Altus Intervention AS Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

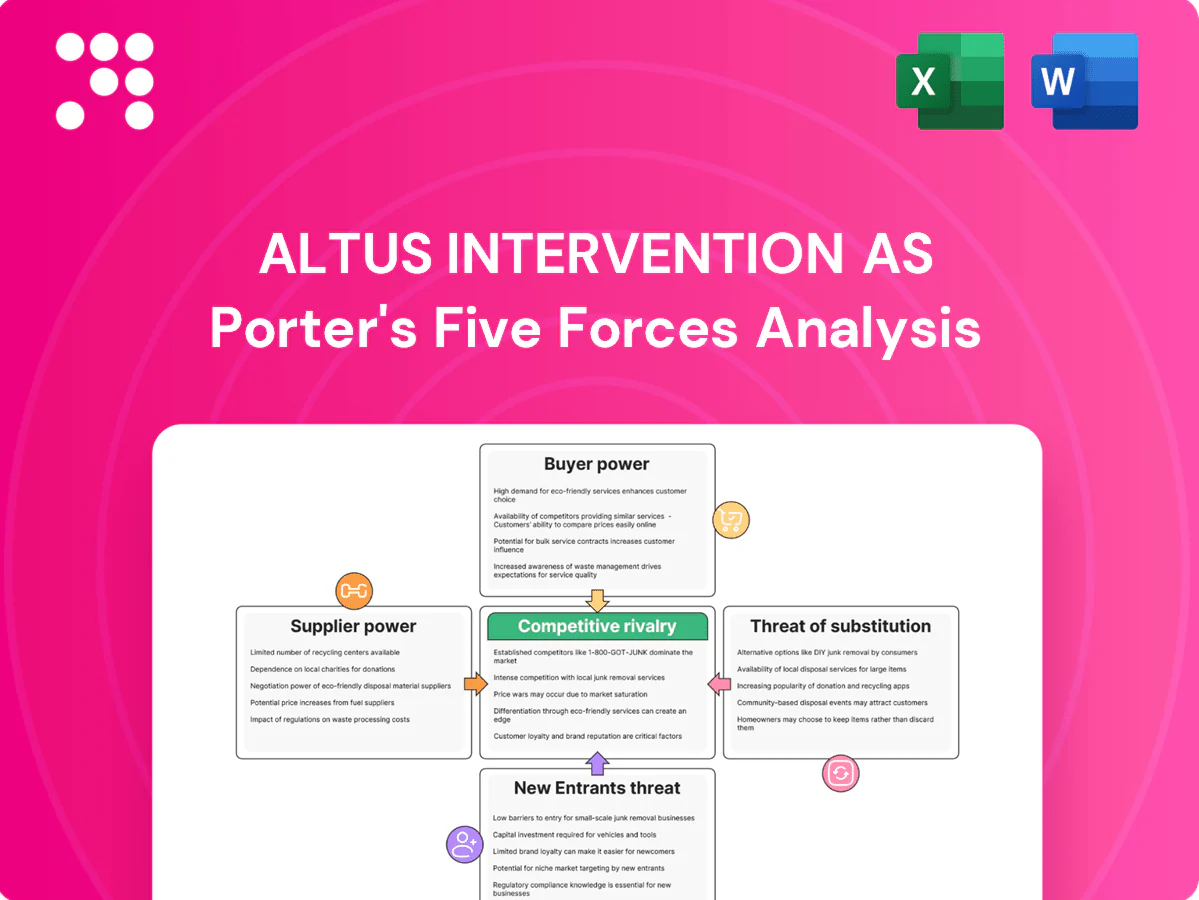

Altus Intervention AS operates in a niche subsea well intervention market where specialized skills, high capex and regulatory standards shape competitive dynamics. Buyers are savvy global oil majors, suppliers are concentrated, and substitutes are limited but technological shifts raise threat levels. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Altus Intervention AS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized tool and OEM concentration

Critical downhole tools, fiber-optics and telemetry kits remain concentrated among a few OEMs—in 2024 the top three suppliers account for over 60% of high-spec tool supply—giving suppliers pricing and scheduling leverage. Lead times commonly range 8–24 weeks and strict qualification standards entrench dependence; any disruption or redesign cycle can cascade across job schedules. Altus mitigates risk via dual-sourcing and selective in-house engineering.

Proprietary technology and IP lock-in

Suppliers holding patented components and proprietary software protocols (notably in 2024 industry reports) can impose licensing fees and integration constraints that raise Altus Intervention AS switching costs and operational lock-in. Compatibility requirements increase switching costs for service providers and can compress margins on turnkey packages. Co-development arrangements and long-term framework agreements help rebalance supplier power.

HSE, certification, and quality requirements

Materials must meet stringent API specs (eg API Spec 6A, 7-1) and ISO/industry HSE standards, which limits the pool of qualified suppliers; operators often face intervention downtime costs exceeding 100,000 USD per day, so failures are costly. Compliance narrows the vendor pool and raises supplier bargaining power, while Altus’s vendor audits and qualification programs build measurable negotiating leverage over time.

Commodity and logistics volatility

Commodity and logistics volatility—notably swings in steel and electronics costs and shipping rates—directly raise Altus Intervention AS tool costs and constrain availability; the Baltic Dry Index averaged ~1,200 in H1 2024, keeping freight premiums elevated for heavy kit. Remote basins and rigless campaigns demand precise, time-sensitive logistics, amplifying supplier leverage. Expedited freight and spares buffers materially increase cost-to-serve, while forward contracts and inventory planning have partially offset price swings.

- Steel/electronics cost exposure

- Freight premiums for remote basins

- Expedited spares raise OPEX

- Forward contracts reduce volatility

Digital and data dependencies

Telemetry, analytics and downhole software for Altus Intervention AS depend on niche vendors, with a 2024 industry survey indicating roughly 62% of service providers rely on third-party digital suppliers; API access, proprietary data formats and cybersecurity clauses can shift bargaining power toward vendors. Support SLAs and update cadences directly affect uptime during critical interventions, while building internal software capability and open-data standards reduces supplier leverage.

- Vendor concentration: high

- API/data format risk: material

- SLA impact on uptime: significant

- Internal dev capability: mitigant

Supplier concentration >60%, 8-24wk lead times raise switching costs

Supplier concentration (>60% top3 in 2024) and 8–24 week lead times give OEMs pricing/scheduling leverage; downtime >100,000 USD/day raises switching costs. Patented components, proprietary software and 62% reliance on third‑party digital vendors (2024) increase lock‑in, while BDI ~1,200 in H1 2024 elevated freight premiums. Altus reduces risk via dual‑sourcing, in‑house engineering and forward contracts.

| Metric | 2024 value |

|---|---|

| Top3 supplier share | >60% |

| Lead times | 8–24 weeks |

| Downtime cost/day | >100,000 USD |

| BDI H1 2024 | ~1,200 |

| Digital vendor reliance | 62% |

What is included in the product

Tailored Porter’s Five Forces analysis for Altus Intervention AS revealing competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A clear, one-sheet Porter's Five Forces summary for Altus Intervention AS—customize pressure levels with your data, view instant strategic pressure via a spider chart, and drop into pitch decks or Excel dashboards without macros or complex code.

Customers Bargaining Power

Concentrated IOCs/NOCs and EPCs

Concentrated IOCs/NOCs and EPCs dominate demand and use global framework agreements to extract volume discounts and standardized KPIs, audit rights and stringent contract terms. This exerts continuous pressure on day rates and tool-rental margins for Altus Intervention AS, compressing pricing power. Deeper operator relationships and proprietary or differentiated intervention technologies can shift focus from price to value, softening margin erosion.

Competitive tendering and frame agreements

Multi-year tenders (commonly 3–5 years) establish benchmark pricing and service levels that buyers use across renewal cycles. Competitive bidding increases buyer leverage and transparency during award and renewal windows, often triggering price resets. Altus defends margins through performance-based clauses and by leveraging unique rapid-response and specialized intervention capabilities.

High switching but calculable costs

Operational integration, standardized procedures and preserved data continuity create measurable switching costs that modestly blunt buyer power. Buyers, however, explicitly quantify transition expenses and commonly maintain dual-source strategies, keeping leverage. Trial jobs and pilot projects are routinely used to de-risk supplier changes. Demonstrable superior uptime and NPT reduction remain the strongest retention levers.

Demand cyclicality with oil price

Demand cyclicality tied to Brent price swings (Brent averaged $88/bbl in 2024) shifts Capex/Opex cadence: downturns drive delayed interventions and discount pressure, while upcycles ease price sensitivity but elevate service-quality and uptime demands; flexible commercial models (risk‑share, unit pricing) smooth buyer urgency and budgets.

- Downturn: delayed spend, higher discounting

- Upcycle: lower price pressure, higher SLA demands

- 2024 Brent ~$88/bbl; flexible contracts cut revenue volatility

Outcome-based procurement

Buyers increasingly demand performance-linked payments tied to production uplift, shifting downside risk to service providers while rewarding proven differentiation; by 2024 major operators expanded pilots of outcome-based contracts across upstream services. Data transparency and metering accuracy become key negotiation levers, and Altus’s production optimization tools support verifiable uplift and reporting.

- Performance-linked payments: pilots expanded in 2024

- Risk transfer: favors providers with proven differentiation

- Negotiation levers: metering accuracy, data transparency

- Altus edge: production optimization and verifiable reporting

Multi-year tenders and outcome pilots compress day rates; Brent volatility amplifies buyer leverage

Buyers (concentrated IOCs/NOCs and EPCs) use global frameworks and multi-year tenders to push down day rates, compressing Altus’s pricing power. Performance-linked payments and metering transparency (pilots expanded in 2024) shift risk to providers but reward differentiated tech. Brent averaged $88/bbl in 2024, creating cyclic demand swings that amplify buyer leverage in downturns.

| Metric | 2024 Value | Impact |

|---|---|---|

| Brent | $88/bbl | Demand cyclicality |

| Tender length | 3–5 yrs | Price benchmarking |

| Outcome pilots | Expanded 2024 | Risk transfer |

Preview Before You Purchase

Altus Intervention AS Porter's Five Forces Analysis

The Altus Intervention AS Porter’s Five Forces analysis evaluates competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes to quantify strategic pressure points and growth constraints. This preview shows the exact document you'll receive—fully formatted and ready for immediate download after purchase. No placeholders, no mockups.

Go Beyond the Preview—Access the Full Strategic Report

Altus Intervention AS operates in a niche subsea well intervention market where specialized skills, high capex and regulatory standards shape competitive dynamics. Buyers are savvy global oil majors, suppliers are concentrated, and substitutes are limited but technological shifts raise threat levels. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Altus Intervention AS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized tool and OEM concentration

Critical downhole tools, fiber-optics and telemetry kits remain concentrated among a few OEMs—in 2024 the top three suppliers account for over 60% of high-spec tool supply—giving suppliers pricing and scheduling leverage. Lead times commonly range 8–24 weeks and strict qualification standards entrench dependence; any disruption or redesign cycle can cascade across job schedules. Altus mitigates risk via dual-sourcing and selective in-house engineering.

Proprietary technology and IP lock-in

Suppliers holding patented components and proprietary software protocols (notably in 2024 industry reports) can impose licensing fees and integration constraints that raise Altus Intervention AS switching costs and operational lock-in. Compatibility requirements increase switching costs for service providers and can compress margins on turnkey packages. Co-development arrangements and long-term framework agreements help rebalance supplier power.

HSE, certification, and quality requirements

Materials must meet stringent API specs (eg API Spec 6A, 7-1) and ISO/industry HSE standards, which limits the pool of qualified suppliers; operators often face intervention downtime costs exceeding 100,000 USD per day, so failures are costly. Compliance narrows the vendor pool and raises supplier bargaining power, while Altus’s vendor audits and qualification programs build measurable negotiating leverage over time.

Commodity and logistics volatility

Commodity and logistics volatility—notably swings in steel and electronics costs and shipping rates—directly raise Altus Intervention AS tool costs and constrain availability; the Baltic Dry Index averaged ~1,200 in H1 2024, keeping freight premiums elevated for heavy kit. Remote basins and rigless campaigns demand precise, time-sensitive logistics, amplifying supplier leverage. Expedited freight and spares buffers materially increase cost-to-serve, while forward contracts and inventory planning have partially offset price swings.

- Steel/electronics cost exposure

- Freight premiums for remote basins

- Expedited spares raise OPEX

- Forward contracts reduce volatility

Digital and data dependencies

Telemetry, analytics and downhole software for Altus Intervention AS depend on niche vendors, with a 2024 industry survey indicating roughly 62% of service providers rely on third-party digital suppliers; API access, proprietary data formats and cybersecurity clauses can shift bargaining power toward vendors. Support SLAs and update cadences directly affect uptime during critical interventions, while building internal software capability and open-data standards reduces supplier leverage.

- Vendor concentration: high

- API/data format risk: material

- SLA impact on uptime: significant

- Internal dev capability: mitigant

Supplier concentration >60%, 8-24wk lead times raise switching costs

Supplier concentration (>60% top3 in 2024) and 8–24 week lead times give OEMs pricing/scheduling leverage; downtime >100,000 USD/day raises switching costs. Patented components, proprietary software and 62% reliance on third‑party digital vendors (2024) increase lock‑in, while BDI ~1,200 in H1 2024 elevated freight premiums. Altus reduces risk via dual‑sourcing, in‑house engineering and forward contracts.

| Metric | 2024 value |

|---|---|

| Top3 supplier share | >60% |

| Lead times | 8–24 weeks |

| Downtime cost/day | >100,000 USD |

| BDI H1 2024 | ~1,200 |

| Digital vendor reliance | 62% |

What is included in the product

Tailored Porter’s Five Forces analysis for Altus Intervention AS revealing competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A clear, one-sheet Porter's Five Forces summary for Altus Intervention AS—customize pressure levels with your data, view instant strategic pressure via a spider chart, and drop into pitch decks or Excel dashboards without macros or complex code.

Customers Bargaining Power

Concentrated IOCs/NOCs and EPCs

Concentrated IOCs/NOCs and EPCs dominate demand and use global framework agreements to extract volume discounts and standardized KPIs, audit rights and stringent contract terms. This exerts continuous pressure on day rates and tool-rental margins for Altus Intervention AS, compressing pricing power. Deeper operator relationships and proprietary or differentiated intervention technologies can shift focus from price to value, softening margin erosion.

Competitive tendering and frame agreements

Multi-year tenders (commonly 3–5 years) establish benchmark pricing and service levels that buyers use across renewal cycles. Competitive bidding increases buyer leverage and transparency during award and renewal windows, often triggering price resets. Altus defends margins through performance-based clauses and by leveraging unique rapid-response and specialized intervention capabilities.

High switching but calculable costs

Operational integration, standardized procedures and preserved data continuity create measurable switching costs that modestly blunt buyer power. Buyers, however, explicitly quantify transition expenses and commonly maintain dual-source strategies, keeping leverage. Trial jobs and pilot projects are routinely used to de-risk supplier changes. Demonstrable superior uptime and NPT reduction remain the strongest retention levers.

Demand cyclicality with oil price

Demand cyclicality tied to Brent price swings (Brent averaged $88/bbl in 2024) shifts Capex/Opex cadence: downturns drive delayed interventions and discount pressure, while upcycles ease price sensitivity but elevate service-quality and uptime demands; flexible commercial models (risk‑share, unit pricing) smooth buyer urgency and budgets.

- Downturn: delayed spend, higher discounting

- Upcycle: lower price pressure, higher SLA demands

- 2024 Brent ~$88/bbl; flexible contracts cut revenue volatility

Outcome-based procurement

Buyers increasingly demand performance-linked payments tied to production uplift, shifting downside risk to service providers while rewarding proven differentiation; by 2024 major operators expanded pilots of outcome-based contracts across upstream services. Data transparency and metering accuracy become key negotiation levers, and Altus’s production optimization tools support verifiable uplift and reporting.

- Performance-linked payments: pilots expanded in 2024

- Risk transfer: favors providers with proven differentiation

- Negotiation levers: metering accuracy, data transparency

- Altus edge: production optimization and verifiable reporting

Multi-year tenders and outcome pilots compress day rates; Brent volatility amplifies buyer leverage

Buyers (concentrated IOCs/NOCs and EPCs) use global frameworks and multi-year tenders to push down day rates, compressing Altus’s pricing power. Performance-linked payments and metering transparency (pilots expanded in 2024) shift risk to providers but reward differentiated tech. Brent averaged $88/bbl in 2024, creating cyclic demand swings that amplify buyer leverage in downturns.

| Metric | 2024 Value | Impact |

|---|---|---|

| Brent | $88/bbl | Demand cyclicality |

| Tender length | 3–5 yrs | Price benchmarking |

| Outcome pilots | Expanded 2024 | Risk transfer |

Preview Before You Purchase

Altus Intervention AS Porter's Five Forces Analysis

The Altus Intervention AS Porter’s Five Forces analysis evaluates competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes to quantify strategic pressure points and growth constraints. This preview shows the exact document you'll receive—fully formatted and ready for immediate download after purchase. No placeholders, no mockups.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Altus Intervention AS operates in a niche subsea well intervention market where specialized skills, high capex and regulatory standards shape competitive dynamics. Buyers are savvy global oil majors, suppliers are concentrated, and substitutes are limited but technological shifts raise threat levels. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Altus Intervention AS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized tool and OEM concentration

Critical downhole tools, fiber-optics and telemetry kits remain concentrated among a few OEMs—in 2024 the top three suppliers account for over 60% of high-spec tool supply—giving suppliers pricing and scheduling leverage. Lead times commonly range 8–24 weeks and strict qualification standards entrench dependence; any disruption or redesign cycle can cascade across job schedules. Altus mitigates risk via dual-sourcing and selective in-house engineering.

Proprietary technology and IP lock-in

Suppliers holding patented components and proprietary software protocols (notably in 2024 industry reports) can impose licensing fees and integration constraints that raise Altus Intervention AS switching costs and operational lock-in. Compatibility requirements increase switching costs for service providers and can compress margins on turnkey packages. Co-development arrangements and long-term framework agreements help rebalance supplier power.

HSE, certification, and quality requirements

Materials must meet stringent API specs (eg API Spec 6A, 7-1) and ISO/industry HSE standards, which limits the pool of qualified suppliers; operators often face intervention downtime costs exceeding 100,000 USD per day, so failures are costly. Compliance narrows the vendor pool and raises supplier bargaining power, while Altus’s vendor audits and qualification programs build measurable negotiating leverage over time.

Commodity and logistics volatility

Commodity and logistics volatility—notably swings in steel and electronics costs and shipping rates—directly raise Altus Intervention AS tool costs and constrain availability; the Baltic Dry Index averaged ~1,200 in H1 2024, keeping freight premiums elevated for heavy kit. Remote basins and rigless campaigns demand precise, time-sensitive logistics, amplifying supplier leverage. Expedited freight and spares buffers materially increase cost-to-serve, while forward contracts and inventory planning have partially offset price swings.

- Steel/electronics cost exposure

- Freight premiums for remote basins

- Expedited spares raise OPEX

- Forward contracts reduce volatility

Digital and data dependencies

Telemetry, analytics and downhole software for Altus Intervention AS depend on niche vendors, with a 2024 industry survey indicating roughly 62% of service providers rely on third-party digital suppliers; API access, proprietary data formats and cybersecurity clauses can shift bargaining power toward vendors. Support SLAs and update cadences directly affect uptime during critical interventions, while building internal software capability and open-data standards reduces supplier leverage.

- Vendor concentration: high

- API/data format risk: material

- SLA impact on uptime: significant

- Internal dev capability: mitigant

Supplier concentration >60%, 8-24wk lead times raise switching costs

Supplier concentration (>60% top3 in 2024) and 8–24 week lead times give OEMs pricing/scheduling leverage; downtime >100,000 USD/day raises switching costs. Patented components, proprietary software and 62% reliance on third‑party digital vendors (2024) increase lock‑in, while BDI ~1,200 in H1 2024 elevated freight premiums. Altus reduces risk via dual‑sourcing, in‑house engineering and forward contracts.

| Metric | 2024 value |

|---|---|

| Top3 supplier share | >60% |

| Lead times | 8–24 weeks |

| Downtime cost/day | >100,000 USD |

| BDI H1 2024 | ~1,200 |

| Digital vendor reliance | 62% |

What is included in the product

Tailored Porter’s Five Forces analysis for Altus Intervention AS revealing competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A clear, one-sheet Porter's Five Forces summary for Altus Intervention AS—customize pressure levels with your data, view instant strategic pressure via a spider chart, and drop into pitch decks or Excel dashboards without macros or complex code.

Customers Bargaining Power

Concentrated IOCs/NOCs and EPCs

Concentrated IOCs/NOCs and EPCs dominate demand and use global framework agreements to extract volume discounts and standardized KPIs, audit rights and stringent contract terms. This exerts continuous pressure on day rates and tool-rental margins for Altus Intervention AS, compressing pricing power. Deeper operator relationships and proprietary or differentiated intervention technologies can shift focus from price to value, softening margin erosion.

Competitive tendering and frame agreements

Multi-year tenders (commonly 3–5 years) establish benchmark pricing and service levels that buyers use across renewal cycles. Competitive bidding increases buyer leverage and transparency during award and renewal windows, often triggering price resets. Altus defends margins through performance-based clauses and by leveraging unique rapid-response and specialized intervention capabilities.

High switching but calculable costs

Operational integration, standardized procedures and preserved data continuity create measurable switching costs that modestly blunt buyer power. Buyers, however, explicitly quantify transition expenses and commonly maintain dual-source strategies, keeping leverage. Trial jobs and pilot projects are routinely used to de-risk supplier changes. Demonstrable superior uptime and NPT reduction remain the strongest retention levers.

Demand cyclicality with oil price

Demand cyclicality tied to Brent price swings (Brent averaged $88/bbl in 2024) shifts Capex/Opex cadence: downturns drive delayed interventions and discount pressure, while upcycles ease price sensitivity but elevate service-quality and uptime demands; flexible commercial models (risk‑share, unit pricing) smooth buyer urgency and budgets.

- Downturn: delayed spend, higher discounting

- Upcycle: lower price pressure, higher SLA demands

- 2024 Brent ~$88/bbl; flexible contracts cut revenue volatility

Outcome-based procurement

Buyers increasingly demand performance-linked payments tied to production uplift, shifting downside risk to service providers while rewarding proven differentiation; by 2024 major operators expanded pilots of outcome-based contracts across upstream services. Data transparency and metering accuracy become key negotiation levers, and Altus’s production optimization tools support verifiable uplift and reporting.

- Performance-linked payments: pilots expanded in 2024

- Risk transfer: favors providers with proven differentiation

- Negotiation levers: metering accuracy, data transparency

- Altus edge: production optimization and verifiable reporting

Multi-year tenders and outcome pilots compress day rates; Brent volatility amplifies buyer leverage

Buyers (concentrated IOCs/NOCs and EPCs) use global frameworks and multi-year tenders to push down day rates, compressing Altus’s pricing power. Performance-linked payments and metering transparency (pilots expanded in 2024) shift risk to providers but reward differentiated tech. Brent averaged $88/bbl in 2024, creating cyclic demand swings that amplify buyer leverage in downturns.

| Metric | 2024 Value | Impact |

|---|---|---|

| Brent | $88/bbl | Demand cyclicality |

| Tender length | 3–5 yrs | Price benchmarking |

| Outcome pilots | Expanded 2024 | Risk transfer |

Preview Before You Purchase

Altus Intervention AS Porter's Five Forces Analysis

The Altus Intervention AS Porter’s Five Forces analysis evaluates competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes to quantify strategic pressure points and growth constraints. This preview shows the exact document you'll receive—fully formatted and ready for immediate download after purchase. No placeholders, no mockups.