Amotiv SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Amotiv’s SWOT highlights innovative product strengths, niche market traction, and operational scalability alongside regulatory and competitive risks that could impact growth. Want the full strategic picture, financial context, and actionable recommendations? Purchase the complete SWOT to get an editable Word report and Excel matrix for planning and investment decisions.

Strengths

End-to-end mobility suite

Amotiv’s end-to-end mobility suite — fleet management, maintenance, repairs, sales and leasing — delivers a one-stop solution that simplifies vendor management, boosting client satisfaction and stickiness. Integrated services enable cross-selling and bundled pricing, increasing ARPU, while breadth cushions revenue through cycles; the global fleet management market was valued at about USD 34.2 billion in 2023, highlighting growth potential.

Recurring fleet revenues

Long-term fleet contracts generate predictable cash flows and higher utilization of service capacity, enabling multi-year planning and more accurate capex underwriting. Recurring revenues smooth demand volatility from retail cycles by converting one-off jobs into steady workstreams. This revenue visibility improves investor confidence and typically supports higher enterprise valuation multiples.

Tailored client solutions

Tailored client solutions align Amotiv offerings to sector-specific duty cycles, improving uptime and lowering TCO; industry studies show customization programs can cut downtime by ~20–30% and TCO by ~10–25% (2023–2024 maintenance analytics). Consultative selling raises switching costs, sharpens differentiation versus commoditized providers and—per recent B2B sales benchmarks—increases win rates by roughly 15–30% and strengthens referenceability.

Operational know-how

- Experience → higher first-time fix rates

- Standardization → lower warranty & rework

- Data-driven schedules → increased uptime

Cross-selling leverage

- Feed: new sales → recurring service

- Touchpoints: maintenance ≈ upsell moments

- Bundles: lower TCO, raise retention

- Result: higher LTV per account

Mobility suite boosts ARPU, stickiness; fleet market USD 34.2B

Integrated end-to-end mobility suite drives higher ARPU and stickiness; global fleet management market USD 34.2B (2023). Long-term contracts provide predictable, recurring cash flows; fleet parc >1.4B expands TAM. Data-driven maintenance (predictive cuts downtime up to 50%) raises uptime and lowers costs, while vehicle sales feed recurring service revenue, boosting LTV.

| Metric | 2023–24 |

|---|---|

| Market size | USD 34.2B |

| Global parc | 1.4B+ vehicles |

| Downtime ↓ | up to 50% |

What is included in the product

Provides a concise SWOT analysis of Amotiv, highlighting core strengths and weaknesses while mapping market opportunities and external threats to assess its competitive position and strategic risks.

Provides a focused Amotiv SWOT matrix that quickly highlights strengths, weaknesses, opportunities, and threats to pinpoint strategic pain points and prioritize corrective actions. Ideal for fast alignment across teams, easy integration into reports, and swift updates as priorities shift.

Weaknesses

Capital intensity

Leasing fleets, service equipment and facilities demand heavy upfront investment and recurring capex, tying up working capital that can strain liquidity; fleet operators often carry months of inventory and receivables. Depreciation risk is acute — first‑year vehicle depreciation commonly runs 20–30% and Manheim’s used‑vehicle index fell roughly 28% from its 2021 peak, amplifying residual‑value swings. This capital intensity increases sensitivity to credit conditions and funding spreads.

Operational complexity

Coordinating multi-line services raises scheduling and logistics complexity, increasing dispatch errors and overtime costs; McKinsey estimates digital operations can boost productivity 20–30%. Without standardization, complexity erodes margins and unit economics, while variability across sites risks inconsistent customer experience—research shows multi-site brands see up to 15% NPS variance. Governance overhead grows substantially as scale and compliance layers multiply.

Margin pressure

Maintenance and fleet services face intense price competition and RFP dynamics in a global MRO market ~82 billion USD in 2024, pressuring win rates and margins. Rising labor, parts and warranty costs—labor inflation around 6% YoY in 2023–24—compress gross margins, while customers increasingly demand transparent, performance‑based pricing; only scale benefits and ~20% higher utilization can meaningfully offset these pressures.

Supply dependence

Amotiv is highly dependent on OEMs and distributors for vehicle availability and parts; OEM lead times spiked past 20 weeks in 2021–22 and averaged about 6–8 weeks in 2024 (S&P Global), so shortages directly delay deliveries and create idle capacity. Supplier-driven price increases during disruptions compress margins and can shift pricing power to suppliers, harming SLA performance and client trust. Persistent supply volatility raises the risk of contract penalties and churn.

- Supply reliance: OEM/distributor bottlenecks

- Lead-time risk: 6–8 weeks avg in 2024

- Pricing risk: supplier leverage in disruptions

- Operational impact: idle capacity, SLA breaches, client churn

Technology investment needs

Modern fleet management demands telematics, analytics, and API integrations; the global fleet telematics market exceeded $20B in 2023 with double‑digit CAGR forecasts, making continuous upgrades costly. Specialized telematics and security engineers commonly command >$150k/year, and cybersecurity risk is material — IBM 2024 reports average data breach cost ~$4.45M — so lagging capabilities risk client churn.

- High capital expense: ongoing platform upgrades

- Talent cost: senior engineers >$150k/yr

- Cyber risk: avg breach cost ~$4.45M (IBM 2024)

- Market pressure: >$20B telematics market (2023)

Heavy capex, 20–30% first‑year depreciation and 6–8 weeks OEM delays squeeze margins

Heavy capex and rapid first‑year vehicle depreciation (20–30%) strain liquidity and elevate residual‑value risk (Manheim down ~28% from 2021 peak). Complex multi‑line operations raise scheduling costs and governance overhead, eroding margins amid ~6% labor inflation (2023–24). Supply and tech dependence—OEM lead times 6–8 weeks (2024) and telematics market >$20B (2023)—increase churn and cyber exposure (~$4.45M breach cost).

| Metric | Value |

|---|---|

| First‑yr depreciation | 20–30% |

| Used‑vehicle index move | −~28% vs 2021 peak |

| OEM lead time (2024) | 6–8 weeks |

| Telematics market (2023) | >$20B |

| Avg breach cost (IBM 2024) | $4.45M |

Same Document Delivered

Amotiv SWOT Analysis

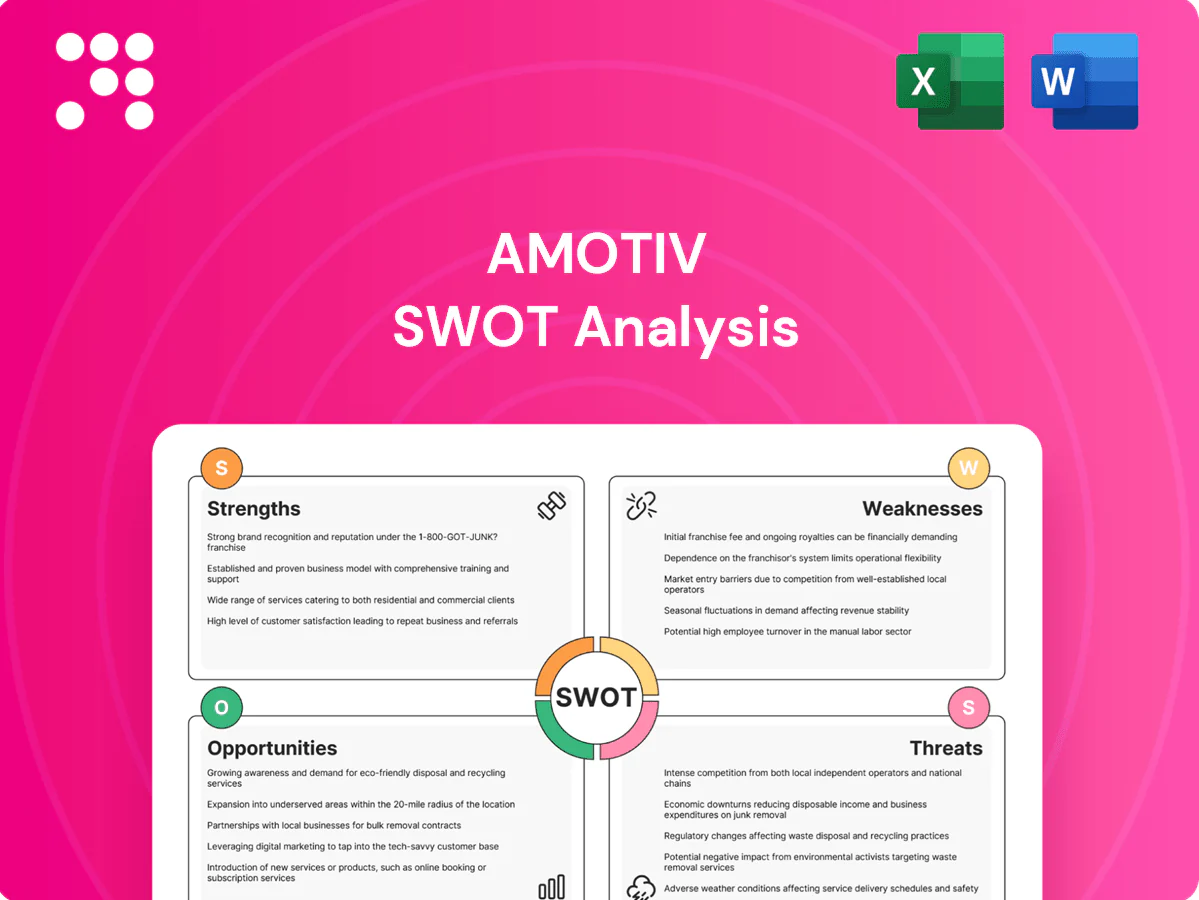

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version. The file shown is the real analysis you'll download after payment.

Dive Deeper Into the Company’s Strategic Blueprint

Amotiv’s SWOT highlights innovative product strengths, niche market traction, and operational scalability alongside regulatory and competitive risks that could impact growth. Want the full strategic picture, financial context, and actionable recommendations? Purchase the complete SWOT to get an editable Word report and Excel matrix for planning and investment decisions.

Strengths

End-to-end mobility suite

Amotiv’s end-to-end mobility suite — fleet management, maintenance, repairs, sales and leasing — delivers a one-stop solution that simplifies vendor management, boosting client satisfaction and stickiness. Integrated services enable cross-selling and bundled pricing, increasing ARPU, while breadth cushions revenue through cycles; the global fleet management market was valued at about USD 34.2 billion in 2023, highlighting growth potential.

Recurring fleet revenues

Long-term fleet contracts generate predictable cash flows and higher utilization of service capacity, enabling multi-year planning and more accurate capex underwriting. Recurring revenues smooth demand volatility from retail cycles by converting one-off jobs into steady workstreams. This revenue visibility improves investor confidence and typically supports higher enterprise valuation multiples.

Tailored client solutions

Tailored client solutions align Amotiv offerings to sector-specific duty cycles, improving uptime and lowering TCO; industry studies show customization programs can cut downtime by ~20–30% and TCO by ~10–25% (2023–2024 maintenance analytics). Consultative selling raises switching costs, sharpens differentiation versus commoditized providers and—per recent B2B sales benchmarks—increases win rates by roughly 15–30% and strengthens referenceability.

Operational know-how

- Experience → higher first-time fix rates

- Standardization → lower warranty & rework

- Data-driven schedules → increased uptime

Cross-selling leverage

- Feed: new sales → recurring service

- Touchpoints: maintenance ≈ upsell moments

- Bundles: lower TCO, raise retention

- Result: higher LTV per account

Mobility suite boosts ARPU, stickiness; fleet market USD 34.2B

Integrated end-to-end mobility suite drives higher ARPU and stickiness; global fleet management market USD 34.2B (2023). Long-term contracts provide predictable, recurring cash flows; fleet parc >1.4B expands TAM. Data-driven maintenance (predictive cuts downtime up to 50%) raises uptime and lowers costs, while vehicle sales feed recurring service revenue, boosting LTV.

| Metric | 2023–24 |

|---|---|

| Market size | USD 34.2B |

| Global parc | 1.4B+ vehicles |

| Downtime ↓ | up to 50% |

What is included in the product

Provides a concise SWOT analysis of Amotiv, highlighting core strengths and weaknesses while mapping market opportunities and external threats to assess its competitive position and strategic risks.

Provides a focused Amotiv SWOT matrix that quickly highlights strengths, weaknesses, opportunities, and threats to pinpoint strategic pain points and prioritize corrective actions. Ideal for fast alignment across teams, easy integration into reports, and swift updates as priorities shift.

Weaknesses

Capital intensity

Leasing fleets, service equipment and facilities demand heavy upfront investment and recurring capex, tying up working capital that can strain liquidity; fleet operators often carry months of inventory and receivables. Depreciation risk is acute — first‑year vehicle depreciation commonly runs 20–30% and Manheim’s used‑vehicle index fell roughly 28% from its 2021 peak, amplifying residual‑value swings. This capital intensity increases sensitivity to credit conditions and funding spreads.

Operational complexity

Coordinating multi-line services raises scheduling and logistics complexity, increasing dispatch errors and overtime costs; McKinsey estimates digital operations can boost productivity 20–30%. Without standardization, complexity erodes margins and unit economics, while variability across sites risks inconsistent customer experience—research shows multi-site brands see up to 15% NPS variance. Governance overhead grows substantially as scale and compliance layers multiply.

Margin pressure

Maintenance and fleet services face intense price competition and RFP dynamics in a global MRO market ~82 billion USD in 2024, pressuring win rates and margins. Rising labor, parts and warranty costs—labor inflation around 6% YoY in 2023–24—compress gross margins, while customers increasingly demand transparent, performance‑based pricing; only scale benefits and ~20% higher utilization can meaningfully offset these pressures.

Supply dependence

Amotiv is highly dependent on OEMs and distributors for vehicle availability and parts; OEM lead times spiked past 20 weeks in 2021–22 and averaged about 6–8 weeks in 2024 (S&P Global), so shortages directly delay deliveries and create idle capacity. Supplier-driven price increases during disruptions compress margins and can shift pricing power to suppliers, harming SLA performance and client trust. Persistent supply volatility raises the risk of contract penalties and churn.

- Supply reliance: OEM/distributor bottlenecks

- Lead-time risk: 6–8 weeks avg in 2024

- Pricing risk: supplier leverage in disruptions

- Operational impact: idle capacity, SLA breaches, client churn

Technology investment needs

Modern fleet management demands telematics, analytics, and API integrations; the global fleet telematics market exceeded $20B in 2023 with double‑digit CAGR forecasts, making continuous upgrades costly. Specialized telematics and security engineers commonly command >$150k/year, and cybersecurity risk is material — IBM 2024 reports average data breach cost ~$4.45M — so lagging capabilities risk client churn.

- High capital expense: ongoing platform upgrades

- Talent cost: senior engineers >$150k/yr

- Cyber risk: avg breach cost ~$4.45M (IBM 2024)

- Market pressure: >$20B telematics market (2023)

Heavy capex, 20–30% first‑year depreciation and 6–8 weeks OEM delays squeeze margins

Heavy capex and rapid first‑year vehicle depreciation (20–30%) strain liquidity and elevate residual‑value risk (Manheim down ~28% from 2021 peak). Complex multi‑line operations raise scheduling costs and governance overhead, eroding margins amid ~6% labor inflation (2023–24). Supply and tech dependence—OEM lead times 6–8 weeks (2024) and telematics market >$20B (2023)—increase churn and cyber exposure (~$4.45M breach cost).

| Metric | Value |

|---|---|

| First‑yr depreciation | 20–30% |

| Used‑vehicle index move | −~28% vs 2021 peak |

| OEM lead time (2024) | 6–8 weeks |

| Telematics market (2023) | >$20B |

| Avg breach cost (IBM 2024) | $4.45M |

Same Document Delivered

Amotiv SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version. The file shown is the real analysis you'll download after payment.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Amotiv’s SWOT highlights innovative product strengths, niche market traction, and operational scalability alongside regulatory and competitive risks that could impact growth. Want the full strategic picture, financial context, and actionable recommendations? Purchase the complete SWOT to get an editable Word report and Excel matrix for planning and investment decisions.

Strengths

End-to-end mobility suite

Amotiv’s end-to-end mobility suite — fleet management, maintenance, repairs, sales and leasing — delivers a one-stop solution that simplifies vendor management, boosting client satisfaction and stickiness. Integrated services enable cross-selling and bundled pricing, increasing ARPU, while breadth cushions revenue through cycles; the global fleet management market was valued at about USD 34.2 billion in 2023, highlighting growth potential.

Recurring fleet revenues

Long-term fleet contracts generate predictable cash flows and higher utilization of service capacity, enabling multi-year planning and more accurate capex underwriting. Recurring revenues smooth demand volatility from retail cycles by converting one-off jobs into steady workstreams. This revenue visibility improves investor confidence and typically supports higher enterprise valuation multiples.

Tailored client solutions

Tailored client solutions align Amotiv offerings to sector-specific duty cycles, improving uptime and lowering TCO; industry studies show customization programs can cut downtime by ~20–30% and TCO by ~10–25% (2023–2024 maintenance analytics). Consultative selling raises switching costs, sharpens differentiation versus commoditized providers and—per recent B2B sales benchmarks—increases win rates by roughly 15–30% and strengthens referenceability.

Operational know-how

- Experience → higher first-time fix rates

- Standardization → lower warranty & rework

- Data-driven schedules → increased uptime

Cross-selling leverage

- Feed: new sales → recurring service

- Touchpoints: maintenance ≈ upsell moments

- Bundles: lower TCO, raise retention

- Result: higher LTV per account

Mobility suite boosts ARPU, stickiness; fleet market USD 34.2B

Integrated end-to-end mobility suite drives higher ARPU and stickiness; global fleet management market USD 34.2B (2023). Long-term contracts provide predictable, recurring cash flows; fleet parc >1.4B expands TAM. Data-driven maintenance (predictive cuts downtime up to 50%) raises uptime and lowers costs, while vehicle sales feed recurring service revenue, boosting LTV.

| Metric | 2023–24 |

|---|---|

| Market size | USD 34.2B |

| Global parc | 1.4B+ vehicles |

| Downtime ↓ | up to 50% |

What is included in the product

Provides a concise SWOT analysis of Amotiv, highlighting core strengths and weaknesses while mapping market opportunities and external threats to assess its competitive position and strategic risks.

Provides a focused Amotiv SWOT matrix that quickly highlights strengths, weaknesses, opportunities, and threats to pinpoint strategic pain points and prioritize corrective actions. Ideal for fast alignment across teams, easy integration into reports, and swift updates as priorities shift.

Weaknesses

Capital intensity

Leasing fleets, service equipment and facilities demand heavy upfront investment and recurring capex, tying up working capital that can strain liquidity; fleet operators often carry months of inventory and receivables. Depreciation risk is acute — first‑year vehicle depreciation commonly runs 20–30% and Manheim’s used‑vehicle index fell roughly 28% from its 2021 peak, amplifying residual‑value swings. This capital intensity increases sensitivity to credit conditions and funding spreads.

Operational complexity

Coordinating multi-line services raises scheduling and logistics complexity, increasing dispatch errors and overtime costs; McKinsey estimates digital operations can boost productivity 20–30%. Without standardization, complexity erodes margins and unit economics, while variability across sites risks inconsistent customer experience—research shows multi-site brands see up to 15% NPS variance. Governance overhead grows substantially as scale and compliance layers multiply.

Margin pressure

Maintenance and fleet services face intense price competition and RFP dynamics in a global MRO market ~82 billion USD in 2024, pressuring win rates and margins. Rising labor, parts and warranty costs—labor inflation around 6% YoY in 2023–24—compress gross margins, while customers increasingly demand transparent, performance‑based pricing; only scale benefits and ~20% higher utilization can meaningfully offset these pressures.

Supply dependence

Amotiv is highly dependent on OEMs and distributors for vehicle availability and parts; OEM lead times spiked past 20 weeks in 2021–22 and averaged about 6–8 weeks in 2024 (S&P Global), so shortages directly delay deliveries and create idle capacity. Supplier-driven price increases during disruptions compress margins and can shift pricing power to suppliers, harming SLA performance and client trust. Persistent supply volatility raises the risk of contract penalties and churn.

- Supply reliance: OEM/distributor bottlenecks

- Lead-time risk: 6–8 weeks avg in 2024

- Pricing risk: supplier leverage in disruptions

- Operational impact: idle capacity, SLA breaches, client churn

Technology investment needs

Modern fleet management demands telematics, analytics, and API integrations; the global fleet telematics market exceeded $20B in 2023 with double‑digit CAGR forecasts, making continuous upgrades costly. Specialized telematics and security engineers commonly command >$150k/year, and cybersecurity risk is material — IBM 2024 reports average data breach cost ~$4.45M — so lagging capabilities risk client churn.

- High capital expense: ongoing platform upgrades

- Talent cost: senior engineers >$150k/yr

- Cyber risk: avg breach cost ~$4.45M (IBM 2024)

- Market pressure: >$20B telematics market (2023)

Heavy capex, 20–30% first‑year depreciation and 6–8 weeks OEM delays squeeze margins

Heavy capex and rapid first‑year vehicle depreciation (20–30%) strain liquidity and elevate residual‑value risk (Manheim down ~28% from 2021 peak). Complex multi‑line operations raise scheduling costs and governance overhead, eroding margins amid ~6% labor inflation (2023–24). Supply and tech dependence—OEM lead times 6–8 weeks (2024) and telematics market >$20B (2023)—increase churn and cyber exposure (~$4.45M breach cost).

| Metric | Value |

|---|---|

| First‑yr depreciation | 20–30% |

| Used‑vehicle index move | −~28% vs 2021 peak |

| OEM lead time (2024) | 6–8 weeks |

| Telematics market (2023) | >$20B |

| Avg breach cost (IBM 2024) | $4.45M |

Same Document Delivered

Amotiv SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version. The file shown is the real analysis you'll download after payment.