Americold Realty Trust Porter's Five Forces Analysis

Don't Miss the Bigger Picture

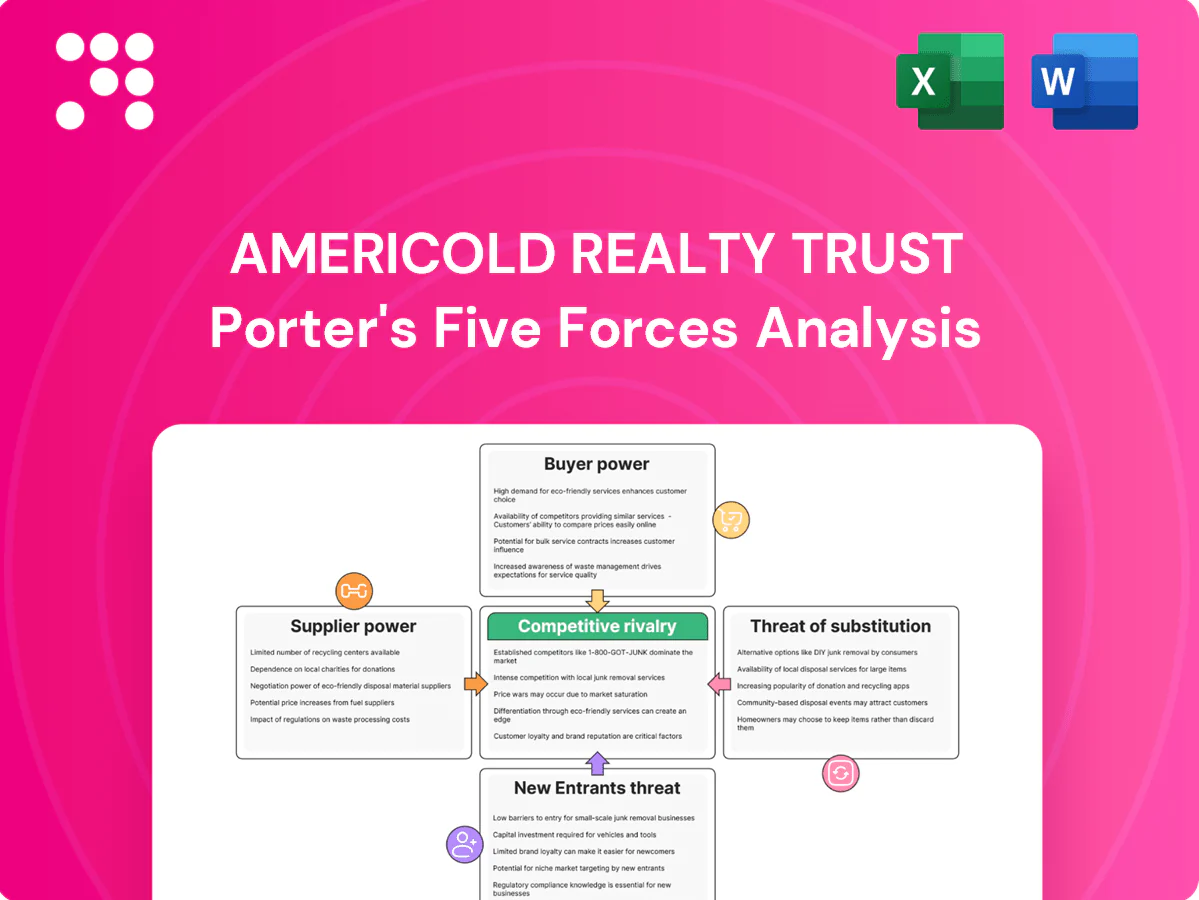

Americold Realty Trust faces intense competitive rivalry and significant buyer power from large grocery and foodservice customers, while supplier leverage is moderate due to specialized cold-chain infrastructure needs. Barriers to entry are high given capital intensity and regulatory demands, though technology and logistics innovation increase substitute risks. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated refrigeration OEMs

Industrial ammonia and CO2 refrigeration relies on a concentrated group of OEMs and systems integrators, raising switching costs and lead times for Americold and increasing vendor pricing leverage. Proprietary controls and tied maintenance contracts deepen operational dependence. Americold mitigates this by enforcing multi-vendor equipment standards and proactive lifecycle planning to reduce single-supplier risk and control capex timing.

Energy and utilities dependency

Cold warehouses are power intensive, making electricity (~$0.09/kWh average for US industrial users in 2024) and natural gas (~$2.60/MMBtu Henry Hub 2024 average) key inputs with limited local supplier choice. Rate volatility and peak demand charges can compress Americold margins during seasonal peaks. Long-term utility contracts and energy-efficiency investments (LED, freezer controls) can soften cost exposure. Onsite solar, CHP and demand-response programs increase negotiating leverage.

Skilled labor and contractors

Certified refrigeration technicians, automation specialists and food-safety personnel are scarce in many markets, raising operational risk for Americold. Tight labor markets — US unemployment ~3.7% in 2024 — elevate wage pressure and vendor rates. Building training pipelines and insourcing critical skills reduces exposure and downtime. Union presence in some locales (private-sector union rate ~6%) can raise local cost structures.

Construction and real estate inputs

Specialized insulated panels, racking, and automated systems have few qualified suppliers, and during build booms lead times often extend 12–24 weeks. Commodity swings—US hot‑rolled coil roughly $600–900/ton in 2024—and panel shortages raise project costs and compress margins. Pre‑buys, framework agreements and design standardization reduce supplier leverage, while site scarcity near demand nodes (industrial vacancy ~4% in top markets in 2024) amplifies input bargaining power.

- Few qualified suppliers: higher switching cost

- Lead times 12–24 weeks: schedule risk

- Steel $600–900/ton (2024): cost volatility

- Vacancy ~4% (top markets, 2024): site scarcity increases pressure

Technology and WMS providers

Technology and WMS providers are highly sticky for Americold, as warehouse management systems, sensors and telemetry become embedded across 240+ temperature-controlled facilities in 16 countries, making data migration and validation in regulated cold chains costly and time-consuming. Vendors can extract pricing power via module and license fees, though open APIs and Americold’s in-house data layers can lower switching costs and restore bargaining balance.

- High stickiness: integrated WMS, sensors, telemetry

- Scale: 240+ facilities across 16 countries

- Supplier leverage: module/license revenue streams

- Mitigation: open APIs and internal data layers reduce power

Supplier concentration and sticky WMS boost pricing power amid energy and labor cost pressure

Supplier concentration for refrigeration OEMs and insulated materials raises switching costs and pricing power. Energy (electricity ~$0.09/kWh, gas ~$2.60/MMBtu in 2024) and tight labor (US unemployment ~3.7% 2024) increase input cost volatility. Sticky WMS/automation across 240+ facilities (16 countries) gives vendors license revenue leverage, partially offset by open APIs and insourcing.

| Metric | 2024 | Impact |

|---|---|---|

| Electricity | $0.09/kWh | High Opex |

| Gas | $2.60/MMBtu | Heating/cooling cost |

| Facilities | 240+ | WMS stickiness |

What is included in the product

Tailored Porter's Five Forces analysis for Americold Realty Trust highlighting competitive rivalry in cold-storage logistics, supplier and buyer bargaining pressures, barriers deterring new entrants, threats from substitutes and disruptive technologies, and strategic implications for pricing and profitability.

A clear one-sheet Porter's Five Forces for Americold—instantly reveals supplier, buyer, rivalry, substitutes and entry pressures for fast decisions; customizable pressure levels and spider-chart visualization make it deck-ready and easy to integrate into reports.

Customers Bargaining Power

Large, concentrated customers

In 2024 food producers, large retailers and QSR/foodservice distributors remained highly consolidated and sophisticated, pressuring Americold for scale, strict SLAs and pricing concessions. National and multinational accounts use their volume to extract favorable terms, creating significant negotiating leverage. Multi-year, multi-site contracts provide revenue stability but typically compress storage and handling margins. This dynamic heightens customer bargaining power for Americold.

Switching and dual-sourcing

Operational switching costs exist, but many shippers dual-source to boost resilience, driving RFP cycles that benchmark prices across networks and pressure margins for Americold (ticker COLD). Americold must differentiate on temperature integrity, value-added services and geographic coverage to defend rates. Deeper integration via EDI, KPIs and SLA-backed performance metrics increases customer stickiness and reduces churn risk.

Demand volatility and seasonality

Demand volatility and seasonality shift bargaining toward capacity assurance as Americold, which operates roughly 250 temperature‑controlled facilities and about 1.6 billion cubic feet of storage, sees utilization spike during peak seasons. Buyers able to commit predictable volumes secure preferred rates and priority access. Flexible contracts with accessorial pricing shift cost risk back to shippers. Active capacity management and dynamic slotting strengthen Americold’s negotiating stance.

Value-added service bundling

Value-added bundles like case picking, blast freezing, kitting and transportation management create embedded workflows that raise effective switching costs and blunt pure price comparisons; Americold leverages its 250+ facility network to scale these services and defend fees. Buyers still pressure fees via total landed-cost analysis, but demonstrated SLA performance and documented savings (single-digit to low-teens percent on logistics for many clients) support premium pricing.

- Case picking: embedded workflow

- Blast freezing: reduces perishables loss

- Kitting: lowers retailer handling

- Transport Mgmt: raises switching cost

- SLA & demonstrated savings defend fees

Price transparency and data

Price transparency and regional benchmarking let customers compare Americold against peers and spot 10-25% rate gaps; with Americold reporting ~4.9B revenue in 2024 and ~275 facilities, high transparency strengthens buyer leverage. Proprietary benchmarking and outcome-based pricing can shift negotiations to value, while real-time KPIs (uptime, temp compliance) justify modest premiums.

- Market rate variance: 10-25%

- Americold 2024 revenue: ~4.9B

- Network size: ~275 facilities

- KPI transparency: supports premium pricing

Consolidated retailers squeeze cold storage margins despite scale and switching costs

Consolidated food retailers and distributors exert strong leverage, extracting volume discounts and SLAs that compress Americold margins. Americold’s scale, 275 facilities and 1.6B cu ft storage, plus value-added services raise switching costs and enable modest premiums. Price transparency (market rate variance 10-25%) and multi-site RFPs keep buyer power elevated.

| Metric | 2024 |

|---|---|

| Revenue | $4.9B |

| Facilities | 275 |

| Storage | 1.6B cu ft |

| Market rate variance | 10-25% |

What You See Is What You Get

Americold Realty Trust Porter's Five Forces Analysis

This Americold Realty Trust Porter’s Five Forces analysis assesses high competitive rivalry driven by consolidation and asset-heavy operations, low threat of new entrants due to capital and scale barriers, low substitute threat for specialized cold storage, and mixed supplier/buyer power shaped by large retailers and logistics partners. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Don't Miss the Bigger Picture

Americold Realty Trust faces intense competitive rivalry and significant buyer power from large grocery and foodservice customers, while supplier leverage is moderate due to specialized cold-chain infrastructure needs. Barriers to entry are high given capital intensity and regulatory demands, though technology and logistics innovation increase substitute risks. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated refrigeration OEMs

Industrial ammonia and CO2 refrigeration relies on a concentrated group of OEMs and systems integrators, raising switching costs and lead times for Americold and increasing vendor pricing leverage. Proprietary controls and tied maintenance contracts deepen operational dependence. Americold mitigates this by enforcing multi-vendor equipment standards and proactive lifecycle planning to reduce single-supplier risk and control capex timing.

Energy and utilities dependency

Cold warehouses are power intensive, making electricity (~$0.09/kWh average for US industrial users in 2024) and natural gas (~$2.60/MMBtu Henry Hub 2024 average) key inputs with limited local supplier choice. Rate volatility and peak demand charges can compress Americold margins during seasonal peaks. Long-term utility contracts and energy-efficiency investments (LED, freezer controls) can soften cost exposure. Onsite solar, CHP and demand-response programs increase negotiating leverage.

Skilled labor and contractors

Certified refrigeration technicians, automation specialists and food-safety personnel are scarce in many markets, raising operational risk for Americold. Tight labor markets — US unemployment ~3.7% in 2024 — elevate wage pressure and vendor rates. Building training pipelines and insourcing critical skills reduces exposure and downtime. Union presence in some locales (private-sector union rate ~6%) can raise local cost structures.

Construction and real estate inputs

Specialized insulated panels, racking, and automated systems have few qualified suppliers, and during build booms lead times often extend 12–24 weeks. Commodity swings—US hot‑rolled coil roughly $600–900/ton in 2024—and panel shortages raise project costs and compress margins. Pre‑buys, framework agreements and design standardization reduce supplier leverage, while site scarcity near demand nodes (industrial vacancy ~4% in top markets in 2024) amplifies input bargaining power.

- Few qualified suppliers: higher switching cost

- Lead times 12–24 weeks: schedule risk

- Steel $600–900/ton (2024): cost volatility

- Vacancy ~4% (top markets, 2024): site scarcity increases pressure

Technology and WMS providers

Technology and WMS providers are highly sticky for Americold, as warehouse management systems, sensors and telemetry become embedded across 240+ temperature-controlled facilities in 16 countries, making data migration and validation in regulated cold chains costly and time-consuming. Vendors can extract pricing power via module and license fees, though open APIs and Americold’s in-house data layers can lower switching costs and restore bargaining balance.

- High stickiness: integrated WMS, sensors, telemetry

- Scale: 240+ facilities across 16 countries

- Supplier leverage: module/license revenue streams

- Mitigation: open APIs and internal data layers reduce power

Supplier concentration and sticky WMS boost pricing power amid energy and labor cost pressure

Supplier concentration for refrigeration OEMs and insulated materials raises switching costs and pricing power. Energy (electricity ~$0.09/kWh, gas ~$2.60/MMBtu in 2024) and tight labor (US unemployment ~3.7% 2024) increase input cost volatility. Sticky WMS/automation across 240+ facilities (16 countries) gives vendors license revenue leverage, partially offset by open APIs and insourcing.

| Metric | 2024 | Impact |

|---|---|---|

| Electricity | $0.09/kWh | High Opex |

| Gas | $2.60/MMBtu | Heating/cooling cost |

| Facilities | 240+ | WMS stickiness |

What is included in the product

Tailored Porter's Five Forces analysis for Americold Realty Trust highlighting competitive rivalry in cold-storage logistics, supplier and buyer bargaining pressures, barriers deterring new entrants, threats from substitutes and disruptive technologies, and strategic implications for pricing and profitability.

A clear one-sheet Porter's Five Forces for Americold—instantly reveals supplier, buyer, rivalry, substitutes and entry pressures for fast decisions; customizable pressure levels and spider-chart visualization make it deck-ready and easy to integrate into reports.

Customers Bargaining Power

Large, concentrated customers

In 2024 food producers, large retailers and QSR/foodservice distributors remained highly consolidated and sophisticated, pressuring Americold for scale, strict SLAs and pricing concessions. National and multinational accounts use their volume to extract favorable terms, creating significant negotiating leverage. Multi-year, multi-site contracts provide revenue stability but typically compress storage and handling margins. This dynamic heightens customer bargaining power for Americold.

Switching and dual-sourcing

Operational switching costs exist, but many shippers dual-source to boost resilience, driving RFP cycles that benchmark prices across networks and pressure margins for Americold (ticker COLD). Americold must differentiate on temperature integrity, value-added services and geographic coverage to defend rates. Deeper integration via EDI, KPIs and SLA-backed performance metrics increases customer stickiness and reduces churn risk.

Demand volatility and seasonality

Demand volatility and seasonality shift bargaining toward capacity assurance as Americold, which operates roughly 250 temperature‑controlled facilities and about 1.6 billion cubic feet of storage, sees utilization spike during peak seasons. Buyers able to commit predictable volumes secure preferred rates and priority access. Flexible contracts with accessorial pricing shift cost risk back to shippers. Active capacity management and dynamic slotting strengthen Americold’s negotiating stance.

Value-added service bundling

Value-added bundles like case picking, blast freezing, kitting and transportation management create embedded workflows that raise effective switching costs and blunt pure price comparisons; Americold leverages its 250+ facility network to scale these services and defend fees. Buyers still pressure fees via total landed-cost analysis, but demonstrated SLA performance and documented savings (single-digit to low-teens percent on logistics for many clients) support premium pricing.

- Case picking: embedded workflow

- Blast freezing: reduces perishables loss

- Kitting: lowers retailer handling

- Transport Mgmt: raises switching cost

- SLA & demonstrated savings defend fees

Price transparency and data

Price transparency and regional benchmarking let customers compare Americold against peers and spot 10-25% rate gaps; with Americold reporting ~4.9B revenue in 2024 and ~275 facilities, high transparency strengthens buyer leverage. Proprietary benchmarking and outcome-based pricing can shift negotiations to value, while real-time KPIs (uptime, temp compliance) justify modest premiums.

- Market rate variance: 10-25%

- Americold 2024 revenue: ~4.9B

- Network size: ~275 facilities

- KPI transparency: supports premium pricing

Consolidated retailers squeeze cold storage margins despite scale and switching costs

Consolidated food retailers and distributors exert strong leverage, extracting volume discounts and SLAs that compress Americold margins. Americold’s scale, 275 facilities and 1.6B cu ft storage, plus value-added services raise switching costs and enable modest premiums. Price transparency (market rate variance 10-25%) and multi-site RFPs keep buyer power elevated.

| Metric | 2024 |

|---|---|

| Revenue | $4.9B |

| Facilities | 275 |

| Storage | 1.6B cu ft |

| Market rate variance | 10-25% |

What You See Is What You Get

Americold Realty Trust Porter's Five Forces Analysis

This Americold Realty Trust Porter’s Five Forces analysis assesses high competitive rivalry driven by consolidation and asset-heavy operations, low threat of new entrants due to capital and scale barriers, low substitute threat for specialized cold storage, and mixed supplier/buyer power shaped by large retailers and logistics partners. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Americold Realty Trust faces intense competitive rivalry and significant buyer power from large grocery and foodservice customers, while supplier leverage is moderate due to specialized cold-chain infrastructure needs. Barriers to entry are high given capital intensity and regulatory demands, though technology and logistics innovation increase substitute risks. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated refrigeration OEMs

Industrial ammonia and CO2 refrigeration relies on a concentrated group of OEMs and systems integrators, raising switching costs and lead times for Americold and increasing vendor pricing leverage. Proprietary controls and tied maintenance contracts deepen operational dependence. Americold mitigates this by enforcing multi-vendor equipment standards and proactive lifecycle planning to reduce single-supplier risk and control capex timing.

Energy and utilities dependency

Cold warehouses are power intensive, making electricity (~$0.09/kWh average for US industrial users in 2024) and natural gas (~$2.60/MMBtu Henry Hub 2024 average) key inputs with limited local supplier choice. Rate volatility and peak demand charges can compress Americold margins during seasonal peaks. Long-term utility contracts and energy-efficiency investments (LED, freezer controls) can soften cost exposure. Onsite solar, CHP and demand-response programs increase negotiating leverage.

Skilled labor and contractors

Certified refrigeration technicians, automation specialists and food-safety personnel are scarce in many markets, raising operational risk for Americold. Tight labor markets — US unemployment ~3.7% in 2024 — elevate wage pressure and vendor rates. Building training pipelines and insourcing critical skills reduces exposure and downtime. Union presence in some locales (private-sector union rate ~6%) can raise local cost structures.

Construction and real estate inputs

Specialized insulated panels, racking, and automated systems have few qualified suppliers, and during build booms lead times often extend 12–24 weeks. Commodity swings—US hot‑rolled coil roughly $600–900/ton in 2024—and panel shortages raise project costs and compress margins. Pre‑buys, framework agreements and design standardization reduce supplier leverage, while site scarcity near demand nodes (industrial vacancy ~4% in top markets in 2024) amplifies input bargaining power.

- Few qualified suppliers: higher switching cost

- Lead times 12–24 weeks: schedule risk

- Steel $600–900/ton (2024): cost volatility

- Vacancy ~4% (top markets, 2024): site scarcity increases pressure

Technology and WMS providers

Technology and WMS providers are highly sticky for Americold, as warehouse management systems, sensors and telemetry become embedded across 240+ temperature-controlled facilities in 16 countries, making data migration and validation in regulated cold chains costly and time-consuming. Vendors can extract pricing power via module and license fees, though open APIs and Americold’s in-house data layers can lower switching costs and restore bargaining balance.

- High stickiness: integrated WMS, sensors, telemetry

- Scale: 240+ facilities across 16 countries

- Supplier leverage: module/license revenue streams

- Mitigation: open APIs and internal data layers reduce power

Supplier concentration and sticky WMS boost pricing power amid energy and labor cost pressure

Supplier concentration for refrigeration OEMs and insulated materials raises switching costs and pricing power. Energy (electricity ~$0.09/kWh, gas ~$2.60/MMBtu in 2024) and tight labor (US unemployment ~3.7% 2024) increase input cost volatility. Sticky WMS/automation across 240+ facilities (16 countries) gives vendors license revenue leverage, partially offset by open APIs and insourcing.

| Metric | 2024 | Impact |

|---|---|---|

| Electricity | $0.09/kWh | High Opex |

| Gas | $2.60/MMBtu | Heating/cooling cost |

| Facilities | 240+ | WMS stickiness |

What is included in the product

Tailored Porter's Five Forces analysis for Americold Realty Trust highlighting competitive rivalry in cold-storage logistics, supplier and buyer bargaining pressures, barriers deterring new entrants, threats from substitutes and disruptive technologies, and strategic implications for pricing and profitability.

A clear one-sheet Porter's Five Forces for Americold—instantly reveals supplier, buyer, rivalry, substitutes and entry pressures for fast decisions; customizable pressure levels and spider-chart visualization make it deck-ready and easy to integrate into reports.

Customers Bargaining Power

Large, concentrated customers

In 2024 food producers, large retailers and QSR/foodservice distributors remained highly consolidated and sophisticated, pressuring Americold for scale, strict SLAs and pricing concessions. National and multinational accounts use their volume to extract favorable terms, creating significant negotiating leverage. Multi-year, multi-site contracts provide revenue stability but typically compress storage and handling margins. This dynamic heightens customer bargaining power for Americold.

Switching and dual-sourcing

Operational switching costs exist, but many shippers dual-source to boost resilience, driving RFP cycles that benchmark prices across networks and pressure margins for Americold (ticker COLD). Americold must differentiate on temperature integrity, value-added services and geographic coverage to defend rates. Deeper integration via EDI, KPIs and SLA-backed performance metrics increases customer stickiness and reduces churn risk.

Demand volatility and seasonality

Demand volatility and seasonality shift bargaining toward capacity assurance as Americold, which operates roughly 250 temperature‑controlled facilities and about 1.6 billion cubic feet of storage, sees utilization spike during peak seasons. Buyers able to commit predictable volumes secure preferred rates and priority access. Flexible contracts with accessorial pricing shift cost risk back to shippers. Active capacity management and dynamic slotting strengthen Americold’s negotiating stance.

Value-added service bundling

Value-added bundles like case picking, blast freezing, kitting and transportation management create embedded workflows that raise effective switching costs and blunt pure price comparisons; Americold leverages its 250+ facility network to scale these services and defend fees. Buyers still pressure fees via total landed-cost analysis, but demonstrated SLA performance and documented savings (single-digit to low-teens percent on logistics for many clients) support premium pricing.

- Case picking: embedded workflow

- Blast freezing: reduces perishables loss

- Kitting: lowers retailer handling

- Transport Mgmt: raises switching cost

- SLA & demonstrated savings defend fees

Price transparency and data

Price transparency and regional benchmarking let customers compare Americold against peers and spot 10-25% rate gaps; with Americold reporting ~4.9B revenue in 2024 and ~275 facilities, high transparency strengthens buyer leverage. Proprietary benchmarking and outcome-based pricing can shift negotiations to value, while real-time KPIs (uptime, temp compliance) justify modest premiums.

- Market rate variance: 10-25%

- Americold 2024 revenue: ~4.9B

- Network size: ~275 facilities

- KPI transparency: supports premium pricing

Consolidated retailers squeeze cold storage margins despite scale and switching costs

Consolidated food retailers and distributors exert strong leverage, extracting volume discounts and SLAs that compress Americold margins. Americold’s scale, 275 facilities and 1.6B cu ft storage, plus value-added services raise switching costs and enable modest premiums. Price transparency (market rate variance 10-25%) and multi-site RFPs keep buyer power elevated.

| Metric | 2024 |

|---|---|

| Revenue | $4.9B |

| Facilities | 275 |

| Storage | 1.6B cu ft |

| Market rate variance | 10-25% |

What You See Is What You Get

Americold Realty Trust Porter's Five Forces Analysis

This Americold Realty Trust Porter’s Five Forces analysis assesses high competitive rivalry driven by consolidation and asset-heavy operations, low threat of new entrants due to capital and scale barriers, low substitute threat for specialized cold storage, and mixed supplier/buyer power shaped by large retailers and logistics partners. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.