Amtech Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

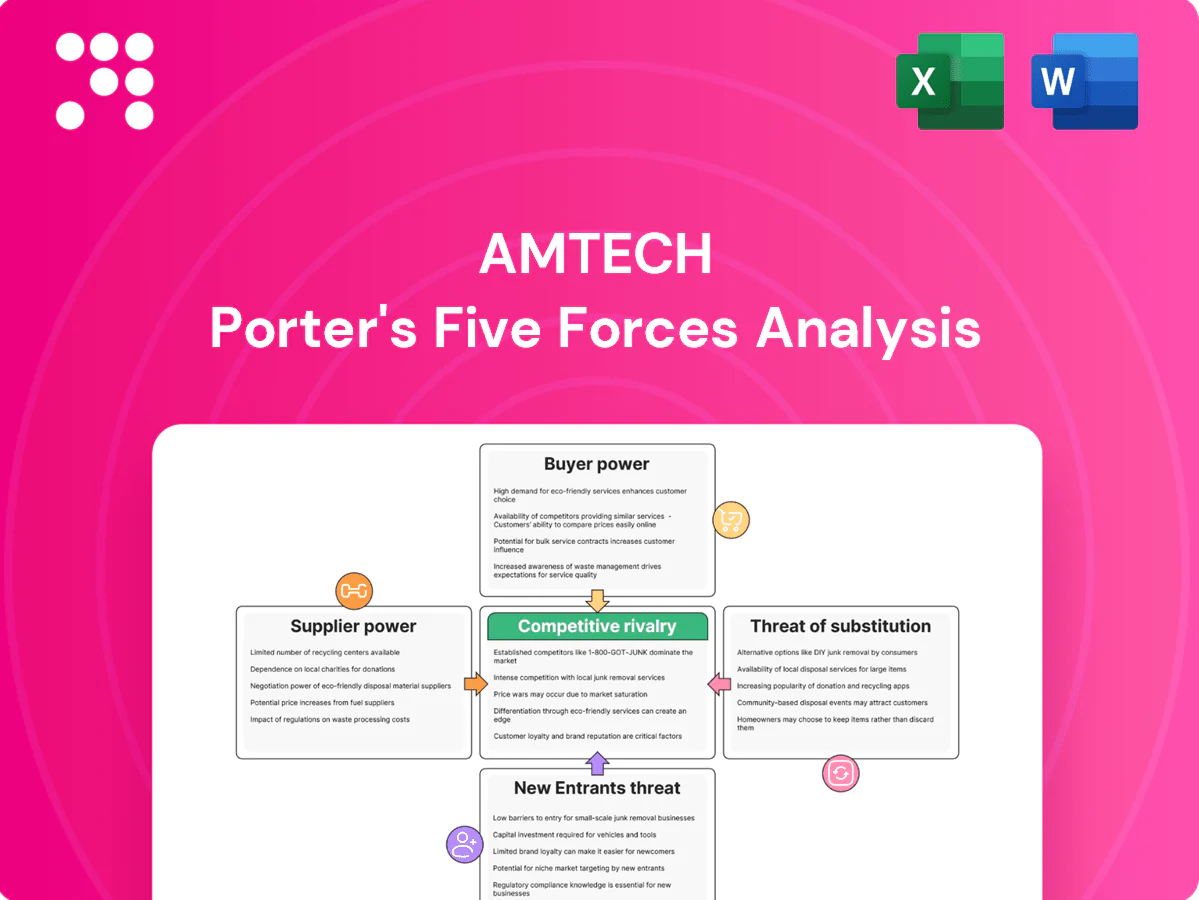

Amtech faces moderate supplier power and evolving buyer expectations, while niche specialization limits new entrants but raises substitute risk. Competitive rivalry centers on technological differentiation and scale economies. This snapshot highlights pressures shaping margins and growth. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized component concentration

Amtech depends on niche inputs such as high‑purity quartzware, vacuum pumps, RF power modules, MFCs, and high‑temperature alloys that come from few qualified vendors, giving suppliers significant leverage. Limited alternates and stringent specs raise switching costs and pricing power. Periodic cycles drive extended lead times that constrain Amtech’s production ramps. Dual‑sourcing reduces but does not eliminate this concentration risk.

Process IP embedded in parts

Certain subassemblies and control software are co‑developed with suppliers, embedding process IP into parts and raising Amtech’s supplier switching costs and requalification timelines. Suppliers thus gain leverage to influence pricing and future upgrade paths, potentially extracting higher margins. Long‑term supply agreements stabilize availability and pricing but also lock Amtech into terms that are hard to renegotiate.

Geopolitical and compliance exposure

Key Amtech inputs largely come from the US, EU and Japan, all subject to strengthened export controls and technical standards—notably US semiconductor export restrictions tightened further in 2023–2024—raising supplier leverage. Regulatory shifts and tighter compliance elevate cost and delay risks, while logistics shocks (port congestion, air freight volatility) amplify bargaining power of compliant suppliers. Buffer inventory and regionalization mitigate but only partially offset elevated supplier bargaining power.

Volume disadvantage vs large OEMs

Compared with mega OEMs, Amtech’s buying volumes are materially smaller, limiting its ability to secure deep volume discounts and making suppliers more likely to favor larger accounts during allocation events, which pressures margins and can delay deliveries.

- Smaller volume => less discount leverage

- Allocation priority typically to larger OEMs

- Can force margin concessions or delivery slippage

- Strategic partnerships buy priority but often at higher pricing

Aftermarket consumables and spares

Recurring quartzware, seals and wear parts are often single-source for specific tool platforms, giving suppliers leverage over pricing and lead times as tool uptime depends on timely spares; predictable, recurring demand allows Amtech to secure framework contracts with fixed pricing and prioritized delivery windows. Design-for-multi-source upgrades can incrementally lower reliance and improve negotiating posture over 12–24 months.

- Single-source dependence: higher supplier leverage

- Predictable demand: enables multi-year framework contracts

- Tool uptime: increases urgency and supplier bargaining power

- Design-for-multi-source: reduces dependence over time

High supplier concentration and 2024 export controls increase lead-time and price risks

Amtech faces high supplier leverage due to few qualified vendors for quartzware, RF modules and specialty alloys, raising switching costs and price risk; 2024 saw tighter US export controls that increased compliance and lead‑time pressure. Dual‑sourcing and design‑for-multi‑source reduce but do not eliminate concentration. Long‑term contracts stabilize supply but limit renegotiation power.

| 2024 Factor | Impact | Mitigation |

|---|---|---|

| Export controls (2024) | Higher lead times/compliance cost | Regionalization, inventory |

What is included in the product

Tailored Porter’s Five Forces for Amtech, uncovering competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, plus disruptive risks and protective market dynamics—ready for inclusion in editable reports.

One-sheet Amtech Porter’s Five Forces that instantly visualizes competitive pressure with a spider chart—customize force levels for new data or scenarios and drop directly into decks for faster, board-ready decisions.

Customers Bargaining Power

Concentrated, sophisticated customers

In 2024, concentrated customers—semiconductor fabs, OSATs, IDMs and large solar producers—hold outsized procurement leverage, running rigorous 12–18 month qualifications and demanding favorable commercial and performance terms. Their in‑house technical teams benchmark vendors stringently, and formal vendor lists plus recurring audits tighten pricing and delivery expectations, squeezing margin for equipment suppliers like Amtech.

High switching costs yet strong negotiation

Once a tool is qualified switching is costly—recipes, operator training and line integration lock customers in, yet in 2024 buyers used multi-vendor sourcing to extract concessions and accelerate roadmap access. Negotiations increasingly hinge on total cost of ownership and uptime SLAs, with fabs pushing for stronger uptime guarantees. Incumbency provides leverage for Amtech but does not eliminate ongoing price pressure.

Demand cyclicality and capex timing

Industry cyclicality lets buyers delay or cancel Amtech orders in downturns, shifting leverage to customers—global semiconductor sales were roughly $583 billion in 2023 with WSTS forecasting ~8% growth in 2024, highlighting volatile demand. Volume bundling in upswings allows buyers to extract pricing concessions; forecast volatility transfers inventory risk to suppliers, making flexible payment, lead-time and return terms a key competitive differentiator.

Customization and co-development asks

Customers increasingly request tailored process modules and automation interfaces, forcing Amtech into bespoke engineering that raises buyers’ leverage over specifications and pricing.

Custom work amplifies dependency yet strengthens customer bargaining power; non-recurring engineering and schedule risks often shift to the vendor during pilots.

Successful pilot projects frequently convert to standardized wins, turning initial customization costs into longer-term product adoption and recurring revenue.

- Customization raises buyer leverage on specs/price

- NRE and schedule risks shift to vendor during pilots

- Pilots that succeed can standardize and lock in revenue

Aftermarket leverage on service

Buyers demand rapid field support and spare availability to protect fab yields, forcing Amtech to accept multi-year service contracts tightly tied to uptime (industry targets commonly exceed 98%), with remote diagnostics and consigned parts now table stakes; poor service can block future tool placements and reduce lifetime revenue per customer.

- Uptime targets: >98%

- Multi-year contracts: heavy negotiation on SLAs

- Remote diagnostics & consigned parts: expected

- Poor service: jeopardizes future placements

Concentrated fab buyers squeeze suppliers: margin pressure amid cyclical chip demand

In 2024 concentrated fab/OSAT/IDM buyers exert strong leverage via long qualifications, multi‑vendor sourcing and TCO/uptime demands, compressing Amtech margins. Switching costs lock tools but buyers extract concessions; cyclical demand (global semiconductor sales $583B in 2023; WSTS +8% est 2024) shifts risk to suppliers. Customization, NRE and >98% SLA demands further increase buyer bargaining power.

| Metric | Value |

|---|---|

| 2023 semiconductor sales | $583B |

| 2024 growth est | ~8% |

| Uptime SLA | >98% |

Preview the Actual Deliverable

Amtech Porter's Five Forces Analysis

This preview shows the exact Amtech Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the fully formatted, ready-to-use file you'll be able to download instantly upon payment. It is the complete, professionally written analysis containing the full assessment and actionable insights.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Amtech faces moderate supplier power and evolving buyer expectations, while niche specialization limits new entrants but raises substitute risk. Competitive rivalry centers on technological differentiation and scale economies. This snapshot highlights pressures shaping margins and growth. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized component concentration

Amtech depends on niche inputs such as high‑purity quartzware, vacuum pumps, RF power modules, MFCs, and high‑temperature alloys that come from few qualified vendors, giving suppliers significant leverage. Limited alternates and stringent specs raise switching costs and pricing power. Periodic cycles drive extended lead times that constrain Amtech’s production ramps. Dual‑sourcing reduces but does not eliminate this concentration risk.

Process IP embedded in parts

Certain subassemblies and control software are co‑developed with suppliers, embedding process IP into parts and raising Amtech’s supplier switching costs and requalification timelines. Suppliers thus gain leverage to influence pricing and future upgrade paths, potentially extracting higher margins. Long‑term supply agreements stabilize availability and pricing but also lock Amtech into terms that are hard to renegotiate.

Geopolitical and compliance exposure

Key Amtech inputs largely come from the US, EU and Japan, all subject to strengthened export controls and technical standards—notably US semiconductor export restrictions tightened further in 2023–2024—raising supplier leverage. Regulatory shifts and tighter compliance elevate cost and delay risks, while logistics shocks (port congestion, air freight volatility) amplify bargaining power of compliant suppliers. Buffer inventory and regionalization mitigate but only partially offset elevated supplier bargaining power.

Volume disadvantage vs large OEMs

Compared with mega OEMs, Amtech’s buying volumes are materially smaller, limiting its ability to secure deep volume discounts and making suppliers more likely to favor larger accounts during allocation events, which pressures margins and can delay deliveries.

- Smaller volume => less discount leverage

- Allocation priority typically to larger OEMs

- Can force margin concessions or delivery slippage

- Strategic partnerships buy priority but often at higher pricing

Aftermarket consumables and spares

Recurring quartzware, seals and wear parts are often single-source for specific tool platforms, giving suppliers leverage over pricing and lead times as tool uptime depends on timely spares; predictable, recurring demand allows Amtech to secure framework contracts with fixed pricing and prioritized delivery windows. Design-for-multi-source upgrades can incrementally lower reliance and improve negotiating posture over 12–24 months.

- Single-source dependence: higher supplier leverage

- Predictable demand: enables multi-year framework contracts

- Tool uptime: increases urgency and supplier bargaining power

- Design-for-multi-source: reduces dependence over time

High supplier concentration and 2024 export controls increase lead-time and price risks

Amtech faces high supplier leverage due to few qualified vendors for quartzware, RF modules and specialty alloys, raising switching costs and price risk; 2024 saw tighter US export controls that increased compliance and lead‑time pressure. Dual‑sourcing and design‑for-multi‑source reduce but do not eliminate concentration. Long‑term contracts stabilize supply but limit renegotiation power.

| 2024 Factor | Impact | Mitigation |

|---|---|---|

| Export controls (2024) | Higher lead times/compliance cost | Regionalization, inventory |

What is included in the product

Tailored Porter’s Five Forces for Amtech, uncovering competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, plus disruptive risks and protective market dynamics—ready for inclusion in editable reports.

One-sheet Amtech Porter’s Five Forces that instantly visualizes competitive pressure with a spider chart—customize force levels for new data or scenarios and drop directly into decks for faster, board-ready decisions.

Customers Bargaining Power

Concentrated, sophisticated customers

In 2024, concentrated customers—semiconductor fabs, OSATs, IDMs and large solar producers—hold outsized procurement leverage, running rigorous 12–18 month qualifications and demanding favorable commercial and performance terms. Their in‑house technical teams benchmark vendors stringently, and formal vendor lists plus recurring audits tighten pricing and delivery expectations, squeezing margin for equipment suppliers like Amtech.

High switching costs yet strong negotiation

Once a tool is qualified switching is costly—recipes, operator training and line integration lock customers in, yet in 2024 buyers used multi-vendor sourcing to extract concessions and accelerate roadmap access. Negotiations increasingly hinge on total cost of ownership and uptime SLAs, with fabs pushing for stronger uptime guarantees. Incumbency provides leverage for Amtech but does not eliminate ongoing price pressure.

Demand cyclicality and capex timing

Industry cyclicality lets buyers delay or cancel Amtech orders in downturns, shifting leverage to customers—global semiconductor sales were roughly $583 billion in 2023 with WSTS forecasting ~8% growth in 2024, highlighting volatile demand. Volume bundling in upswings allows buyers to extract pricing concessions; forecast volatility transfers inventory risk to suppliers, making flexible payment, lead-time and return terms a key competitive differentiator.

Customization and co-development asks

Customers increasingly request tailored process modules and automation interfaces, forcing Amtech into bespoke engineering that raises buyers’ leverage over specifications and pricing.

Custom work amplifies dependency yet strengthens customer bargaining power; non-recurring engineering and schedule risks often shift to the vendor during pilots.

Successful pilot projects frequently convert to standardized wins, turning initial customization costs into longer-term product adoption and recurring revenue.

- Customization raises buyer leverage on specs/price

- NRE and schedule risks shift to vendor during pilots

- Pilots that succeed can standardize and lock in revenue

Aftermarket leverage on service

Buyers demand rapid field support and spare availability to protect fab yields, forcing Amtech to accept multi-year service contracts tightly tied to uptime (industry targets commonly exceed 98%), with remote diagnostics and consigned parts now table stakes; poor service can block future tool placements and reduce lifetime revenue per customer.

- Uptime targets: >98%

- Multi-year contracts: heavy negotiation on SLAs

- Remote diagnostics & consigned parts: expected

- Poor service: jeopardizes future placements

Concentrated fab buyers squeeze suppliers: margin pressure amid cyclical chip demand

In 2024 concentrated fab/OSAT/IDM buyers exert strong leverage via long qualifications, multi‑vendor sourcing and TCO/uptime demands, compressing Amtech margins. Switching costs lock tools but buyers extract concessions; cyclical demand (global semiconductor sales $583B in 2023; WSTS +8% est 2024) shifts risk to suppliers. Customization, NRE and >98% SLA demands further increase buyer bargaining power.

| Metric | Value |

|---|---|

| 2023 semiconductor sales | $583B |

| 2024 growth est | ~8% |

| Uptime SLA | >98% |

Preview the Actual Deliverable

Amtech Porter's Five Forces Analysis

This preview shows the exact Amtech Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the fully formatted, ready-to-use file you'll be able to download instantly upon payment. It is the complete, professionally written analysis containing the full assessment and actionable insights.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Amtech faces moderate supplier power and evolving buyer expectations, while niche specialization limits new entrants but raises substitute risk. Competitive rivalry centers on technological differentiation and scale economies. This snapshot highlights pressures shaping margins and growth. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized component concentration

Amtech depends on niche inputs such as high‑purity quartzware, vacuum pumps, RF power modules, MFCs, and high‑temperature alloys that come from few qualified vendors, giving suppliers significant leverage. Limited alternates and stringent specs raise switching costs and pricing power. Periodic cycles drive extended lead times that constrain Amtech’s production ramps. Dual‑sourcing reduces but does not eliminate this concentration risk.

Process IP embedded in parts

Certain subassemblies and control software are co‑developed with suppliers, embedding process IP into parts and raising Amtech’s supplier switching costs and requalification timelines. Suppliers thus gain leverage to influence pricing and future upgrade paths, potentially extracting higher margins. Long‑term supply agreements stabilize availability and pricing but also lock Amtech into terms that are hard to renegotiate.

Geopolitical and compliance exposure

Key Amtech inputs largely come from the US, EU and Japan, all subject to strengthened export controls and technical standards—notably US semiconductor export restrictions tightened further in 2023–2024—raising supplier leverage. Regulatory shifts and tighter compliance elevate cost and delay risks, while logistics shocks (port congestion, air freight volatility) amplify bargaining power of compliant suppliers. Buffer inventory and regionalization mitigate but only partially offset elevated supplier bargaining power.

Volume disadvantage vs large OEMs

Compared with mega OEMs, Amtech’s buying volumes are materially smaller, limiting its ability to secure deep volume discounts and making suppliers more likely to favor larger accounts during allocation events, which pressures margins and can delay deliveries.

- Smaller volume => less discount leverage

- Allocation priority typically to larger OEMs

- Can force margin concessions or delivery slippage

- Strategic partnerships buy priority but often at higher pricing

Aftermarket consumables and spares

Recurring quartzware, seals and wear parts are often single-source for specific tool platforms, giving suppliers leverage over pricing and lead times as tool uptime depends on timely spares; predictable, recurring demand allows Amtech to secure framework contracts with fixed pricing and prioritized delivery windows. Design-for-multi-source upgrades can incrementally lower reliance and improve negotiating posture over 12–24 months.

- Single-source dependence: higher supplier leverage

- Predictable demand: enables multi-year framework contracts

- Tool uptime: increases urgency and supplier bargaining power

- Design-for-multi-source: reduces dependence over time

High supplier concentration and 2024 export controls increase lead-time and price risks

Amtech faces high supplier leverage due to few qualified vendors for quartzware, RF modules and specialty alloys, raising switching costs and price risk; 2024 saw tighter US export controls that increased compliance and lead‑time pressure. Dual‑sourcing and design‑for-multi‑source reduce but do not eliminate concentration. Long‑term contracts stabilize supply but limit renegotiation power.

| 2024 Factor | Impact | Mitigation |

|---|---|---|

| Export controls (2024) | Higher lead times/compliance cost | Regionalization, inventory |

What is included in the product

Tailored Porter’s Five Forces for Amtech, uncovering competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, plus disruptive risks and protective market dynamics—ready for inclusion in editable reports.

One-sheet Amtech Porter’s Five Forces that instantly visualizes competitive pressure with a spider chart—customize force levels for new data or scenarios and drop directly into decks for faster, board-ready decisions.

Customers Bargaining Power

Concentrated, sophisticated customers

In 2024, concentrated customers—semiconductor fabs, OSATs, IDMs and large solar producers—hold outsized procurement leverage, running rigorous 12–18 month qualifications and demanding favorable commercial and performance terms. Their in‑house technical teams benchmark vendors stringently, and formal vendor lists plus recurring audits tighten pricing and delivery expectations, squeezing margin for equipment suppliers like Amtech.

High switching costs yet strong negotiation

Once a tool is qualified switching is costly—recipes, operator training and line integration lock customers in, yet in 2024 buyers used multi-vendor sourcing to extract concessions and accelerate roadmap access. Negotiations increasingly hinge on total cost of ownership and uptime SLAs, with fabs pushing for stronger uptime guarantees. Incumbency provides leverage for Amtech but does not eliminate ongoing price pressure.

Demand cyclicality and capex timing

Industry cyclicality lets buyers delay or cancel Amtech orders in downturns, shifting leverage to customers—global semiconductor sales were roughly $583 billion in 2023 with WSTS forecasting ~8% growth in 2024, highlighting volatile demand. Volume bundling in upswings allows buyers to extract pricing concessions; forecast volatility transfers inventory risk to suppliers, making flexible payment, lead-time and return terms a key competitive differentiator.

Customization and co-development asks

Customers increasingly request tailored process modules and automation interfaces, forcing Amtech into bespoke engineering that raises buyers’ leverage over specifications and pricing.

Custom work amplifies dependency yet strengthens customer bargaining power; non-recurring engineering and schedule risks often shift to the vendor during pilots.

Successful pilot projects frequently convert to standardized wins, turning initial customization costs into longer-term product adoption and recurring revenue.

- Customization raises buyer leverage on specs/price

- NRE and schedule risks shift to vendor during pilots

- Pilots that succeed can standardize and lock in revenue

Aftermarket leverage on service

Buyers demand rapid field support and spare availability to protect fab yields, forcing Amtech to accept multi-year service contracts tightly tied to uptime (industry targets commonly exceed 98%), with remote diagnostics and consigned parts now table stakes; poor service can block future tool placements and reduce lifetime revenue per customer.

- Uptime targets: >98%

- Multi-year contracts: heavy negotiation on SLAs

- Remote diagnostics & consigned parts: expected

- Poor service: jeopardizes future placements

Concentrated fab buyers squeeze suppliers: margin pressure amid cyclical chip demand

In 2024 concentrated fab/OSAT/IDM buyers exert strong leverage via long qualifications, multi‑vendor sourcing and TCO/uptime demands, compressing Amtech margins. Switching costs lock tools but buyers extract concessions; cyclical demand (global semiconductor sales $583B in 2023; WSTS +8% est 2024) shifts risk to suppliers. Customization, NRE and >98% SLA demands further increase buyer bargaining power.

| Metric | Value |

|---|---|

| 2023 semiconductor sales | $583B |

| 2024 growth est | ~8% |

| Uptime SLA | >98% |

Preview the Actual Deliverable

Amtech Porter's Five Forces Analysis

This preview shows the exact Amtech Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is the fully formatted, ready-to-use file you'll be able to download instantly upon payment. It is the complete, professionally written analysis containing the full assessment and actionable insights.