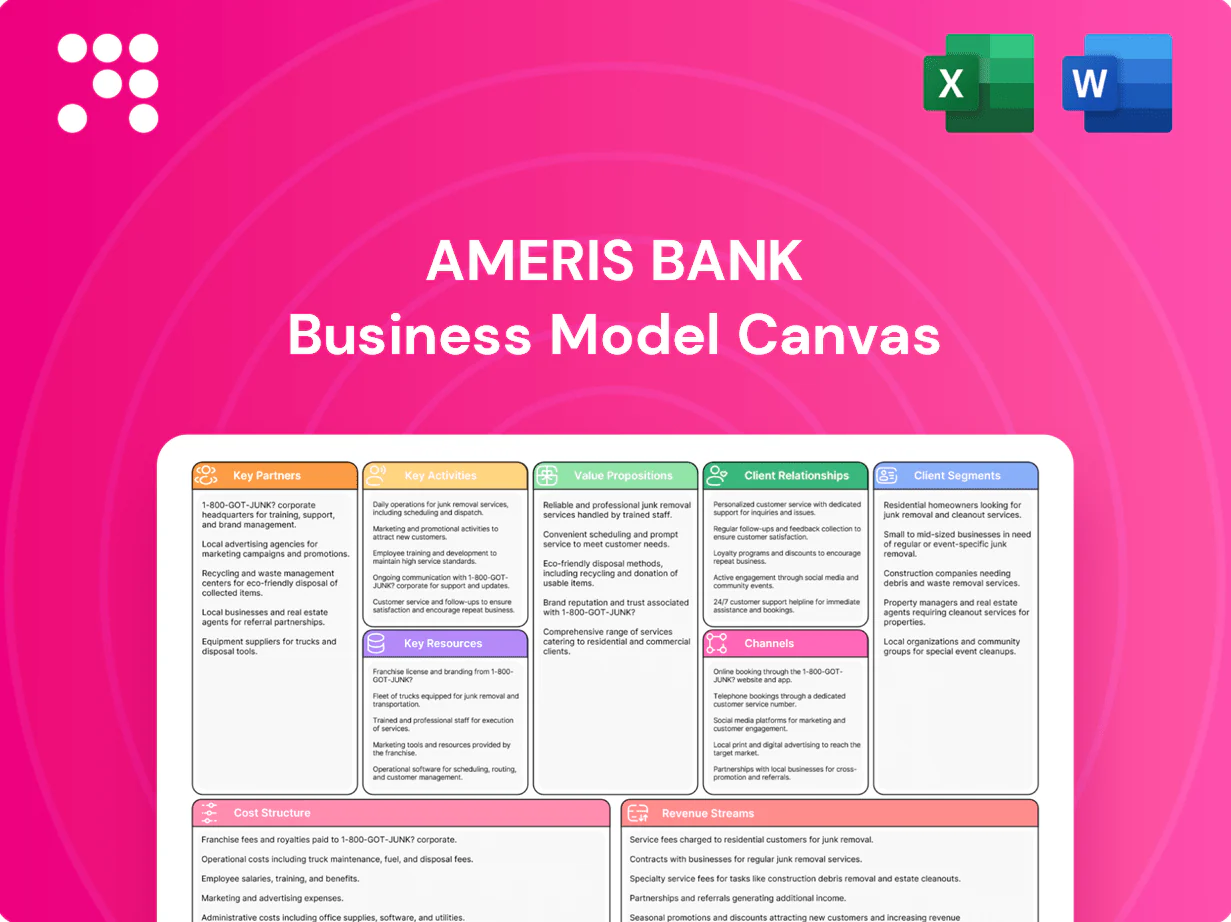

Ameris Bank Business Model Canvas

Business Model Canvas for a Regional Bank: Strategic Blueprint for Investors

Unlock the full strategic blueprint behind Ameris Bank’s business model in one actionable document. This in-depth Business Model Canvas reveals value propositions, customer segments, revenue drivers and cost structure to inform strategic decisions. Ideal for investors, consultants, and founders—download the complete canvas to benchmark and apply winning bank strategies.

Partnerships

Core banking and fintech vendors

Core banking and fintech vendors supply Ameris Bank with core systems, digital banking platforms, and payments rails that the bank relies on daily, backed by vendor SLAs typically targeting 99.95% uptime and SOC 2/PCI DSS compliance. These alliances accelerate feature rollout and lower build costs through shared roadmaps and APIs, with co-innovation plans focused on uptime, security, and UX. Vendors undergo quarterly audits to support regulatory and resilience standards.

Payment networks and processors

Payment networks and processors enable debit, credit, ACH, wires and RTP for Ameris Bank retail and commercial clients, with real-time payments adoption up ~40% year-over-year in 2024 driving higher transaction volumes. Interchange economics and routing options materially influence fee income, typically representing 20–40% of noninterest fee revenue at regional banks. Co-marketing and shared fraud tools raise card usage and cut losses, while deep integrations ensure speed, reliability and regulatory compliance.

Mortgage brokers and real estate partners

Mortgage brokers and real estate partners expand Ameris Bank mortgage origination across its Southeast footprint, driving lead flow for purchase, refinance, and construction loans. Joint education events and pre-approval programs deepen pipelines and increase conversion rates. Clear SLAs reduce cycle times and improve closing certainty, strengthening referral relationships and repeat business.

Credit bureaus and risk analytics firms

Data partners supply full credit files, scores and fraud signals to underwrite safely; in 2024 the US average FICO is ~714, improving risk segmentation. Advanced analytics refine pricing, line assignment and loss forecasting, cutting expected losses and VAR. Continuous portfolio monitoring lowers delinquencies and regulatory capital strain while APIs enable instant decisioning for consumers and small business.

- Data: credit files, scores, fraud signals

- Models: pricing, line assignment, loss forecasting

- Monitoring: delinquency & capital relief

- APIs: real-time decisioning

Community organizations and SBA programs

Ameris Bank partners with community organizations and SBA programs to advance CRA goals and catalyze small business growth. SBA 7a guarantees (85% for loans up to 150,000; 75% above) expand lending capacity and widen credit access. Local chambers and nonprofits boost brand visibility and referrals, while joint initiatives enhance financial inclusion and measurable community impact.

- CRA-aligned partnerships

- SBA 7a guaranty: 85%/75%

- Chambers/nonprofits for referrals

- Joint initiatives for inclusion

Digital bank scales fee income with 99.95% uptime, RTP +40% and instant underwriting

Ameris Bank leverages core banking and fintech vendors (SLA 99.95%, SOC2/PCI) and payment networks (RTP adoption +40% YoY 2024) to scale digital services and fee income (interchange 20–40% of noninterest fees). Data partners (avg FICO 714) enable instant underwriting and portfolio monitoring. SBA 7a (85%/75%) and community ties drive CRA lending and referrals.

| Metric | Value |

|---|---|

| Uptime | 99.95% |

| RTP Growth 2024 | +40% YoY |

| Interchange | 20–40% |

| Avg FICO | 714 |

| SBA 7a Guarantee | 85% / 75% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Ameris Bank outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams, with integrated SWOT and competitive insights for strategic use.

High-level view of Ameris Bank’s business model with editable cells—condenses strategy into a digestible one-page snapshot, saves hours of formatting, and is perfect for team collaboration, quick executive summaries, or comparing models side-by-side.

Activities

Deposit gathering and treasury services

Ameris focuses on acquiring and retaining low-cost retail and business deposits, supporting a deposit base of about $20.3 billion as of year-end 2024 to underpin lending and liquidity. The bank optimizes pricing, product mix, and targeted promotions by market to lower funding costs and boost sticky balances. Treasury offerings—cash management, ACH, wires, and merchant services—drive fee income and deepen business relationships while balance strategies manage liquidity and interest rate risk.

Lending origination and portfolio management

Underwrite consumer, mortgage, and commercial credits to Ameris Bank standards, supporting a loan portfolio of roughly $30 billion in 2024 while maintaining conservative credit metrics. Balance growth with risk via disciplined pricing, covenant enforcement, and collateralization to protect asset quality. Continuously monitor portfolios for early‑warning signs and workout needs, keeping nonperforming loans low (around 0.45% in 2024). Align capital allocation to maximize risk‑adjusted returns and preserve regulatory capital ratios.

Digital banking development

Enhance mobile and online features for seamless onboarding and servicing, targeting the 80%+ of customers who prefer digital channels in 2024 and supporting Ameris Bancorp’s scale (about $33.8B in assets). Prioritize payments, real-time alerts, P2P and robust self-service tools to cut branch traffic and reduce servicing costs. Use analytics to personalize offers, lift conversion rates, and remove friction. Maintain cybersecurity, resilience and consistent UX to protect deposits and uptime.

Risk, compliance, and audit

Ameris Bank operates within safety-and-soundness frameworks, adhering to Basel III minima (CET1 4.5%) and FDIC deposit insurance limits of 250,000 per depositor; it manages BSA/AML, KYC, fair-lending, and privacy controls with continuous monitoring. Internal audits identify and remediate findings promptly, while robust models, policies, and active board oversight govern risk appetite and compliance.

- Regulatory minima: CET1 4.5%

- FDIC insurance: 250,000

- BSA/AML & KYC continuous monitoring

- Internal audit → timely remediation

- Board oversight of models & policies

Relationship management and wealth advisory

Ameris Bank covers retail, business, and affluent clients with tailored guidance, coordinating deposits, lending, treasury, and investments to deliver integrated relationship management and wealth advisory.

It provides planning, fiduciary, and trust solutions to deepen share-of-wallet and extend client longevity; as of 2024 Ameris Bancorp reported approximately $38.6 billion in total assets and rising wealth-management fee income.

- Client segments: retail, business, affluent

- Integrated services: deposits, lending, treasury, investments

- Advisory: planning, fiduciary, trust

- Goals: higher share-of-wallet, longer client tenure

Low-cost deposits fuel $30B loan growth; NPLs 0.45% and CET1 4.5% safeguard $33.8B assets

Key activities: acquire/retain low‑cost deposits ($20.3B YE2024), underwrite and manage a ~$30B loan portfolio with NPLs ~0.45%, expand digital/treasury services to boost fee income, and maintain compliance/capital (CET1 minima 4.5%, FDIC limit 250,000) to support ~$33.8B in assets (2024).

| Metric | 2024 |

|---|---|

| Retail & business deposits | $20.3B |

| Loan portfolio | $30B |

| Total assets | $33.8B |

| NPL ratio | 0.45% |

| CET1 minimum | 4.5% |

| FDIC limit | $250,000 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Ameris Bank Business Model Canvas you'll receive—no mockups or samples. Upon purchase you'll get the full, editable file formatted identically to this preview, ready for presentation, analysis, or customization. No hidden pages, no surprises.

Business Model Canvas for a Regional Bank: Strategic Blueprint for Investors

Unlock the full strategic blueprint behind Ameris Bank’s business model in one actionable document. This in-depth Business Model Canvas reveals value propositions, customer segments, revenue drivers and cost structure to inform strategic decisions. Ideal for investors, consultants, and founders—download the complete canvas to benchmark and apply winning bank strategies.

Partnerships

Core banking and fintech vendors

Core banking and fintech vendors supply Ameris Bank with core systems, digital banking platforms, and payments rails that the bank relies on daily, backed by vendor SLAs typically targeting 99.95% uptime and SOC 2/PCI DSS compliance. These alliances accelerate feature rollout and lower build costs through shared roadmaps and APIs, with co-innovation plans focused on uptime, security, and UX. Vendors undergo quarterly audits to support regulatory and resilience standards.

Payment networks and processors

Payment networks and processors enable debit, credit, ACH, wires and RTP for Ameris Bank retail and commercial clients, with real-time payments adoption up ~40% year-over-year in 2024 driving higher transaction volumes. Interchange economics and routing options materially influence fee income, typically representing 20–40% of noninterest fee revenue at regional banks. Co-marketing and shared fraud tools raise card usage and cut losses, while deep integrations ensure speed, reliability and regulatory compliance.

Mortgage brokers and real estate partners

Mortgage brokers and real estate partners expand Ameris Bank mortgage origination across its Southeast footprint, driving lead flow for purchase, refinance, and construction loans. Joint education events and pre-approval programs deepen pipelines and increase conversion rates. Clear SLAs reduce cycle times and improve closing certainty, strengthening referral relationships and repeat business.

Credit bureaus and risk analytics firms

Data partners supply full credit files, scores and fraud signals to underwrite safely; in 2024 the US average FICO is ~714, improving risk segmentation. Advanced analytics refine pricing, line assignment and loss forecasting, cutting expected losses and VAR. Continuous portfolio monitoring lowers delinquencies and regulatory capital strain while APIs enable instant decisioning for consumers and small business.

- Data: credit files, scores, fraud signals

- Models: pricing, line assignment, loss forecasting

- Monitoring: delinquency & capital relief

- APIs: real-time decisioning

Community organizations and SBA programs

Ameris Bank partners with community organizations and SBA programs to advance CRA goals and catalyze small business growth. SBA 7a guarantees (85% for loans up to 150,000; 75% above) expand lending capacity and widen credit access. Local chambers and nonprofits boost brand visibility and referrals, while joint initiatives enhance financial inclusion and measurable community impact.

- CRA-aligned partnerships

- SBA 7a guaranty: 85%/75%

- Chambers/nonprofits for referrals

- Joint initiatives for inclusion

Digital bank scales fee income with 99.95% uptime, RTP +40% and instant underwriting

Ameris Bank leverages core banking and fintech vendors (SLA 99.95%, SOC2/PCI) and payment networks (RTP adoption +40% YoY 2024) to scale digital services and fee income (interchange 20–40% of noninterest fees). Data partners (avg FICO 714) enable instant underwriting and portfolio monitoring. SBA 7a (85%/75%) and community ties drive CRA lending and referrals.

| Metric | Value |

|---|---|

| Uptime | 99.95% |

| RTP Growth 2024 | +40% YoY |

| Interchange | 20–40% |

| Avg FICO | 714 |

| SBA 7a Guarantee | 85% / 75% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Ameris Bank outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams, with integrated SWOT and competitive insights for strategic use.

High-level view of Ameris Bank’s business model with editable cells—condenses strategy into a digestible one-page snapshot, saves hours of formatting, and is perfect for team collaboration, quick executive summaries, or comparing models side-by-side.

Activities

Deposit gathering and treasury services

Ameris focuses on acquiring and retaining low-cost retail and business deposits, supporting a deposit base of about $20.3 billion as of year-end 2024 to underpin lending and liquidity. The bank optimizes pricing, product mix, and targeted promotions by market to lower funding costs and boost sticky balances. Treasury offerings—cash management, ACH, wires, and merchant services—drive fee income and deepen business relationships while balance strategies manage liquidity and interest rate risk.

Lending origination and portfolio management

Underwrite consumer, mortgage, and commercial credits to Ameris Bank standards, supporting a loan portfolio of roughly $30 billion in 2024 while maintaining conservative credit metrics. Balance growth with risk via disciplined pricing, covenant enforcement, and collateralization to protect asset quality. Continuously monitor portfolios for early‑warning signs and workout needs, keeping nonperforming loans low (around 0.45% in 2024). Align capital allocation to maximize risk‑adjusted returns and preserve regulatory capital ratios.

Digital banking development

Enhance mobile and online features for seamless onboarding and servicing, targeting the 80%+ of customers who prefer digital channels in 2024 and supporting Ameris Bancorp’s scale (about $33.8B in assets). Prioritize payments, real-time alerts, P2P and robust self-service tools to cut branch traffic and reduce servicing costs. Use analytics to personalize offers, lift conversion rates, and remove friction. Maintain cybersecurity, resilience and consistent UX to protect deposits and uptime.

Risk, compliance, and audit

Ameris Bank operates within safety-and-soundness frameworks, adhering to Basel III minima (CET1 4.5%) and FDIC deposit insurance limits of 250,000 per depositor; it manages BSA/AML, KYC, fair-lending, and privacy controls with continuous monitoring. Internal audits identify and remediate findings promptly, while robust models, policies, and active board oversight govern risk appetite and compliance.

- Regulatory minima: CET1 4.5%

- FDIC insurance: 250,000

- BSA/AML & KYC continuous monitoring

- Internal audit → timely remediation

- Board oversight of models & policies

Relationship management and wealth advisory

Ameris Bank covers retail, business, and affluent clients with tailored guidance, coordinating deposits, lending, treasury, and investments to deliver integrated relationship management and wealth advisory.

It provides planning, fiduciary, and trust solutions to deepen share-of-wallet and extend client longevity; as of 2024 Ameris Bancorp reported approximately $38.6 billion in total assets and rising wealth-management fee income.

- Client segments: retail, business, affluent

- Integrated services: deposits, lending, treasury, investments

- Advisory: planning, fiduciary, trust

- Goals: higher share-of-wallet, longer client tenure

Low-cost deposits fuel $30B loan growth; NPLs 0.45% and CET1 4.5% safeguard $33.8B assets

Key activities: acquire/retain low‑cost deposits ($20.3B YE2024), underwrite and manage a ~$30B loan portfolio with NPLs ~0.45%, expand digital/treasury services to boost fee income, and maintain compliance/capital (CET1 minima 4.5%, FDIC limit 250,000) to support ~$33.8B in assets (2024).

| Metric | 2024 |

|---|---|

| Retail & business deposits | $20.3B |

| Loan portfolio | $30B |

| Total assets | $33.8B |

| NPL ratio | 0.45% |

| CET1 minimum | 4.5% |

| FDIC limit | $250,000 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Ameris Bank Business Model Canvas you'll receive—no mockups or samples. Upon purchase you'll get the full, editable file formatted identically to this preview, ready for presentation, analysis, or customization. No hidden pages, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas for a Regional Bank: Strategic Blueprint for Investors

Unlock the full strategic blueprint behind Ameris Bank’s business model in one actionable document. This in-depth Business Model Canvas reveals value propositions, customer segments, revenue drivers and cost structure to inform strategic decisions. Ideal for investors, consultants, and founders—download the complete canvas to benchmark and apply winning bank strategies.

Partnerships

Core banking and fintech vendors

Core banking and fintech vendors supply Ameris Bank with core systems, digital banking platforms, and payments rails that the bank relies on daily, backed by vendor SLAs typically targeting 99.95% uptime and SOC 2/PCI DSS compliance. These alliances accelerate feature rollout and lower build costs through shared roadmaps and APIs, with co-innovation plans focused on uptime, security, and UX. Vendors undergo quarterly audits to support regulatory and resilience standards.

Payment networks and processors

Payment networks and processors enable debit, credit, ACH, wires and RTP for Ameris Bank retail and commercial clients, with real-time payments adoption up ~40% year-over-year in 2024 driving higher transaction volumes. Interchange economics and routing options materially influence fee income, typically representing 20–40% of noninterest fee revenue at regional banks. Co-marketing and shared fraud tools raise card usage and cut losses, while deep integrations ensure speed, reliability and regulatory compliance.

Mortgage brokers and real estate partners

Mortgage brokers and real estate partners expand Ameris Bank mortgage origination across its Southeast footprint, driving lead flow for purchase, refinance, and construction loans. Joint education events and pre-approval programs deepen pipelines and increase conversion rates. Clear SLAs reduce cycle times and improve closing certainty, strengthening referral relationships and repeat business.

Credit bureaus and risk analytics firms

Data partners supply full credit files, scores and fraud signals to underwrite safely; in 2024 the US average FICO is ~714, improving risk segmentation. Advanced analytics refine pricing, line assignment and loss forecasting, cutting expected losses and VAR. Continuous portfolio monitoring lowers delinquencies and regulatory capital strain while APIs enable instant decisioning for consumers and small business.

- Data: credit files, scores, fraud signals

- Models: pricing, line assignment, loss forecasting

- Monitoring: delinquency & capital relief

- APIs: real-time decisioning

Community organizations and SBA programs

Ameris Bank partners with community organizations and SBA programs to advance CRA goals and catalyze small business growth. SBA 7a guarantees (85% for loans up to 150,000; 75% above) expand lending capacity and widen credit access. Local chambers and nonprofits boost brand visibility and referrals, while joint initiatives enhance financial inclusion and measurable community impact.

- CRA-aligned partnerships

- SBA 7a guaranty: 85%/75%

- Chambers/nonprofits for referrals

- Joint initiatives for inclusion

Digital bank scales fee income with 99.95% uptime, RTP +40% and instant underwriting

Ameris Bank leverages core banking and fintech vendors (SLA 99.95%, SOC2/PCI) and payment networks (RTP adoption +40% YoY 2024) to scale digital services and fee income (interchange 20–40% of noninterest fees). Data partners (avg FICO 714) enable instant underwriting and portfolio monitoring. SBA 7a (85%/75%) and community ties drive CRA lending and referrals.

| Metric | Value |

|---|---|

| Uptime | 99.95% |

| RTP Growth 2024 | +40% YoY |

| Interchange | 20–40% |

| Avg FICO | 714 |

| SBA 7a Guarantee | 85% / 75% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Ameris Bank outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams, with integrated SWOT and competitive insights for strategic use.

High-level view of Ameris Bank’s business model with editable cells—condenses strategy into a digestible one-page snapshot, saves hours of formatting, and is perfect for team collaboration, quick executive summaries, or comparing models side-by-side.

Activities

Deposit gathering and treasury services

Ameris focuses on acquiring and retaining low-cost retail and business deposits, supporting a deposit base of about $20.3 billion as of year-end 2024 to underpin lending and liquidity. The bank optimizes pricing, product mix, and targeted promotions by market to lower funding costs and boost sticky balances. Treasury offerings—cash management, ACH, wires, and merchant services—drive fee income and deepen business relationships while balance strategies manage liquidity and interest rate risk.

Lending origination and portfolio management

Underwrite consumer, mortgage, and commercial credits to Ameris Bank standards, supporting a loan portfolio of roughly $30 billion in 2024 while maintaining conservative credit metrics. Balance growth with risk via disciplined pricing, covenant enforcement, and collateralization to protect asset quality. Continuously monitor portfolios for early‑warning signs and workout needs, keeping nonperforming loans low (around 0.45% in 2024). Align capital allocation to maximize risk‑adjusted returns and preserve regulatory capital ratios.

Digital banking development

Enhance mobile and online features for seamless onboarding and servicing, targeting the 80%+ of customers who prefer digital channels in 2024 and supporting Ameris Bancorp’s scale (about $33.8B in assets). Prioritize payments, real-time alerts, P2P and robust self-service tools to cut branch traffic and reduce servicing costs. Use analytics to personalize offers, lift conversion rates, and remove friction. Maintain cybersecurity, resilience and consistent UX to protect deposits and uptime.

Risk, compliance, and audit

Ameris Bank operates within safety-and-soundness frameworks, adhering to Basel III minima (CET1 4.5%) and FDIC deposit insurance limits of 250,000 per depositor; it manages BSA/AML, KYC, fair-lending, and privacy controls with continuous monitoring. Internal audits identify and remediate findings promptly, while robust models, policies, and active board oversight govern risk appetite and compliance.

- Regulatory minima: CET1 4.5%

- FDIC insurance: 250,000

- BSA/AML & KYC continuous monitoring

- Internal audit → timely remediation

- Board oversight of models & policies

Relationship management and wealth advisory

Ameris Bank covers retail, business, and affluent clients with tailored guidance, coordinating deposits, lending, treasury, and investments to deliver integrated relationship management and wealth advisory.

It provides planning, fiduciary, and trust solutions to deepen share-of-wallet and extend client longevity; as of 2024 Ameris Bancorp reported approximately $38.6 billion in total assets and rising wealth-management fee income.

- Client segments: retail, business, affluent

- Integrated services: deposits, lending, treasury, investments

- Advisory: planning, fiduciary, trust

- Goals: higher share-of-wallet, longer client tenure

Low-cost deposits fuel $30B loan growth; NPLs 0.45% and CET1 4.5% safeguard $33.8B assets

Key activities: acquire/retain low‑cost deposits ($20.3B YE2024), underwrite and manage a ~$30B loan portfolio with NPLs ~0.45%, expand digital/treasury services to boost fee income, and maintain compliance/capital (CET1 minima 4.5%, FDIC limit 250,000) to support ~$33.8B in assets (2024).

| Metric | 2024 |

|---|---|

| Retail & business deposits | $20.3B |

| Loan portfolio | $30B |

| Total assets | $33.8B |

| NPL ratio | 0.45% |

| CET1 minimum | 4.5% |

| FDIC limit | $250,000 |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Ameris Bank Business Model Canvas you'll receive—no mockups or samples. Upon purchase you'll get the full, editable file formatted identically to this preview, ready for presentation, analysis, or customization. No hidden pages, no surprises.