Ampol Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

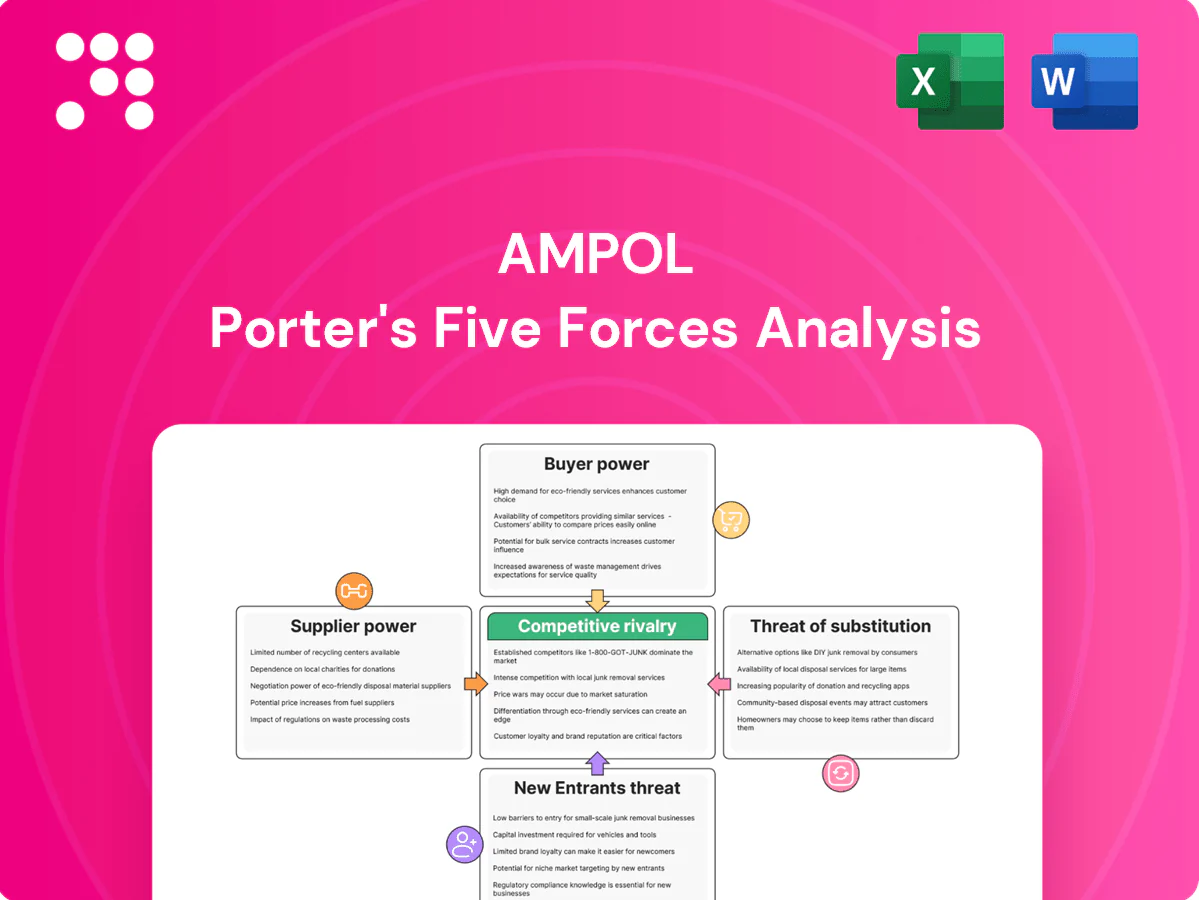

Ampol navigates intense supplier negotiation, evolving buyer expectations, and growing low‑carbon substitutes while industry scale and regulatory barriers temper new entrants and rivalry. This snapshot highlights key tensions shaping margins and strategy. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for force‑by‑force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated crude and product sources

Upstream supply is concentrated: OPEC+ and major trading houses accounted for about 40% of global crude supply in 2024, limiting Ampol’s bargaining leverage on price and terms. Domestic Australian crude production is modest at roughly 1.0 million barrels per day (2023), forcing higher import dependence for feedstock. Geopolitical moves or cartel decisions transmit rapidly into refining margins and input costs. Ampol hedges and diversifies cargo sources, but structural concentration remains.

Refining inputs and spec compliance

Meeting Australian fuel standards — diesel sulfur capped at 10 ppm and petrol typically 91 RON minimum — narrows acceptable feedstocks and components. Specialty additives and lubricant packages come from a small set of global majors such as Infineum, Afton, BASF and Chevron Oronite, raising switching costs and delay risks and giving niche suppliers modest pricing power in tight 2024 markets.

Logistics and terminal capacity constraints

Jetty slots, storage and pipeline access in Australia are regionally concentrated, creating chokepoints that give infrastructure owners outsized leverage over suppliers and refiners like Ampol.

Disruptions at key terminals or shipping lanes rapidly tighten supply and have historically transmitted higher freight and demurrage into landed fuel costs.

Control of critical terminals and pipeline access by a small number of operators therefore elevates supplier bargaining power and pass-through risk to margins.

Currency and commodity volatility

Ampol buys crude and refined product priced in USD while retail sales are predominantly in AUD, leaving margins sensitive to AUD/USD swings; recent 2024 FX volatility increased supplier leverage during tightening cycles. Oil price swings in 2024 compressed and widened supplier pricing power over short periods; hedging reduces but cannot remove basis risk, forcing quicker retail price resets to defend unit economics.

- USD procurement vs AUD sales — FX exposure

- 2024 oil volatility amplified short-cycle supplier power

- Hedging mitigates, not eliminates, basis risk

- Price spikes trigger faster retail resets

Emerging new energy inputs

Supply of renewable diesel, SAF, hydrogen and high-quality bio-components is nascent and tight, and early-stage markets in 2024 still favor suppliers with scarce certified capacity; SAF production remains under 0.1% of global jet fuel demand (industry estimates), boosting supplier leverage. Long-term offtake deals secure volumes but command premium pricing, temporarily heightening supplier power in Ampol’s energy transition.

- Nascent supply: certified capacity scarce

- 2024 SAF <0.1% of jet fuel demand

- Offtake = volume security at premium

OPEC+ 40% grip and FX swings squeeze Aus fuel margins; SAF 0.1% remains tiny

Upstream concentration (OPEC+ ~40% of supply in 2024) and Australia crude ~1.0 mbpd (2023) limit Ampol’s price leverage; specialty additive suppliers and terminal owners retain niche pricing power. FX exposure (USD procurement vs AUD sales) and 2024 oil volatility amplify pass-through risk. SAF <0.1% global jet demand (2024) keeps renewable feedstocks premium-priced.

| Metric | Value |

|---|---|

| OPEC+ share (2024) | ~40% |

| AUS crude prod (2023) | ~1.0 mbpd |

| Diesel sulfur | 10 ppm |

| SAF global share (2024) | <0.1% |

| Key additive suppliers | Infineum, Afton, BASF, Chevron Oronite |

What is included in the product

Tailored Porter's Five Forces analysis for Ampol uncovering competitive drivers, supplier and buyer power, and barriers to entry that shape profitability. Identifies substitutes, disruptive threats, and strategic levers Ampol can use to protect market share and optimize pricing.

A clear, one-sheet Porter's Five Forces summary for Ampol—instantly highlights supplier, buyer, competitor, substitute and entry pressures to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Retail buyers with low switching costs

Motorists can switch stations easily based on price boards and proximity, and with Ampol operating over 1,900 retail sites in 2024 this creates constant local competition. Apps and price-comparison tools have raised transparency, enabling rapid detection of undercutting. Loyalty programs and convenience offers partially dampen churn but do not eliminate it. Net effect: high day-to-day buyer power on pump pricing.

Large B2B contracts exert leverage

Mining, aviation and marine customers buy at scale via tenders—contracts frequently exceed 1 million liters/year and span multi-year terms, driving negotiated discounts and strict SLAs. Volume commitments in 2024 pushed average contract discounts of around 3–6% in commoditized grades. Buyers can dual-source between Ampol, BP, Viva and independents, giving them high bargaining power, especially on standard diesel and jet-A.

Price elasticity and discount cycles

Frequent discounting in metro markets conditions buyers to wait for troughs, with weekly price swings often reaching ~10c/L in 2024, prompting timing behavior. Small price gaps (5–10c/L) can drive meaningful volume swings of roughly 3–5%, transferring pricing pressure to Ampol. With ~1,900 retail sites, Ampol must use dynamic pricing and localized promotions to defend margins and manage traffic flow.

Bundled convenience expectations

- Value drivers: food, coffee, parcels

- Cross-sell lowers fuel price elasticity

- Weak convenience = higher buyer power

- Ampol scale ~1,900 sites (2024)

Sustainability and fuel spec preferences

Corporate fleets increasingly demand lower-carbon fuels and transparent reporting; Ampol states net-zero by 2050, pushing buyers to ask for bio-blends, SAF or offsets and narrowing supplier options. Buyers can shift compliance costs back to suppliers, raising margin pressure and contracting leverage. IATA targets 10% SAF by 2030, giving sophisticated buyers extra negotiating power during the transition.

- Corporate mandates raise demand for bio-blends/SAF

- Compliance costs often shifted to suppliers

- Narrowed supplier pool increases buyer leverage

- IATA 10% SAF by 2030 strengthens buyer bargaining

High retail churn, ~1,900 sites; contracts 3-6% off; weekly swings ~10c/L

High retail churn due to price transparency; Ampol ~1,900 sites (2024). Commercial tenders drive 3–6% contract discounts; weekly metro price swings ~10c/L causing 3–5% volume shifts. Corporate demand for SAF/bio-blends (IATA 10% SAF by 2030) raises supplier leverage.

| Metric | 2024 |

|---|---|

| Retail sites | ~1,900 |

| Contract discounts | 3–6% |

| Weekly price swing | ~10c/L |

| Volume sensitivity | 3–5% |

Full Version Awaits

Ampol Porter's Five Forces Analysis

This preview shows the exact Ampol Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted, ready to download and use immediately, providing the same detailed industry, competitor, supplier, buyer, and threat assessments you see here.

Go Beyond the Preview—Access the Full Strategic Report

Ampol navigates intense supplier negotiation, evolving buyer expectations, and growing low‑carbon substitutes while industry scale and regulatory barriers temper new entrants and rivalry. This snapshot highlights key tensions shaping margins and strategy. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for force‑by‑force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated crude and product sources

Upstream supply is concentrated: OPEC+ and major trading houses accounted for about 40% of global crude supply in 2024, limiting Ampol’s bargaining leverage on price and terms. Domestic Australian crude production is modest at roughly 1.0 million barrels per day (2023), forcing higher import dependence for feedstock. Geopolitical moves or cartel decisions transmit rapidly into refining margins and input costs. Ampol hedges and diversifies cargo sources, but structural concentration remains.

Refining inputs and spec compliance

Meeting Australian fuel standards — diesel sulfur capped at 10 ppm and petrol typically 91 RON minimum — narrows acceptable feedstocks and components. Specialty additives and lubricant packages come from a small set of global majors such as Infineum, Afton, BASF and Chevron Oronite, raising switching costs and delay risks and giving niche suppliers modest pricing power in tight 2024 markets.

Logistics and terminal capacity constraints

Jetty slots, storage and pipeline access in Australia are regionally concentrated, creating chokepoints that give infrastructure owners outsized leverage over suppliers and refiners like Ampol.

Disruptions at key terminals or shipping lanes rapidly tighten supply and have historically transmitted higher freight and demurrage into landed fuel costs.

Control of critical terminals and pipeline access by a small number of operators therefore elevates supplier bargaining power and pass-through risk to margins.

Currency and commodity volatility

Ampol buys crude and refined product priced in USD while retail sales are predominantly in AUD, leaving margins sensitive to AUD/USD swings; recent 2024 FX volatility increased supplier leverage during tightening cycles. Oil price swings in 2024 compressed and widened supplier pricing power over short periods; hedging reduces but cannot remove basis risk, forcing quicker retail price resets to defend unit economics.

- USD procurement vs AUD sales — FX exposure

- 2024 oil volatility amplified short-cycle supplier power

- Hedging mitigates, not eliminates, basis risk

- Price spikes trigger faster retail resets

Emerging new energy inputs

Supply of renewable diesel, SAF, hydrogen and high-quality bio-components is nascent and tight, and early-stage markets in 2024 still favor suppliers with scarce certified capacity; SAF production remains under 0.1% of global jet fuel demand (industry estimates), boosting supplier leverage. Long-term offtake deals secure volumes but command premium pricing, temporarily heightening supplier power in Ampol’s energy transition.

- Nascent supply: certified capacity scarce

- 2024 SAF <0.1% of jet fuel demand

- Offtake = volume security at premium

OPEC+ 40% grip and FX swings squeeze Aus fuel margins; SAF 0.1% remains tiny

Upstream concentration (OPEC+ ~40% of supply in 2024) and Australia crude ~1.0 mbpd (2023) limit Ampol’s price leverage; specialty additive suppliers and terminal owners retain niche pricing power. FX exposure (USD procurement vs AUD sales) and 2024 oil volatility amplify pass-through risk. SAF <0.1% global jet demand (2024) keeps renewable feedstocks premium-priced.

| Metric | Value |

|---|---|

| OPEC+ share (2024) | ~40% |

| AUS crude prod (2023) | ~1.0 mbpd |

| Diesel sulfur | 10 ppm |

| SAF global share (2024) | <0.1% |

| Key additive suppliers | Infineum, Afton, BASF, Chevron Oronite |

What is included in the product

Tailored Porter's Five Forces analysis for Ampol uncovering competitive drivers, supplier and buyer power, and barriers to entry that shape profitability. Identifies substitutes, disruptive threats, and strategic levers Ampol can use to protect market share and optimize pricing.

A clear, one-sheet Porter's Five Forces summary for Ampol—instantly highlights supplier, buyer, competitor, substitute and entry pressures to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Retail buyers with low switching costs

Motorists can switch stations easily based on price boards and proximity, and with Ampol operating over 1,900 retail sites in 2024 this creates constant local competition. Apps and price-comparison tools have raised transparency, enabling rapid detection of undercutting. Loyalty programs and convenience offers partially dampen churn but do not eliminate it. Net effect: high day-to-day buyer power on pump pricing.

Large B2B contracts exert leverage

Mining, aviation and marine customers buy at scale via tenders—contracts frequently exceed 1 million liters/year and span multi-year terms, driving negotiated discounts and strict SLAs. Volume commitments in 2024 pushed average contract discounts of around 3–6% in commoditized grades. Buyers can dual-source between Ampol, BP, Viva and independents, giving them high bargaining power, especially on standard diesel and jet-A.

Price elasticity and discount cycles

Frequent discounting in metro markets conditions buyers to wait for troughs, with weekly price swings often reaching ~10c/L in 2024, prompting timing behavior. Small price gaps (5–10c/L) can drive meaningful volume swings of roughly 3–5%, transferring pricing pressure to Ampol. With ~1,900 retail sites, Ampol must use dynamic pricing and localized promotions to defend margins and manage traffic flow.

Bundled convenience expectations

- Value drivers: food, coffee, parcels

- Cross-sell lowers fuel price elasticity

- Weak convenience = higher buyer power

- Ampol scale ~1,900 sites (2024)

Sustainability and fuel spec preferences

Corporate fleets increasingly demand lower-carbon fuels and transparent reporting; Ampol states net-zero by 2050, pushing buyers to ask for bio-blends, SAF or offsets and narrowing supplier options. Buyers can shift compliance costs back to suppliers, raising margin pressure and contracting leverage. IATA targets 10% SAF by 2030, giving sophisticated buyers extra negotiating power during the transition.

- Corporate mandates raise demand for bio-blends/SAF

- Compliance costs often shifted to suppliers

- Narrowed supplier pool increases buyer leverage

- IATA 10% SAF by 2030 strengthens buyer bargaining

High retail churn, ~1,900 sites; contracts 3-6% off; weekly swings ~10c/L

High retail churn due to price transparency; Ampol ~1,900 sites (2024). Commercial tenders drive 3–6% contract discounts; weekly metro price swings ~10c/L causing 3–5% volume shifts. Corporate demand for SAF/bio-blends (IATA 10% SAF by 2030) raises supplier leverage.

| Metric | 2024 |

|---|---|

| Retail sites | ~1,900 |

| Contract discounts | 3–6% |

| Weekly price swing | ~10c/L |

| Volume sensitivity | 3–5% |

Full Version Awaits

Ampol Porter's Five Forces Analysis

This preview shows the exact Ampol Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted, ready to download and use immediately, providing the same detailed industry, competitor, supplier, buyer, and threat assessments you see here.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Ampol navigates intense supplier negotiation, evolving buyer expectations, and growing low‑carbon substitutes while industry scale and regulatory barriers temper new entrants and rivalry. This snapshot highlights key tensions shaping margins and strategy. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for force‑by‑force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated crude and product sources

Upstream supply is concentrated: OPEC+ and major trading houses accounted for about 40% of global crude supply in 2024, limiting Ampol’s bargaining leverage on price and terms. Domestic Australian crude production is modest at roughly 1.0 million barrels per day (2023), forcing higher import dependence for feedstock. Geopolitical moves or cartel decisions transmit rapidly into refining margins and input costs. Ampol hedges and diversifies cargo sources, but structural concentration remains.

Refining inputs and spec compliance

Meeting Australian fuel standards — diesel sulfur capped at 10 ppm and petrol typically 91 RON minimum — narrows acceptable feedstocks and components. Specialty additives and lubricant packages come from a small set of global majors such as Infineum, Afton, BASF and Chevron Oronite, raising switching costs and delay risks and giving niche suppliers modest pricing power in tight 2024 markets.

Logistics and terminal capacity constraints

Jetty slots, storage and pipeline access in Australia are regionally concentrated, creating chokepoints that give infrastructure owners outsized leverage over suppliers and refiners like Ampol.

Disruptions at key terminals or shipping lanes rapidly tighten supply and have historically transmitted higher freight and demurrage into landed fuel costs.

Control of critical terminals and pipeline access by a small number of operators therefore elevates supplier bargaining power and pass-through risk to margins.

Currency and commodity volatility

Ampol buys crude and refined product priced in USD while retail sales are predominantly in AUD, leaving margins sensitive to AUD/USD swings; recent 2024 FX volatility increased supplier leverage during tightening cycles. Oil price swings in 2024 compressed and widened supplier pricing power over short periods; hedging reduces but cannot remove basis risk, forcing quicker retail price resets to defend unit economics.

- USD procurement vs AUD sales — FX exposure

- 2024 oil volatility amplified short-cycle supplier power

- Hedging mitigates, not eliminates, basis risk

- Price spikes trigger faster retail resets

Emerging new energy inputs

Supply of renewable diesel, SAF, hydrogen and high-quality bio-components is nascent and tight, and early-stage markets in 2024 still favor suppliers with scarce certified capacity; SAF production remains under 0.1% of global jet fuel demand (industry estimates), boosting supplier leverage. Long-term offtake deals secure volumes but command premium pricing, temporarily heightening supplier power in Ampol’s energy transition.

- Nascent supply: certified capacity scarce

- 2024 SAF <0.1% of jet fuel demand

- Offtake = volume security at premium

OPEC+ 40% grip and FX swings squeeze Aus fuel margins; SAF 0.1% remains tiny

Upstream concentration (OPEC+ ~40% of supply in 2024) and Australia crude ~1.0 mbpd (2023) limit Ampol’s price leverage; specialty additive suppliers and terminal owners retain niche pricing power. FX exposure (USD procurement vs AUD sales) and 2024 oil volatility amplify pass-through risk. SAF <0.1% global jet demand (2024) keeps renewable feedstocks premium-priced.

| Metric | Value |

|---|---|

| OPEC+ share (2024) | ~40% |

| AUS crude prod (2023) | ~1.0 mbpd |

| Diesel sulfur | 10 ppm |

| SAF global share (2024) | <0.1% |

| Key additive suppliers | Infineum, Afton, BASF, Chevron Oronite |

What is included in the product

Tailored Porter's Five Forces analysis for Ampol uncovering competitive drivers, supplier and buyer power, and barriers to entry that shape profitability. Identifies substitutes, disruptive threats, and strategic levers Ampol can use to protect market share and optimize pricing.

A clear, one-sheet Porter's Five Forces summary for Ampol—instantly highlights supplier, buyer, competitor, substitute and entry pressures to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Retail buyers with low switching costs

Motorists can switch stations easily based on price boards and proximity, and with Ampol operating over 1,900 retail sites in 2024 this creates constant local competition. Apps and price-comparison tools have raised transparency, enabling rapid detection of undercutting. Loyalty programs and convenience offers partially dampen churn but do not eliminate it. Net effect: high day-to-day buyer power on pump pricing.

Large B2B contracts exert leverage

Mining, aviation and marine customers buy at scale via tenders—contracts frequently exceed 1 million liters/year and span multi-year terms, driving negotiated discounts and strict SLAs. Volume commitments in 2024 pushed average contract discounts of around 3–6% in commoditized grades. Buyers can dual-source between Ampol, BP, Viva and independents, giving them high bargaining power, especially on standard diesel and jet-A.

Price elasticity and discount cycles

Frequent discounting in metro markets conditions buyers to wait for troughs, with weekly price swings often reaching ~10c/L in 2024, prompting timing behavior. Small price gaps (5–10c/L) can drive meaningful volume swings of roughly 3–5%, transferring pricing pressure to Ampol. With ~1,900 retail sites, Ampol must use dynamic pricing and localized promotions to defend margins and manage traffic flow.

Bundled convenience expectations

- Value drivers: food, coffee, parcels

- Cross-sell lowers fuel price elasticity

- Weak convenience = higher buyer power

- Ampol scale ~1,900 sites (2024)

Sustainability and fuel spec preferences

Corporate fleets increasingly demand lower-carbon fuels and transparent reporting; Ampol states net-zero by 2050, pushing buyers to ask for bio-blends, SAF or offsets and narrowing supplier options. Buyers can shift compliance costs back to suppliers, raising margin pressure and contracting leverage. IATA targets 10% SAF by 2030, giving sophisticated buyers extra negotiating power during the transition.

- Corporate mandates raise demand for bio-blends/SAF

- Compliance costs often shifted to suppliers

- Narrowed supplier pool increases buyer leverage

- IATA 10% SAF by 2030 strengthens buyer bargaining

High retail churn, ~1,900 sites; contracts 3-6% off; weekly swings ~10c/L

High retail churn due to price transparency; Ampol ~1,900 sites (2024). Commercial tenders drive 3–6% contract discounts; weekly metro price swings ~10c/L causing 3–5% volume shifts. Corporate demand for SAF/bio-blends (IATA 10% SAF by 2030) raises supplier leverage.

| Metric | 2024 |

|---|---|

| Retail sites | ~1,900 |

| Contract discounts | 3–6% |

| Weekly price swing | ~10c/L |

| Volume sensitivity | 3–5% |

Full Version Awaits

Ampol Porter's Five Forces Analysis

This preview shows the exact Ampol Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted, ready to download and use immediately, providing the same detailed industry, competitor, supplier, buyer, and threat assessments you see here.