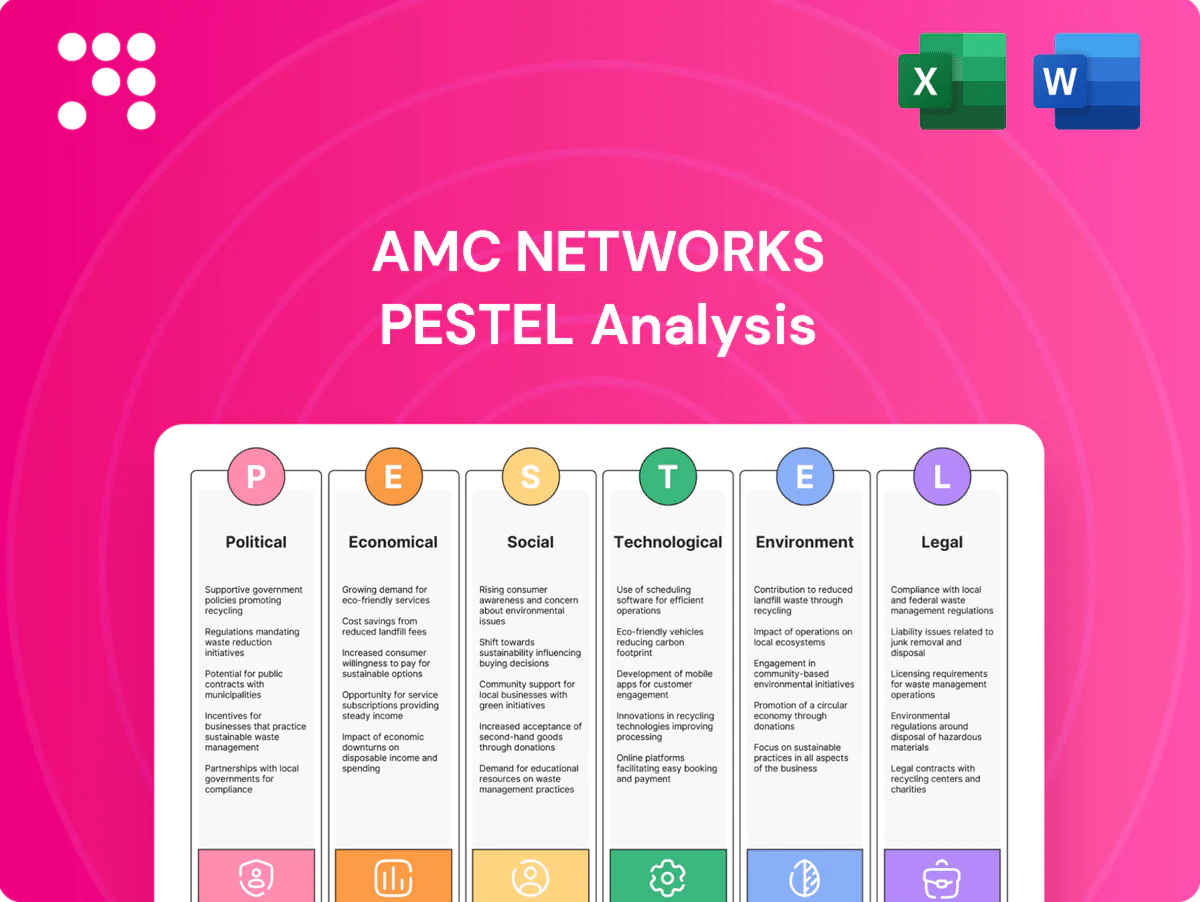

AMC Networks PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of AMC Networks—three to five concise insights into political, economic, social, technological, legal, and environmental trends shaping its future. This ready-to-use report helps investors and strategists forecast risks and spot growth opportunities. Purchase the full, downloadable version now for the complete, editable briefing.

Political factors

Regulatory shifts in media ownership and carriage

Regulatory shifts in FCC and international rules can reshape channel carriage, bundling and distribution fees, squeezing AMC Networks' wholesale pricing and MVPD agreements as U.S. pay-TV subscribers have fallen roughly 40% since 2010. AMC relies on MVPD deals for linear channels and faces political pressure for à la carte mandates that would reduce bundling leverage. Cross-border rules directly affect BBC America, a 50/50 joint venture with BBC Studios, and international distribution economics.

Public funding and partnerships with foreign broadcasters

Content collaborations such as BBC America are sensitive to UK and US public media policies, with funding shifts altering co-production terms; Creative Europe’s 2021–27 budget of €2.44bn and US state film tax credits (up to ~40%) materially affect cost sharing. Political tensions, sanctions or trade disputes can complicate co-productions and licensing across markets. Stable bilateral relations support pipeline diversity and premium content economics for AMC Networks.

Trade policy and content export controls

Tariffs for digital content are minimal, but quotas, censorship and local content rules materially shape availability in key markets; the EU AVMSD requires at least 30% European works in on‑demand catalogs. China blocks many foreign platforms and enforces strict approvals, while India introduced OTT self‑classification rules in 2023. Sanctions and geopolitical frictions, e.g., market exits from Russia in 2022, can disrupt sales, so efficient localization and compliance mitigate revenue volatility.

Tax incentives for film and TV production

State and national production tax credits materially reduce AMC Networks show budgets, with California Film & TV Tax Credit Program 3.0 at roughly 330 million USD annually and New York maintaining a ~420 million USD annual cap, driving shoot location choices. Political cycles can renew, scale back, or eliminate incentives, shifting production hubs and increasing location concentration risk for AMC. Incentive competition between regions affects scheduling and vendor selection, frequently altering timelines and cost structures.

- Impacts: lower production costs, higher ROI

- Risk: political change can reallocate spend

- Operational: location-driven scheduling/vendor shifts

- Exposure: concentration risk in incentive-heavy states

Net neutrality and platform prioritization policies

Net neutrality rule changes can shift bandwidth costs, quality of service and discoverability for AMC+; with video already representing roughly two-thirds of downstream internet traffic per Cisco, ISP prioritization could raise customer acquisition costs or impair streaming performance. Political swings in enforcement increase planning uncertainty, so advocacy and diversified CDN strategies hedge operational risk.

- Impact: higher bandwidth and CDN spend

- Risk: ISP prioritization raises acquisition costs

- Mitigation: advocacy + multi-CDN strategy

Regulatory shifts, tax credits and net neutrality reshape pay‑TV and streaming economics

Regulatory shifts (FCC, AVMSD) and à la carte pressure reduce AMC Networks’ bundling leverage as US pay‑TV subs fell ~40% since 2010. Production tax credits (CA ~$330M cap, NY ~$420M cap) and EU funding (Creative Europe €2.44bn) materially alter costs and shoot locations. Net neutrality and ISP prioritization risk streaming QoS—video ≈66% of downstream traffic per Cisco, raising CDN spend.

| Metric | Value |

|---|---|

| US pay‑TV decline since 2010 | ~40% |

| EU AVMSD quota | ≥30% European works |

| CA Film & TV tax credit | ~$330M |

| NY annual cap | ~$420M |

| Video share of downstream traffic | ~66% |

What is included in the product

Explores how macro-environmental factors — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact AMC Networks, with data-backed trends, forward-looking scenarios, and actionable implications to help executives, investors, and strategists identify opportunities and risks in media and streaming markets.

A concise PESTLE snapshot of AMC Networks that highlights external risks and opportunities, formatted for quick insertion into presentations and team briefs; editable notes allow regional or business-line customization for faster decision-making.

Economic factors

Cord-cutting and pay-TV affiliate revenue pressure

Accelerating cord-cutting has roughly halved U.S. pay-TV penetration since 2010, compressing AMC Networks’ affiliate and advertising revenue as linear subscribers decline. AMC leans on AMC+ and niche streamers to recover revenue, but streaming ARPU is typically lower and churn higher than legacy cable. Partial rebundling via vMVPDs (Hulu Live, YouTube TV) cushions losses. Rigorous cost discipline and strategic theatrical/streaming windowing are critical to margin stability.

Advertising market cyclicality

US national ad spend, tied to GDP and rates, dipped in 2023 then was projected to rebound ~3% to about $304B in 2024 (eMarketer); genre mix matters—premium drama and true crime typically command 15–30% higher CPMs than lifestyle, boosting resilience; addressable and streaming ad tiers now capture roughly 40% of digital video ad dollars, and 2024 political cycles drove an estimated $9–11B episodic boost to certain channels.

Content cost inflation and ROI discipline

Labor-driven cost inflation since the 2023 WGA/SAG-AFTRA strikes and rising talent, production and marketing fees—with prestige drama often costing roughly 5–10 million per episode—have tightened AMC’s greenlight discipline; AMC’s premium brands (AMC, Shudder, IFC, Sundance Now) force careful slate curation to avoid overspend vs mass-market streamers, while co-productions and library exploitation boost ROI and FX volatility pressures international production budgets.

Subscriber acquisition cost and churn economics

Competitive SVOD dynamics have driven higher subscriber acquisition cost and heavier promotional intensity, while niche brands like Shudder, Acorn TV and ALLBLK lower CAC by targeting passionate communities but limit total addressable market. Bundling AMC+ with partners reduces churn risk, and data-driven retention plus strategic windowing smooths lifetime value.

- Competitive SVOD: higher CAC, more promos

- Niche brands: lower CAC, capped TAM

- Bundling: lowers churn

- Data/windowing: stabilizes LTV

Interest rates, leverage, and cash flow

Higher interest rates (federal funds 5.25–5.50% in 2024–2025) raise AMC Networks’ debt service costs and compress media valuation multiples, pressuring P/E and EV/EBITDA benchmarks; stable library licensing provides recurring cash that supports liquidity and debt coverage. Timing of working-capital around series launches can swing quarterly cash flow, while asset sales or JVs remain tools to optimize capital allocation and reduce leverage.

- Interest-rate backdrop: federal funds 5.25–5.50% (2024–2025)

- Library licensing: steady recurring cash supports liquidity

- Working-capital: series launches cause quarter-to-quarter swings

- Capital actions: asset sales/JVs to lower leverage and reallocate capital

Regulatory shifts, tax credits and net neutrality reshape pay‑TV and streaming economics

Cord-cutting halved US pay-TV since 2010, squeezing affiliate and linear ad revenue and forcing AMC toward lower-ARPU streaming and rebundling via vMVPDs. US ad spend ~ $304B in 2024 with streaming/ addressable now ~40% of digital video ads; premium drama commands $5–10M per episode, tightening greenlight discipline. Fed funds 5.25–5.50% (2024–25) raises debt service and compresses media multiples.

| Metric | Value (2024/25) |

|---|---|

| US ad spend | $304B (2024) |

| Streaming ad share | ~40% |

| Drama cost | $5–10M/ep |

| Fed funds | 5.25–5.50% |

What You See Is What You Get

AMC Networks PESTLE Analysis

The AMC Networks PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains all political, economic, social, technological, legal, and environmental insights as displayed, with no placeholders or edits pending.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of AMC Networks—three to five concise insights into political, economic, social, technological, legal, and environmental trends shaping its future. This ready-to-use report helps investors and strategists forecast risks and spot growth opportunities. Purchase the full, downloadable version now for the complete, editable briefing.

Political factors

Regulatory shifts in media ownership and carriage

Regulatory shifts in FCC and international rules can reshape channel carriage, bundling and distribution fees, squeezing AMC Networks' wholesale pricing and MVPD agreements as U.S. pay-TV subscribers have fallen roughly 40% since 2010. AMC relies on MVPD deals for linear channels and faces political pressure for à la carte mandates that would reduce bundling leverage. Cross-border rules directly affect BBC America, a 50/50 joint venture with BBC Studios, and international distribution economics.

Public funding and partnerships with foreign broadcasters

Content collaborations such as BBC America are sensitive to UK and US public media policies, with funding shifts altering co-production terms; Creative Europe’s 2021–27 budget of €2.44bn and US state film tax credits (up to ~40%) materially affect cost sharing. Political tensions, sanctions or trade disputes can complicate co-productions and licensing across markets. Stable bilateral relations support pipeline diversity and premium content economics for AMC Networks.

Trade policy and content export controls

Tariffs for digital content are minimal, but quotas, censorship and local content rules materially shape availability in key markets; the EU AVMSD requires at least 30% European works in on‑demand catalogs. China blocks many foreign platforms and enforces strict approvals, while India introduced OTT self‑classification rules in 2023. Sanctions and geopolitical frictions, e.g., market exits from Russia in 2022, can disrupt sales, so efficient localization and compliance mitigate revenue volatility.

Tax incentives for film and TV production

State and national production tax credits materially reduce AMC Networks show budgets, with California Film & TV Tax Credit Program 3.0 at roughly 330 million USD annually and New York maintaining a ~420 million USD annual cap, driving shoot location choices. Political cycles can renew, scale back, or eliminate incentives, shifting production hubs and increasing location concentration risk for AMC. Incentive competition between regions affects scheduling and vendor selection, frequently altering timelines and cost structures.

- Impacts: lower production costs, higher ROI

- Risk: political change can reallocate spend

- Operational: location-driven scheduling/vendor shifts

- Exposure: concentration risk in incentive-heavy states

Net neutrality and platform prioritization policies

Net neutrality rule changes can shift bandwidth costs, quality of service and discoverability for AMC+; with video already representing roughly two-thirds of downstream internet traffic per Cisco, ISP prioritization could raise customer acquisition costs or impair streaming performance. Political swings in enforcement increase planning uncertainty, so advocacy and diversified CDN strategies hedge operational risk.

- Impact: higher bandwidth and CDN spend

- Risk: ISP prioritization raises acquisition costs

- Mitigation: advocacy + multi-CDN strategy

Regulatory shifts, tax credits and net neutrality reshape pay‑TV and streaming economics

Regulatory shifts (FCC, AVMSD) and à la carte pressure reduce AMC Networks’ bundling leverage as US pay‑TV subs fell ~40% since 2010. Production tax credits (CA ~$330M cap, NY ~$420M cap) and EU funding (Creative Europe €2.44bn) materially alter costs and shoot locations. Net neutrality and ISP prioritization risk streaming QoS—video ≈66% of downstream traffic per Cisco, raising CDN spend.

| Metric | Value |

|---|---|

| US pay‑TV decline since 2010 | ~40% |

| EU AVMSD quota | ≥30% European works |

| CA Film & TV tax credit | ~$330M |

| NY annual cap | ~$420M |

| Video share of downstream traffic | ~66% |

What is included in the product

Explores how macro-environmental factors — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact AMC Networks, with data-backed trends, forward-looking scenarios, and actionable implications to help executives, investors, and strategists identify opportunities and risks in media and streaming markets.

A concise PESTLE snapshot of AMC Networks that highlights external risks and opportunities, formatted for quick insertion into presentations and team briefs; editable notes allow regional or business-line customization for faster decision-making.

Economic factors

Cord-cutting and pay-TV affiliate revenue pressure

Accelerating cord-cutting has roughly halved U.S. pay-TV penetration since 2010, compressing AMC Networks’ affiliate and advertising revenue as linear subscribers decline. AMC leans on AMC+ and niche streamers to recover revenue, but streaming ARPU is typically lower and churn higher than legacy cable. Partial rebundling via vMVPDs (Hulu Live, YouTube TV) cushions losses. Rigorous cost discipline and strategic theatrical/streaming windowing are critical to margin stability.

Advertising market cyclicality

US national ad spend, tied to GDP and rates, dipped in 2023 then was projected to rebound ~3% to about $304B in 2024 (eMarketer); genre mix matters—premium drama and true crime typically command 15–30% higher CPMs than lifestyle, boosting resilience; addressable and streaming ad tiers now capture roughly 40% of digital video ad dollars, and 2024 political cycles drove an estimated $9–11B episodic boost to certain channels.

Content cost inflation and ROI discipline

Labor-driven cost inflation since the 2023 WGA/SAG-AFTRA strikes and rising talent, production and marketing fees—with prestige drama often costing roughly 5–10 million per episode—have tightened AMC’s greenlight discipline; AMC’s premium brands (AMC, Shudder, IFC, Sundance Now) force careful slate curation to avoid overspend vs mass-market streamers, while co-productions and library exploitation boost ROI and FX volatility pressures international production budgets.

Subscriber acquisition cost and churn economics

Competitive SVOD dynamics have driven higher subscriber acquisition cost and heavier promotional intensity, while niche brands like Shudder, Acorn TV and ALLBLK lower CAC by targeting passionate communities but limit total addressable market. Bundling AMC+ with partners reduces churn risk, and data-driven retention plus strategic windowing smooths lifetime value.

- Competitive SVOD: higher CAC, more promos

- Niche brands: lower CAC, capped TAM

- Bundling: lowers churn

- Data/windowing: stabilizes LTV

Interest rates, leverage, and cash flow

Higher interest rates (federal funds 5.25–5.50% in 2024–2025) raise AMC Networks’ debt service costs and compress media valuation multiples, pressuring P/E and EV/EBITDA benchmarks; stable library licensing provides recurring cash that supports liquidity and debt coverage. Timing of working-capital around series launches can swing quarterly cash flow, while asset sales or JVs remain tools to optimize capital allocation and reduce leverage.

- Interest-rate backdrop: federal funds 5.25–5.50% (2024–2025)

- Library licensing: steady recurring cash supports liquidity

- Working-capital: series launches cause quarter-to-quarter swings

- Capital actions: asset sales/JVs to lower leverage and reallocate capital

Regulatory shifts, tax credits and net neutrality reshape pay‑TV and streaming economics

Cord-cutting halved US pay-TV since 2010, squeezing affiliate and linear ad revenue and forcing AMC toward lower-ARPU streaming and rebundling via vMVPDs. US ad spend ~ $304B in 2024 with streaming/ addressable now ~40% of digital video ads; premium drama commands $5–10M per episode, tightening greenlight discipline. Fed funds 5.25–5.50% (2024–25) raises debt service and compresses media multiples.

| Metric | Value (2024/25) |

|---|---|

| US ad spend | $304B (2024) |

| Streaming ad share | ~40% |

| Drama cost | $5–10M/ep |

| Fed funds | 5.25–5.50% |

What You See Is What You Get

AMC Networks PESTLE Analysis

The AMC Networks PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains all political, economic, social, technological, legal, and environmental insights as displayed, with no placeholders or edits pending.

Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of AMC Networks—three to five concise insights into political, economic, social, technological, legal, and environmental trends shaping its future. This ready-to-use report helps investors and strategists forecast risks and spot growth opportunities. Purchase the full, downloadable version now for the complete, editable briefing.

Political factors

Regulatory shifts in media ownership and carriage

Regulatory shifts in FCC and international rules can reshape channel carriage, bundling and distribution fees, squeezing AMC Networks' wholesale pricing and MVPD agreements as U.S. pay-TV subscribers have fallen roughly 40% since 2010. AMC relies on MVPD deals for linear channels and faces political pressure for à la carte mandates that would reduce bundling leverage. Cross-border rules directly affect BBC America, a 50/50 joint venture with BBC Studios, and international distribution economics.

Public funding and partnerships with foreign broadcasters

Content collaborations such as BBC America are sensitive to UK and US public media policies, with funding shifts altering co-production terms; Creative Europe’s 2021–27 budget of €2.44bn and US state film tax credits (up to ~40%) materially affect cost sharing. Political tensions, sanctions or trade disputes can complicate co-productions and licensing across markets. Stable bilateral relations support pipeline diversity and premium content economics for AMC Networks.

Trade policy and content export controls

Tariffs for digital content are minimal, but quotas, censorship and local content rules materially shape availability in key markets; the EU AVMSD requires at least 30% European works in on‑demand catalogs. China blocks many foreign platforms and enforces strict approvals, while India introduced OTT self‑classification rules in 2023. Sanctions and geopolitical frictions, e.g., market exits from Russia in 2022, can disrupt sales, so efficient localization and compliance mitigate revenue volatility.

Tax incentives for film and TV production

State and national production tax credits materially reduce AMC Networks show budgets, with California Film & TV Tax Credit Program 3.0 at roughly 330 million USD annually and New York maintaining a ~420 million USD annual cap, driving shoot location choices. Political cycles can renew, scale back, or eliminate incentives, shifting production hubs and increasing location concentration risk for AMC. Incentive competition between regions affects scheduling and vendor selection, frequently altering timelines and cost structures.

- Impacts: lower production costs, higher ROI

- Risk: political change can reallocate spend

- Operational: location-driven scheduling/vendor shifts

- Exposure: concentration risk in incentive-heavy states

Net neutrality and platform prioritization policies

Net neutrality rule changes can shift bandwidth costs, quality of service and discoverability for AMC+; with video already representing roughly two-thirds of downstream internet traffic per Cisco, ISP prioritization could raise customer acquisition costs or impair streaming performance. Political swings in enforcement increase planning uncertainty, so advocacy and diversified CDN strategies hedge operational risk.

- Impact: higher bandwidth and CDN spend

- Risk: ISP prioritization raises acquisition costs

- Mitigation: advocacy + multi-CDN strategy

Regulatory shifts, tax credits and net neutrality reshape pay‑TV and streaming economics

Regulatory shifts (FCC, AVMSD) and à la carte pressure reduce AMC Networks’ bundling leverage as US pay‑TV subs fell ~40% since 2010. Production tax credits (CA ~$330M cap, NY ~$420M cap) and EU funding (Creative Europe €2.44bn) materially alter costs and shoot locations. Net neutrality and ISP prioritization risk streaming QoS—video ≈66% of downstream traffic per Cisco, raising CDN spend.

| Metric | Value |

|---|---|

| US pay‑TV decline since 2010 | ~40% |

| EU AVMSD quota | ≥30% European works |

| CA Film & TV tax credit | ~$330M |

| NY annual cap | ~$420M |

| Video share of downstream traffic | ~66% |

What is included in the product

Explores how macro-environmental factors — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact AMC Networks, with data-backed trends, forward-looking scenarios, and actionable implications to help executives, investors, and strategists identify opportunities and risks in media and streaming markets.

A concise PESTLE snapshot of AMC Networks that highlights external risks and opportunities, formatted for quick insertion into presentations and team briefs; editable notes allow regional or business-line customization for faster decision-making.

Economic factors

Cord-cutting and pay-TV affiliate revenue pressure

Accelerating cord-cutting has roughly halved U.S. pay-TV penetration since 2010, compressing AMC Networks’ affiliate and advertising revenue as linear subscribers decline. AMC leans on AMC+ and niche streamers to recover revenue, but streaming ARPU is typically lower and churn higher than legacy cable. Partial rebundling via vMVPDs (Hulu Live, YouTube TV) cushions losses. Rigorous cost discipline and strategic theatrical/streaming windowing are critical to margin stability.

Advertising market cyclicality

US national ad spend, tied to GDP and rates, dipped in 2023 then was projected to rebound ~3% to about $304B in 2024 (eMarketer); genre mix matters—premium drama and true crime typically command 15–30% higher CPMs than lifestyle, boosting resilience; addressable and streaming ad tiers now capture roughly 40% of digital video ad dollars, and 2024 political cycles drove an estimated $9–11B episodic boost to certain channels.

Content cost inflation and ROI discipline

Labor-driven cost inflation since the 2023 WGA/SAG-AFTRA strikes and rising talent, production and marketing fees—with prestige drama often costing roughly 5–10 million per episode—have tightened AMC’s greenlight discipline; AMC’s premium brands (AMC, Shudder, IFC, Sundance Now) force careful slate curation to avoid overspend vs mass-market streamers, while co-productions and library exploitation boost ROI and FX volatility pressures international production budgets.

Subscriber acquisition cost and churn economics

Competitive SVOD dynamics have driven higher subscriber acquisition cost and heavier promotional intensity, while niche brands like Shudder, Acorn TV and ALLBLK lower CAC by targeting passionate communities but limit total addressable market. Bundling AMC+ with partners reduces churn risk, and data-driven retention plus strategic windowing smooths lifetime value.

- Competitive SVOD: higher CAC, more promos

- Niche brands: lower CAC, capped TAM

- Bundling: lowers churn

- Data/windowing: stabilizes LTV

Interest rates, leverage, and cash flow

Higher interest rates (federal funds 5.25–5.50% in 2024–2025) raise AMC Networks’ debt service costs and compress media valuation multiples, pressuring P/E and EV/EBITDA benchmarks; stable library licensing provides recurring cash that supports liquidity and debt coverage. Timing of working-capital around series launches can swing quarterly cash flow, while asset sales or JVs remain tools to optimize capital allocation and reduce leverage.

- Interest-rate backdrop: federal funds 5.25–5.50% (2024–2025)

- Library licensing: steady recurring cash supports liquidity

- Working-capital: series launches cause quarter-to-quarter swings

- Capital actions: asset sales/JVs to lower leverage and reallocate capital

Regulatory shifts, tax credits and net neutrality reshape pay‑TV and streaming economics

Cord-cutting halved US pay-TV since 2010, squeezing affiliate and linear ad revenue and forcing AMC toward lower-ARPU streaming and rebundling via vMVPDs. US ad spend ~ $304B in 2024 with streaming/ addressable now ~40% of digital video ads; premium drama commands $5–10M per episode, tightening greenlight discipline. Fed funds 5.25–5.50% (2024–25) raises debt service and compresses media multiples.

| Metric | Value (2024/25) |

|---|---|

| US ad spend | $304B (2024) |

| Streaming ad share | ~40% |

| Drama cost | $5–10M/ep |

| Fed funds | 5.25–5.50% |

What You See Is What You Get

AMC Networks PESTLE Analysis

The AMC Networks PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains all political, economic, social, technological, legal, and environmental insights as displayed, with no placeholders or edits pending.