Air Maintenance Estonia AS Porter's Five Forces Analysis

From Overview to Strategy Blueprint

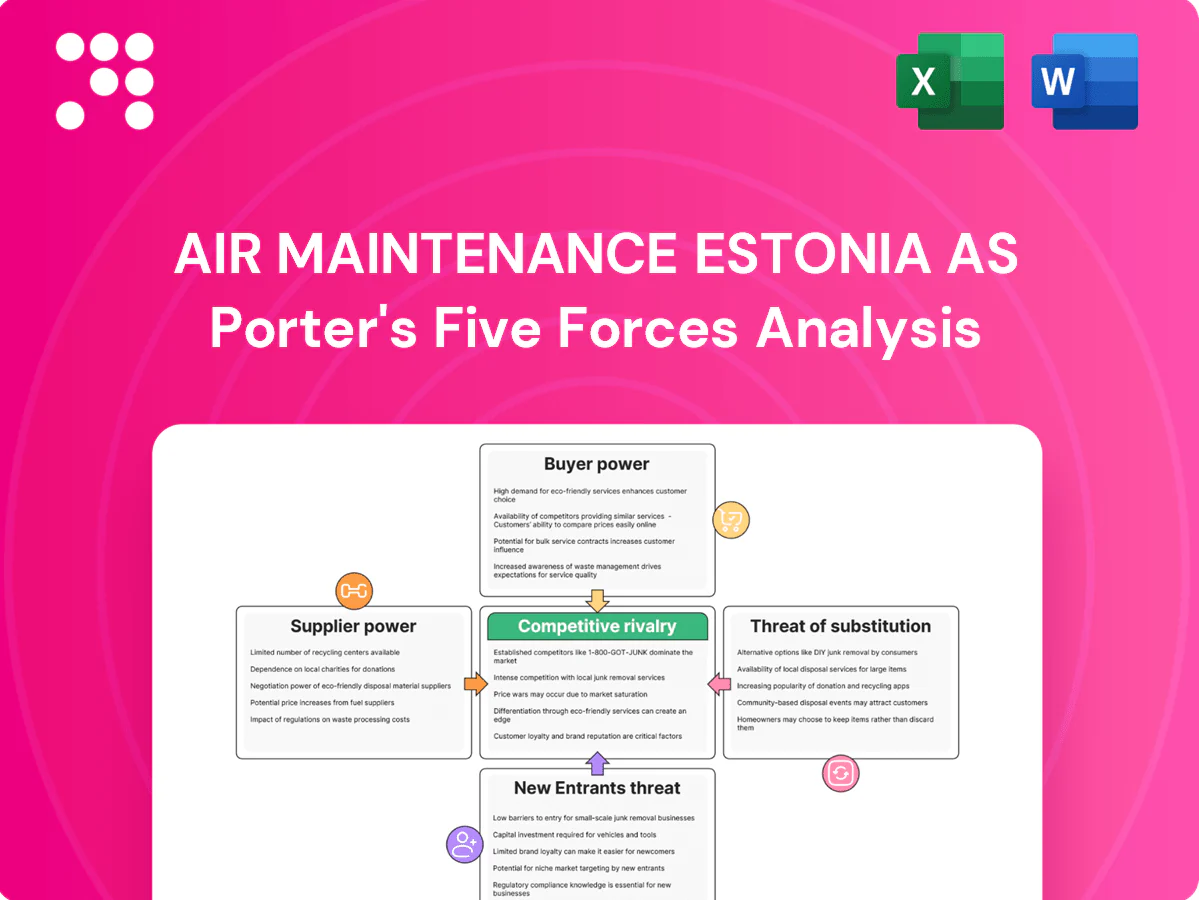

Air Maintenance Estonia AS faces moderate supplier leverage and niche customer demands, balanced by regulatory barriers and moderate threat of entrants in MRO services. Competitive rivalry hinges on technical expertise and turn-time advantages, while substitutes remain limited for certified maintenance. This snapshot highlights key pressures and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

OEM control of parts and manuals

OEMs tightly control proprietary parts, repair data and tooling approvals, giving them strong pricing power and direct control over aftermarket access in 2024. Air Maintenance Estonia requires current manuals and licences to maintain Boeing 737 and Airbus A320 families, which together comprise roughly two-thirds of the global narrowbody fleet. Limited alternative sources for critical components constrain AME’s negotiation leverage, lengthening lead times and elevating input costs.

Engine and component shop dependencies

Specialized engine/APU and module overhauls are concentrated in a handful of certified shops (notably CFM and Pratt & Whitney authorized facilities), limiting Air Maintenance Estonia’s supplier options and raising switching costs. AOG incidents in 2024 amplify supplier leverage as emergency slots command premiums and prioritize OEM-affiliated shops. Scarce overhaul slots constrain AME’s ability to meet TAT commitments to customers, increasing service risk and cost exposure.

Approved distributor and logistics networks

Approved distributors for rotables and logistics providers directly shape cost and availability, with AOG expedited shipping premiums commonly reaching up to 25% in 2024; Estonian operations benefit from EU single-market movement but rely on EU-wide logistics to maintain 2–4 day transit to major hubs. Freight volatility and fuel-linked surcharges remain material, while non-EU parts face customs processing that can add 24–72 hours and extra fees, allowing suppliers to charge for speed and certainty.

Tooling, calibration, and software licensing

Recurring costs for calibrated tooling, test equipment and the maintenance software stack materially impact Air Maintenance Estonia; the global aircraft MRO market was about 89 billion USD in 2024 and digital MRO subscriptions grew ~12% YoY, strengthening supplier pricing power. Vendor lock-in around digital maintenance platforms and data subscriptions raises switching costs and dependency. Compliance-driven calibration intervals and software updates are mandatory; lapses risk audit findings and operational delays.

- Calibration & tooling: recurring CAPEX/OPEX concentration

- Software/data: rising subscription spend, vendor lock-in

- Compliance risk: missed calibrations → audit findings/downtime

Skilled labor and subcontractors

Licensed B1/B2 technicians and niche subcontractors remain scarce across Europe, with EASA in 2024 noting persistent skills shortages that elevate their bargaining power; wage inflation and increased mobility further strengthen leverage. AME must offer competitive pay, clear career progression and in-house training to retain staff, otherwise staffing gaps force reliance on premium-priced subcontracting.

- Licensed B1/B2 scarcity — raises supplier leverage

- Wage inflation & mobility — increase compensation pressure

- Training & pay essential — reduces turnover

- Staff gaps → costly subcontract premiums

OEM parts & scarce shop capacity drive supplier pricing power in 89bn 2024 MRO market

OEM control of parts/tooling and limited certified overhaul shops give suppliers strong pricing power; 2024 MRO market ~89bn USD, AOG premiums up to 25% and overhaul slots scarce. Logistics: 2–4 day EU transit, non-EU customs add 24–72h. Skilled B1/B2 scarcity (EASA 2024) raises labor costs and subcontract reliance.

| Factor | 2024 metric | Impact |

|---|---|---|

| Market size | 89bn USD | Supplier leverage |

| AOG premium | up to 25% | Higher emergency costs |

| Transit/customs | 2–4d / 24–72h | Availability delays |

What is included in the product

Concise Porter's Five Forces assessment for Air Maintenance Estonia AS, outlining competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to clarify pricing pressure, profitability levers, and strategic vulnerabilities.

A concise one-sheet Porter's Five Forces for Air Maintenance Estonia AS—visual spider chart and editable pressure sliders to instantly reveal competitive pain points and strategy gaps, ready to drop into pitch decks or integrate with your Excel dashboards.

Customers Bargaining Power

Airlines and lessors concentrate demand

Airline groups and top lessors concentrate buying power—top 10 lessors control roughly 50% of the leased fleet and airlines accounted for the bulk of the ~90 billion USD global commercial MRO spend in 2023. They benchmark MROs aggressively on price, turnaround time and on-wing reliability across competitive panels. Volume commitments unlock tiered discounts that compress supplier margins. AME must therefore differentiate on lower unit cost, higher quality and strict schedule adherence to retain contracts.

Price sensitivity and cyclical budgets

Operators increasingly scrutinize maintenance costs amid cyclical budgets and 2024 fuel and demand volatility, driving tougher price talks with AME. Heavy check deferrals within regulatory limits amplify leverage, concentrating spend into fewer, high-stakes events and intensifying negotiations. Buyers demand PBH/hourly contracts and fixed TAT penalties, pressuring margins. AME must offer flexible pricing and value-added options to protect profitability.

Moderate switching costs within EASA network

Within the EASA-regulated market covering the EU27, buyers can shift work between certified MROs with relative ease, though onboarding new providers incurs induction, ferry and learning-curve costs; multiyear frame agreements commonly spanning 3–5 years partially lock in scopes, and delivering superior first-time quality materially reduces churn risk.

Demand for bundled services (CAMO + MRO)

Customers increasingly prefer integrated CAMO plus MRO to simplify oversight and comply with EASA Part-CAMO requirements; bundling lowers buyer search and coordination costs, though many still unbundle services periodically to price-check, keeping bargaining power moderate. End-to-end packages enhance AME’s client stickiness, while contract renewals remain tightly tied to measurable performance KPIs.

- Integrated CAMO+MRO reduces admin burden

- Bundling lowers search/coordination costs

- Buyers unbundle to benchmark pricing

- Renewals driven by KPI performance

Seasonality and slot leverage

Peak seasons let buyers who pre-book slots up to 12 months ahead secure better terms, while off-peak capacity pressures MROs to discount—industry reports show utilization swings driving price concessions around 10–15% in low months. Airlines with flexible schedules arbitrage timing, and AME’s slot management directly shifts its pricing power and margin capture.

- Pre-booking: up to 12 months

- Price concessions: ~10–15% off-peak

- Utilization swings: seasonal

- AME slot control: key to margins

Buyers have high leverage: top-10 lessors ~50%; global MRO ~90B USD

Buyers hold moderate-to-high bargaining power: top 10 lessors control ~50% of the leased fleet and global commercial MRO spend was ~90 billion USD in 2023, driving aggressive price/turnaround benchmarking. Volume commitments and PBH contracts compress margins; off-peak pricing concessions run ~10–15% while pre-booking up to 12 months secures better terms. Bundled CAMO+MRO raises stickiness but renewals hinge on KPI performance.

| Metric | Value |

|---|---|

| Top-10 lessors share | ~50% |

| Global MRO spend (2023) | ~90 B USD |

| Pre-booking | Up to 12 months |

| Off-peak concessions | ~10–15% |

Preview Before You Purchase

Air Maintenance Estonia AS Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Air Maintenance Estonia AS you will receive after purchase—no placeholders. The report evaluates competitive rivalry, supplier and buyer power, and threats of entry and substitutes. It's professionally formatted, complete, and ready for immediate download and use.

From Overview to Strategy Blueprint

Air Maintenance Estonia AS faces moderate supplier leverage and niche customer demands, balanced by regulatory barriers and moderate threat of entrants in MRO services. Competitive rivalry hinges on technical expertise and turn-time advantages, while substitutes remain limited for certified maintenance. This snapshot highlights key pressures and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

OEM control of parts and manuals

OEMs tightly control proprietary parts, repair data and tooling approvals, giving them strong pricing power and direct control over aftermarket access in 2024. Air Maintenance Estonia requires current manuals and licences to maintain Boeing 737 and Airbus A320 families, which together comprise roughly two-thirds of the global narrowbody fleet. Limited alternative sources for critical components constrain AME’s negotiation leverage, lengthening lead times and elevating input costs.

Engine and component shop dependencies

Specialized engine/APU and module overhauls are concentrated in a handful of certified shops (notably CFM and Pratt & Whitney authorized facilities), limiting Air Maintenance Estonia’s supplier options and raising switching costs. AOG incidents in 2024 amplify supplier leverage as emergency slots command premiums and prioritize OEM-affiliated shops. Scarce overhaul slots constrain AME’s ability to meet TAT commitments to customers, increasing service risk and cost exposure.

Approved distributor and logistics networks

Approved distributors for rotables and logistics providers directly shape cost and availability, with AOG expedited shipping premiums commonly reaching up to 25% in 2024; Estonian operations benefit from EU single-market movement but rely on EU-wide logistics to maintain 2–4 day transit to major hubs. Freight volatility and fuel-linked surcharges remain material, while non-EU parts face customs processing that can add 24–72 hours and extra fees, allowing suppliers to charge for speed and certainty.

Tooling, calibration, and software licensing

Recurring costs for calibrated tooling, test equipment and the maintenance software stack materially impact Air Maintenance Estonia; the global aircraft MRO market was about 89 billion USD in 2024 and digital MRO subscriptions grew ~12% YoY, strengthening supplier pricing power. Vendor lock-in around digital maintenance platforms and data subscriptions raises switching costs and dependency. Compliance-driven calibration intervals and software updates are mandatory; lapses risk audit findings and operational delays.

- Calibration & tooling: recurring CAPEX/OPEX concentration

- Software/data: rising subscription spend, vendor lock-in

- Compliance risk: missed calibrations → audit findings/downtime

Skilled labor and subcontractors

Licensed B1/B2 technicians and niche subcontractors remain scarce across Europe, with EASA in 2024 noting persistent skills shortages that elevate their bargaining power; wage inflation and increased mobility further strengthen leverage. AME must offer competitive pay, clear career progression and in-house training to retain staff, otherwise staffing gaps force reliance on premium-priced subcontracting.

- Licensed B1/B2 scarcity — raises supplier leverage

- Wage inflation & mobility — increase compensation pressure

- Training & pay essential — reduces turnover

- Staff gaps → costly subcontract premiums

OEM parts & scarce shop capacity drive supplier pricing power in 89bn 2024 MRO market

OEM control of parts/tooling and limited certified overhaul shops give suppliers strong pricing power; 2024 MRO market ~89bn USD, AOG premiums up to 25% and overhaul slots scarce. Logistics: 2–4 day EU transit, non-EU customs add 24–72h. Skilled B1/B2 scarcity (EASA 2024) raises labor costs and subcontract reliance.

| Factor | 2024 metric | Impact |

|---|---|---|

| Market size | 89bn USD | Supplier leverage |

| AOG premium | up to 25% | Higher emergency costs |

| Transit/customs | 2–4d / 24–72h | Availability delays |

What is included in the product

Concise Porter's Five Forces assessment for Air Maintenance Estonia AS, outlining competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to clarify pricing pressure, profitability levers, and strategic vulnerabilities.

A concise one-sheet Porter's Five Forces for Air Maintenance Estonia AS—visual spider chart and editable pressure sliders to instantly reveal competitive pain points and strategy gaps, ready to drop into pitch decks or integrate with your Excel dashboards.

Customers Bargaining Power

Airlines and lessors concentrate demand

Airline groups and top lessors concentrate buying power—top 10 lessors control roughly 50% of the leased fleet and airlines accounted for the bulk of the ~90 billion USD global commercial MRO spend in 2023. They benchmark MROs aggressively on price, turnaround time and on-wing reliability across competitive panels. Volume commitments unlock tiered discounts that compress supplier margins. AME must therefore differentiate on lower unit cost, higher quality and strict schedule adherence to retain contracts.

Price sensitivity and cyclical budgets

Operators increasingly scrutinize maintenance costs amid cyclical budgets and 2024 fuel and demand volatility, driving tougher price talks with AME. Heavy check deferrals within regulatory limits amplify leverage, concentrating spend into fewer, high-stakes events and intensifying negotiations. Buyers demand PBH/hourly contracts and fixed TAT penalties, pressuring margins. AME must offer flexible pricing and value-added options to protect profitability.

Moderate switching costs within EASA network

Within the EASA-regulated market covering the EU27, buyers can shift work between certified MROs with relative ease, though onboarding new providers incurs induction, ferry and learning-curve costs; multiyear frame agreements commonly spanning 3–5 years partially lock in scopes, and delivering superior first-time quality materially reduces churn risk.

Demand for bundled services (CAMO + MRO)

Customers increasingly prefer integrated CAMO plus MRO to simplify oversight and comply with EASA Part-CAMO requirements; bundling lowers buyer search and coordination costs, though many still unbundle services periodically to price-check, keeping bargaining power moderate. End-to-end packages enhance AME’s client stickiness, while contract renewals remain tightly tied to measurable performance KPIs.

- Integrated CAMO+MRO reduces admin burden

- Bundling lowers search/coordination costs

- Buyers unbundle to benchmark pricing

- Renewals driven by KPI performance

Seasonality and slot leverage

Peak seasons let buyers who pre-book slots up to 12 months ahead secure better terms, while off-peak capacity pressures MROs to discount—industry reports show utilization swings driving price concessions around 10–15% in low months. Airlines with flexible schedules arbitrage timing, and AME’s slot management directly shifts its pricing power and margin capture.

- Pre-booking: up to 12 months

- Price concessions: ~10–15% off-peak

- Utilization swings: seasonal

- AME slot control: key to margins

Buyers have high leverage: top-10 lessors ~50%; global MRO ~90B USD

Buyers hold moderate-to-high bargaining power: top 10 lessors control ~50% of the leased fleet and global commercial MRO spend was ~90 billion USD in 2023, driving aggressive price/turnaround benchmarking. Volume commitments and PBH contracts compress margins; off-peak pricing concessions run ~10–15% while pre-booking up to 12 months secures better terms. Bundled CAMO+MRO raises stickiness but renewals hinge on KPI performance.

| Metric | Value |

|---|---|

| Top-10 lessors share | ~50% |

| Global MRO spend (2023) | ~90 B USD |

| Pre-booking | Up to 12 months |

| Off-peak concessions | ~10–15% |

Preview Before You Purchase

Air Maintenance Estonia AS Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Air Maintenance Estonia AS you will receive after purchase—no placeholders. The report evaluates competitive rivalry, supplier and buyer power, and threats of entry and substitutes. It's professionally formatted, complete, and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Air Maintenance Estonia AS faces moderate supplier leverage and niche customer demands, balanced by regulatory barriers and moderate threat of entrants in MRO services. Competitive rivalry hinges on technical expertise and turn-time advantages, while substitutes remain limited for certified maintenance. This snapshot highlights key pressures and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

OEM control of parts and manuals

OEMs tightly control proprietary parts, repair data and tooling approvals, giving them strong pricing power and direct control over aftermarket access in 2024. Air Maintenance Estonia requires current manuals and licences to maintain Boeing 737 and Airbus A320 families, which together comprise roughly two-thirds of the global narrowbody fleet. Limited alternative sources for critical components constrain AME’s negotiation leverage, lengthening lead times and elevating input costs.

Engine and component shop dependencies

Specialized engine/APU and module overhauls are concentrated in a handful of certified shops (notably CFM and Pratt & Whitney authorized facilities), limiting Air Maintenance Estonia’s supplier options and raising switching costs. AOG incidents in 2024 amplify supplier leverage as emergency slots command premiums and prioritize OEM-affiliated shops. Scarce overhaul slots constrain AME’s ability to meet TAT commitments to customers, increasing service risk and cost exposure.

Approved distributor and logistics networks

Approved distributors for rotables and logistics providers directly shape cost and availability, with AOG expedited shipping premiums commonly reaching up to 25% in 2024; Estonian operations benefit from EU single-market movement but rely on EU-wide logistics to maintain 2–4 day transit to major hubs. Freight volatility and fuel-linked surcharges remain material, while non-EU parts face customs processing that can add 24–72 hours and extra fees, allowing suppliers to charge for speed and certainty.

Tooling, calibration, and software licensing

Recurring costs for calibrated tooling, test equipment and the maintenance software stack materially impact Air Maintenance Estonia; the global aircraft MRO market was about 89 billion USD in 2024 and digital MRO subscriptions grew ~12% YoY, strengthening supplier pricing power. Vendor lock-in around digital maintenance platforms and data subscriptions raises switching costs and dependency. Compliance-driven calibration intervals and software updates are mandatory; lapses risk audit findings and operational delays.

- Calibration & tooling: recurring CAPEX/OPEX concentration

- Software/data: rising subscription spend, vendor lock-in

- Compliance risk: missed calibrations → audit findings/downtime

Skilled labor and subcontractors

Licensed B1/B2 technicians and niche subcontractors remain scarce across Europe, with EASA in 2024 noting persistent skills shortages that elevate their bargaining power; wage inflation and increased mobility further strengthen leverage. AME must offer competitive pay, clear career progression and in-house training to retain staff, otherwise staffing gaps force reliance on premium-priced subcontracting.

- Licensed B1/B2 scarcity — raises supplier leverage

- Wage inflation & mobility — increase compensation pressure

- Training & pay essential — reduces turnover

- Staff gaps → costly subcontract premiums

OEM parts & scarce shop capacity drive supplier pricing power in 89bn 2024 MRO market

OEM control of parts/tooling and limited certified overhaul shops give suppliers strong pricing power; 2024 MRO market ~89bn USD, AOG premiums up to 25% and overhaul slots scarce. Logistics: 2–4 day EU transit, non-EU customs add 24–72h. Skilled B1/B2 scarcity (EASA 2024) raises labor costs and subcontract reliance.

| Factor | 2024 metric | Impact |

|---|---|---|

| Market size | 89bn USD | Supplier leverage |

| AOG premium | up to 25% | Higher emergency costs |

| Transit/customs | 2–4d / 24–72h | Availability delays |

What is included in the product

Concise Porter's Five Forces assessment for Air Maintenance Estonia AS, outlining competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to clarify pricing pressure, profitability levers, and strategic vulnerabilities.

A concise one-sheet Porter's Five Forces for Air Maintenance Estonia AS—visual spider chart and editable pressure sliders to instantly reveal competitive pain points and strategy gaps, ready to drop into pitch decks or integrate with your Excel dashboards.

Customers Bargaining Power

Airlines and lessors concentrate demand

Airline groups and top lessors concentrate buying power—top 10 lessors control roughly 50% of the leased fleet and airlines accounted for the bulk of the ~90 billion USD global commercial MRO spend in 2023. They benchmark MROs aggressively on price, turnaround time and on-wing reliability across competitive panels. Volume commitments unlock tiered discounts that compress supplier margins. AME must therefore differentiate on lower unit cost, higher quality and strict schedule adherence to retain contracts.

Price sensitivity and cyclical budgets

Operators increasingly scrutinize maintenance costs amid cyclical budgets and 2024 fuel and demand volatility, driving tougher price talks with AME. Heavy check deferrals within regulatory limits amplify leverage, concentrating spend into fewer, high-stakes events and intensifying negotiations. Buyers demand PBH/hourly contracts and fixed TAT penalties, pressuring margins. AME must offer flexible pricing and value-added options to protect profitability.

Moderate switching costs within EASA network

Within the EASA-regulated market covering the EU27, buyers can shift work between certified MROs with relative ease, though onboarding new providers incurs induction, ferry and learning-curve costs; multiyear frame agreements commonly spanning 3–5 years partially lock in scopes, and delivering superior first-time quality materially reduces churn risk.

Demand for bundled services (CAMO + MRO)

Customers increasingly prefer integrated CAMO plus MRO to simplify oversight and comply with EASA Part-CAMO requirements; bundling lowers buyer search and coordination costs, though many still unbundle services periodically to price-check, keeping bargaining power moderate. End-to-end packages enhance AME’s client stickiness, while contract renewals remain tightly tied to measurable performance KPIs.

- Integrated CAMO+MRO reduces admin burden

- Bundling lowers search/coordination costs

- Buyers unbundle to benchmark pricing

- Renewals driven by KPI performance

Seasonality and slot leverage

Peak seasons let buyers who pre-book slots up to 12 months ahead secure better terms, while off-peak capacity pressures MROs to discount—industry reports show utilization swings driving price concessions around 10–15% in low months. Airlines with flexible schedules arbitrage timing, and AME’s slot management directly shifts its pricing power and margin capture.

- Pre-booking: up to 12 months

- Price concessions: ~10–15% off-peak

- Utilization swings: seasonal

- AME slot control: key to margins

Buyers have high leverage: top-10 lessors ~50%; global MRO ~90B USD

Buyers hold moderate-to-high bargaining power: top 10 lessors control ~50% of the leased fleet and global commercial MRO spend was ~90 billion USD in 2023, driving aggressive price/turnaround benchmarking. Volume commitments and PBH contracts compress margins; off-peak pricing concessions run ~10–15% while pre-booking up to 12 months secures better terms. Bundled CAMO+MRO raises stickiness but renewals hinge on KPI performance.

| Metric | Value |

|---|---|

| Top-10 lessors share | ~50% |

| Global MRO spend (2023) | ~90 B USD |

| Pre-booking | Up to 12 months |

| Off-peak concessions | ~10–15% |

Preview Before You Purchase

Air Maintenance Estonia AS Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Air Maintenance Estonia AS you will receive after purchase—no placeholders. The report evaluates competitive rivalry, supplier and buyer power, and threats of entry and substitutes. It's professionally formatted, complete, and ready for immediate download and use.