AMCON Distributing PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

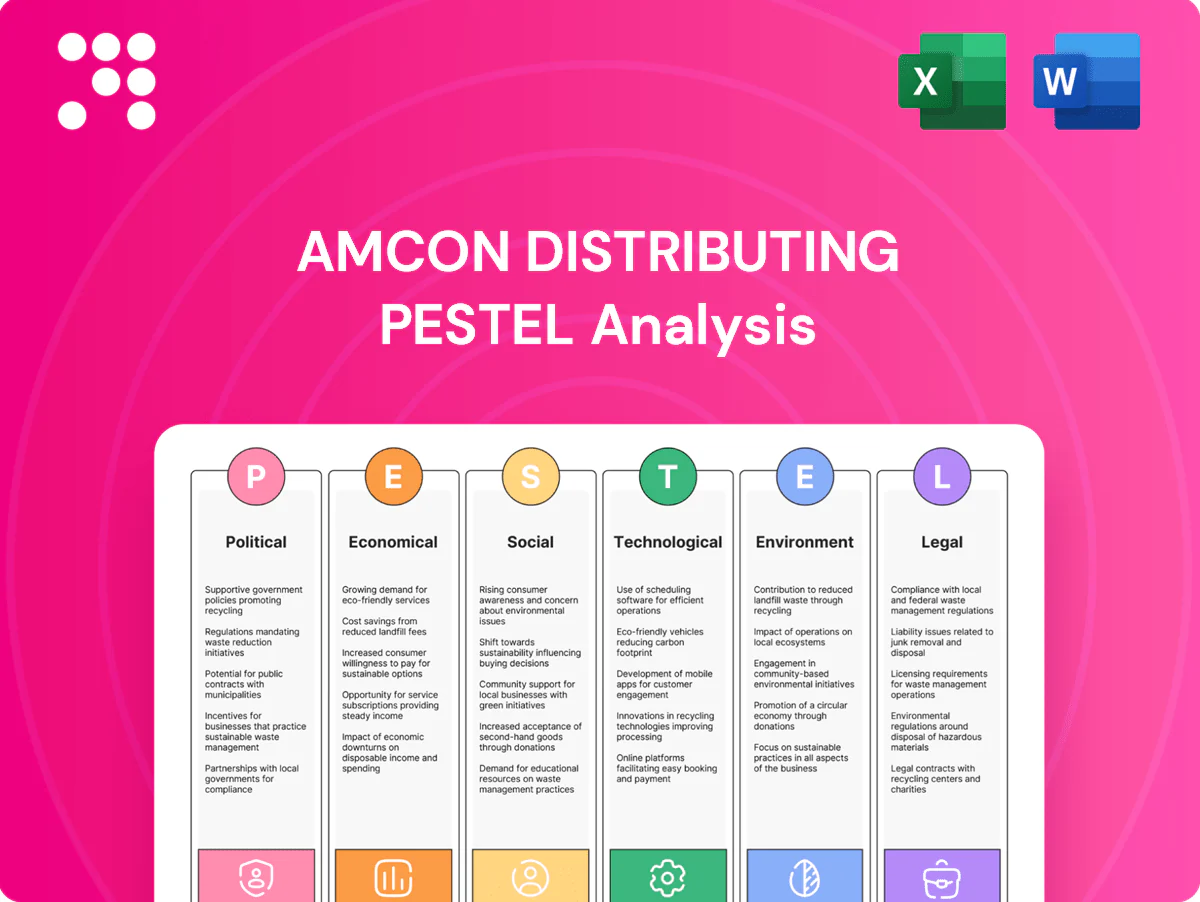

Unlock strategic clarity with our PESTLE Analysis tailored to AMCON Distributing—three to five critical perspectives on political, economic, social, technological, legal, and environmental forces shaping its future. Perfect for investors and planners, this concise briefing highlights risks and opportunities you can act on today. Purchase the full report for the complete, editable breakdown and immediate download.

Political factors

Tobacco excise and sin tax policy

Frequent federal and state excise changes materially affect AMCON: federal cigarette tax remains $1.01/pack (2024) and state taxes average about $1.91/pack, combining to roughly $2.92/pack, forcing rapid repricing to stay compliant. Higher taxes compress margins, typically reduce volumes (price elasticity ~-0.4 to -0.6) and shift sales toward value brands. Election cycles increase political appetite for sin tax hikes, raising regulatory and pricing volatility.

Flavor and menthol bans momentum

State and municipal flavored tobacco bans and the FDA's proposed menthol product standard (announced April 2022, rulemaking active through 2025) threaten to compress AMCON's high-margin flavored/menthol SKUs. Policy heterogeneity across jurisdictions complicates inventory, routing and requires SKU diversification and jurisdiction-specific contingency plans. Retailer education and substitution strategies will be critical to preserve margins and shelf turnover.

Minimum wage and labor policy direction

Federal minimum wage remains $7.25 hourly, while roughly 30 states and DC set higher rates (many now at or near $15–16/hr in hubs like CA and NY), raising distribution center and driver labor costs. The DOL overtime salary threshold rose to about $43,888/year, tightening staffing models and scheduling. Political focus on worker protections increases compliance overhead and firms must push pricing and productivity gains to offset wage inflation.

Trade and tariff dynamics

Tariffs on imported candies, beverages and packaging lift input costs and, per WTO data, global average applied MFN tariffs sat near 3%–4% in 2023, with specific confectionery lines facing higher duty bands; port slowdowns from geopolitical tensions have cut fill rates by double-digit percentages in acute episodes. AMCON mitigates via supplier diversification and industry advocacy to anticipate policy shifts and preserve margins.

- Tariff exposure: confectionery/packaging duty bands often exceed average MFN rates

- Supply risk: port disruptions can reduce fill rates by 10%+ in spikes

- Mitigation: diversified suppliers cushion shocks

- Advocacy: trade groups improve policy visibility

Cannabis and nicotine product policy

Legalization trends for cannabis and tighter regulation on nicotine alternatives create mixed-category risk and opportunity; 24 states permit adult-use cannabis and 38 allow medical use, forcing tailored compliance and channel strategies.

Political outcomes shape distribution rights and retailer demand, and AMCON can pilot adjacent product logistics where legally permitted.

- State-by-state compliance

- Pilot adjacent-product logistics

Tax hikes and regs reduce volumes; margins hit $2.92/pack

Frequent federal/state excise hikes (federal $1.01/pack 2024; state avg $1.91) compress margins and reduce volumes (elasticity ~-0.5); election cycles increase tax risk. Flavor/menthol regs (FDA rulemaking through 2025) and state bans threaten premium SKUs. Rising state wages (~30 states near $15–16) increase distribution labor costs; tariffs/port disruptions add input volatility.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Excise tax | $2.92/pack total | Margin pressure |

| Elasticity | -0.4 to -0.6 | Volume decline |

| Wages | ~30 states $15–16 | Higher Opex |

What is included in the product

Explores how macro-environmental forces uniquely affect AMCON Distributing across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region/industry specificity to identify risks and opportunities. Designed for executives, investors, and strategists, each section offers forward-looking analysis ready for business plans and scenario planning.

A concise, visually segmented PESTLE summary for AMCON Distributing that’s easily dropped into presentations, shared across teams, and customized with notes to support quick alignment and external risk discussions during planning.

Economic factors

Consumer disposable income swings

Macro cycles drive basket size in convenience retail: when U.S. CPI slowed to about 3.4% in 2024 and average hourly earnings rose roughly 4.1% y/y (BLS), discretionary lift in beverages and candy was observed, while downturns push consumers to value tobacco, private labels and smaller pack sizes; AMCON’s broad assortment and SKU depth help smooth sales volatility and margin pressure across these income-driven shifts.

Fuel costs and freight inflation

Diesel price spikes—U.S. on‑road diesel averaged about $3.80/gal in H1 2025 per EIA—flow directly into AMCON route economics and require higher delivery fees. Tight trucking capacity pushed spot truckload rates roughly 10–15% above 2023 levels (DAT/ACT), raising third‑party and driver retention costs. Network optimization and fuel hedging programs reduce volatility, but freight surcharges may be necessary to preserve margins.

Supplier pricing and rebate structures

CPG and tobacco manufacturers raised list prices and incentive floors 3–7% in 2023–24 to offset inflation; CPI averaged about 3.4% in 2024. Rebate tiers and promotional funding—often 4–8% of distributor revenue—materially drive AMCON’s gross profit and working capital. Economic pressure can cut vendor support, compressing margins 100–300 bps, while data-driven SKU mix and promotion optimization can recapture 150–250 bps.

Interest rates and working capital

Higher policy rates (Fed funds ~5.25–5.50% in July 2025) elevate inventory financing costs in AMCON’s high-throughput, low-margin model; a 100bp rise adds $1.0m p.a. interest on $100m inventory. Tighter liquidity makes retailer credit terms critical, forcing trade-off between service levels and days inventory outstanding; cash discipline and dynamic pricing protect returns.

- Inventory financing sensitivity: +100bp = +$1m per $100m

- Focus: reduce DIO to preserve margins

- Negotiate stricter retailer terms

- Use dynamic pricing to defend cash returns

Labor market tightness

Competition for warehouse and CDL talent raises wage pressure and turnover; the commercial driver shortage was estimated at about 80,000 drivers (American Trucking Associations, 2022) and wage growth in logistics accelerated into 2024, squeezing margins. Investment in training and automation boosts productivity per labor hour and can cut costs over time, while economic slack eases hiring but may lower average skill levels and service quality risks; retention programs reduce recruitment spend long-term.

- Driver shortage: ~80,000 (ATA 2022)

- Wage inflation in logistics: up into 2024

- Training/automation: raises output per labor hour

- Retention: lowers recurring recruitment costs

Tax hikes and regs reduce volumes; margins hit $2.92/pack

Macro cycles shift basket size: 2024 CPI ~3.4% and avg hourly earnings +4.1% (BLS) lifted discretionary SKUs; downturns favor value tobacco and private labels, smoothing via AMCON’s SKU depth.

Diesel averaged ~$3.80/gal H1 2025 (EIA); spot truck rates +10–15% vs 2023, pressuring delivery costs and margins.

Fed funds ~5.25–5.50% Jul 2025 raises inventory finance; +100bp ≈ +$1m p.a. per $100m inventory.

| Metric | Value |

|---|---|

| 2024 CPI | 3.4% |

| Avg hourly | +4.1% y/y |

| Diesel H1 2025 | $3.80/gal |

| Fed funds Jul 2025 | 5.25–5.50% |

What You See Is What You Get

AMCON Distributing PESTLE Analysis

This AMCON Distributing PESTLE Analysis preview is the exact file you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are identical to the final document. No placeholders, no teasers—download the same file immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis tailored to AMCON Distributing—three to five critical perspectives on political, economic, social, technological, legal, and environmental forces shaping its future. Perfect for investors and planners, this concise briefing highlights risks and opportunities you can act on today. Purchase the full report for the complete, editable breakdown and immediate download.

Political factors

Tobacco excise and sin tax policy

Frequent federal and state excise changes materially affect AMCON: federal cigarette tax remains $1.01/pack (2024) and state taxes average about $1.91/pack, combining to roughly $2.92/pack, forcing rapid repricing to stay compliant. Higher taxes compress margins, typically reduce volumes (price elasticity ~-0.4 to -0.6) and shift sales toward value brands. Election cycles increase political appetite for sin tax hikes, raising regulatory and pricing volatility.

Flavor and menthol bans momentum

State and municipal flavored tobacco bans and the FDA's proposed menthol product standard (announced April 2022, rulemaking active through 2025) threaten to compress AMCON's high-margin flavored/menthol SKUs. Policy heterogeneity across jurisdictions complicates inventory, routing and requires SKU diversification and jurisdiction-specific contingency plans. Retailer education and substitution strategies will be critical to preserve margins and shelf turnover.

Minimum wage and labor policy direction

Federal minimum wage remains $7.25 hourly, while roughly 30 states and DC set higher rates (many now at or near $15–16/hr in hubs like CA and NY), raising distribution center and driver labor costs. The DOL overtime salary threshold rose to about $43,888/year, tightening staffing models and scheduling. Political focus on worker protections increases compliance overhead and firms must push pricing and productivity gains to offset wage inflation.

Trade and tariff dynamics

Tariffs on imported candies, beverages and packaging lift input costs and, per WTO data, global average applied MFN tariffs sat near 3%–4% in 2023, with specific confectionery lines facing higher duty bands; port slowdowns from geopolitical tensions have cut fill rates by double-digit percentages in acute episodes. AMCON mitigates via supplier diversification and industry advocacy to anticipate policy shifts and preserve margins.

- Tariff exposure: confectionery/packaging duty bands often exceed average MFN rates

- Supply risk: port disruptions can reduce fill rates by 10%+ in spikes

- Mitigation: diversified suppliers cushion shocks

- Advocacy: trade groups improve policy visibility

Cannabis and nicotine product policy

Legalization trends for cannabis and tighter regulation on nicotine alternatives create mixed-category risk and opportunity; 24 states permit adult-use cannabis and 38 allow medical use, forcing tailored compliance and channel strategies.

Political outcomes shape distribution rights and retailer demand, and AMCON can pilot adjacent product logistics where legally permitted.

- State-by-state compliance

- Pilot adjacent-product logistics

Tax hikes and regs reduce volumes; margins hit $2.92/pack

Frequent federal/state excise hikes (federal $1.01/pack 2024; state avg $1.91) compress margins and reduce volumes (elasticity ~-0.5); election cycles increase tax risk. Flavor/menthol regs (FDA rulemaking through 2025) and state bans threaten premium SKUs. Rising state wages (~30 states near $15–16) increase distribution labor costs; tariffs/port disruptions add input volatility.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Excise tax | $2.92/pack total | Margin pressure |

| Elasticity | -0.4 to -0.6 | Volume decline |

| Wages | ~30 states $15–16 | Higher Opex |

What is included in the product

Explores how macro-environmental forces uniquely affect AMCON Distributing across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region/industry specificity to identify risks and opportunities. Designed for executives, investors, and strategists, each section offers forward-looking analysis ready for business plans and scenario planning.

A concise, visually segmented PESTLE summary for AMCON Distributing that’s easily dropped into presentations, shared across teams, and customized with notes to support quick alignment and external risk discussions during planning.

Economic factors

Consumer disposable income swings

Macro cycles drive basket size in convenience retail: when U.S. CPI slowed to about 3.4% in 2024 and average hourly earnings rose roughly 4.1% y/y (BLS), discretionary lift in beverages and candy was observed, while downturns push consumers to value tobacco, private labels and smaller pack sizes; AMCON’s broad assortment and SKU depth help smooth sales volatility and margin pressure across these income-driven shifts.

Fuel costs and freight inflation

Diesel price spikes—U.S. on‑road diesel averaged about $3.80/gal in H1 2025 per EIA—flow directly into AMCON route economics and require higher delivery fees. Tight trucking capacity pushed spot truckload rates roughly 10–15% above 2023 levels (DAT/ACT), raising third‑party and driver retention costs. Network optimization and fuel hedging programs reduce volatility, but freight surcharges may be necessary to preserve margins.

Supplier pricing and rebate structures

CPG and tobacco manufacturers raised list prices and incentive floors 3–7% in 2023–24 to offset inflation; CPI averaged about 3.4% in 2024. Rebate tiers and promotional funding—often 4–8% of distributor revenue—materially drive AMCON’s gross profit and working capital. Economic pressure can cut vendor support, compressing margins 100–300 bps, while data-driven SKU mix and promotion optimization can recapture 150–250 bps.

Interest rates and working capital

Higher policy rates (Fed funds ~5.25–5.50% in July 2025) elevate inventory financing costs in AMCON’s high-throughput, low-margin model; a 100bp rise adds $1.0m p.a. interest on $100m inventory. Tighter liquidity makes retailer credit terms critical, forcing trade-off between service levels and days inventory outstanding; cash discipline and dynamic pricing protect returns.

- Inventory financing sensitivity: +100bp = +$1m per $100m

- Focus: reduce DIO to preserve margins

- Negotiate stricter retailer terms

- Use dynamic pricing to defend cash returns

Labor market tightness

Competition for warehouse and CDL talent raises wage pressure and turnover; the commercial driver shortage was estimated at about 80,000 drivers (American Trucking Associations, 2022) and wage growth in logistics accelerated into 2024, squeezing margins. Investment in training and automation boosts productivity per labor hour and can cut costs over time, while economic slack eases hiring but may lower average skill levels and service quality risks; retention programs reduce recruitment spend long-term.

- Driver shortage: ~80,000 (ATA 2022)

- Wage inflation in logistics: up into 2024

- Training/automation: raises output per labor hour

- Retention: lowers recurring recruitment costs

Tax hikes and regs reduce volumes; margins hit $2.92/pack

Macro cycles shift basket size: 2024 CPI ~3.4% and avg hourly earnings +4.1% (BLS) lifted discretionary SKUs; downturns favor value tobacco and private labels, smoothing via AMCON’s SKU depth.

Diesel averaged ~$3.80/gal H1 2025 (EIA); spot truck rates +10–15% vs 2023, pressuring delivery costs and margins.

Fed funds ~5.25–5.50% Jul 2025 raises inventory finance; +100bp ≈ +$1m p.a. per $100m inventory.

| Metric | Value |

|---|---|

| 2024 CPI | 3.4% |

| Avg hourly | +4.1% y/y |

| Diesel H1 2025 | $3.80/gal |

| Fed funds Jul 2025 | 5.25–5.50% |

What You See Is What You Get

AMCON Distributing PESTLE Analysis

This AMCON Distributing PESTLE Analysis preview is the exact file you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are identical to the final document. No placeholders, no teasers—download the same file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis tailored to AMCON Distributing—three to five critical perspectives on political, economic, social, technological, legal, and environmental forces shaping its future. Perfect for investors and planners, this concise briefing highlights risks and opportunities you can act on today. Purchase the full report for the complete, editable breakdown and immediate download.

Political factors

Tobacco excise and sin tax policy

Frequent federal and state excise changes materially affect AMCON: federal cigarette tax remains $1.01/pack (2024) and state taxes average about $1.91/pack, combining to roughly $2.92/pack, forcing rapid repricing to stay compliant. Higher taxes compress margins, typically reduce volumes (price elasticity ~-0.4 to -0.6) and shift sales toward value brands. Election cycles increase political appetite for sin tax hikes, raising regulatory and pricing volatility.

Flavor and menthol bans momentum

State and municipal flavored tobacco bans and the FDA's proposed menthol product standard (announced April 2022, rulemaking active through 2025) threaten to compress AMCON's high-margin flavored/menthol SKUs. Policy heterogeneity across jurisdictions complicates inventory, routing and requires SKU diversification and jurisdiction-specific contingency plans. Retailer education and substitution strategies will be critical to preserve margins and shelf turnover.

Minimum wage and labor policy direction

Federal minimum wage remains $7.25 hourly, while roughly 30 states and DC set higher rates (many now at or near $15–16/hr in hubs like CA and NY), raising distribution center and driver labor costs. The DOL overtime salary threshold rose to about $43,888/year, tightening staffing models and scheduling. Political focus on worker protections increases compliance overhead and firms must push pricing and productivity gains to offset wage inflation.

Trade and tariff dynamics

Tariffs on imported candies, beverages and packaging lift input costs and, per WTO data, global average applied MFN tariffs sat near 3%–4% in 2023, with specific confectionery lines facing higher duty bands; port slowdowns from geopolitical tensions have cut fill rates by double-digit percentages in acute episodes. AMCON mitigates via supplier diversification and industry advocacy to anticipate policy shifts and preserve margins.

- Tariff exposure: confectionery/packaging duty bands often exceed average MFN rates

- Supply risk: port disruptions can reduce fill rates by 10%+ in spikes

- Mitigation: diversified suppliers cushion shocks

- Advocacy: trade groups improve policy visibility

Cannabis and nicotine product policy

Legalization trends for cannabis and tighter regulation on nicotine alternatives create mixed-category risk and opportunity; 24 states permit adult-use cannabis and 38 allow medical use, forcing tailored compliance and channel strategies.

Political outcomes shape distribution rights and retailer demand, and AMCON can pilot adjacent product logistics where legally permitted.

- State-by-state compliance

- Pilot adjacent-product logistics

Tax hikes and regs reduce volumes; margins hit $2.92/pack

Frequent federal/state excise hikes (federal $1.01/pack 2024; state avg $1.91) compress margins and reduce volumes (elasticity ~-0.5); election cycles increase tax risk. Flavor/menthol regs (FDA rulemaking through 2025) and state bans threaten premium SKUs. Rising state wages (~30 states near $15–16) increase distribution labor costs; tariffs/port disruptions add input volatility.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Excise tax | $2.92/pack total | Margin pressure |

| Elasticity | -0.4 to -0.6 | Volume decline |

| Wages | ~30 states $15–16 | Higher Opex |

What is included in the product

Explores how macro-environmental forces uniquely affect AMCON Distributing across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and region/industry specificity to identify risks and opportunities. Designed for executives, investors, and strategists, each section offers forward-looking analysis ready for business plans and scenario planning.

A concise, visually segmented PESTLE summary for AMCON Distributing that’s easily dropped into presentations, shared across teams, and customized with notes to support quick alignment and external risk discussions during planning.

Economic factors

Consumer disposable income swings

Macro cycles drive basket size in convenience retail: when U.S. CPI slowed to about 3.4% in 2024 and average hourly earnings rose roughly 4.1% y/y (BLS), discretionary lift in beverages and candy was observed, while downturns push consumers to value tobacco, private labels and smaller pack sizes; AMCON’s broad assortment and SKU depth help smooth sales volatility and margin pressure across these income-driven shifts.

Fuel costs and freight inflation

Diesel price spikes—U.S. on‑road diesel averaged about $3.80/gal in H1 2025 per EIA—flow directly into AMCON route economics and require higher delivery fees. Tight trucking capacity pushed spot truckload rates roughly 10–15% above 2023 levels (DAT/ACT), raising third‑party and driver retention costs. Network optimization and fuel hedging programs reduce volatility, but freight surcharges may be necessary to preserve margins.

Supplier pricing and rebate structures

CPG and tobacco manufacturers raised list prices and incentive floors 3–7% in 2023–24 to offset inflation; CPI averaged about 3.4% in 2024. Rebate tiers and promotional funding—often 4–8% of distributor revenue—materially drive AMCON’s gross profit and working capital. Economic pressure can cut vendor support, compressing margins 100–300 bps, while data-driven SKU mix and promotion optimization can recapture 150–250 bps.

Interest rates and working capital

Higher policy rates (Fed funds ~5.25–5.50% in July 2025) elevate inventory financing costs in AMCON’s high-throughput, low-margin model; a 100bp rise adds $1.0m p.a. interest on $100m inventory. Tighter liquidity makes retailer credit terms critical, forcing trade-off between service levels and days inventory outstanding; cash discipline and dynamic pricing protect returns.

- Inventory financing sensitivity: +100bp = +$1m per $100m

- Focus: reduce DIO to preserve margins

- Negotiate stricter retailer terms

- Use dynamic pricing to defend cash returns

Labor market tightness

Competition for warehouse and CDL talent raises wage pressure and turnover; the commercial driver shortage was estimated at about 80,000 drivers (American Trucking Associations, 2022) and wage growth in logistics accelerated into 2024, squeezing margins. Investment in training and automation boosts productivity per labor hour and can cut costs over time, while economic slack eases hiring but may lower average skill levels and service quality risks; retention programs reduce recruitment spend long-term.

- Driver shortage: ~80,000 (ATA 2022)

- Wage inflation in logistics: up into 2024

- Training/automation: raises output per labor hour

- Retention: lowers recurring recruitment costs

Tax hikes and regs reduce volumes; margins hit $2.92/pack

Macro cycles shift basket size: 2024 CPI ~3.4% and avg hourly earnings +4.1% (BLS) lifted discretionary SKUs; downturns favor value tobacco and private labels, smoothing via AMCON’s SKU depth.

Diesel averaged ~$3.80/gal H1 2025 (EIA); spot truck rates +10–15% vs 2023, pressuring delivery costs and margins.

Fed funds ~5.25–5.50% Jul 2025 raises inventory finance; +100bp ≈ +$1m p.a. per $100m inventory.

| Metric | Value |

|---|---|

| 2024 CPI | 3.4% |

| Avg hourly | +4.1% y/y |

| Diesel H1 2025 | $3.80/gal |

| Fed funds Jul 2025 | 5.25–5.50% |

What You See Is What You Get

AMCON Distributing PESTLE Analysis

This AMCON Distributing PESTLE Analysis preview is the exact file you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure shown are identical to the final document. No placeholders, no teasers—download the same file immediately after checkout.