Ambac Porter's Five Forces Analysis

From Overview to Strategy Blueprint

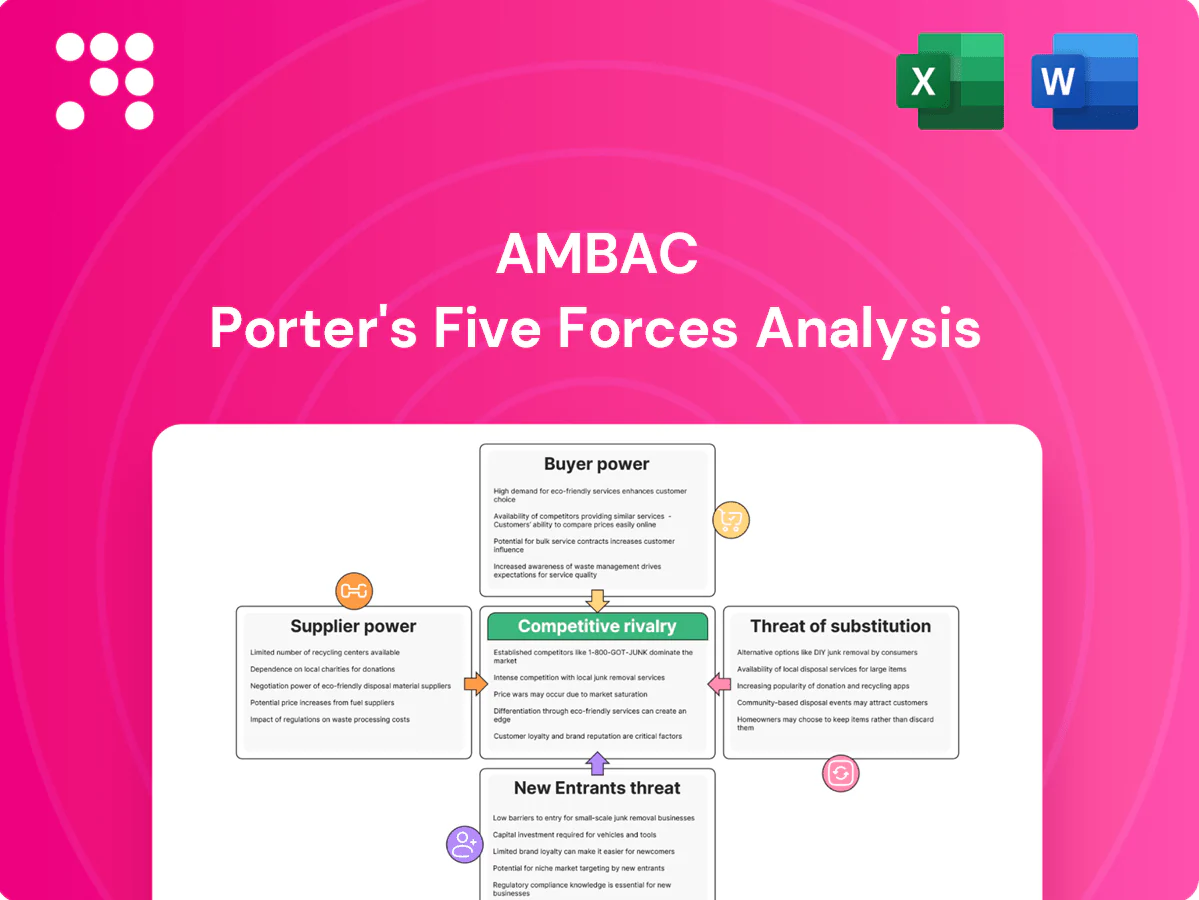

Ambac faces significant buyer scrutiny and regulatory pressure, while credit market dynamics and competitor strategies shape its margin risk. Supplier concentration and substitutes introduce tactical vulnerabilities that require close monitoring. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Dependence on capital providers

Ambac’s capacity and pricing hinge on access to low-cost, long-duration capital provided by debt investors, equity holders and reinsurers; these parties effectively supply risk-bearing capacity. When capital tightens their bargaining power rises, compressing margins and limiting new guarantees. Broad credit cycles amplify this dependency, especially with U.S. policy rates around 5.25–5.50% in 2024.

Rating agencies as quasi-suppliers

Rating agencies act as quasi-suppliers for Ambac by supplying credibility essential to sell wraps and guarantees, and methodology shifts can force rapid changes in business mix and product terms. Their influence shapes underwriting standards and the pace of growth, since the Big Three accounted for roughly 90% of global issuer-paid ratings in 2024. A negative outlook from a major agency can materially raise Ambac’s funding costs and capital charges, tightening capacity and margins.

Bank and dealer pipelines

Underwriting banks originate the municipal and structured finance deals Ambac insures, and concentrated arranger relationships—with the top 5 underwriters handling roughly 46% of negotiated municipal placement in 2024—give banks leverage over fee splits and contract terms.

Pipeline access is often conditioned on pricing flexibility and rating support, and losing key channels can sharply reduce volume visibility and near-term insured issuance.

Specialist data, models, and tech

Specialist credit performance data, catastrophe/ESG analytics and modeling platforms (eg Verisk, RMS, AIR) underpin Ambac’s risk selection, letting vendors with proprietary datasets command premium pricing and sticky multi-year contracts; switching costs and validation burdens (internal model revalidation, regulatory checks) raise supplier power and integration risk deters rapid changes.

- Proprietary datasets: high pricing

- Validation burden: slow switching

- Integration risk: lock-in

Reinsurers and retrocession

Reinsurers and retrocession optimize Ambac’s capital and reduce volatility but act as powerful suppliers whose pricing and terms tightened during the 2023–2024 hard reinsurance market, raising ceding costs and reducing capacity for chunky or correlated municipal credit risks.

Counterparty credit limits from reinsurers and retrocessionaires constrain Ambac’s growth and underwriting appetite, increasing dependency where exposures concentrate or for large single-name guarantees.

- Market: hardening in 2023–2024 raised ceding costs

- Capacity: tighter terms reduce available cover for large/correlated risks

- Credit limits: reinsurer limits directly cap Ambac growth

Supplier power squeezes muni insurer: rates ~5.25–5.50%, ratings concentrated

Ambac faces strong supplier power: capital providers, reinsurers and rating agencies can tighten capacity and raise costs, amplified by 2024 U.S. policy rates (~5.25–5.50%). Rating concentration (Big Three ~90% of issuer-paid ratings in 2024) and top-5 underwriters controlling ~46% of negotiated municipal placement increase dependency. A hard reinsurance market in 2023–2024 raised ceding costs and constrained large-ticket capacity.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Capital providers | Rates ~5.25–5.50% | Higher funding costs |

| Rating agencies | Big Three ~90% | Rating-driven terms |

| Underwriters | Top 5 ~46% | Pipeline leverage |

| Reinsurers | Hard market 2023–24 | Tighter capacity/ceding costs |

What is included in the product

Tailored Porter's Five Forces analysis for Ambac that uncovers competitive drivers, buyer/supplier influence, substitutes and entry barriers, identifies disruptive threats to market share, and delivers strategic insights suitable for investor materials, internal strategy decks, or academic use.

Clear one-sheet Porter's Five Forces for Ambac—quickly visualizes competitive pressures with an editable radar chart and simple layout, so teams can customize inputs, compare scenarios, and drop slides into decks without code or finance expertise.

Customers Bargaining Power

Municipal issuers’ price sensitivity

Cities, states and authorities weigh guarantee costs against yield savings, with insurers' premiums typically ranging roughly 5–60 basis points and issuers demanding commensurate yield relief to justify the fee. In low-spread markets (post-2023–24 tightening) many issuers push for lower premiums or opt to go uninsured. Larger issuers run competitive RFPs to extract concessions, and fiscal constraints and budget pressures amplify issuers' bargaining power.

Structured finance sponsors

Structured finance sponsors model tranche economics precisely, often replacing monoline wraps with internal credit enhancement when spreads widen; in 2024 top sponsors accounted for roughly 65% of placements, reducing reliance on external guarantees. Competitive placement markets and deeper investor demand let sponsors forego wraps if spread pick-up exceeds wrap costs. Scale sponsors therefore wield strong negotiating leverage over pricing and terms.

Institutional investors’ preferences

Institutional investors, which own about 70% of the U.S. municipal market (2023–24), have outsized influence on demand for insured paper and by extension on insurer ratings and market access. If the buy-side tolerates uninsured risk, demand for wraps falls and pricing compresses as wrap fees become less necessary. In risk-off periods buyers seek stronger guarantees and tighter covenants, swinging pricing power cyclically.

Insurance distribution clients

In Ambac’s distribution arm, carriers and agencies actively benchmark commissions and placement terms; multi-channel distribution and digital platforms—which captured about 30% of new-policy sales in 2024—raise switching ease, while large carriers leverage scale to negotiate tighter economics and service-level agreements, compressing intermediary margins and pressuring commission rates.

- Benchmarking pressure on commissions

- 30% digital channel share (2024)

- Large carriers negotiate SLAs/economics

- Intermediary margin compression

Concentration of large accounts

High-value issuers and sponsors supply outsized premium pools for Ambac; losing a single large account in 2024 would force aggressive repricing to recapture volume, as relationship stickiness mitigates but does not eliminate concentrated buyer leverage. Tailored covenants and pricing concessions increasingly serve as bargaining chips in renewal negotiations.

- Concentration magnifies leverage

- Loss triggers aggressive pricing

- Relationship stickiness limits but doesn’t remove risk

- Customized terms used to retain business

Concentration drives aggressive repricing: top sponsors ~65% and institutions ~70% ownership

Cities, sponsors and large institutional buyers exert strong bargaining power: premiums typically 5–60 bps, top sponsors drove ~65% of placements in 2024, and institutional investors own ~70% of the U.S. muni market. Digital channels reached ~30% of new-policy sales, compressing commissions. Concentration means losing one large account forces aggressive repricing.

| Metric | 2024 value |

|---|---|

| Insurer premium range | 5–60 bps |

| Top sponsors share | ~65% |

| Institutional ownership | ~70% |

| Digital sales share | ~30% |

What You See Is What You Get

Ambac Porter's Five Forces Analysis

This preview shows the exact Ambac Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you complete payment. What you see is the final deliverable, available instantly.

From Overview to Strategy Blueprint

Ambac faces significant buyer scrutiny and regulatory pressure, while credit market dynamics and competitor strategies shape its margin risk. Supplier concentration and substitutes introduce tactical vulnerabilities that require close monitoring. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Dependence on capital providers

Ambac’s capacity and pricing hinge on access to low-cost, long-duration capital provided by debt investors, equity holders and reinsurers; these parties effectively supply risk-bearing capacity. When capital tightens their bargaining power rises, compressing margins and limiting new guarantees. Broad credit cycles amplify this dependency, especially with U.S. policy rates around 5.25–5.50% in 2024.

Rating agencies as quasi-suppliers

Rating agencies act as quasi-suppliers for Ambac by supplying credibility essential to sell wraps and guarantees, and methodology shifts can force rapid changes in business mix and product terms. Their influence shapes underwriting standards and the pace of growth, since the Big Three accounted for roughly 90% of global issuer-paid ratings in 2024. A negative outlook from a major agency can materially raise Ambac’s funding costs and capital charges, tightening capacity and margins.

Bank and dealer pipelines

Underwriting banks originate the municipal and structured finance deals Ambac insures, and concentrated arranger relationships—with the top 5 underwriters handling roughly 46% of negotiated municipal placement in 2024—give banks leverage over fee splits and contract terms.

Pipeline access is often conditioned on pricing flexibility and rating support, and losing key channels can sharply reduce volume visibility and near-term insured issuance.

Specialist data, models, and tech

Specialist credit performance data, catastrophe/ESG analytics and modeling platforms (eg Verisk, RMS, AIR) underpin Ambac’s risk selection, letting vendors with proprietary datasets command premium pricing and sticky multi-year contracts; switching costs and validation burdens (internal model revalidation, regulatory checks) raise supplier power and integration risk deters rapid changes.

- Proprietary datasets: high pricing

- Validation burden: slow switching

- Integration risk: lock-in

Reinsurers and retrocession

Reinsurers and retrocession optimize Ambac’s capital and reduce volatility but act as powerful suppliers whose pricing and terms tightened during the 2023–2024 hard reinsurance market, raising ceding costs and reducing capacity for chunky or correlated municipal credit risks.

Counterparty credit limits from reinsurers and retrocessionaires constrain Ambac’s growth and underwriting appetite, increasing dependency where exposures concentrate or for large single-name guarantees.

- Market: hardening in 2023–2024 raised ceding costs

- Capacity: tighter terms reduce available cover for large/correlated risks

- Credit limits: reinsurer limits directly cap Ambac growth

Supplier power squeezes muni insurer: rates ~5.25–5.50%, ratings concentrated

Ambac faces strong supplier power: capital providers, reinsurers and rating agencies can tighten capacity and raise costs, amplified by 2024 U.S. policy rates (~5.25–5.50%). Rating concentration (Big Three ~90% of issuer-paid ratings in 2024) and top-5 underwriters controlling ~46% of negotiated municipal placement increase dependency. A hard reinsurance market in 2023–2024 raised ceding costs and constrained large-ticket capacity.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Capital providers | Rates ~5.25–5.50% | Higher funding costs |

| Rating agencies | Big Three ~90% | Rating-driven terms |

| Underwriters | Top 5 ~46% | Pipeline leverage |

| Reinsurers | Hard market 2023–24 | Tighter capacity/ceding costs |

What is included in the product

Tailored Porter's Five Forces analysis for Ambac that uncovers competitive drivers, buyer/supplier influence, substitutes and entry barriers, identifies disruptive threats to market share, and delivers strategic insights suitable for investor materials, internal strategy decks, or academic use.

Clear one-sheet Porter's Five Forces for Ambac—quickly visualizes competitive pressures with an editable radar chart and simple layout, so teams can customize inputs, compare scenarios, and drop slides into decks without code or finance expertise.

Customers Bargaining Power

Municipal issuers’ price sensitivity

Cities, states and authorities weigh guarantee costs against yield savings, with insurers' premiums typically ranging roughly 5–60 basis points and issuers demanding commensurate yield relief to justify the fee. In low-spread markets (post-2023–24 tightening) many issuers push for lower premiums or opt to go uninsured. Larger issuers run competitive RFPs to extract concessions, and fiscal constraints and budget pressures amplify issuers' bargaining power.

Structured finance sponsors

Structured finance sponsors model tranche economics precisely, often replacing monoline wraps with internal credit enhancement when spreads widen; in 2024 top sponsors accounted for roughly 65% of placements, reducing reliance on external guarantees. Competitive placement markets and deeper investor demand let sponsors forego wraps if spread pick-up exceeds wrap costs. Scale sponsors therefore wield strong negotiating leverage over pricing and terms.

Institutional investors’ preferences

Institutional investors, which own about 70% of the U.S. municipal market (2023–24), have outsized influence on demand for insured paper and by extension on insurer ratings and market access. If the buy-side tolerates uninsured risk, demand for wraps falls and pricing compresses as wrap fees become less necessary. In risk-off periods buyers seek stronger guarantees and tighter covenants, swinging pricing power cyclically.

Insurance distribution clients

In Ambac’s distribution arm, carriers and agencies actively benchmark commissions and placement terms; multi-channel distribution and digital platforms—which captured about 30% of new-policy sales in 2024—raise switching ease, while large carriers leverage scale to negotiate tighter economics and service-level agreements, compressing intermediary margins and pressuring commission rates.

- Benchmarking pressure on commissions

- 30% digital channel share (2024)

- Large carriers negotiate SLAs/economics

- Intermediary margin compression

Concentration of large accounts

High-value issuers and sponsors supply outsized premium pools for Ambac; losing a single large account in 2024 would force aggressive repricing to recapture volume, as relationship stickiness mitigates but does not eliminate concentrated buyer leverage. Tailored covenants and pricing concessions increasingly serve as bargaining chips in renewal negotiations.

- Concentration magnifies leverage

- Loss triggers aggressive pricing

- Relationship stickiness limits but doesn’t remove risk

- Customized terms used to retain business

Concentration drives aggressive repricing: top sponsors ~65% and institutions ~70% ownership

Cities, sponsors and large institutional buyers exert strong bargaining power: premiums typically 5–60 bps, top sponsors drove ~65% of placements in 2024, and institutional investors own ~70% of the U.S. muni market. Digital channels reached ~30% of new-policy sales, compressing commissions. Concentration means losing one large account forces aggressive repricing.

| Metric | 2024 value |

|---|---|

| Insurer premium range | 5–60 bps |

| Top sponsors share | ~65% |

| Institutional ownership | ~70% |

| Digital sales share | ~30% |

What You See Is What You Get

Ambac Porter's Five Forces Analysis

This preview shows the exact Ambac Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you complete payment. What you see is the final deliverable, available instantly.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Ambac faces significant buyer scrutiny and regulatory pressure, while credit market dynamics and competitor strategies shape its margin risk. Supplier concentration and substitutes introduce tactical vulnerabilities that require close monitoring. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Dependence on capital providers

Ambac’s capacity and pricing hinge on access to low-cost, long-duration capital provided by debt investors, equity holders and reinsurers; these parties effectively supply risk-bearing capacity. When capital tightens their bargaining power rises, compressing margins and limiting new guarantees. Broad credit cycles amplify this dependency, especially with U.S. policy rates around 5.25–5.50% in 2024.

Rating agencies as quasi-suppliers

Rating agencies act as quasi-suppliers for Ambac by supplying credibility essential to sell wraps and guarantees, and methodology shifts can force rapid changes in business mix and product terms. Their influence shapes underwriting standards and the pace of growth, since the Big Three accounted for roughly 90% of global issuer-paid ratings in 2024. A negative outlook from a major agency can materially raise Ambac’s funding costs and capital charges, tightening capacity and margins.

Bank and dealer pipelines

Underwriting banks originate the municipal and structured finance deals Ambac insures, and concentrated arranger relationships—with the top 5 underwriters handling roughly 46% of negotiated municipal placement in 2024—give banks leverage over fee splits and contract terms.

Pipeline access is often conditioned on pricing flexibility and rating support, and losing key channels can sharply reduce volume visibility and near-term insured issuance.

Specialist data, models, and tech

Specialist credit performance data, catastrophe/ESG analytics and modeling platforms (eg Verisk, RMS, AIR) underpin Ambac’s risk selection, letting vendors with proprietary datasets command premium pricing and sticky multi-year contracts; switching costs and validation burdens (internal model revalidation, regulatory checks) raise supplier power and integration risk deters rapid changes.

- Proprietary datasets: high pricing

- Validation burden: slow switching

- Integration risk: lock-in

Reinsurers and retrocession

Reinsurers and retrocession optimize Ambac’s capital and reduce volatility but act as powerful suppliers whose pricing and terms tightened during the 2023–2024 hard reinsurance market, raising ceding costs and reducing capacity for chunky or correlated municipal credit risks.

Counterparty credit limits from reinsurers and retrocessionaires constrain Ambac’s growth and underwriting appetite, increasing dependency where exposures concentrate or for large single-name guarantees.

- Market: hardening in 2023–2024 raised ceding costs

- Capacity: tighter terms reduce available cover for large/correlated risks

- Credit limits: reinsurer limits directly cap Ambac growth

Supplier power squeezes muni insurer: rates ~5.25–5.50%, ratings concentrated

Ambac faces strong supplier power: capital providers, reinsurers and rating agencies can tighten capacity and raise costs, amplified by 2024 U.S. policy rates (~5.25–5.50%). Rating concentration (Big Three ~90% of issuer-paid ratings in 2024) and top-5 underwriters controlling ~46% of negotiated municipal placement increase dependency. A hard reinsurance market in 2023–2024 raised ceding costs and constrained large-ticket capacity.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Capital providers | Rates ~5.25–5.50% | Higher funding costs |

| Rating agencies | Big Three ~90% | Rating-driven terms |

| Underwriters | Top 5 ~46% | Pipeline leverage |

| Reinsurers | Hard market 2023–24 | Tighter capacity/ceding costs |

What is included in the product

Tailored Porter's Five Forces analysis for Ambac that uncovers competitive drivers, buyer/supplier influence, substitutes and entry barriers, identifies disruptive threats to market share, and delivers strategic insights suitable for investor materials, internal strategy decks, or academic use.

Clear one-sheet Porter's Five Forces for Ambac—quickly visualizes competitive pressures with an editable radar chart and simple layout, so teams can customize inputs, compare scenarios, and drop slides into decks without code or finance expertise.

Customers Bargaining Power

Municipal issuers’ price sensitivity

Cities, states and authorities weigh guarantee costs against yield savings, with insurers' premiums typically ranging roughly 5–60 basis points and issuers demanding commensurate yield relief to justify the fee. In low-spread markets (post-2023–24 tightening) many issuers push for lower premiums or opt to go uninsured. Larger issuers run competitive RFPs to extract concessions, and fiscal constraints and budget pressures amplify issuers' bargaining power.

Structured finance sponsors

Structured finance sponsors model tranche economics precisely, often replacing monoline wraps with internal credit enhancement when spreads widen; in 2024 top sponsors accounted for roughly 65% of placements, reducing reliance on external guarantees. Competitive placement markets and deeper investor demand let sponsors forego wraps if spread pick-up exceeds wrap costs. Scale sponsors therefore wield strong negotiating leverage over pricing and terms.

Institutional investors’ preferences

Institutional investors, which own about 70% of the U.S. municipal market (2023–24), have outsized influence on demand for insured paper and by extension on insurer ratings and market access. If the buy-side tolerates uninsured risk, demand for wraps falls and pricing compresses as wrap fees become less necessary. In risk-off periods buyers seek stronger guarantees and tighter covenants, swinging pricing power cyclically.

Insurance distribution clients

In Ambac’s distribution arm, carriers and agencies actively benchmark commissions and placement terms; multi-channel distribution and digital platforms—which captured about 30% of new-policy sales in 2024—raise switching ease, while large carriers leverage scale to negotiate tighter economics and service-level agreements, compressing intermediary margins and pressuring commission rates.

- Benchmarking pressure on commissions

- 30% digital channel share (2024)

- Large carriers negotiate SLAs/economics

- Intermediary margin compression

Concentration of large accounts

High-value issuers and sponsors supply outsized premium pools for Ambac; losing a single large account in 2024 would force aggressive repricing to recapture volume, as relationship stickiness mitigates but does not eliminate concentrated buyer leverage. Tailored covenants and pricing concessions increasingly serve as bargaining chips in renewal negotiations.

- Concentration magnifies leverage

- Loss triggers aggressive pricing

- Relationship stickiness limits but doesn’t remove risk

- Customized terms used to retain business

Concentration drives aggressive repricing: top sponsors ~65% and institutions ~70% ownership

Cities, sponsors and large institutional buyers exert strong bargaining power: premiums typically 5–60 bps, top sponsors drove ~65% of placements in 2024, and institutional investors own ~70% of the U.S. muni market. Digital channels reached ~30% of new-policy sales, compressing commissions. Concentration means losing one large account forces aggressive repricing.

| Metric | 2024 value |

|---|---|

| Insurer premium range | 5–60 bps |

| Top sponsors share | ~65% |

| Institutional ownership | ~70% |

| Digital sales share | ~30% |

What You See Is What You Get

Ambac Porter's Five Forces Analysis

This preview shows the exact Ambac Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you complete payment. What you see is the final deliverable, available instantly.