A-Mark Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

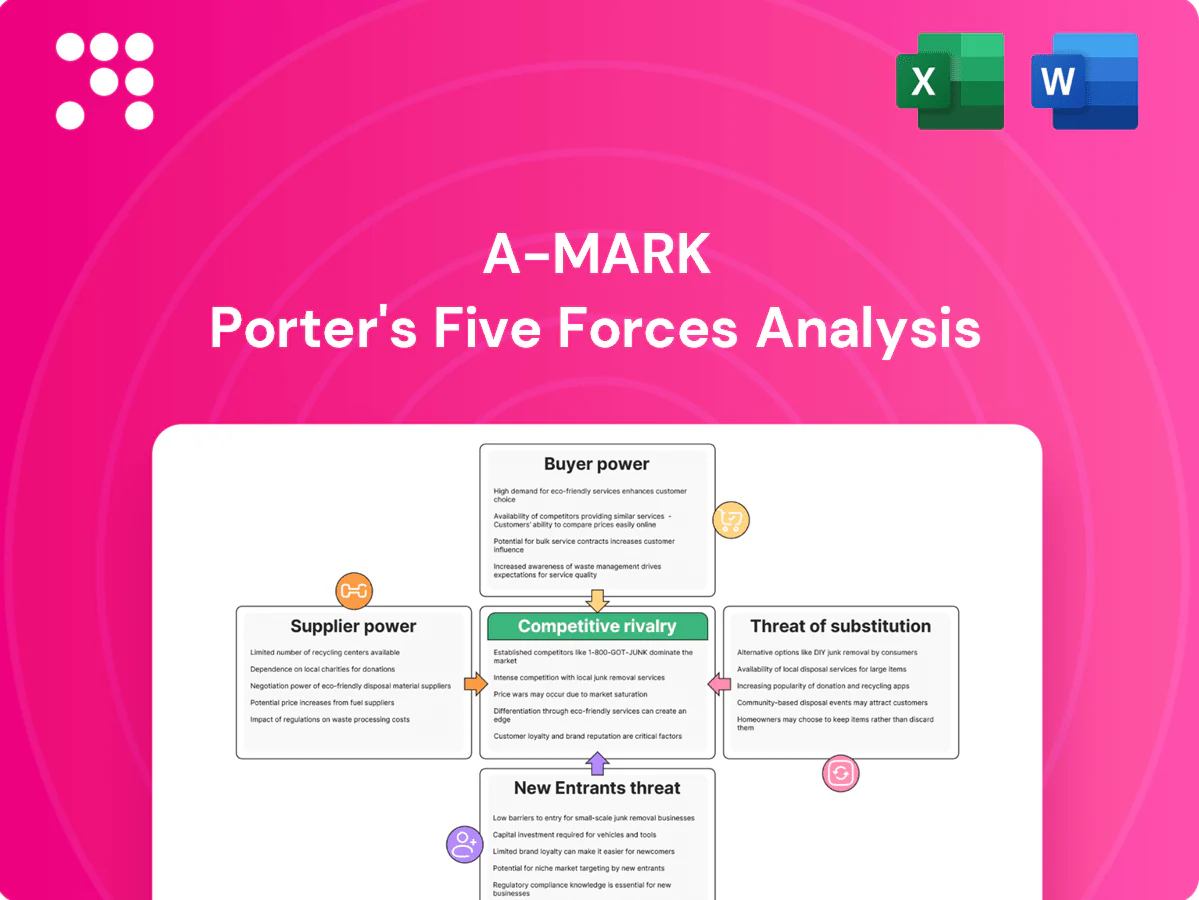

A-Mark’s Porter's Five Forces snapshot highlights moderate supplier power, high buyer price sensitivity, low substitute threat, and intense rivalry among bullion dealers. Regulatory and entry barriers shape profitability and margins. This brief preview outlines key pressures and strategic implications. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated mints & refiners

A-Mark depends on a limited set of sovereign mints (notably the U.S. Mint and Royal Canadian Mint) and LBMA-accredited refiners that control iconic coins and purity standards, concentrating supply power. This concentration raises supplier leverage over allocations, premiums and commercial terms, even as preferred-dealer status and multi-sourcing mitigate but do not eliminate the dependence. Disruptions at these suppliers can rapidly tighten A-Mark inventory and widen retail–wholesale spreads.

Allocation and premium control

Sovereign mints such as the U.S. Mint and Royal Canadian Mint control production schedules, product mixes and allocation formulas that can ration supply in high-demand periods. Suppliers raised fabrication premiums in 2024, compressing distributor margins and pressuring spreads. A-Mark offsets volatility with forward commitments and strategic inventory positioning, yet upstream pricing power and brand-specific coin scarcity maintain supplier leverage. Limited substitution for flagship coins sustains that influence.

Commodity pass-through dynamics

Spot metal costs are largely pass-through to customers, while fabrication premiums and logistics are retained by suppliers and not fully passed through; when market volatility spikes suppliers can reprice terms and premiums faster than distributors can reset multi-channel pricing, temporarily increasing supplier power. Hedging reduces exposure but cannot eliminate basis mismatches and premium/logistics risk.

Logistics and custody dependencies

Approved vaults, assay labs, and insured transport providers remain specialized and limited, concentrating leverage among a few gateway nodes; dependence on these third parties gives suppliers pricing and priority power that can spike rapidly if capacity tightens. A-Mark’s integrated logistics reduce exposure but still interfaces with external custodians and carriers, creating chokepoints where a single bottleneck can abruptly elevate supplier bargaining power. Recent industry reporting in 2024 highlighted ongoing consolidation among custodial vaults, reinforcing this concentrated supply-side risk.

- Few specialized providers: concentrated custody and assay capacity

- Supplier leverage: price and priority control at chokepoints

- A-Mark mitigation: integrated logistics, but third-party interfaces remain

- 2024 trend: continued custodial consolidation increasing systemic vulnerability

Compliance and ESG constraints

Compliance and ESG constraints (responsible sourcing, KYC/AML, sanctions screening) materially narrow eligible supplier pools; FATF's 40 recommendations (2024) underpin tougher due diligence that favors accredited suppliers who command price and contractual advantages. A-Mark’s scale and compliance infrastructure improve access but do not eliminate scarcity premiums, and further regulatory tightening would likely boost supplier power.

- Responsible sourcing narrows suppliers

- KYC/AML increases onboarding friction

- Sanctions screening elevates counterparty risk

- Accredited suppliers gain pricing leverage

Mint/refiner concentration tightens allocations, raising fabrication premiums and widening spreads

A-Mark faces concentrated supplier power from sovereign mints and LBMA refiners, giving suppliers leverage over allocations, premiums and terms. 2024 saw rising fabrication premiums and custodial consolidation, tightening allocations and widening retail–wholesale spreads despite A-Mark’s hedging and integrated logistics. Compliance rules further narrow suppliers, sustaining scarcity premiums.

| Metric | 2024 Signal |

|---|---|

| Fabrication premiums | Increased (industry reports 2024) |

| Custodial concentration | Higher consolidation (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to A‑Mark, with detailed evaluation of supplier and buyer power, substitutes, rivalry, and entry barriers; identifies disruptive threats and strategic levers to protect margins and market share, delivered in fully editable Word format for decks, plans, or reports.

A concise, one-sheet Porter's Five Forces for A‑Mark that instantly relieves decision paralysis by visualizing competitive pressures and priority actions; ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

High price transparency

High price transparency — with spot quotes and premiums posted in real time on platforms like Kitco and dealers in 2024 — lets buyers compare and arbitrage spreads often below 1%, compressing margins. Buyers routinely exploit sub-1% spread differences, increasing pressure on dealer premiums and execution fees. A-Mark offsets this by offering deep inventory and reliable trade execution, but transparency structurally raises buyer leverage.

Low switching costs

Wholesale and retail customers can pivot among dealers and e-commerce sites with minimal friction, as shipping, live pricing and payment rails are industry-standard; A-Mark (NASDAQ: AMRK) offsets this by offering financing, vaulted storage and liquidity services that increase client stickiness. Despite these services, baseline switching costs remain low, keeping buyer bargaining power elevated in 2024.

Volume buyer leverage

Institutions, large dealers, and OEMs extract tighter spreads and priority allocations from A-Mark, leveraging steady order flow — A-Mark reported $5.74 billion revenue in 2024, underscoring scale that attracts large buyers. The firm routinely trades concessions for wallet share and multi-year contracts to lock in volume. Concentration of top accounts materially amplifies buyer bargaining power, pressuring margins on headline volumes.

Demand cyclicality

During risk-off surges buyers exhibit urgency that reduces price sensitivity and eases buyer power; 2024 saw the VIX average near 16, reflecting intermittent risk-off episodes that tightened supply willingness. In calmer 2024 quarters, buyers pushed for lower premiums and extended terms, and A-Mark’s diversified channels (wholesale, retail, B2B) smooth but cannot fully offset these shifts. Seasonality and macro sentiment swing leverage back to buyers in normal times.

- Risk-off: lower buyer price sensitivity

- Calm markets: demand for lower premiums, longer terms

- A-Mark diversification dampens but not eliminates cycles

- 2024 VIX ~16 indicates recurring risk-off spikes

Substitute access

Customers can pivot to ETFs, futures, or tokenized metals for exposure without handling physical, and ready alternatives compress A-Mark’s leverage over premiums and storage fees; SPDR Gold Shares (GLD) held about 60 billion USD AUM in 2024 while COMEX gold futures open interest regularly exceeded 600k contracts, keeping financial substitutes compelling despite A-Mark’s physical deliverability, product variety, and custody services.

- Substitute access: ETFs, futures, tokenized metals

- 2024 tags: GLD ~60B AUM; COMEX OI >600k

- A-Mark strengths: physical delivery, SKU breadth, custody

- Impact: tighter premiums, selective customer migration

Price transparency and low switching costs empower buyers, squeezing precious-metal premiums

High price transparency and low switching costs in 2024 give customers strong leverage, compressing premiums despite A-Mark’s scale. Large buyers extract tighter spreads; A-Mark reported $5.74B revenue in 2024 and concedes volume discounts. Financial substitutes (GLD ~60B AUM; COMEX OI >600k) and intermittent risk-off (VIX ~16) keep buyer power elevated.

| Metric | 2024 |

|---|---|

| A-Mark revenue | $5.74B |

| GLD AUM | $60B |

| COMEX OI | >600k contracts |

| VIX average | ~16 |

Preview Before You Purchase

A-Mark Porter's Five Forces Analysis

This preview shows A‑Mark's Porter’s Five Forces Analysis and is the exact document you’ll receive immediately after purchase—no placeholders or samples. The report is professionally formatted, complete, and ready for download and use the moment payment is processed. No surprises; the file available to you post‑purchase is precisely this one.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

A-Mark’s Porter's Five Forces snapshot highlights moderate supplier power, high buyer price sensitivity, low substitute threat, and intense rivalry among bullion dealers. Regulatory and entry barriers shape profitability and margins. This brief preview outlines key pressures and strategic implications. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated mints & refiners

A-Mark depends on a limited set of sovereign mints (notably the U.S. Mint and Royal Canadian Mint) and LBMA-accredited refiners that control iconic coins and purity standards, concentrating supply power. This concentration raises supplier leverage over allocations, premiums and commercial terms, even as preferred-dealer status and multi-sourcing mitigate but do not eliminate the dependence. Disruptions at these suppliers can rapidly tighten A-Mark inventory and widen retail–wholesale spreads.

Allocation and premium control

Sovereign mints such as the U.S. Mint and Royal Canadian Mint control production schedules, product mixes and allocation formulas that can ration supply in high-demand periods. Suppliers raised fabrication premiums in 2024, compressing distributor margins and pressuring spreads. A-Mark offsets volatility with forward commitments and strategic inventory positioning, yet upstream pricing power and brand-specific coin scarcity maintain supplier leverage. Limited substitution for flagship coins sustains that influence.

Commodity pass-through dynamics

Spot metal costs are largely pass-through to customers, while fabrication premiums and logistics are retained by suppliers and not fully passed through; when market volatility spikes suppliers can reprice terms and premiums faster than distributors can reset multi-channel pricing, temporarily increasing supplier power. Hedging reduces exposure but cannot eliminate basis mismatches and premium/logistics risk.

Logistics and custody dependencies

Approved vaults, assay labs, and insured transport providers remain specialized and limited, concentrating leverage among a few gateway nodes; dependence on these third parties gives suppliers pricing and priority power that can spike rapidly if capacity tightens. A-Mark’s integrated logistics reduce exposure but still interfaces with external custodians and carriers, creating chokepoints where a single bottleneck can abruptly elevate supplier bargaining power. Recent industry reporting in 2024 highlighted ongoing consolidation among custodial vaults, reinforcing this concentrated supply-side risk.

- Few specialized providers: concentrated custody and assay capacity

- Supplier leverage: price and priority control at chokepoints

- A-Mark mitigation: integrated logistics, but third-party interfaces remain

- 2024 trend: continued custodial consolidation increasing systemic vulnerability

Compliance and ESG constraints

Compliance and ESG constraints (responsible sourcing, KYC/AML, sanctions screening) materially narrow eligible supplier pools; FATF's 40 recommendations (2024) underpin tougher due diligence that favors accredited suppliers who command price and contractual advantages. A-Mark’s scale and compliance infrastructure improve access but do not eliminate scarcity premiums, and further regulatory tightening would likely boost supplier power.

- Responsible sourcing narrows suppliers

- KYC/AML increases onboarding friction

- Sanctions screening elevates counterparty risk

- Accredited suppliers gain pricing leverage

Mint/refiner concentration tightens allocations, raising fabrication premiums and widening spreads

A-Mark faces concentrated supplier power from sovereign mints and LBMA refiners, giving suppliers leverage over allocations, premiums and terms. 2024 saw rising fabrication premiums and custodial consolidation, tightening allocations and widening retail–wholesale spreads despite A-Mark’s hedging and integrated logistics. Compliance rules further narrow suppliers, sustaining scarcity premiums.

| Metric | 2024 Signal |

|---|---|

| Fabrication premiums | Increased (industry reports 2024) |

| Custodial concentration | Higher consolidation (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to A‑Mark, with detailed evaluation of supplier and buyer power, substitutes, rivalry, and entry barriers; identifies disruptive threats and strategic levers to protect margins and market share, delivered in fully editable Word format for decks, plans, or reports.

A concise, one-sheet Porter's Five Forces for A‑Mark that instantly relieves decision paralysis by visualizing competitive pressures and priority actions; ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

High price transparency

High price transparency — with spot quotes and premiums posted in real time on platforms like Kitco and dealers in 2024 — lets buyers compare and arbitrage spreads often below 1%, compressing margins. Buyers routinely exploit sub-1% spread differences, increasing pressure on dealer premiums and execution fees. A-Mark offsets this by offering deep inventory and reliable trade execution, but transparency structurally raises buyer leverage.

Low switching costs

Wholesale and retail customers can pivot among dealers and e-commerce sites with minimal friction, as shipping, live pricing and payment rails are industry-standard; A-Mark (NASDAQ: AMRK) offsets this by offering financing, vaulted storage and liquidity services that increase client stickiness. Despite these services, baseline switching costs remain low, keeping buyer bargaining power elevated in 2024.

Volume buyer leverage

Institutions, large dealers, and OEMs extract tighter spreads and priority allocations from A-Mark, leveraging steady order flow — A-Mark reported $5.74 billion revenue in 2024, underscoring scale that attracts large buyers. The firm routinely trades concessions for wallet share and multi-year contracts to lock in volume. Concentration of top accounts materially amplifies buyer bargaining power, pressuring margins on headline volumes.

Demand cyclicality

During risk-off surges buyers exhibit urgency that reduces price sensitivity and eases buyer power; 2024 saw the VIX average near 16, reflecting intermittent risk-off episodes that tightened supply willingness. In calmer 2024 quarters, buyers pushed for lower premiums and extended terms, and A-Mark’s diversified channels (wholesale, retail, B2B) smooth but cannot fully offset these shifts. Seasonality and macro sentiment swing leverage back to buyers in normal times.

- Risk-off: lower buyer price sensitivity

- Calm markets: demand for lower premiums, longer terms

- A-Mark diversification dampens but not eliminates cycles

- 2024 VIX ~16 indicates recurring risk-off spikes

Substitute access

Customers can pivot to ETFs, futures, or tokenized metals for exposure without handling physical, and ready alternatives compress A-Mark’s leverage over premiums and storage fees; SPDR Gold Shares (GLD) held about 60 billion USD AUM in 2024 while COMEX gold futures open interest regularly exceeded 600k contracts, keeping financial substitutes compelling despite A-Mark’s physical deliverability, product variety, and custody services.

- Substitute access: ETFs, futures, tokenized metals

- 2024 tags: GLD ~60B AUM; COMEX OI >600k

- A-Mark strengths: physical delivery, SKU breadth, custody

- Impact: tighter premiums, selective customer migration

Price transparency and low switching costs empower buyers, squeezing precious-metal premiums

High price transparency and low switching costs in 2024 give customers strong leverage, compressing premiums despite A-Mark’s scale. Large buyers extract tighter spreads; A-Mark reported $5.74B revenue in 2024 and concedes volume discounts. Financial substitutes (GLD ~60B AUM; COMEX OI >600k) and intermittent risk-off (VIX ~16) keep buyer power elevated.

| Metric | 2024 |

|---|---|

| A-Mark revenue | $5.74B |

| GLD AUM | $60B |

| COMEX OI | >600k contracts |

| VIX average | ~16 |

Preview Before You Purchase

A-Mark Porter's Five Forces Analysis

This preview shows A‑Mark's Porter’s Five Forces Analysis and is the exact document you’ll receive immediately after purchase—no placeholders or samples. The report is professionally formatted, complete, and ready for download and use the moment payment is processed. No surprises; the file available to you post‑purchase is precisely this one.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

A-Mark’s Porter's Five Forces snapshot highlights moderate supplier power, high buyer price sensitivity, low substitute threat, and intense rivalry among bullion dealers. Regulatory and entry barriers shape profitability and margins. This brief preview outlines key pressures and strategic implications. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated mints & refiners

A-Mark depends on a limited set of sovereign mints (notably the U.S. Mint and Royal Canadian Mint) and LBMA-accredited refiners that control iconic coins and purity standards, concentrating supply power. This concentration raises supplier leverage over allocations, premiums and commercial terms, even as preferred-dealer status and multi-sourcing mitigate but do not eliminate the dependence. Disruptions at these suppliers can rapidly tighten A-Mark inventory and widen retail–wholesale spreads.

Allocation and premium control

Sovereign mints such as the U.S. Mint and Royal Canadian Mint control production schedules, product mixes and allocation formulas that can ration supply in high-demand periods. Suppliers raised fabrication premiums in 2024, compressing distributor margins and pressuring spreads. A-Mark offsets volatility with forward commitments and strategic inventory positioning, yet upstream pricing power and brand-specific coin scarcity maintain supplier leverage. Limited substitution for flagship coins sustains that influence.

Commodity pass-through dynamics

Spot metal costs are largely pass-through to customers, while fabrication premiums and logistics are retained by suppliers and not fully passed through; when market volatility spikes suppliers can reprice terms and premiums faster than distributors can reset multi-channel pricing, temporarily increasing supplier power. Hedging reduces exposure but cannot eliminate basis mismatches and premium/logistics risk.

Logistics and custody dependencies

Approved vaults, assay labs, and insured transport providers remain specialized and limited, concentrating leverage among a few gateway nodes; dependence on these third parties gives suppliers pricing and priority power that can spike rapidly if capacity tightens. A-Mark’s integrated logistics reduce exposure but still interfaces with external custodians and carriers, creating chokepoints where a single bottleneck can abruptly elevate supplier bargaining power. Recent industry reporting in 2024 highlighted ongoing consolidation among custodial vaults, reinforcing this concentrated supply-side risk.

- Few specialized providers: concentrated custody and assay capacity

- Supplier leverage: price and priority control at chokepoints

- A-Mark mitigation: integrated logistics, but third-party interfaces remain

- 2024 trend: continued custodial consolidation increasing systemic vulnerability

Compliance and ESG constraints

Compliance and ESG constraints (responsible sourcing, KYC/AML, sanctions screening) materially narrow eligible supplier pools; FATF's 40 recommendations (2024) underpin tougher due diligence that favors accredited suppliers who command price and contractual advantages. A-Mark’s scale and compliance infrastructure improve access but do not eliminate scarcity premiums, and further regulatory tightening would likely boost supplier power.

- Responsible sourcing narrows suppliers

- KYC/AML increases onboarding friction

- Sanctions screening elevates counterparty risk

- Accredited suppliers gain pricing leverage

Mint/refiner concentration tightens allocations, raising fabrication premiums and widening spreads

A-Mark faces concentrated supplier power from sovereign mints and LBMA refiners, giving suppliers leverage over allocations, premiums and terms. 2024 saw rising fabrication premiums and custodial consolidation, tightening allocations and widening retail–wholesale spreads despite A-Mark’s hedging and integrated logistics. Compliance rules further narrow suppliers, sustaining scarcity premiums.

| Metric | 2024 Signal |

|---|---|

| Fabrication premiums | Increased (industry reports 2024) |

| Custodial concentration | Higher consolidation (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to A‑Mark, with detailed evaluation of supplier and buyer power, substitutes, rivalry, and entry barriers; identifies disruptive threats and strategic levers to protect margins and market share, delivered in fully editable Word format for decks, plans, or reports.

A concise, one-sheet Porter's Five Forces for A‑Mark that instantly relieves decision paralysis by visualizing competitive pressures and priority actions; ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

High price transparency

High price transparency — with spot quotes and premiums posted in real time on platforms like Kitco and dealers in 2024 — lets buyers compare and arbitrage spreads often below 1%, compressing margins. Buyers routinely exploit sub-1% spread differences, increasing pressure on dealer premiums and execution fees. A-Mark offsets this by offering deep inventory and reliable trade execution, but transparency structurally raises buyer leverage.

Low switching costs

Wholesale and retail customers can pivot among dealers and e-commerce sites with minimal friction, as shipping, live pricing and payment rails are industry-standard; A-Mark (NASDAQ: AMRK) offsets this by offering financing, vaulted storage and liquidity services that increase client stickiness. Despite these services, baseline switching costs remain low, keeping buyer bargaining power elevated in 2024.

Volume buyer leverage

Institutions, large dealers, and OEMs extract tighter spreads and priority allocations from A-Mark, leveraging steady order flow — A-Mark reported $5.74 billion revenue in 2024, underscoring scale that attracts large buyers. The firm routinely trades concessions for wallet share and multi-year contracts to lock in volume. Concentration of top accounts materially amplifies buyer bargaining power, pressuring margins on headline volumes.

Demand cyclicality

During risk-off surges buyers exhibit urgency that reduces price sensitivity and eases buyer power; 2024 saw the VIX average near 16, reflecting intermittent risk-off episodes that tightened supply willingness. In calmer 2024 quarters, buyers pushed for lower premiums and extended terms, and A-Mark’s diversified channels (wholesale, retail, B2B) smooth but cannot fully offset these shifts. Seasonality and macro sentiment swing leverage back to buyers in normal times.

- Risk-off: lower buyer price sensitivity

- Calm markets: demand for lower premiums, longer terms

- A-Mark diversification dampens but not eliminates cycles

- 2024 VIX ~16 indicates recurring risk-off spikes

Substitute access

Customers can pivot to ETFs, futures, or tokenized metals for exposure without handling physical, and ready alternatives compress A-Mark’s leverage over premiums and storage fees; SPDR Gold Shares (GLD) held about 60 billion USD AUM in 2024 while COMEX gold futures open interest regularly exceeded 600k contracts, keeping financial substitutes compelling despite A-Mark’s physical deliverability, product variety, and custody services.

- Substitute access: ETFs, futures, tokenized metals

- 2024 tags: GLD ~60B AUM; COMEX OI >600k

- A-Mark strengths: physical delivery, SKU breadth, custody

- Impact: tighter premiums, selective customer migration

Price transparency and low switching costs empower buyers, squeezing precious-metal premiums

High price transparency and low switching costs in 2024 give customers strong leverage, compressing premiums despite A-Mark’s scale. Large buyers extract tighter spreads; A-Mark reported $5.74B revenue in 2024 and concedes volume discounts. Financial substitutes (GLD ~60B AUM; COMEX OI >600k) and intermittent risk-off (VIX ~16) keep buyer power elevated.

| Metric | 2024 |

|---|---|

| A-Mark revenue | $5.74B |

| GLD AUM | $60B |

| COMEX OI | >600k contracts |

| VIX average | ~16 |

Preview Before You Purchase

A-Mark Porter's Five Forces Analysis

This preview shows A‑Mark's Porter’s Five Forces Analysis and is the exact document you’ll receive immediately after purchase—no placeholders or samples. The report is professionally formatted, complete, and ready for download and use the moment payment is processed. No surprises; the file available to you post‑purchase is precisely this one.