Ameris Bank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

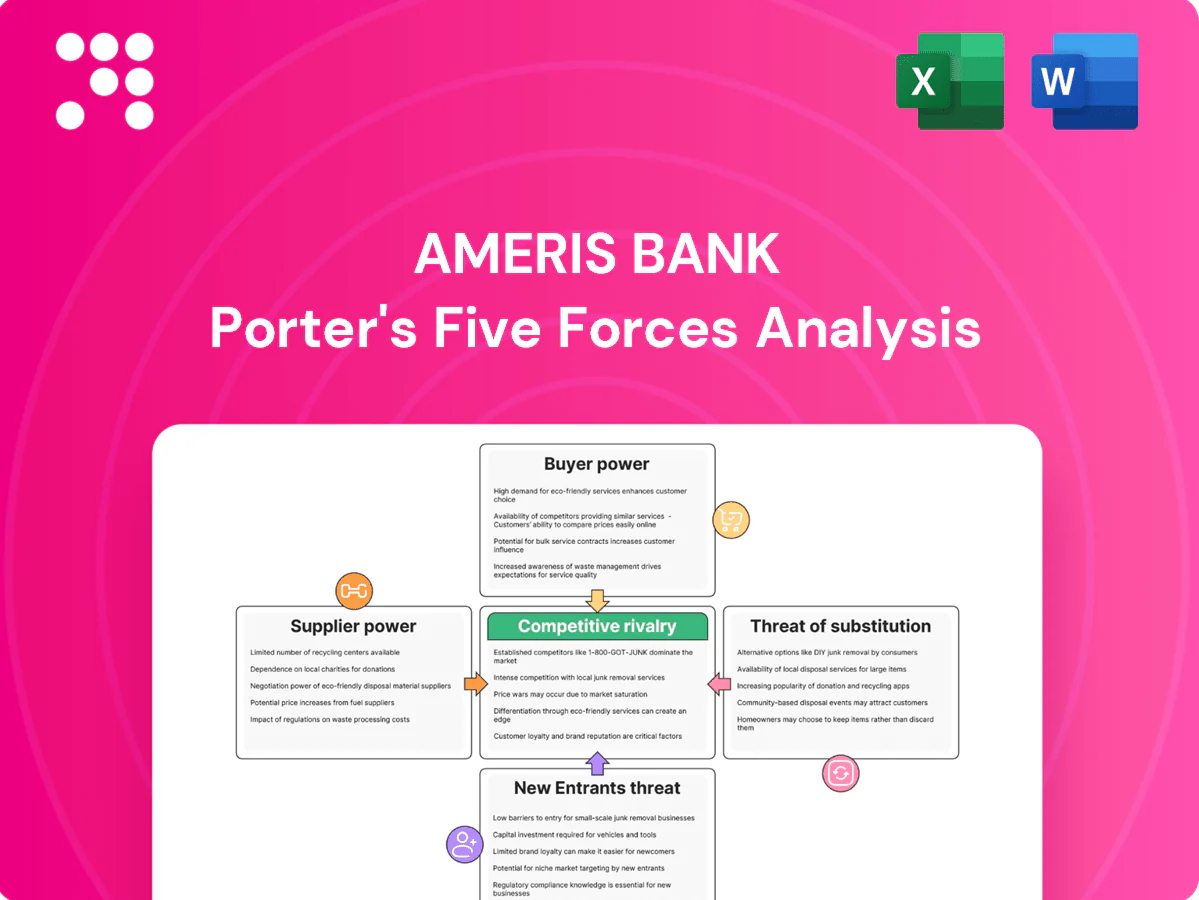

Ameris Bank faces moderate competitive rivalry, evolving regulatory pressures, and rising tech-enabled substitutes that could reshape margins and growth prospects; supplier and buyer power vary across its regional markets. This snapshot highlights key risks and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

Ameris Bank depends on a concentrated set of core banking processors, payment networks and cloud providers, a structural dynamic reflected in the US market where the top three core processors held roughly 70% market share in 2024, raising contractual lock-in and switching costs. This concentration gives suppliers leverage over pricing, SLAs and product roadmaps, pressuring margins. Ameris’s scale — $22.6B assets at YE 2024 — and multi-vendor sourcing partially offset supplier negotiating power.

Wholesale funding and capital markets

Access to brokered deposits, FHLB advances (system-wide advances around $1.0 trillion) and bond markets directly shape Ameris Bank’s cost of funds; reliance raises vulnerability to market spreads. In tighter liquidity cycles suppliers command higher spreads and stricter covenants, pressuring net interest margins. Credit ratings and market sentiment amplify pricing power, while a strong local deposit franchise reduces dependence on wholesale suppliers and associated leverage.

Specialized talent and compliance expertise

Skilled lenders, credit risk officers, and fintech engineers are scarce across the Southeast, giving these specialists heightened bargaining power over regional banks like Ameris. Wage inflation and poaching by nationwide banks pushed compensation premiums roughly into the high single digits in 2024, increasing hiring costs and turnover. Rising regulatory complexity drove compliance headcount needs materially higher, while strong culture and clear career paths remain the most effective levers to retain talent.

Data, fraud, and cybersecurity vendors

Risk analytics, KYC/AML, and fraud tools are mission-critical for Ameris Bank, with the global fraud detection market estimated near 27 billion USD in 2024, giving top vendors pricing clout as best-in-class options remain limited and regularly upgraded.

- Integration often 6–12 months, raising switching frictions

- Limited suppliers drive premium pricing and roadmap dependence

- Volume commitments or consortium deals can cut unit costs 10–30%

Real estate and facilities providers

Prime branch and office locations in growth markets remain highly competitive; landlords in high-demand corridors can dictate lease terms and escalate rents, compressing margins. Long, often non-cancellable leases limit Ameris Bank’s flexibility to optimize its footprint, while 2024 digital banking adoption (~85% of retail interactions) gradually lowers physical-location dependence.

- Landlord leverage: high in growth corridors

- Lease rigidity: long terms restrict footprint changes

- Digital shift: ~85% retail interactions digital in 2024

Vendor concentration and funding risk pressure margins despite strong deposits and 85% digital use

Supplier concentration (top 3 core processors ~70% share in 2024) and mission-critical vendors (fraud market ~$27B) give pricing and roadmap leverage, pressuring margins despite Ameris’s $22.6B assets (YE2024). Funding suppliers (FHLB/wholesale) and market spreads (system advances ~$1.0T) drive cost-of-funds sensitivity; strong local deposits and digital adoption (~85% retail interactions 2024) mitigate reliance.

| Metric | 2024 |

|---|---|

| Top-3 core share | ~70% |

| Ameris assets | $22.6B |

| Fraud market | $27B |

| System advances | $1.0T |

| Digital retail | ~85% |

What is included in the product

Tailored Porter's Five Forces analysis for Ameris Bank that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes and emerging threats, with strategic insights to inform pricing, growth and risk decisions.

A clear one-sheet Porter's Five Forces for Ameris Bank—quickly highlights competitive pressures, regulatory risks, and supplier/customer leverage to speed strategic decisions and investor briefings.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can rapidly switch to higher-yield options via digital channels; online banks commonly offered >4% APY in 2024. Money market funds yielding ~4.3% and roughly $5.2 trillion in assets increase price transparency. This raises pressure on deposit betas and retention costs, squeezing margins for regional banks. Relationship bundles and cash-management features can materially reduce churn by improving stickiness.

Commercial borrowers with alternatives

Commercial borrowers can shop loans among regional banks, credit unions and private credit, increasing their leverage when competing term sheets drive tighter rates and looser covenants. Treasury services bundling by Ameris partially offsets price pressure by raising switching costs and deposit stickiness. Speed and certainty of close remain decisive advantages—borrowers often pick certainty over marginally better pricing.

Mortgage and consumer loan shoppers

Digital marketplaces let mortgage and consumer loan shoppers compare APRs and fees instantly, with online rate-shopping cited by industry surveys as a dominant channel in 2024. Brokers and fintechs, now handling roughly double-digit market share gains year-over-year, intensify bidding pressure on pricing. Buyers increasingly demand fee waivers and faster underwriting—average digital close times fell to days, not weeks in 2024—forcing Ameris to balance tighter pricing with credit risk controls and service quality.

Wealth and treasury management clients

High-balance wealth and treasury clients negotiate fees by AUM and volumes, pressuring margins; Ameris Bancorp reported total assets of about 38.0 billion USD at 12/31/2023. Platform breadth and advisor quality raise stickiness, while multi-bank relationships increase client leverage. Advanced analytics and bespoke reporting can justify premium pricing.

- Fee negotiation: AUM/volume

- Stickiness: platform + advisors

- Leverage: multi-bank links

- Pricing support: analytics

Low switching costs via digital

Digital account-opening and transfer tools have slashed friction, letting customers move deposits quickly; Ameris Bancorp reported about 32.6 billion in assets in 2024, increasing competitive pressure on margins. Buyers can diversify across institutions easily, making rewards and UX decisive; loyalty programs and embedded services are the main levers to raise switching costs.

- Frictionless onboarding

- Diversification ease

- Rewards/UX as differentiators

- Loyalty/embedded services raise costs

Depositors chase >4% APY; MMFs ~4.3% squeeze bank margins

Rate-sensitive depositors shift to >4% APY online; money market funds yield ~4.3% with $5.2T assets, tightening deposit betas. Commercial borrowers shop term sheets; speed, certainty and treasury bundles boost stickiness. Ameris assets ~$32.6B (2024); loyalty, analytics and platform breadth are primary levers to defend margins.

| Metric | 2024 value |

|---|---|

| Online savings APY | >4% |

| Money market yield / assets | ~4.3% / $5.2T |

| Digital close time | days |

| Ameris total assets | $32.6B |

What You See Is What You Get

Ameris Bank Porter's Five Forces Analysis

This preview shows the exact Ameris Bank Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the fully formatted, ready-to-use file covering bargaining power of suppliers and buyers, competitive rivalry, and threats of new entrants and substitutes. Upon payment you'll get instant access to this identical file for download and use.

Don't Miss the Bigger Picture

Ameris Bank faces moderate competitive rivalry, evolving regulatory pressures, and rising tech-enabled substitutes that could reshape margins and growth prospects; supplier and buyer power vary across its regional markets. This snapshot highlights key risks and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

Ameris Bank depends on a concentrated set of core banking processors, payment networks and cloud providers, a structural dynamic reflected in the US market where the top three core processors held roughly 70% market share in 2024, raising contractual lock-in and switching costs. This concentration gives suppliers leverage over pricing, SLAs and product roadmaps, pressuring margins. Ameris’s scale — $22.6B assets at YE 2024 — and multi-vendor sourcing partially offset supplier negotiating power.

Wholesale funding and capital markets

Access to brokered deposits, FHLB advances (system-wide advances around $1.0 trillion) and bond markets directly shape Ameris Bank’s cost of funds; reliance raises vulnerability to market spreads. In tighter liquidity cycles suppliers command higher spreads and stricter covenants, pressuring net interest margins. Credit ratings and market sentiment amplify pricing power, while a strong local deposit franchise reduces dependence on wholesale suppliers and associated leverage.

Specialized talent and compliance expertise

Skilled lenders, credit risk officers, and fintech engineers are scarce across the Southeast, giving these specialists heightened bargaining power over regional banks like Ameris. Wage inflation and poaching by nationwide banks pushed compensation premiums roughly into the high single digits in 2024, increasing hiring costs and turnover. Rising regulatory complexity drove compliance headcount needs materially higher, while strong culture and clear career paths remain the most effective levers to retain talent.

Data, fraud, and cybersecurity vendors

Risk analytics, KYC/AML, and fraud tools are mission-critical for Ameris Bank, with the global fraud detection market estimated near 27 billion USD in 2024, giving top vendors pricing clout as best-in-class options remain limited and regularly upgraded.

- Integration often 6–12 months, raising switching frictions

- Limited suppliers drive premium pricing and roadmap dependence

- Volume commitments or consortium deals can cut unit costs 10–30%

Real estate and facilities providers

Prime branch and office locations in growth markets remain highly competitive; landlords in high-demand corridors can dictate lease terms and escalate rents, compressing margins. Long, often non-cancellable leases limit Ameris Bank’s flexibility to optimize its footprint, while 2024 digital banking adoption (~85% of retail interactions) gradually lowers physical-location dependence.

- Landlord leverage: high in growth corridors

- Lease rigidity: long terms restrict footprint changes

- Digital shift: ~85% retail interactions digital in 2024

Vendor concentration and funding risk pressure margins despite strong deposits and 85% digital use

Supplier concentration (top 3 core processors ~70% share in 2024) and mission-critical vendors (fraud market ~$27B) give pricing and roadmap leverage, pressuring margins despite Ameris’s $22.6B assets (YE2024). Funding suppliers (FHLB/wholesale) and market spreads (system advances ~$1.0T) drive cost-of-funds sensitivity; strong local deposits and digital adoption (~85% retail interactions 2024) mitigate reliance.

| Metric | 2024 |

|---|---|

| Top-3 core share | ~70% |

| Ameris assets | $22.6B |

| Fraud market | $27B |

| System advances | $1.0T |

| Digital retail | ~85% |

What is included in the product

Tailored Porter's Five Forces analysis for Ameris Bank that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes and emerging threats, with strategic insights to inform pricing, growth and risk decisions.

A clear one-sheet Porter's Five Forces for Ameris Bank—quickly highlights competitive pressures, regulatory risks, and supplier/customer leverage to speed strategic decisions and investor briefings.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can rapidly switch to higher-yield options via digital channels; online banks commonly offered >4% APY in 2024. Money market funds yielding ~4.3% and roughly $5.2 trillion in assets increase price transparency. This raises pressure on deposit betas and retention costs, squeezing margins for regional banks. Relationship bundles and cash-management features can materially reduce churn by improving stickiness.

Commercial borrowers with alternatives

Commercial borrowers can shop loans among regional banks, credit unions and private credit, increasing their leverage when competing term sheets drive tighter rates and looser covenants. Treasury services bundling by Ameris partially offsets price pressure by raising switching costs and deposit stickiness. Speed and certainty of close remain decisive advantages—borrowers often pick certainty over marginally better pricing.

Mortgage and consumer loan shoppers

Digital marketplaces let mortgage and consumer loan shoppers compare APRs and fees instantly, with online rate-shopping cited by industry surveys as a dominant channel in 2024. Brokers and fintechs, now handling roughly double-digit market share gains year-over-year, intensify bidding pressure on pricing. Buyers increasingly demand fee waivers and faster underwriting—average digital close times fell to days, not weeks in 2024—forcing Ameris to balance tighter pricing with credit risk controls and service quality.

Wealth and treasury management clients

High-balance wealth and treasury clients negotiate fees by AUM and volumes, pressuring margins; Ameris Bancorp reported total assets of about 38.0 billion USD at 12/31/2023. Platform breadth and advisor quality raise stickiness, while multi-bank relationships increase client leverage. Advanced analytics and bespoke reporting can justify premium pricing.

- Fee negotiation: AUM/volume

- Stickiness: platform + advisors

- Leverage: multi-bank links

- Pricing support: analytics

Low switching costs via digital

Digital account-opening and transfer tools have slashed friction, letting customers move deposits quickly; Ameris Bancorp reported about 32.6 billion in assets in 2024, increasing competitive pressure on margins. Buyers can diversify across institutions easily, making rewards and UX decisive; loyalty programs and embedded services are the main levers to raise switching costs.

- Frictionless onboarding

- Diversification ease

- Rewards/UX as differentiators

- Loyalty/embedded services raise costs

Depositors chase >4% APY; MMFs ~4.3% squeeze bank margins

Rate-sensitive depositors shift to >4% APY online; money market funds yield ~4.3% with $5.2T assets, tightening deposit betas. Commercial borrowers shop term sheets; speed, certainty and treasury bundles boost stickiness. Ameris assets ~$32.6B (2024); loyalty, analytics and platform breadth are primary levers to defend margins.

| Metric | 2024 value |

|---|---|

| Online savings APY | >4% |

| Money market yield / assets | ~4.3% / $5.2T |

| Digital close time | days |

| Ameris total assets | $32.6B |

What You See Is What You Get

Ameris Bank Porter's Five Forces Analysis

This preview shows the exact Ameris Bank Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the fully formatted, ready-to-use file covering bargaining power of suppliers and buyers, competitive rivalry, and threats of new entrants and substitutes. Upon payment you'll get instant access to this identical file for download and use.

Description

Don't Miss the Bigger Picture

Ameris Bank faces moderate competitive rivalry, evolving regulatory pressures, and rising tech-enabled substitutes that could reshape margins and growth prospects; supplier and buyer power vary across its regional markets. This snapshot highlights key risks and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

Ameris Bank depends on a concentrated set of core banking processors, payment networks and cloud providers, a structural dynamic reflected in the US market where the top three core processors held roughly 70% market share in 2024, raising contractual lock-in and switching costs. This concentration gives suppliers leverage over pricing, SLAs and product roadmaps, pressuring margins. Ameris’s scale — $22.6B assets at YE 2024 — and multi-vendor sourcing partially offset supplier negotiating power.

Wholesale funding and capital markets

Access to brokered deposits, FHLB advances (system-wide advances around $1.0 trillion) and bond markets directly shape Ameris Bank’s cost of funds; reliance raises vulnerability to market spreads. In tighter liquidity cycles suppliers command higher spreads and stricter covenants, pressuring net interest margins. Credit ratings and market sentiment amplify pricing power, while a strong local deposit franchise reduces dependence on wholesale suppliers and associated leverage.

Specialized talent and compliance expertise

Skilled lenders, credit risk officers, and fintech engineers are scarce across the Southeast, giving these specialists heightened bargaining power over regional banks like Ameris. Wage inflation and poaching by nationwide banks pushed compensation premiums roughly into the high single digits in 2024, increasing hiring costs and turnover. Rising regulatory complexity drove compliance headcount needs materially higher, while strong culture and clear career paths remain the most effective levers to retain talent.

Data, fraud, and cybersecurity vendors

Risk analytics, KYC/AML, and fraud tools are mission-critical for Ameris Bank, with the global fraud detection market estimated near 27 billion USD in 2024, giving top vendors pricing clout as best-in-class options remain limited and regularly upgraded.

- Integration often 6–12 months, raising switching frictions

- Limited suppliers drive premium pricing and roadmap dependence

- Volume commitments or consortium deals can cut unit costs 10–30%

Real estate and facilities providers

Prime branch and office locations in growth markets remain highly competitive; landlords in high-demand corridors can dictate lease terms and escalate rents, compressing margins. Long, often non-cancellable leases limit Ameris Bank’s flexibility to optimize its footprint, while 2024 digital banking adoption (~85% of retail interactions) gradually lowers physical-location dependence.

- Landlord leverage: high in growth corridors

- Lease rigidity: long terms restrict footprint changes

- Digital shift: ~85% retail interactions digital in 2024

Vendor concentration and funding risk pressure margins despite strong deposits and 85% digital use

Supplier concentration (top 3 core processors ~70% share in 2024) and mission-critical vendors (fraud market ~$27B) give pricing and roadmap leverage, pressuring margins despite Ameris’s $22.6B assets (YE2024). Funding suppliers (FHLB/wholesale) and market spreads (system advances ~$1.0T) drive cost-of-funds sensitivity; strong local deposits and digital adoption (~85% retail interactions 2024) mitigate reliance.

| Metric | 2024 |

|---|---|

| Top-3 core share | ~70% |

| Ameris assets | $22.6B |

| Fraud market | $27B |

| System advances | $1.0T |

| Digital retail | ~85% |

What is included in the product

Tailored Porter's Five Forces analysis for Ameris Bank that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes and emerging threats, with strategic insights to inform pricing, growth and risk decisions.

A clear one-sheet Porter's Five Forces for Ameris Bank—quickly highlights competitive pressures, regulatory risks, and supplier/customer leverage to speed strategic decisions and investor briefings.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can rapidly switch to higher-yield options via digital channels; online banks commonly offered >4% APY in 2024. Money market funds yielding ~4.3% and roughly $5.2 trillion in assets increase price transparency. This raises pressure on deposit betas and retention costs, squeezing margins for regional banks. Relationship bundles and cash-management features can materially reduce churn by improving stickiness.

Commercial borrowers with alternatives

Commercial borrowers can shop loans among regional banks, credit unions and private credit, increasing their leverage when competing term sheets drive tighter rates and looser covenants. Treasury services bundling by Ameris partially offsets price pressure by raising switching costs and deposit stickiness. Speed and certainty of close remain decisive advantages—borrowers often pick certainty over marginally better pricing.

Mortgage and consumer loan shoppers

Digital marketplaces let mortgage and consumer loan shoppers compare APRs and fees instantly, with online rate-shopping cited by industry surveys as a dominant channel in 2024. Brokers and fintechs, now handling roughly double-digit market share gains year-over-year, intensify bidding pressure on pricing. Buyers increasingly demand fee waivers and faster underwriting—average digital close times fell to days, not weeks in 2024—forcing Ameris to balance tighter pricing with credit risk controls and service quality.

Wealth and treasury management clients

High-balance wealth and treasury clients negotiate fees by AUM and volumes, pressuring margins; Ameris Bancorp reported total assets of about 38.0 billion USD at 12/31/2023. Platform breadth and advisor quality raise stickiness, while multi-bank relationships increase client leverage. Advanced analytics and bespoke reporting can justify premium pricing.

- Fee negotiation: AUM/volume

- Stickiness: platform + advisors

- Leverage: multi-bank links

- Pricing support: analytics

Low switching costs via digital

Digital account-opening and transfer tools have slashed friction, letting customers move deposits quickly; Ameris Bancorp reported about 32.6 billion in assets in 2024, increasing competitive pressure on margins. Buyers can diversify across institutions easily, making rewards and UX decisive; loyalty programs and embedded services are the main levers to raise switching costs.

- Frictionless onboarding

- Diversification ease

- Rewards/UX as differentiators

- Loyalty/embedded services raise costs

Depositors chase >4% APY; MMFs ~4.3% squeeze bank margins

Rate-sensitive depositors shift to >4% APY online; money market funds yield ~4.3% with $5.2T assets, tightening deposit betas. Commercial borrowers shop term sheets; speed, certainty and treasury bundles boost stickiness. Ameris assets ~$32.6B (2024); loyalty, analytics and platform breadth are primary levers to defend margins.

| Metric | 2024 value |

|---|---|

| Online savings APY | >4% |

| Money market yield / assets | ~4.3% / $5.2T |

| Digital close time | days |

| Ameris total assets | $32.6B |

What You See Is What You Get

Ameris Bank Porter's Five Forces Analysis

This preview shows the exact Ameris Bank Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the fully formatted, ready-to-use file covering bargaining power of suppliers and buyers, competitive rivalry, and threats of new entrants and substitutes. Upon payment you'll get instant access to this identical file for download and use.