intensity from local and global IT services firms; substitutes and regulatory shifts also shape margins. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore Altron’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on global OEMs

Altron depends on major OEMs like Microsoft, Cisco and hyperscalers for core licenses and hardware, leaving it exposed to supplier pricing power and roadmap control. Microsoft and AWS held roughly 23% and 32% global cloud market share in 2024, underscoring hyperscaler influence. Partner tiering and certification rules constrain discounting, and losing a top OEM badge would materially raise procurement costs and weaken competitive bids.

Specialist talent and subcontractors

Scarce skills in cybersecurity, cloud and data engineering drove a 2024 estimated global cyber workforce gap of ~3.5 million, pushing niche partner rates and reported premiums up to 40% versus general IT suppliers. Limited subcontractor pools lengthen delivery lead times and raise SLA breach risk, with 60%+ of firms citing resource constraints in 2024 surveys. Concentration in a few boutiques raises switching costs; building internal bench reduces supplier leverage but increases fixed payroll and training expense.

Hardware and semiconductor exposure

Global supply volatility continues to delay infrastructure rollouts and inflate hardware costs, with lead times for networking, servers and endpoints running about 12–16 weeks in 2024, shifting bargaining power toward upstream suppliers. Currency swings in South Africa amplify import pricing pressure, and buffer inventory plus multi-vendor designs mitigate but do not fully neutralize supplier leverage.

Carrier and data center dependencies

Carrier and colocation providers (notably large operators in 2024) drive service quality and bundled pricing for Altron, with limited regional alternatives amplifying supplier leverage; cross-connect and egress fees remain recurring cost drivers and can be sticky. Long-term carrier contracts mitigate short-term price shocks but lock Altron into fixed terms and capacity commitments.

- Regional scarcity increases supplier leverage

- Cross-connect/egress fees = recurring cost pressure

- Long-term contracts = price stability but reduced flexibility

Standards and interoperability

Open standards lower supplier power by easing vendor switching and reducing integration costs; in 2024 firms with API-first strategies cut average integration time by roughly 30%, tightening competitive sourcing. Proprietary ecosystems and vendor certifications can re-tighten lock-in, raising renewal margins and switching costs. Mature APIs reduce Altron's integration expense, while enterprise-wide agreements across portfolios can rebalance supplier bargaining.

- Open standards: lower switching costs

- Proprietary ecosystems: increase lock-in

- API maturity: cuts integration time ~30% (2024)

- Enterprise agreements: rebalance supplier leverage

Hyperscaler dominance, cyber skills gap and long hardware lead times squeeze margins

Altron faces strong supplier power from OEMs and hyperscalers (Microsoft ~23%, AWS ~32% global cloud share in 2024), raising price and roadmap exposure. Cyber skills gap (~3.5M global in 2024) and 12–16 week hardware lead times boost niche supplier premiums and delivery risk. Carrier egress fees and long contracts create recurring cost stickiness.

| Metric | 2024 |

|---|---|

| Hyperscaler share | MS 23% / AWS 32% |

| Cyber workforce gap | ~3.5M |

| Hardware lead times | 12–16 weeks |

What is included in the product

Concise Porter's Five Forces assessment of Altron that uncovers competitive drivers, supplier and buyer power, barriers to entry, substitution risks, and strategic implications for market positioning.

A concise one-sheet Porter's Five Forces for Altron that maps supplier, buyer, rivalry, substitutes and entrant pressures—delivering slide-ready clarity for fast strategic decisions and stakeholder briefings.

Customers Bargaining Power

Enterprise and public-sector procurement

Enterprise and public-sector procurement runs competitive RFPs that push Altron to offer volume discounts and tiered pricing, with framework agreements and rate cards intensifying price pressure. In 2024, public-sector demand remained a primary IT-services driver, and compliance and localization clauses are routinely leveraged to extract concessions. Multi-year deals are used to trade margin for revenue stability and predictable cash flow.

Switching costs versus integration lock-in

Deeply integrated managed services raise exit costs and can blunt buyer power—with the global managed services market exceeding $250 billion in 2024 many contracts embed proprietary integrations that increase switching friction. Yet standard cloud stacks and multi-cloud strategies (92% of enterprises in Flexera 2024) make components more swappable, encouraging unbundling to best-of-breed. Clear SLAs, runbooks and data portability clauses lower perceived switching risk and shift leverage back to buyers.

Outcome-based and SLA penalties

By 2024 clients increasingly demand outcome-based fees and SLA credits, often tying 5–10% of contract value to performance, shifting risk to Altron and compressing margins when delivery slips. High-visibility KPIs give buyers leverage in renegotiations, enabling clawbacks or rate resets. Strong governance, contract clauses and automation of delivery and monitoring can protect Altron’s economics and limit downside.

Insourcing and captive centers

Larger organisations increasingly insource digital capability as an alternative to vendors; Gartner 2024 reports worldwide IT spending near 4.7 trillion USD, underpinning internal build investments. Talent availability and local cost differentials dictate feasibility and bargaining stance. Hybrid models retain external leverage while capping spend growth; Altron must demonstrate superior time-to-value to defend pricing.

- Insourcing trend: internal teams vs vendors

- Resource cost and availability drive leverage

- Hybrid model: preserves vendor leverage, limits spend

- Altron must prove faster time-to-value

Demand for end-to-end solutions

Buyers increasingly favor consolidated partners that bundle infrastructure, software and services, which can lift deal sizes while concentrating negotiating leverage with large enterprise clients. Successful cross-selling depends on clear, demonstrable integration benefits and measurable ROI to overcome switching risk. Strong referenceability and vertical expertise often tip procurement decisions in favor of integrated providers.

- Consolidation boosts deal size

- Concentrates buyer power

- Cross-sell needs measurable integration ROI

- Referenceability and vertical expertise decisive

Price squeeze: $250B+ managed services lock-in, 92% multi-cloud, 5–10% SLA fees

Public RFPs and framework discounts tightened price pressure in 2024. Managed services scale (>250B market 2024) raises switching costs but 92% multi-cloud adoption enables unbundling. Buyers tie 5–10% of fees to SLAs, shifting risk and compressing margins.

| Metric | 2024 |

|---|---|

| Managed services market | $250B+ |

| Multi-cloud adoption (Flexera) | 92% |

| SLA-linked fees | 5–10% |

Same Document Delivered

Altron Porter's Five Forces Analysis

This preview shows the exact Altron Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The file is fully formatted and ready for use, containing supplier and buyer power, competitive rivalry, threat of entry, and substitutes insights. You'll get instant access to this exact document upon payment.