AMG Porter's Five Forces Analysis

Don't Miss the Bigger Picture

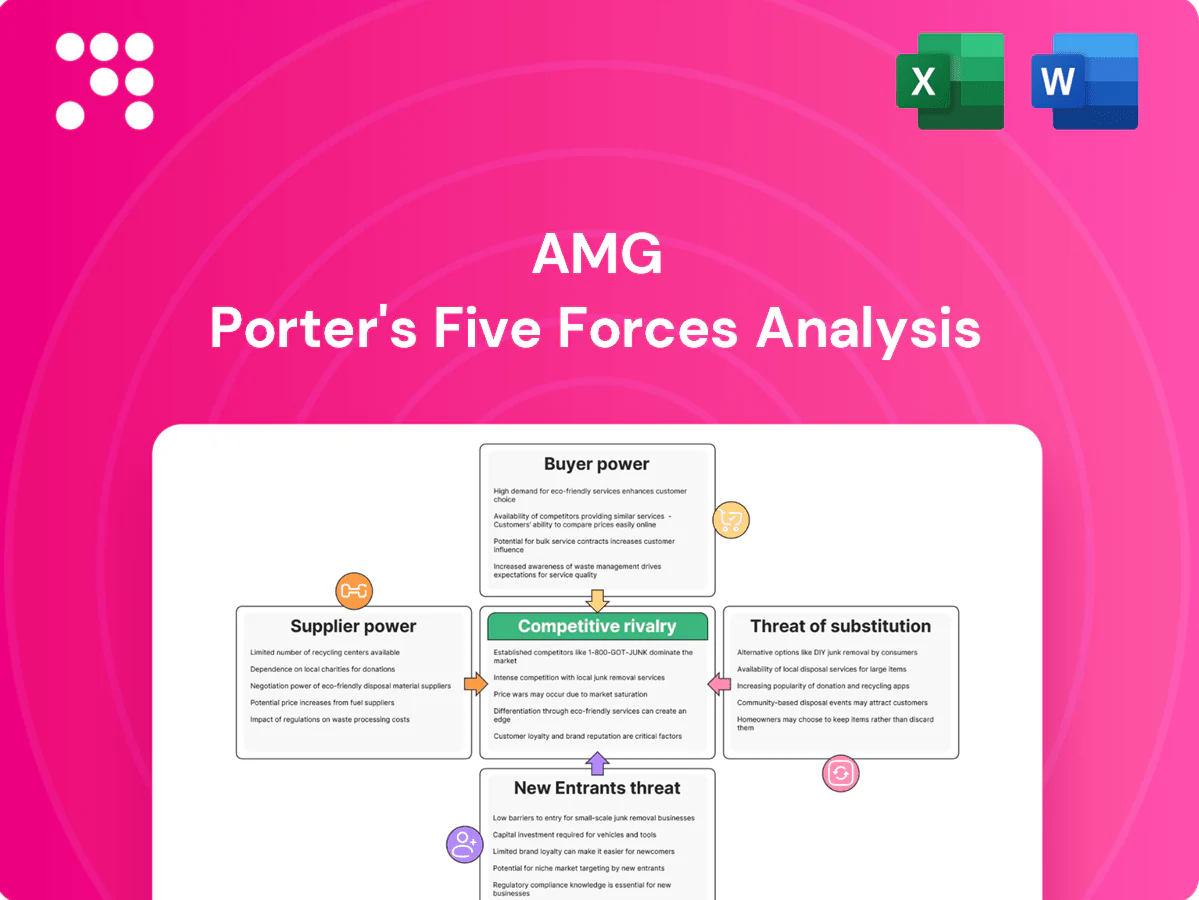

AMG’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, and substitute threats shaping its strategic outlook. This brief overview points to key vulnerabilities and opportunities but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AMG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Affiliate investment talent concentration

AMG’s core suppliers are its Affiliate portfolio managers and principals whose track records drive asset flows and fee rates; AMG reported roughly $763 billion AUM in 2024, underscoring the scale of talent-dependent flows. Scarce, high-performing managers can negotiate higher economics and autonomy. Retention packages and equity alignment reduce but do not remove this leverage. Performance cyclicality can rapidly reverse bargaining power.

Data, tech, and market infrastructure vendors

AMG and Affiliates depend on index licensors, market data, OMS/PMS, custodians and prime brokers, with Bloomberg reporting ~325,000 terminals in 2024 highlighting market-data concentration. Switching costs are moderate-to-high due to workflow integration and compliance, and vendor consolidation—top custodians holding a majority of global AUC in 2024—can boost pricing power, especially in niche analytics where fees rose materially in 2023–24. Multi-vendor strategies and scale contracts mitigate this.

Distribution platforms and intermediaries

Retail platforms, wirehouses and model marketplaces control shelf access, with the top 5 platforms holding roughly 60% of retail advisory distribution in 2024. Gatekeepers can impose platform fees, revenue shares (commonly 10–30%) and extensive due-diligence requirements. AMG’s multi-affiliate lineup and institutional brand strengthen negotiating leverage. Ongoing platform consolidation, however, is pushing take-rates and restrictive terms higher.

Regulatory and compliance dependencies

Regulators effectively supply licenses and cross-border approvals, and in 2024 firms reported compliance budgets rising roughly 8–12% as new liquidity, ESG disclosure and derivatives rules increased fixed costs and operational checks. Compliance vendors and law firms create supplier dependency; larger scale dilutes per-unit compliance spend but multiplies governance complexity.

- Regulatory approvals = gatekeepers

- Compliance spend +8–12% in 2024

- Vendors/legal = operational dependency

- Scale lowers unit cost, ups complexity

Capital and financing partners

For AMG’s acquisitions and seeding, cost of capital is decisive amid a 2024 policy rate backdrop of about 5.25–5.50%, so banks and private credit providers can tighten deal terms during credit stress. AMG’s public-company track record since 1997 and balance-sheet strength improve access and pricing, but market stress can quickly shift bargaining power back to capital providers.

- Cost of capital: higher rates raise hurdle rates for deals

- Capital providers: banks/private credit set tighter covenants in downturns

- AMG advantages: long public track record since 1997 and stronger balance sheet

- Risk: stressed markets increase lender leverage

Suppliers gain leverage over talent-driven $763B AUM and top-5 platforms ~60%

AMG’s suppliers—affiliate managers, data/vendors, platforms, custodians and capital providers—hold meaningful leverage given AMG’s talent-driven $763B AUM (2024) and vendor concentration (Bloomberg ~325,000 terminals, 2024). Top-5 retail platforms control ~60% distribution, and compliance costs rose ~8–12% in 2024, while 2024 policy rates ~5.25–5.50% tighten capital terms.

| Supplier | 2024 metric |

|---|---|

| Affiliate managers | $763B AUM |

| Market data | ~325,000 terminals |

| Platforms | Top-5 = ~60% |

| Compliance | +8–12% spend |

| Cost of capital | 5.25–5.50% policy rate |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and rivalry specific to AMG, highlighting disruptive threats, pricing leverage, and strategic defenses; fully editable for reports and decks.

AMG Porter's Five Forces delivers a one-sheet, visual summary with customizable pressure levels and radar chart to simplify strategic assessment and create slide-ready outputs—no macros or finance expertise needed.

Customers Bargaining Power

Institutional clients and consultants

Institutional clients—pensions, endowments and sovereigns—run competitive searches and consultants (advising on roughly 60–70% of large-plan searches) amplify bargaining power; global institutional AUM exceeds $100 trillion. Fee pressure persists via tiered schedules and performance gates, often shaving fees by tens of basis points. AMG’s specialist Affiliates and demonstrable alpha can defend pricing, but underperformance prompts swift reallocations.

High-net-worth and retail channels

Advisors and platforms increasingly pit managers on fees, performance and tax efficiency, with model portfolios and SMAs—used by roughly 60% of advisers in 2024—intensifying comparability and substitution; strong brand plus boutique expertise helps retention, but growing fee transparency amplifies buyer leverage, making distribution support and platform-level servicing vital to mitigate churn.

Shift toward passive and low-fee products

Buyers increasingly default to passive for core allocations—passive funds held over 50% of U.S. equity fund assets in 2024—so investors demand clear alpha or alternative exposures for active sleeves. This sharpens price sensitivity for traditional strategies. AMG’s alternatives and differentiated boutiques help justify fees. Yet blended portfolios set hard caps on aggregate active fee budgets.

Mandate concentration and ticket size

Fewer, larger mandates amplify customers' negotiating clout and push due-diligence intensity higher; in 2024 this dynamic drove more side letters and bespoke reporting requests that increase AMG's cost to serve. AMG benefits when Affiliates can deliver customized solutions, but mandate concentration heightens performance-continuity risk and operational exposure.

- Concentration: raises counterparty risk

- Custom requests: increase servicing costs

- Bespoke capability: competitive advantage

- Continuity: failure impact amplified

OCIOs and multi-asset allocators

OCIOs and multi-asset allocators consolidate decision-making and, in 2024, continued to compress manager fees while overseeing multi-billion dollar mandates; they can redeploy large allocations quickly across managers. AMG’s breadth across strategies helps deepen relationships and cross-sell, but OCIO bargaining leverage remains high given their scale and fee sensitivity.

- Scale reduces fees

- Rapid reallocation across managers

- AMG breadth strengthens ties

- OCIO leverage remains high

Institutional fee pressure: global AUM >$100T, consultants 60-70%

Institutional clients (global AUM >100T) and consultants (60–70% of large-plan searches) exert strong fee pressure, often cutting tens of bps; AMG’s boutiques and alternatives help defend pricing but underperformance triggers reallocations. Advisors using SMAs/model portfolios (~60% in 2024) and passive (>50% of US equity assets in 2024) heighten comparability and price sensitivity. Fewer, larger mandates and OCIOs speed reallocations and raise bespoke servicing costs, increasing bargaining leverage.

| Metric | 2024 Value |

|---|---|

| Global institutional AUM | >$100T |

| Consultant influence | 60–70% large-plan searches |

| Advisors using SMAs/models | ~60% |

| Passive US equity share | >50% |

What You See Is What You Get

AMG Porter's Five Forces Analysis

This preview shows the exact AMG Porter's Five Forces Analysis you'll receive after purchase—no placeholders or surprises. The document displayed is the full, professionally formatted analysis ready for immediate download and use the moment you buy. You’ll get instant access to this same file with all data, insights, and actionable recommendations intact.

Don't Miss the Bigger Picture

AMG’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, and substitute threats shaping its strategic outlook. This brief overview points to key vulnerabilities and opportunities but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AMG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Affiliate investment talent concentration

AMG’s core suppliers are its Affiliate portfolio managers and principals whose track records drive asset flows and fee rates; AMG reported roughly $763 billion AUM in 2024, underscoring the scale of talent-dependent flows. Scarce, high-performing managers can negotiate higher economics and autonomy. Retention packages and equity alignment reduce but do not remove this leverage. Performance cyclicality can rapidly reverse bargaining power.

Data, tech, and market infrastructure vendors

AMG and Affiliates depend on index licensors, market data, OMS/PMS, custodians and prime brokers, with Bloomberg reporting ~325,000 terminals in 2024 highlighting market-data concentration. Switching costs are moderate-to-high due to workflow integration and compliance, and vendor consolidation—top custodians holding a majority of global AUC in 2024—can boost pricing power, especially in niche analytics where fees rose materially in 2023–24. Multi-vendor strategies and scale contracts mitigate this.

Distribution platforms and intermediaries

Retail platforms, wirehouses and model marketplaces control shelf access, with the top 5 platforms holding roughly 60% of retail advisory distribution in 2024. Gatekeepers can impose platform fees, revenue shares (commonly 10–30%) and extensive due-diligence requirements. AMG’s multi-affiliate lineup and institutional brand strengthen negotiating leverage. Ongoing platform consolidation, however, is pushing take-rates and restrictive terms higher.

Regulatory and compliance dependencies

Regulators effectively supply licenses and cross-border approvals, and in 2024 firms reported compliance budgets rising roughly 8–12% as new liquidity, ESG disclosure and derivatives rules increased fixed costs and operational checks. Compliance vendors and law firms create supplier dependency; larger scale dilutes per-unit compliance spend but multiplies governance complexity.

- Regulatory approvals = gatekeepers

- Compliance spend +8–12% in 2024

- Vendors/legal = operational dependency

- Scale lowers unit cost, ups complexity

Capital and financing partners

For AMG’s acquisitions and seeding, cost of capital is decisive amid a 2024 policy rate backdrop of about 5.25–5.50%, so banks and private credit providers can tighten deal terms during credit stress. AMG’s public-company track record since 1997 and balance-sheet strength improve access and pricing, but market stress can quickly shift bargaining power back to capital providers.

- Cost of capital: higher rates raise hurdle rates for deals

- Capital providers: banks/private credit set tighter covenants in downturns

- AMG advantages: long public track record since 1997 and stronger balance sheet

- Risk: stressed markets increase lender leverage

Suppliers gain leverage over talent-driven $763B AUM and top-5 platforms ~60%

AMG’s suppliers—affiliate managers, data/vendors, platforms, custodians and capital providers—hold meaningful leverage given AMG’s talent-driven $763B AUM (2024) and vendor concentration (Bloomberg ~325,000 terminals, 2024). Top-5 retail platforms control ~60% distribution, and compliance costs rose ~8–12% in 2024, while 2024 policy rates ~5.25–5.50% tighten capital terms.

| Supplier | 2024 metric |

|---|---|

| Affiliate managers | $763B AUM |

| Market data | ~325,000 terminals |

| Platforms | Top-5 = ~60% |

| Compliance | +8–12% spend |

| Cost of capital | 5.25–5.50% policy rate |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and rivalry specific to AMG, highlighting disruptive threats, pricing leverage, and strategic defenses; fully editable for reports and decks.

AMG Porter's Five Forces delivers a one-sheet, visual summary with customizable pressure levels and radar chart to simplify strategic assessment and create slide-ready outputs—no macros or finance expertise needed.

Customers Bargaining Power

Institutional clients and consultants

Institutional clients—pensions, endowments and sovereigns—run competitive searches and consultants (advising on roughly 60–70% of large-plan searches) amplify bargaining power; global institutional AUM exceeds $100 trillion. Fee pressure persists via tiered schedules and performance gates, often shaving fees by tens of basis points. AMG’s specialist Affiliates and demonstrable alpha can defend pricing, but underperformance prompts swift reallocations.

High-net-worth and retail channels

Advisors and platforms increasingly pit managers on fees, performance and tax efficiency, with model portfolios and SMAs—used by roughly 60% of advisers in 2024—intensifying comparability and substitution; strong brand plus boutique expertise helps retention, but growing fee transparency amplifies buyer leverage, making distribution support and platform-level servicing vital to mitigate churn.

Shift toward passive and low-fee products

Buyers increasingly default to passive for core allocations—passive funds held over 50% of U.S. equity fund assets in 2024—so investors demand clear alpha or alternative exposures for active sleeves. This sharpens price sensitivity for traditional strategies. AMG’s alternatives and differentiated boutiques help justify fees. Yet blended portfolios set hard caps on aggregate active fee budgets.

Mandate concentration and ticket size

Fewer, larger mandates amplify customers' negotiating clout and push due-diligence intensity higher; in 2024 this dynamic drove more side letters and bespoke reporting requests that increase AMG's cost to serve. AMG benefits when Affiliates can deliver customized solutions, but mandate concentration heightens performance-continuity risk and operational exposure.

- Concentration: raises counterparty risk

- Custom requests: increase servicing costs

- Bespoke capability: competitive advantage

- Continuity: failure impact amplified

OCIOs and multi-asset allocators

OCIOs and multi-asset allocators consolidate decision-making and, in 2024, continued to compress manager fees while overseeing multi-billion dollar mandates; they can redeploy large allocations quickly across managers. AMG’s breadth across strategies helps deepen relationships and cross-sell, but OCIO bargaining leverage remains high given their scale and fee sensitivity.

- Scale reduces fees

- Rapid reallocation across managers

- AMG breadth strengthens ties

- OCIO leverage remains high

Institutional fee pressure: global AUM >$100T, consultants 60-70%

Institutional clients (global AUM >100T) and consultants (60–70% of large-plan searches) exert strong fee pressure, often cutting tens of bps; AMG’s boutiques and alternatives help defend pricing but underperformance triggers reallocations. Advisors using SMAs/model portfolios (~60% in 2024) and passive (>50% of US equity assets in 2024) heighten comparability and price sensitivity. Fewer, larger mandates and OCIOs speed reallocations and raise bespoke servicing costs, increasing bargaining leverage.

| Metric | 2024 Value |

|---|---|

| Global institutional AUM | >$100T |

| Consultant influence | 60–70% large-plan searches |

| Advisors using SMAs/models | ~60% |

| Passive US equity share | >50% |

What You See Is What You Get

AMG Porter's Five Forces Analysis

This preview shows the exact AMG Porter's Five Forces Analysis you'll receive after purchase—no placeholders or surprises. The document displayed is the full, professionally formatted analysis ready for immediate download and use the moment you buy. You’ll get instant access to this same file with all data, insights, and actionable recommendations intact.

Description

Don't Miss the Bigger Picture

AMG’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, and substitute threats shaping its strategic outlook. This brief overview points to key vulnerabilities and opportunities but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AMG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Affiliate investment talent concentration

AMG’s core suppliers are its Affiliate portfolio managers and principals whose track records drive asset flows and fee rates; AMG reported roughly $763 billion AUM in 2024, underscoring the scale of talent-dependent flows. Scarce, high-performing managers can negotiate higher economics and autonomy. Retention packages and equity alignment reduce but do not remove this leverage. Performance cyclicality can rapidly reverse bargaining power.

Data, tech, and market infrastructure vendors

AMG and Affiliates depend on index licensors, market data, OMS/PMS, custodians and prime brokers, with Bloomberg reporting ~325,000 terminals in 2024 highlighting market-data concentration. Switching costs are moderate-to-high due to workflow integration and compliance, and vendor consolidation—top custodians holding a majority of global AUC in 2024—can boost pricing power, especially in niche analytics where fees rose materially in 2023–24. Multi-vendor strategies and scale contracts mitigate this.

Distribution platforms and intermediaries

Retail platforms, wirehouses and model marketplaces control shelf access, with the top 5 platforms holding roughly 60% of retail advisory distribution in 2024. Gatekeepers can impose platform fees, revenue shares (commonly 10–30%) and extensive due-diligence requirements. AMG’s multi-affiliate lineup and institutional brand strengthen negotiating leverage. Ongoing platform consolidation, however, is pushing take-rates and restrictive terms higher.

Regulatory and compliance dependencies

Regulators effectively supply licenses and cross-border approvals, and in 2024 firms reported compliance budgets rising roughly 8–12% as new liquidity, ESG disclosure and derivatives rules increased fixed costs and operational checks. Compliance vendors and law firms create supplier dependency; larger scale dilutes per-unit compliance spend but multiplies governance complexity.

- Regulatory approvals = gatekeepers

- Compliance spend +8–12% in 2024

- Vendors/legal = operational dependency

- Scale lowers unit cost, ups complexity

Capital and financing partners

For AMG’s acquisitions and seeding, cost of capital is decisive amid a 2024 policy rate backdrop of about 5.25–5.50%, so banks and private credit providers can tighten deal terms during credit stress. AMG’s public-company track record since 1997 and balance-sheet strength improve access and pricing, but market stress can quickly shift bargaining power back to capital providers.

- Cost of capital: higher rates raise hurdle rates for deals

- Capital providers: banks/private credit set tighter covenants in downturns

- AMG advantages: long public track record since 1997 and stronger balance sheet

- Risk: stressed markets increase lender leverage

Suppliers gain leverage over talent-driven $763B AUM and top-5 platforms ~60%

AMG’s suppliers—affiliate managers, data/vendors, platforms, custodians and capital providers—hold meaningful leverage given AMG’s talent-driven $763B AUM (2024) and vendor concentration (Bloomberg ~325,000 terminals, 2024). Top-5 retail platforms control ~60% distribution, and compliance costs rose ~8–12% in 2024, while 2024 policy rates ~5.25–5.50% tighten capital terms.

| Supplier | 2024 metric |

|---|---|

| Affiliate managers | $763B AUM |

| Market data | ~325,000 terminals |

| Platforms | Top-5 = ~60% |

| Compliance | +8–12% spend |

| Cost of capital | 5.25–5.50% policy rate |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and rivalry specific to AMG, highlighting disruptive threats, pricing leverage, and strategic defenses; fully editable for reports and decks.

AMG Porter's Five Forces delivers a one-sheet, visual summary with customizable pressure levels and radar chart to simplify strategic assessment and create slide-ready outputs—no macros or finance expertise needed.

Customers Bargaining Power

Institutional clients and consultants

Institutional clients—pensions, endowments and sovereigns—run competitive searches and consultants (advising on roughly 60–70% of large-plan searches) amplify bargaining power; global institutional AUM exceeds $100 trillion. Fee pressure persists via tiered schedules and performance gates, often shaving fees by tens of basis points. AMG’s specialist Affiliates and demonstrable alpha can defend pricing, but underperformance prompts swift reallocations.

High-net-worth and retail channels

Advisors and platforms increasingly pit managers on fees, performance and tax efficiency, with model portfolios and SMAs—used by roughly 60% of advisers in 2024—intensifying comparability and substitution; strong brand plus boutique expertise helps retention, but growing fee transparency amplifies buyer leverage, making distribution support and platform-level servicing vital to mitigate churn.

Shift toward passive and low-fee products

Buyers increasingly default to passive for core allocations—passive funds held over 50% of U.S. equity fund assets in 2024—so investors demand clear alpha or alternative exposures for active sleeves. This sharpens price sensitivity for traditional strategies. AMG’s alternatives and differentiated boutiques help justify fees. Yet blended portfolios set hard caps on aggregate active fee budgets.

Mandate concentration and ticket size

Fewer, larger mandates amplify customers' negotiating clout and push due-diligence intensity higher; in 2024 this dynamic drove more side letters and bespoke reporting requests that increase AMG's cost to serve. AMG benefits when Affiliates can deliver customized solutions, but mandate concentration heightens performance-continuity risk and operational exposure.

- Concentration: raises counterparty risk

- Custom requests: increase servicing costs

- Bespoke capability: competitive advantage

- Continuity: failure impact amplified

OCIOs and multi-asset allocators

OCIOs and multi-asset allocators consolidate decision-making and, in 2024, continued to compress manager fees while overseeing multi-billion dollar mandates; they can redeploy large allocations quickly across managers. AMG’s breadth across strategies helps deepen relationships and cross-sell, but OCIO bargaining leverage remains high given their scale and fee sensitivity.

- Scale reduces fees

- Rapid reallocation across managers

- AMG breadth strengthens ties

- OCIO leverage remains high

Institutional fee pressure: global AUM >$100T, consultants 60-70%

Institutional clients (global AUM >100T) and consultants (60–70% of large-plan searches) exert strong fee pressure, often cutting tens of bps; AMG’s boutiques and alternatives help defend pricing but underperformance triggers reallocations. Advisors using SMAs/model portfolios (~60% in 2024) and passive (>50% of US equity assets in 2024) heighten comparability and price sensitivity. Fewer, larger mandates and OCIOs speed reallocations and raise bespoke servicing costs, increasing bargaining leverage.

| Metric | 2024 Value |

|---|---|

| Global institutional AUM | >$100T |

| Consultant influence | 60–70% large-plan searches |

| Advisors using SMAs/models | ~60% |

| Passive US equity share | >50% |

What You See Is What You Get

AMG Porter's Five Forces Analysis

This preview shows the exact AMG Porter's Five Forces Analysis you'll receive after purchase—no placeholders or surprises. The document displayed is the full, professionally formatted analysis ready for immediate download and use the moment you buy. You’ll get instant access to this same file with all data, insights, and actionable recommendations intact.