AMC Networks Porter's Five Forces Analysis

From Overview to Strategy Blueprint

AMC Networks faces moderate buyer power, rising substitute threats from streaming platforms, limited supplier leverage for premium content, and barriers that temper new entrants but intensify competition among incumbents. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AMC Networks’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Premium talent and showrunners leverage

High-profile writers, directors and actors can command premium fees—top showrunners and A-list talent often earn in excess of $1 million per episode—raising supplier power for AMC. Scarcity of top-tier creators fuels bidding across networks and streamers, intensifying acquisition costs. The 2023 WGA strike (148 days) and SAG-AFTRA action (118 days) demonstrated how labor stoppages halt pipelines and spike costs. AMC must weigh star-driven prestige against strict cost discipline to protect margins.

Studios and rights-holders concentration

AMC licenses key content from a concentrated set of major studios and BBC Studios for BBC America, concentrating negotiating power with a few suppliers and raising costs via exclusive windowing, escalators and minimum guarantees. Limited alternative sources for prestige scripted IP increase switching costs and bargaining leverage for suppliers. Co-productions reduce spend but do not remove dependence on studio-controlled IP. AMC Networks reported $2.67B revenue in 2024.

Union and guild constraints

Guild agreements (WGA ~11,500 members, SAG-AFTRA ~160,000) set wage floors, residuals and strict work rules that constrain production flexibility; the 2023 WGA strike lasted 148 days and SAG-AFTRA 118 days, showing disruption risk. Periodic renegotiations create step-up costs and uncertainty, streaming residuals shift unit economics versus linear, and compliance is non-negotiable, limiting AMC’s pricing latitude with suppliers.

Technology and distribution infrastructure vendors

Technology and distribution vendors—CDNs, cloud, DRM and analytics—exert soft power over AMC Networks' streaming through pricing and SLAs; the global CDN market was about $20 billion in 2024 and peak events can raise capacity costs by roughly 2–3x, making switching complex and QoS-risky.

- Dependency: high

- Switching risk: elevated

- Peak cost impact: 2–3x

- Mitigation: multi-vendor (adds integration complexity)

Music, format, and niche content rights

Music licensing, international format deals, and niche genre rights (notably Shudder’s horror catalog) are fragmented and can be disproportionately expensive; clearance risks and holdbacks routinely delay releases and raise legal overhead for AMC Networks. Small rights-holders for scarce niches can demand outsized terms, while cross-service bundling helps but is often infeasible.

- Licensing fragmentation raises costs and delays

- Niche scarcity increases bargaining leverage

- Clearance/holdbacks add legal overhead

- Bundling eases negotiation but limited in practice

Talent & CDNs squeeze margins — top pay > $1M/ep, CDN market ~$20B

Suppliers wield high power: A‑list talent can exceed 1M per episode and studios/BBC hold scarce IP, pushing costs up; AMC reported $2.67B revenue in 2024. Guild rules (WGA ~11,500; SAG‑AFTRA ~160,000) and 2023 strikes (WGA 148d, SAG‑AFTRA 118d) raise disruption risk and step‑up costs. CDNs/cloud (global CDN market ~$20B in 2024) can double–triple peak delivery costs, making multi‑vendor mitigation complex.

| Metric | Value |

|---|---|

| AMC revenue (2024) | $2.67B |

| Top talent pay | >$1M/ep |

| WGA / SAG‑AFTRA | 11,500 / 160,000 |

| CDN market (2024) | $20B |

| Peak cost uplift | 2–3x |

What is included in the product

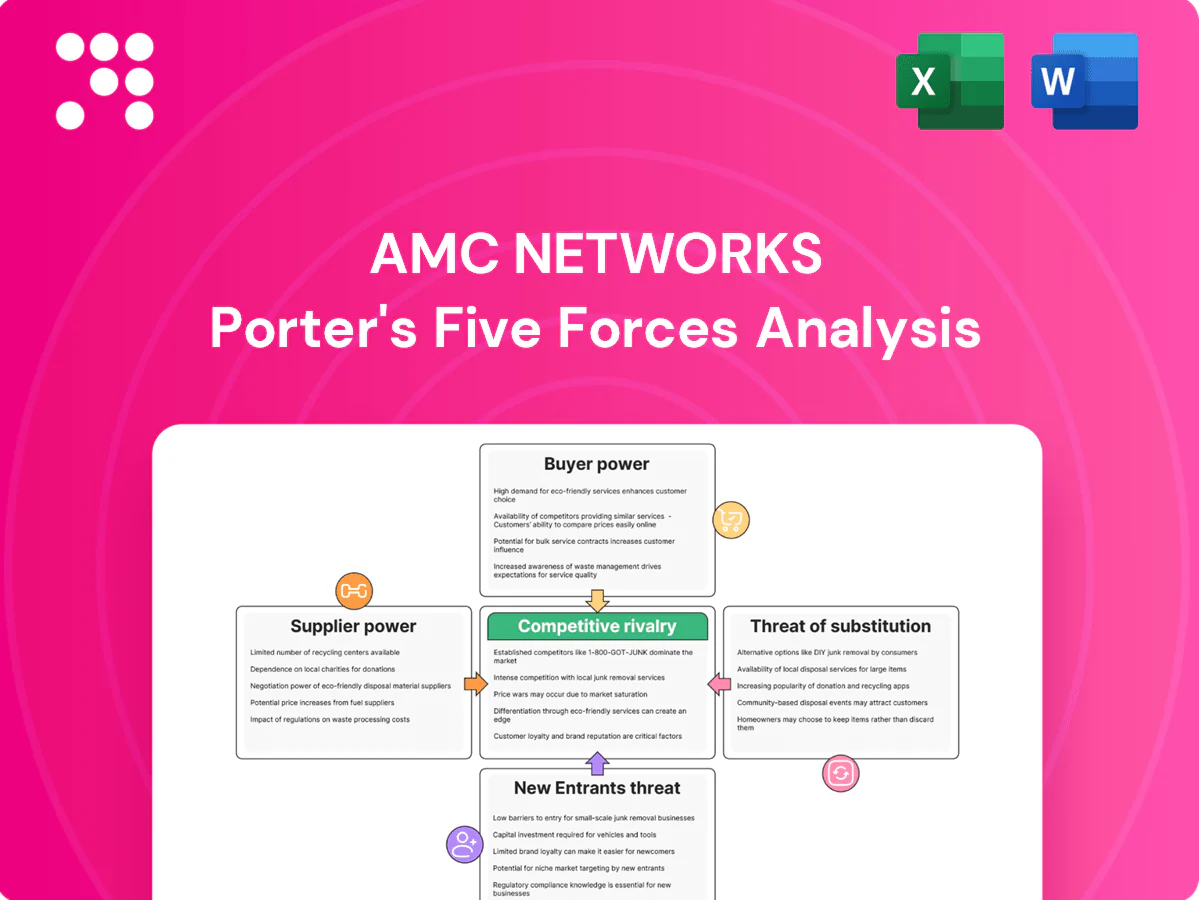

Tailored Porter's Five Forces analysis for AMC Networks, highlighting competitive rivalry, buyer and supplier power, threat of substitutes and entrants, and identifying strategic pressures and opportunities shaping its profitability.

One-sheet Porter’s Five Forces for AMC Networks that instantly highlights competitive pressures and streaming threats, ready to copy into pitch decks or board slides. Customize force levels with your data and view strategic exposure on a clean spider chart—no code, easy for non-finance users.

Customers Bargaining Power

MVPDs and vMVPDs carriage power

Pay-TV operators and vMVPDs negotiate affiliate fees and placement for AMC’s linear nets, with a small number of consolidated distributors controlling over 60% of multichannel subscribers and thus strong leverage. They can threaten tiering, downgrades or blackouts to extract concessions, and cord-cutting—U.S. pay-TV households down roughly 20% since 2019 through 2024—heightens sensitivity to channel value. AMC must demonstrate audience engagement and measurable ad ROI to sustain per-subscriber rates.

Direct-to-consumer churn sensitivity

AMC Networks faces high DTC churn sensitivity as AMC+, Shudder and Acorn TV subscribers face low switching costs and monthly cancellation options, contributing to an industry average SVOD monthly churn of about 2.6% in 2024. Content drop-offs or price hikes prompt immediate cancellations, while promotional pricing conditions customers to shop for deals. Stabilizing LTV/CAC requires a robust release cadence and bundling across brands to reduce churn and lift retention.

Advertisers’ budget flexibility

Brands reallocate spend across linear, CTV, social and search, increasing price pressure; US CTV ad spend grew roughly 20% YoY to about $21B in 2024, shifting dollars from linear.

Measurement is moving to outcomes and attribution—around 70% of marketers in 2024 prioritized ROI-based metrics—raising demand for better data and targeting.

Economic slowdowns compress CPMs and scatter demand, so AMC must deliver distinctive, addressable audiences to protect yield.

Platform gatekeepers’ influence

Platform gatekeepers — app stores and CTV marketplaces like Apple, Google and Roku — control discovery and billing, with App Store commissions of 15–30% (2024 rules) and similar take rates on CTV transactions, reducing AMC’s net ARPU; prominence and merchandising on these platforms directly affect subscriber flow. Direct billing via owned apps improves margins but limits reach versus platform distribution.

- Discovery control: Apple/Google/Roku

- Take rates: App Store 15–30% (2024)

- Prominence = subscriber flow

- Owned apps: higher ARPU, lower reach

International distributors’ selectivity

Outside the U.S., international distributors choose among a crowded pool of content suppliers, and with global streaming subscriptions exceeding 1 billion in 2024, competition for shelf space intensified; cultural fit and dubbing/subtitling requirements add negotiation friction, while buyers increasingly demand broader rights at lower per-territory prices, forcing AMC to tailor windows, packaging, and pricing to secure favorable slots.

- High selectivity: many suppliers vs. limited slots

- Localization friction: dubbing/subtitles raise costs and lead times

- Pricing pressure: demand for wider rights at lower per-territory fees

Distributor control >60% boosts leverage; CTV ads surge to $21B

Concentrated distributors control over 60% of multichannel subs and can force tiering/blackouts; US pay-TV households fell ~20% since 2019 (through 2024), increasing leverage. DTC churn ~2.6% monthly (2024) and CTV ad spend rose ~20% YoY to ~$21B, shifting buyer budgets. App stores/CTV marketplaces take 15–30% (2024), compressing ARPU; global streaming >1B subs intensifies licensing pressure.

| Metric | 2024 Value |

|---|---|

| Distributor share | >60% |

| Pay-TV decline since 2019 | ~20% |

| SVOD monthly churn | ~2.6% |

| CTV ad spend | ~$21B (+20% YoY) |

| App store take rates | 15–30% |

| Global streaming subs | >1B |

What You See Is What You Get

AMC Networks Porter's Five Forces Analysis

This preview shows the AMC Networks Porter's Five Forces analysis exactly as delivered—no placeholders or excerpts. The full, professionally formatted document you see here will be available to download immediately after purchase. Use it as-is for strategic or investment decisions.

From Overview to Strategy Blueprint

AMC Networks faces moderate buyer power, rising substitute threats from streaming platforms, limited supplier leverage for premium content, and barriers that temper new entrants but intensify competition among incumbents. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AMC Networks’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Premium talent and showrunners leverage

High-profile writers, directors and actors can command premium fees—top showrunners and A-list talent often earn in excess of $1 million per episode—raising supplier power for AMC. Scarcity of top-tier creators fuels bidding across networks and streamers, intensifying acquisition costs. The 2023 WGA strike (148 days) and SAG-AFTRA action (118 days) demonstrated how labor stoppages halt pipelines and spike costs. AMC must weigh star-driven prestige against strict cost discipline to protect margins.

Studios and rights-holders concentration

AMC licenses key content from a concentrated set of major studios and BBC Studios for BBC America, concentrating negotiating power with a few suppliers and raising costs via exclusive windowing, escalators and minimum guarantees. Limited alternative sources for prestige scripted IP increase switching costs and bargaining leverage for suppliers. Co-productions reduce spend but do not remove dependence on studio-controlled IP. AMC Networks reported $2.67B revenue in 2024.

Union and guild constraints

Guild agreements (WGA ~11,500 members, SAG-AFTRA ~160,000) set wage floors, residuals and strict work rules that constrain production flexibility; the 2023 WGA strike lasted 148 days and SAG-AFTRA 118 days, showing disruption risk. Periodic renegotiations create step-up costs and uncertainty, streaming residuals shift unit economics versus linear, and compliance is non-negotiable, limiting AMC’s pricing latitude with suppliers.

Technology and distribution infrastructure vendors

Technology and distribution vendors—CDNs, cloud, DRM and analytics—exert soft power over AMC Networks' streaming through pricing and SLAs; the global CDN market was about $20 billion in 2024 and peak events can raise capacity costs by roughly 2–3x, making switching complex and QoS-risky.

- Dependency: high

- Switching risk: elevated

- Peak cost impact: 2–3x

- Mitigation: multi-vendor (adds integration complexity)

Music, format, and niche content rights

Music licensing, international format deals, and niche genre rights (notably Shudder’s horror catalog) are fragmented and can be disproportionately expensive; clearance risks and holdbacks routinely delay releases and raise legal overhead for AMC Networks. Small rights-holders for scarce niches can demand outsized terms, while cross-service bundling helps but is often infeasible.

- Licensing fragmentation raises costs and delays

- Niche scarcity increases bargaining leverage

- Clearance/holdbacks add legal overhead

- Bundling eases negotiation but limited in practice

Talent & CDNs squeeze margins — top pay > $1M/ep, CDN market ~$20B

Suppliers wield high power: A‑list talent can exceed 1M per episode and studios/BBC hold scarce IP, pushing costs up; AMC reported $2.67B revenue in 2024. Guild rules (WGA ~11,500; SAG‑AFTRA ~160,000) and 2023 strikes (WGA 148d, SAG‑AFTRA 118d) raise disruption risk and step‑up costs. CDNs/cloud (global CDN market ~$20B in 2024) can double–triple peak delivery costs, making multi‑vendor mitigation complex.

| Metric | Value |

|---|---|

| AMC revenue (2024) | $2.67B |

| Top talent pay | >$1M/ep |

| WGA / SAG‑AFTRA | 11,500 / 160,000 |

| CDN market (2024) | $20B |

| Peak cost uplift | 2–3x |

What is included in the product

Tailored Porter's Five Forces analysis for AMC Networks, highlighting competitive rivalry, buyer and supplier power, threat of substitutes and entrants, and identifying strategic pressures and opportunities shaping its profitability.

One-sheet Porter’s Five Forces for AMC Networks that instantly highlights competitive pressures and streaming threats, ready to copy into pitch decks or board slides. Customize force levels with your data and view strategic exposure on a clean spider chart—no code, easy for non-finance users.

Customers Bargaining Power

MVPDs and vMVPDs carriage power

Pay-TV operators and vMVPDs negotiate affiliate fees and placement for AMC’s linear nets, with a small number of consolidated distributors controlling over 60% of multichannel subscribers and thus strong leverage. They can threaten tiering, downgrades or blackouts to extract concessions, and cord-cutting—U.S. pay-TV households down roughly 20% since 2019 through 2024—heightens sensitivity to channel value. AMC must demonstrate audience engagement and measurable ad ROI to sustain per-subscriber rates.

Direct-to-consumer churn sensitivity

AMC Networks faces high DTC churn sensitivity as AMC+, Shudder and Acorn TV subscribers face low switching costs and monthly cancellation options, contributing to an industry average SVOD monthly churn of about 2.6% in 2024. Content drop-offs or price hikes prompt immediate cancellations, while promotional pricing conditions customers to shop for deals. Stabilizing LTV/CAC requires a robust release cadence and bundling across brands to reduce churn and lift retention.

Advertisers’ budget flexibility

Brands reallocate spend across linear, CTV, social and search, increasing price pressure; US CTV ad spend grew roughly 20% YoY to about $21B in 2024, shifting dollars from linear.

Measurement is moving to outcomes and attribution—around 70% of marketers in 2024 prioritized ROI-based metrics—raising demand for better data and targeting.

Economic slowdowns compress CPMs and scatter demand, so AMC must deliver distinctive, addressable audiences to protect yield.

Platform gatekeepers’ influence

Platform gatekeepers — app stores and CTV marketplaces like Apple, Google and Roku — control discovery and billing, with App Store commissions of 15–30% (2024 rules) and similar take rates on CTV transactions, reducing AMC’s net ARPU; prominence and merchandising on these platforms directly affect subscriber flow. Direct billing via owned apps improves margins but limits reach versus platform distribution.

- Discovery control: Apple/Google/Roku

- Take rates: App Store 15–30% (2024)

- Prominence = subscriber flow

- Owned apps: higher ARPU, lower reach

International distributors’ selectivity

Outside the U.S., international distributors choose among a crowded pool of content suppliers, and with global streaming subscriptions exceeding 1 billion in 2024, competition for shelf space intensified; cultural fit and dubbing/subtitling requirements add negotiation friction, while buyers increasingly demand broader rights at lower per-territory prices, forcing AMC to tailor windows, packaging, and pricing to secure favorable slots.

- High selectivity: many suppliers vs. limited slots

- Localization friction: dubbing/subtitles raise costs and lead times

- Pricing pressure: demand for wider rights at lower per-territory fees

Distributor control >60% boosts leverage; CTV ads surge to $21B

Concentrated distributors control over 60% of multichannel subs and can force tiering/blackouts; US pay-TV households fell ~20% since 2019 (through 2024), increasing leverage. DTC churn ~2.6% monthly (2024) and CTV ad spend rose ~20% YoY to ~$21B, shifting buyer budgets. App stores/CTV marketplaces take 15–30% (2024), compressing ARPU; global streaming >1B subs intensifies licensing pressure.

| Metric | 2024 Value |

|---|---|

| Distributor share | >60% |

| Pay-TV decline since 2019 | ~20% |

| SVOD monthly churn | ~2.6% |

| CTV ad spend | ~$21B (+20% YoY) |

| App store take rates | 15–30% |

| Global streaming subs | >1B |

What You See Is What You Get

AMC Networks Porter's Five Forces Analysis

This preview shows the AMC Networks Porter's Five Forces analysis exactly as delivered—no placeholders or excerpts. The full, professionally formatted document you see here will be available to download immediately after purchase. Use it as-is for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

AMC Networks faces moderate buyer power, rising substitute threats from streaming platforms, limited supplier leverage for premium content, and barriers that temper new entrants but intensify competition among incumbents. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AMC Networks’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Premium talent and showrunners leverage

High-profile writers, directors and actors can command premium fees—top showrunners and A-list talent often earn in excess of $1 million per episode—raising supplier power for AMC. Scarcity of top-tier creators fuels bidding across networks and streamers, intensifying acquisition costs. The 2023 WGA strike (148 days) and SAG-AFTRA action (118 days) demonstrated how labor stoppages halt pipelines and spike costs. AMC must weigh star-driven prestige against strict cost discipline to protect margins.

Studios and rights-holders concentration

AMC licenses key content from a concentrated set of major studios and BBC Studios for BBC America, concentrating negotiating power with a few suppliers and raising costs via exclusive windowing, escalators and minimum guarantees. Limited alternative sources for prestige scripted IP increase switching costs and bargaining leverage for suppliers. Co-productions reduce spend but do not remove dependence on studio-controlled IP. AMC Networks reported $2.67B revenue in 2024.

Union and guild constraints

Guild agreements (WGA ~11,500 members, SAG-AFTRA ~160,000) set wage floors, residuals and strict work rules that constrain production flexibility; the 2023 WGA strike lasted 148 days and SAG-AFTRA 118 days, showing disruption risk. Periodic renegotiations create step-up costs and uncertainty, streaming residuals shift unit economics versus linear, and compliance is non-negotiable, limiting AMC’s pricing latitude with suppliers.

Technology and distribution infrastructure vendors

Technology and distribution vendors—CDNs, cloud, DRM and analytics—exert soft power over AMC Networks' streaming through pricing and SLAs; the global CDN market was about $20 billion in 2024 and peak events can raise capacity costs by roughly 2–3x, making switching complex and QoS-risky.

- Dependency: high

- Switching risk: elevated

- Peak cost impact: 2–3x

- Mitigation: multi-vendor (adds integration complexity)

Music, format, and niche content rights

Music licensing, international format deals, and niche genre rights (notably Shudder’s horror catalog) are fragmented and can be disproportionately expensive; clearance risks and holdbacks routinely delay releases and raise legal overhead for AMC Networks. Small rights-holders for scarce niches can demand outsized terms, while cross-service bundling helps but is often infeasible.

- Licensing fragmentation raises costs and delays

- Niche scarcity increases bargaining leverage

- Clearance/holdbacks add legal overhead

- Bundling eases negotiation but limited in practice

Talent & CDNs squeeze margins — top pay > $1M/ep, CDN market ~$20B

Suppliers wield high power: A‑list talent can exceed 1M per episode and studios/BBC hold scarce IP, pushing costs up; AMC reported $2.67B revenue in 2024. Guild rules (WGA ~11,500; SAG‑AFTRA ~160,000) and 2023 strikes (WGA 148d, SAG‑AFTRA 118d) raise disruption risk and step‑up costs. CDNs/cloud (global CDN market ~$20B in 2024) can double–triple peak delivery costs, making multi‑vendor mitigation complex.

| Metric | Value |

|---|---|

| AMC revenue (2024) | $2.67B |

| Top talent pay | >$1M/ep |

| WGA / SAG‑AFTRA | 11,500 / 160,000 |

| CDN market (2024) | $20B |

| Peak cost uplift | 2–3x |

What is included in the product

Tailored Porter's Five Forces analysis for AMC Networks, highlighting competitive rivalry, buyer and supplier power, threat of substitutes and entrants, and identifying strategic pressures and opportunities shaping its profitability.

One-sheet Porter’s Five Forces for AMC Networks that instantly highlights competitive pressures and streaming threats, ready to copy into pitch decks or board slides. Customize force levels with your data and view strategic exposure on a clean spider chart—no code, easy for non-finance users.

Customers Bargaining Power

MVPDs and vMVPDs carriage power

Pay-TV operators and vMVPDs negotiate affiliate fees and placement for AMC’s linear nets, with a small number of consolidated distributors controlling over 60% of multichannel subscribers and thus strong leverage. They can threaten tiering, downgrades or blackouts to extract concessions, and cord-cutting—U.S. pay-TV households down roughly 20% since 2019 through 2024—heightens sensitivity to channel value. AMC must demonstrate audience engagement and measurable ad ROI to sustain per-subscriber rates.

Direct-to-consumer churn sensitivity

AMC Networks faces high DTC churn sensitivity as AMC+, Shudder and Acorn TV subscribers face low switching costs and monthly cancellation options, contributing to an industry average SVOD monthly churn of about 2.6% in 2024. Content drop-offs or price hikes prompt immediate cancellations, while promotional pricing conditions customers to shop for deals. Stabilizing LTV/CAC requires a robust release cadence and bundling across brands to reduce churn and lift retention.

Advertisers’ budget flexibility

Brands reallocate spend across linear, CTV, social and search, increasing price pressure; US CTV ad spend grew roughly 20% YoY to about $21B in 2024, shifting dollars from linear.

Measurement is moving to outcomes and attribution—around 70% of marketers in 2024 prioritized ROI-based metrics—raising demand for better data and targeting.

Economic slowdowns compress CPMs and scatter demand, so AMC must deliver distinctive, addressable audiences to protect yield.

Platform gatekeepers’ influence

Platform gatekeepers — app stores and CTV marketplaces like Apple, Google and Roku — control discovery and billing, with App Store commissions of 15–30% (2024 rules) and similar take rates on CTV transactions, reducing AMC’s net ARPU; prominence and merchandising on these platforms directly affect subscriber flow. Direct billing via owned apps improves margins but limits reach versus platform distribution.

- Discovery control: Apple/Google/Roku

- Take rates: App Store 15–30% (2024)

- Prominence = subscriber flow

- Owned apps: higher ARPU, lower reach

International distributors’ selectivity

Outside the U.S., international distributors choose among a crowded pool of content suppliers, and with global streaming subscriptions exceeding 1 billion in 2024, competition for shelf space intensified; cultural fit and dubbing/subtitling requirements add negotiation friction, while buyers increasingly demand broader rights at lower per-territory prices, forcing AMC to tailor windows, packaging, and pricing to secure favorable slots.

- High selectivity: many suppliers vs. limited slots

- Localization friction: dubbing/subtitles raise costs and lead times

- Pricing pressure: demand for wider rights at lower per-territory fees

Distributor control >60% boosts leverage; CTV ads surge to $21B

Concentrated distributors control over 60% of multichannel subs and can force tiering/blackouts; US pay-TV households fell ~20% since 2019 (through 2024), increasing leverage. DTC churn ~2.6% monthly (2024) and CTV ad spend rose ~20% YoY to ~$21B, shifting buyer budgets. App stores/CTV marketplaces take 15–30% (2024), compressing ARPU; global streaming >1B subs intensifies licensing pressure.

| Metric | 2024 Value |

|---|---|

| Distributor share | >60% |

| Pay-TV decline since 2019 | ~20% |

| SVOD monthly churn | ~2.6% |

| CTV ad spend | ~$21B (+20% YoY) |

| App store take rates | 15–30% |

| Global streaming subs | >1B |

What You See Is What You Get

AMC Networks Porter's Five Forces Analysis

This preview shows the AMC Networks Porter's Five Forces analysis exactly as delivered—no placeholders or excerpts. The full, professionally formatted document you see here will be available to download immediately after purchase. Use it as-is for strategic or investment decisions.