Amplify Energy SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Amplify Energy's SWOT snapshot highlights operational strengths, exposure to commodity cycles, and key regulatory risks shaping near-term outlook. Our full SWOT unpacks financial drivers, competitive positioning, and scenario-based risks with actionable strategies. Purchase the complete, editable report (Word + Excel) to plan, pitch, or invest with confidence.

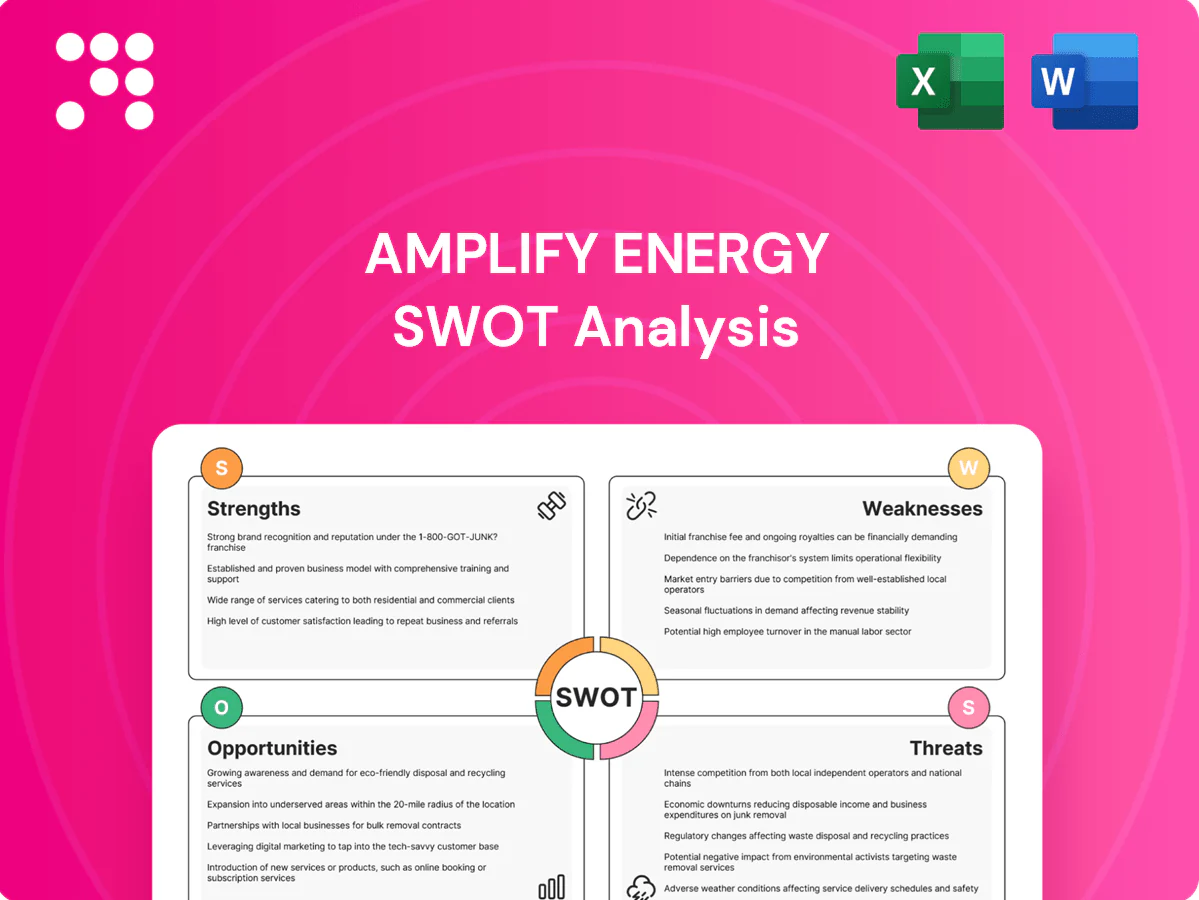

Strengths

Diversified mature asset base

Amplify Energy’s operations span four states—Oklahoma, Texas, Louisiana and California—reducing single-basin risk while leveraging known reservoirs; mature conventional fields lower geological uncertainty and support repeatable operations, underpinning steadier production profiles versus frontier exploration, and the geographic spread enables capital redeployment to highest-return projects as local conditions evolve.

Focus on operational efficiency

Amplify’s focus on squeezing value from legacy wells—via tight cost control, targeted workovers and production optimization—aims to lower lifting costs and downtime, historically boosting margins by double digits; with U.S. oil mid-cycle around $60–70/bbl, these gains can sustain free cash flow. Standardized procedures across similar conventional assets compound returns and improve resilient cash generation.

Acquisition and exploitation expertise

Amplify targets PDP-heavy assets where operational uplift and decline management create value, typically converting small capital into incremental barrels within 6–12 months. Its due diligence and integration experience uncovers overlooked upside in conventional reservoirs, improving recovery rates and near-term cash flow. Structured development plans prioritize quick-payback volumes, accelerating returns versus drilling-led growth.

Conventional reservoir predictability

Conventional reservoir predictability provides steadier decline profiles than ultra-tight plays, improving budgeting, hedging and maintenance planning; EIA 2023 notes conventional fields show markedly lower short-term output volatility. Predictable declines enable targeted recompletions and artificial lift upgrades, raising capital efficiency and planning accuracy for Amplify Energy.

- Lower output volatility

- Better hedging accuracy

- Higher ROI on recompletions

Cash flow from existing production

Amplify Energy's production assets generate immediate operating cash flow, which management has cited as supporting debt service and selective capital expenditures while enabling opportunistic asset buys. Lower exploration exposure reduces capital volatility and preserves liquidity. These steadier cash flows improve resilience through commodity cycles.

- Supports debt service

- Funds selective capex

- Enables opportunistic acquisitions

- Lower exploration risk, less cash volatility

Multi-state PDP oil portfolio: steady cash, quick paybacks at $60-70/bbl

Operations across four states (OK, TX, LA, CA) lower single-basin risk and leverage mature conventional reservoirs; PDP-heavy focus and rapid recompletions drive short paybacks and steady cash flow. Tight cost control and standardized ops reduce lifting costs, supporting debt service and opportunistic buys at mid-cycle oil $60–70/bbl (EIA 2023).

| Metric | Value |

|---|---|

| States | 4 |

| Asset type | Conventional/PDP-heavy |

| Mid-cycle oil | $60–70/bbl (EIA 2023) |

What is included in the product

Provides a concise strategic overview of Amplify Energy’s internal strengths and weaknesses and external opportunities and threats, highlighting operational capabilities, market position, growth drivers, and the regulatory, commodity-price, and environmental risks shaping its future.

Provides a concise, Amplify Energy–focused SWOT matrix for fast strategic alignment and stakeholder briefings, with editable elements to quickly reflect operational risks, market shifts, and capital constraints.

Weaknesses

Limited organic growth runway

Reliance on mature fields limits Amplify Energy’s organic growth absent acquisitions, since mature-asset programs rarely offset decline; shale/field decline rates of 60–70% first year underline the risk of falling volumes. Without sustained workovers and recompletions, production can trend flat-to-declining, raising per-unit costs as fixed overhead spreads over fewer barrels. Investors may demand higher yields to price in slower growth and elevated operational risk.

Legacy infrastructure intensity

Older Amplify Energy facilities demand higher maintenance and integrity management, a vulnerability highlighted by the 2021 Huntington Beach spill that released roughly 25,000 gallons of crude, underscoring repair and remediation exposure. Unexpected repairs can sharply increase operating costs and downtime, compressing margins. Aging assets raise HSE and reliability risks if not proactively managed, elevating sustaining capex requirements.

Smaller scale vs. peers

Smaller scale limits Amplify Energy's bargaining power with service providers and midstream, raising per-unit costs and making fixed-cost absorption harder when volumes fluctuate. Limited scale also makes access to low-cost capital more cyclical, especially with 10-year Treasury rates near 4.2% in mid-2025, widening spreads versus larger peers. Scale constraints slow portfolio-wide deployment of technology and efficiency gains, reducing resilience to price swings (WTI ~$80–85/bbl in 2024–H1 2025).

Exposure to regulatory complexity

Operating in California and multiple jurisdictions raises Amplify Energy's compliance burden, as permit timelines, emissions rules and detailed reporting can delay project starts and timelines. Sudden regulatory shifts may force capital reallocation or operational curtailments, while multi-state oversight elevates administrative and legal costs.

- Compliance delays: permits and emissions reporting

- Capex risk: reallocation or curtailment

- Higher admin/legal costs across states

High commodity sensitivity

Revenue and cash flow for Amplify Energy are highly tied to oil and gas price swings; WTI averaged about $77/bbl in 2024, so price drops quickly reduce topline and EBITDA. Limited hedges or hedges rolling off leave liquidity and planned capex exposed, while conventional assets can become margin-thin below breakeven points. Price volatility complicates multi-year planning and access to capital.

- WTI 2024 average ≈ $77/bbl — amplifies revenue sensitivity

- Hedge roll-off raises short-term liquidity risk

- Conventional asset margins compress at low prices

- Volatility hinders long-term capex and financing

Aging oil assets slash first-year output 60-70%, raising costs and HSE risks

Reliance on mature fields limits organic growth; first-year decline 60–70% and without workovers production falls, raising unit costs. Aging assets increase maintenance and HSE exposure (Huntington Beach spill ~25,000 gallons, 2021). Small scale raises per-unit costs and financing spreads as 10-year Treasury ≈4.2% mid-2025; WTI avg $77/bbl in 2024 heightens revenue sensitivity.

| Metric | Value |

|---|---|

| First-year decline | 60–70% |

| Huntington Beach spill | ~25,000 gallons (2021) |

| WTI (2024 avg) | $77/bbl |

| 10-yr Treasury (mid-2025) | ≈4.2% |

Full Version Awaits

Amplify Energy SWOT Analysis

This is the actual Amplify Energy SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content is ready to use and edit. Purchase unlocks the entire in-depth version immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Amplify Energy's SWOT snapshot highlights operational strengths, exposure to commodity cycles, and key regulatory risks shaping near-term outlook. Our full SWOT unpacks financial drivers, competitive positioning, and scenario-based risks with actionable strategies. Purchase the complete, editable report (Word + Excel) to plan, pitch, or invest with confidence.

Strengths

Diversified mature asset base

Amplify Energy’s operations span four states—Oklahoma, Texas, Louisiana and California—reducing single-basin risk while leveraging known reservoirs; mature conventional fields lower geological uncertainty and support repeatable operations, underpinning steadier production profiles versus frontier exploration, and the geographic spread enables capital redeployment to highest-return projects as local conditions evolve.

Focus on operational efficiency

Amplify’s focus on squeezing value from legacy wells—via tight cost control, targeted workovers and production optimization—aims to lower lifting costs and downtime, historically boosting margins by double digits; with U.S. oil mid-cycle around $60–70/bbl, these gains can sustain free cash flow. Standardized procedures across similar conventional assets compound returns and improve resilient cash generation.

Acquisition and exploitation expertise

Amplify targets PDP-heavy assets where operational uplift and decline management create value, typically converting small capital into incremental barrels within 6–12 months. Its due diligence and integration experience uncovers overlooked upside in conventional reservoirs, improving recovery rates and near-term cash flow. Structured development plans prioritize quick-payback volumes, accelerating returns versus drilling-led growth.

Conventional reservoir predictability

Conventional reservoir predictability provides steadier decline profiles than ultra-tight plays, improving budgeting, hedging and maintenance planning; EIA 2023 notes conventional fields show markedly lower short-term output volatility. Predictable declines enable targeted recompletions and artificial lift upgrades, raising capital efficiency and planning accuracy for Amplify Energy.

- Lower output volatility

- Better hedging accuracy

- Higher ROI on recompletions

Cash flow from existing production

Amplify Energy's production assets generate immediate operating cash flow, which management has cited as supporting debt service and selective capital expenditures while enabling opportunistic asset buys. Lower exploration exposure reduces capital volatility and preserves liquidity. These steadier cash flows improve resilience through commodity cycles.

- Supports debt service

- Funds selective capex

- Enables opportunistic acquisitions

- Lower exploration risk, less cash volatility

Multi-state PDP oil portfolio: steady cash, quick paybacks at $60-70/bbl

Operations across four states (OK, TX, LA, CA) lower single-basin risk and leverage mature conventional reservoirs; PDP-heavy focus and rapid recompletions drive short paybacks and steady cash flow. Tight cost control and standardized ops reduce lifting costs, supporting debt service and opportunistic buys at mid-cycle oil $60–70/bbl (EIA 2023).

| Metric | Value |

|---|---|

| States | 4 |

| Asset type | Conventional/PDP-heavy |

| Mid-cycle oil | $60–70/bbl (EIA 2023) |

What is included in the product

Provides a concise strategic overview of Amplify Energy’s internal strengths and weaknesses and external opportunities and threats, highlighting operational capabilities, market position, growth drivers, and the regulatory, commodity-price, and environmental risks shaping its future.

Provides a concise, Amplify Energy–focused SWOT matrix for fast strategic alignment and stakeholder briefings, with editable elements to quickly reflect operational risks, market shifts, and capital constraints.

Weaknesses

Limited organic growth runway

Reliance on mature fields limits Amplify Energy’s organic growth absent acquisitions, since mature-asset programs rarely offset decline; shale/field decline rates of 60–70% first year underline the risk of falling volumes. Without sustained workovers and recompletions, production can trend flat-to-declining, raising per-unit costs as fixed overhead spreads over fewer barrels. Investors may demand higher yields to price in slower growth and elevated operational risk.

Legacy infrastructure intensity

Older Amplify Energy facilities demand higher maintenance and integrity management, a vulnerability highlighted by the 2021 Huntington Beach spill that released roughly 25,000 gallons of crude, underscoring repair and remediation exposure. Unexpected repairs can sharply increase operating costs and downtime, compressing margins. Aging assets raise HSE and reliability risks if not proactively managed, elevating sustaining capex requirements.

Smaller scale vs. peers

Smaller scale limits Amplify Energy's bargaining power with service providers and midstream, raising per-unit costs and making fixed-cost absorption harder when volumes fluctuate. Limited scale also makes access to low-cost capital more cyclical, especially with 10-year Treasury rates near 4.2% in mid-2025, widening spreads versus larger peers. Scale constraints slow portfolio-wide deployment of technology and efficiency gains, reducing resilience to price swings (WTI ~$80–85/bbl in 2024–H1 2025).

Exposure to regulatory complexity

Operating in California and multiple jurisdictions raises Amplify Energy's compliance burden, as permit timelines, emissions rules and detailed reporting can delay project starts and timelines. Sudden regulatory shifts may force capital reallocation or operational curtailments, while multi-state oversight elevates administrative and legal costs.

- Compliance delays: permits and emissions reporting

- Capex risk: reallocation or curtailment

- Higher admin/legal costs across states

High commodity sensitivity

Revenue and cash flow for Amplify Energy are highly tied to oil and gas price swings; WTI averaged about $77/bbl in 2024, so price drops quickly reduce topline and EBITDA. Limited hedges or hedges rolling off leave liquidity and planned capex exposed, while conventional assets can become margin-thin below breakeven points. Price volatility complicates multi-year planning and access to capital.

- WTI 2024 average ≈ $77/bbl — amplifies revenue sensitivity

- Hedge roll-off raises short-term liquidity risk

- Conventional asset margins compress at low prices

- Volatility hinders long-term capex and financing

Aging oil assets slash first-year output 60-70%, raising costs and HSE risks

Reliance on mature fields limits organic growth; first-year decline 60–70% and without workovers production falls, raising unit costs. Aging assets increase maintenance and HSE exposure (Huntington Beach spill ~25,000 gallons, 2021). Small scale raises per-unit costs and financing spreads as 10-year Treasury ≈4.2% mid-2025; WTI avg $77/bbl in 2024 heightens revenue sensitivity.

| Metric | Value |

|---|---|

| First-year decline | 60–70% |

| Huntington Beach spill | ~25,000 gallons (2021) |

| WTI (2024 avg) | $77/bbl |

| 10-yr Treasury (mid-2025) | ≈4.2% |

Full Version Awaits

Amplify Energy SWOT Analysis

This is the actual Amplify Energy SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content is ready to use and edit. Purchase unlocks the entire in-depth version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Amplify Energy's SWOT snapshot highlights operational strengths, exposure to commodity cycles, and key regulatory risks shaping near-term outlook. Our full SWOT unpacks financial drivers, competitive positioning, and scenario-based risks with actionable strategies. Purchase the complete, editable report (Word + Excel) to plan, pitch, or invest with confidence.

Strengths

Diversified mature asset base

Amplify Energy’s operations span four states—Oklahoma, Texas, Louisiana and California—reducing single-basin risk while leveraging known reservoirs; mature conventional fields lower geological uncertainty and support repeatable operations, underpinning steadier production profiles versus frontier exploration, and the geographic spread enables capital redeployment to highest-return projects as local conditions evolve.

Focus on operational efficiency

Amplify’s focus on squeezing value from legacy wells—via tight cost control, targeted workovers and production optimization—aims to lower lifting costs and downtime, historically boosting margins by double digits; with U.S. oil mid-cycle around $60–70/bbl, these gains can sustain free cash flow. Standardized procedures across similar conventional assets compound returns and improve resilient cash generation.

Acquisition and exploitation expertise

Amplify targets PDP-heavy assets where operational uplift and decline management create value, typically converting small capital into incremental barrels within 6–12 months. Its due diligence and integration experience uncovers overlooked upside in conventional reservoirs, improving recovery rates and near-term cash flow. Structured development plans prioritize quick-payback volumes, accelerating returns versus drilling-led growth.

Conventional reservoir predictability

Conventional reservoir predictability provides steadier decline profiles than ultra-tight plays, improving budgeting, hedging and maintenance planning; EIA 2023 notes conventional fields show markedly lower short-term output volatility. Predictable declines enable targeted recompletions and artificial lift upgrades, raising capital efficiency and planning accuracy for Amplify Energy.

- Lower output volatility

- Better hedging accuracy

- Higher ROI on recompletions

Cash flow from existing production

Amplify Energy's production assets generate immediate operating cash flow, which management has cited as supporting debt service and selective capital expenditures while enabling opportunistic asset buys. Lower exploration exposure reduces capital volatility and preserves liquidity. These steadier cash flows improve resilience through commodity cycles.

- Supports debt service

- Funds selective capex

- Enables opportunistic acquisitions

- Lower exploration risk, less cash volatility

Multi-state PDP oil portfolio: steady cash, quick paybacks at $60-70/bbl

Operations across four states (OK, TX, LA, CA) lower single-basin risk and leverage mature conventional reservoirs; PDP-heavy focus and rapid recompletions drive short paybacks and steady cash flow. Tight cost control and standardized ops reduce lifting costs, supporting debt service and opportunistic buys at mid-cycle oil $60–70/bbl (EIA 2023).

| Metric | Value |

|---|---|

| States | 4 |

| Asset type | Conventional/PDP-heavy |

| Mid-cycle oil | $60–70/bbl (EIA 2023) |

What is included in the product

Provides a concise strategic overview of Amplify Energy’s internal strengths and weaknesses and external opportunities and threats, highlighting operational capabilities, market position, growth drivers, and the regulatory, commodity-price, and environmental risks shaping its future.

Provides a concise, Amplify Energy–focused SWOT matrix for fast strategic alignment and stakeholder briefings, with editable elements to quickly reflect operational risks, market shifts, and capital constraints.

Weaknesses

Limited organic growth runway

Reliance on mature fields limits Amplify Energy’s organic growth absent acquisitions, since mature-asset programs rarely offset decline; shale/field decline rates of 60–70% first year underline the risk of falling volumes. Without sustained workovers and recompletions, production can trend flat-to-declining, raising per-unit costs as fixed overhead spreads over fewer barrels. Investors may demand higher yields to price in slower growth and elevated operational risk.

Legacy infrastructure intensity

Older Amplify Energy facilities demand higher maintenance and integrity management, a vulnerability highlighted by the 2021 Huntington Beach spill that released roughly 25,000 gallons of crude, underscoring repair and remediation exposure. Unexpected repairs can sharply increase operating costs and downtime, compressing margins. Aging assets raise HSE and reliability risks if not proactively managed, elevating sustaining capex requirements.

Smaller scale vs. peers

Smaller scale limits Amplify Energy's bargaining power with service providers and midstream, raising per-unit costs and making fixed-cost absorption harder when volumes fluctuate. Limited scale also makes access to low-cost capital more cyclical, especially with 10-year Treasury rates near 4.2% in mid-2025, widening spreads versus larger peers. Scale constraints slow portfolio-wide deployment of technology and efficiency gains, reducing resilience to price swings (WTI ~$80–85/bbl in 2024–H1 2025).

Exposure to regulatory complexity

Operating in California and multiple jurisdictions raises Amplify Energy's compliance burden, as permit timelines, emissions rules and detailed reporting can delay project starts and timelines. Sudden regulatory shifts may force capital reallocation or operational curtailments, while multi-state oversight elevates administrative and legal costs.

- Compliance delays: permits and emissions reporting

- Capex risk: reallocation or curtailment

- Higher admin/legal costs across states

High commodity sensitivity

Revenue and cash flow for Amplify Energy are highly tied to oil and gas price swings; WTI averaged about $77/bbl in 2024, so price drops quickly reduce topline and EBITDA. Limited hedges or hedges rolling off leave liquidity and planned capex exposed, while conventional assets can become margin-thin below breakeven points. Price volatility complicates multi-year planning and access to capital.

- WTI 2024 average ≈ $77/bbl — amplifies revenue sensitivity

- Hedge roll-off raises short-term liquidity risk

- Conventional asset margins compress at low prices

- Volatility hinders long-term capex and financing

Aging oil assets slash first-year output 60-70%, raising costs and HSE risks

Reliance on mature fields limits organic growth; first-year decline 60–70% and without workovers production falls, raising unit costs. Aging assets increase maintenance and HSE exposure (Huntington Beach spill ~25,000 gallons, 2021). Small scale raises per-unit costs and financing spreads as 10-year Treasury ≈4.2% mid-2025; WTI avg $77/bbl in 2024 heightens revenue sensitivity.

| Metric | Value |

|---|---|

| First-year decline | 60–70% |

| Huntington Beach spill | ~25,000 gallons (2021) |

| WTI (2024 avg) | $77/bbl |

| 10-yr Treasury (mid-2025) | ≈4.2% |

Full Version Awaits

Amplify Energy SWOT Analysis

This is the actual Amplify Energy SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content is ready to use and edit. Purchase unlocks the entire in-depth version immediately after checkout.