AmTrust Financial Services Porter's Five Forces Analysis

From Overview to Strategy Blueprint

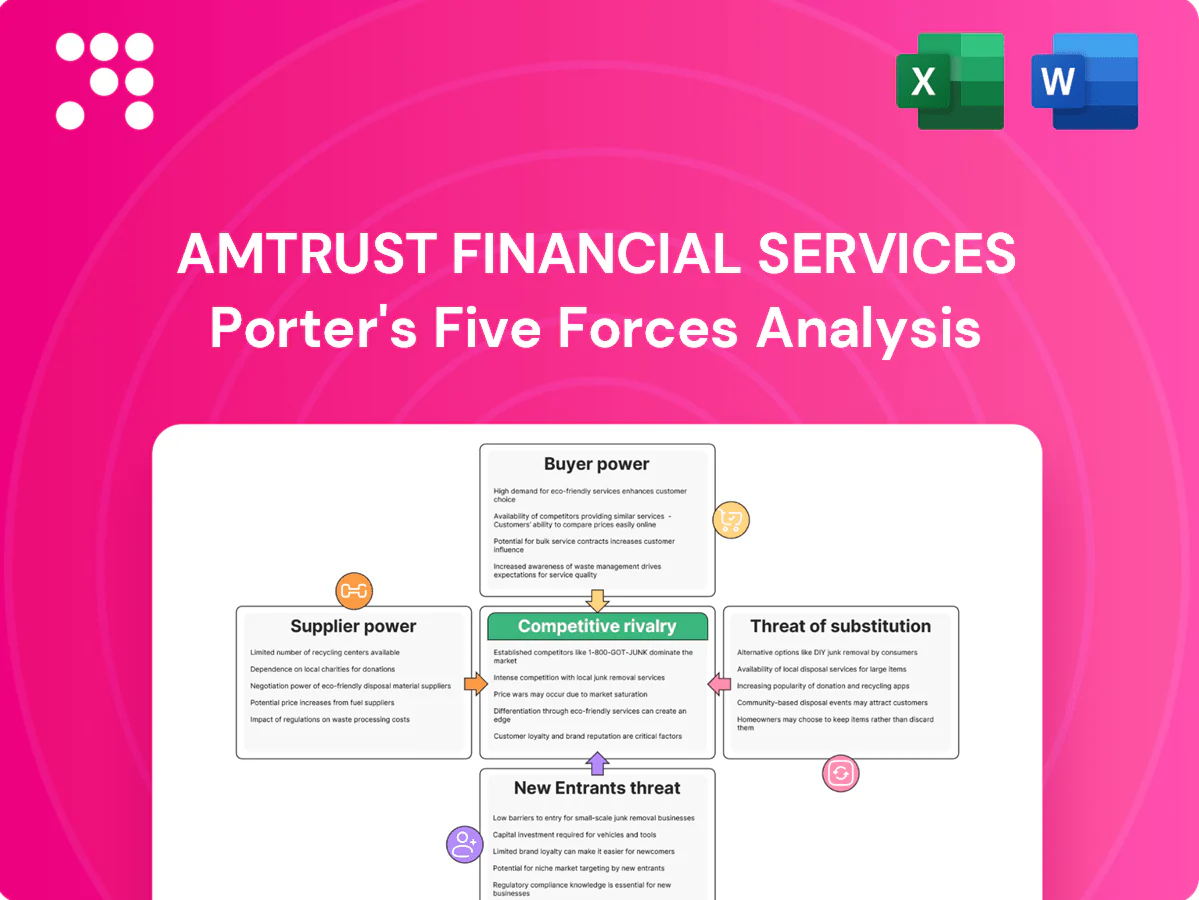

AmTrust Financial Services faces moderate buyer power, concentrated distribution channels, and niche substitute risks that shape pricing and underwriting strategy; supplier influence is limited but regulatory pressure raises barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AmTrust’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance dependence

AmTrust depends on reinsurers to manage peak and catastrophe risk across workers’ comp and specialty lines, and in 2024 reinsurance costs remained elevated following recent catastrophe years. When reinsurance markets harden, pricing and terms tighten, raising ceded costs and constraining capacity. Large global reinsurers retain leverage over attachment points, exclusions, and collateral; diversified panels and multi-year treaties soften but do not remove that dependency.

Data and analytics vendors

Third-party data, modeling, and fraud-detection platforms are critical to AmTrust’s tech-driven underwriting and claims, and niche, high-accuracy datasets such as payroll and telematics give suppliers meaningful bargaining leverage. Switching vendors risks model disruption and costly retraining, creating vendor stickiness. Volume commitments and growing in-house analytics capabilities help AmTrust rebalance supplier terms.

Distribution intermediaries

Independent agents, brokers and MGAs serve as gatekeepers to AmTrust’s SMB book, with the company noting the majority of commercial premiums are placed through these intermediaries in recent filings. Aggregators holding concentrated books can extract higher commissions and favorable terms. The overall fragmentation of the SMB channel limits any single intermediary’s bargaining power, while growing direct and digital channels further dilute intermediary leverage.

Specialty service providers

Specialty service providers—medical networks, TPAs, repair networks, and warranty administrators—directly affect AmTrust’s loss costs and customer experience through network rates, claims processing speed, and repair quality.

Providers with niche expertise can command pricing power; AmTrust mitigates this via multi-vendor strategies, outcome-based contracts, and selective vertical integration in claims workflows.

- Supply categories: medical, TPA, repair, warranty

- Mitigants: multi-vendor, outcome contracts, vertical integration

- Impact: loss cost and CX drivers

Human capital and actuarial talent

Experienced underwriters, actuaries, and claims leaders remain scarce, pushing up compensation and retention costs; median actuary pay was $108,350 (BLS May 2023) and insurers reported elevated salary inflation into 2024. Talent hubs concentrate bargaining power, though remote hiring expands the candidate pool while insurtechs and large carriers keep competition high. AmTrust’s strong culture, proprietary tools, and clear career paths help mitigate turnover risk.

- Scarcity raises costs

- Hubs increase supplier power

- Remote hiring widens pool but competition persists

- Culture/tools reduce turnover

Insurer faces 2024 reinsurance cost surge, vendor stickiness and talent squeeze

AmTrust faces elevated 2024 reinsurance costs and capacity pressure from global reinsurers, maintaining dependency despite multi-year treaties. Critical data and fraud vendors create stickiness; switching risks model disruption while in-house analytics partially offsets leverage. Independent agents/MGAs gatekeep SMB flow but fragmented channels and growing direct digital sales limit concentrated power. Specialized TPAs, medical networks and talent scarcity drive loss costs and service risk.

| Supplier | 2024 Reality | Mitigant |

|---|---|---|

| Reinsurers | Elevated costs, capacity tightening 2024 | Multi-year treaties |

| Data vendors | High switching cost | In-house analytics |

| Agents/MGAs | Major SMB channel, fragmented | Direct/digital growth |

| Talent | Median actuary pay $108,350 (BLS May 2023) | Culture, tools |

What is included in the product

Provides a tailored Porter’s Five Forces analysis of AmTrust Financial Services, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive risks to its market position.

A clear, one-sheet Porter’s Five Forces summary for AmTrust Financial Services—instantly visualizes competitive pressure with an editable radar chart and clean layout, ready to drop into pitch decks or broader Excel dashboards.

Customers Bargaining Power

SMB price sensitivity

SMBs, which make up 99.9% of US firms, are highly price-sensitive and commonly shop carriers at renewal, increasing buyer leverage for AmTrust in the small-commercial market. Comparable coverage from multiple carriers intensifies this pressure, while AmTrust’s loss-control and risk-engineering services can offset pure price focus. Multi-policy bundling modestly raises switching costs but does not eliminate shopping behavior.

Broker-driven leverage

Brokers aggregate demand and run competitive remarketing across carriers, giving them leverage to steer accounts and exert downward pressure on pricing and terms; brokers handle over 50% of commercial placements in the U.S. market. Preferred carrier status and consistent service-level excellence secure placement priority and higher retention. Transparent, fast quoting—responses within 24–48 hours—has been shown to improve win rates by double digits.

Regulatory and mandated coverages

Workers’ compensation is mandated in most US states as of 2024, with Texas as an opt-out outlier, limiting employers’ ability to forgo coverage. State filings and NCCI models standardize coverages, narrowing product differentiation and easing carrier switching. Consequently, service quality and claims handling are primary tie-breakers for buyers, moderating but not eliminating buyer power.

Digital comparison and speed

- Rapid multi-quote bidding boosts price sensitivity

- ~30% digital purchase mix (2024) increases visibility

- Instant bind/endorsements improve retention

- Smooth UX cuts churn and preserves lifetime value

Large program and warranty clients

OEMs and large retailers for extended warranties demand bespoke terms and volume pricing, amplifying buyer power and compressing fees; they frequently insist on performance SLAs and loss-sharing arrangements that shift risk to insurers. Long-term partnerships and co-innovation can mitigate margin pressure by enabling joint product improvements and data-sharing.

- Scale => stronger negotiation

- SLA & loss-sharing demanded

- Volume pricing => fee compression risk

- Long-term co-innovation tempers margins

SMB price sensitivity (99.9%), brokers (> 50% placements), digital (~30%) pressure workers’ comp

SMBs (99.9% of US firms) are highly price-sensitive and frequently shop at renewal, raising buyer leverage; AmTrust’s loss-control services partially offset this. Brokers control >50% of commercial placements, steering accounts and pressuring price/terms. Digital channels reached ~30% of insurance purchases in 2024, increasing transparency. Workers’ comp is mandated in most states (Texas opt-out), limiting coverage avoidance.

| Driver | 2024 metric | Impact |

|---|---|---|

| SMB share | 99.9% | High price sensitivity |

| Brokers | >50% placements | Negotiation leverage |

| Digital | ~30% | Greater price transparency |

| Workers’ comp | Mandated (TX opt-out) | Reduced avoidance |

Same Document Delivered

AmTrust Financial Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for AmTrust Financial Services that you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download. What you see here is precisely the deliverable available instantly upon payment.

From Overview to Strategy Blueprint

AmTrust Financial Services faces moderate buyer power, concentrated distribution channels, and niche substitute risks that shape pricing and underwriting strategy; supplier influence is limited but regulatory pressure raises barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AmTrust’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance dependence

AmTrust depends on reinsurers to manage peak and catastrophe risk across workers’ comp and specialty lines, and in 2024 reinsurance costs remained elevated following recent catastrophe years. When reinsurance markets harden, pricing and terms tighten, raising ceded costs and constraining capacity. Large global reinsurers retain leverage over attachment points, exclusions, and collateral; diversified panels and multi-year treaties soften but do not remove that dependency.

Data and analytics vendors

Third-party data, modeling, and fraud-detection platforms are critical to AmTrust’s tech-driven underwriting and claims, and niche, high-accuracy datasets such as payroll and telematics give suppliers meaningful bargaining leverage. Switching vendors risks model disruption and costly retraining, creating vendor stickiness. Volume commitments and growing in-house analytics capabilities help AmTrust rebalance supplier terms.

Distribution intermediaries

Independent agents, brokers and MGAs serve as gatekeepers to AmTrust’s SMB book, with the company noting the majority of commercial premiums are placed through these intermediaries in recent filings. Aggregators holding concentrated books can extract higher commissions and favorable terms. The overall fragmentation of the SMB channel limits any single intermediary’s bargaining power, while growing direct and digital channels further dilute intermediary leverage.

Specialty service providers

Specialty service providers—medical networks, TPAs, repair networks, and warranty administrators—directly affect AmTrust’s loss costs and customer experience through network rates, claims processing speed, and repair quality.

Providers with niche expertise can command pricing power; AmTrust mitigates this via multi-vendor strategies, outcome-based contracts, and selective vertical integration in claims workflows.

- Supply categories: medical, TPA, repair, warranty

- Mitigants: multi-vendor, outcome contracts, vertical integration

- Impact: loss cost and CX drivers

Human capital and actuarial talent

Experienced underwriters, actuaries, and claims leaders remain scarce, pushing up compensation and retention costs; median actuary pay was $108,350 (BLS May 2023) and insurers reported elevated salary inflation into 2024. Talent hubs concentrate bargaining power, though remote hiring expands the candidate pool while insurtechs and large carriers keep competition high. AmTrust’s strong culture, proprietary tools, and clear career paths help mitigate turnover risk.

- Scarcity raises costs

- Hubs increase supplier power

- Remote hiring widens pool but competition persists

- Culture/tools reduce turnover

Insurer faces 2024 reinsurance cost surge, vendor stickiness and talent squeeze

AmTrust faces elevated 2024 reinsurance costs and capacity pressure from global reinsurers, maintaining dependency despite multi-year treaties. Critical data and fraud vendors create stickiness; switching risks model disruption while in-house analytics partially offsets leverage. Independent agents/MGAs gatekeep SMB flow but fragmented channels and growing direct digital sales limit concentrated power. Specialized TPAs, medical networks and talent scarcity drive loss costs and service risk.

| Supplier | 2024 Reality | Mitigant |

|---|---|---|

| Reinsurers | Elevated costs, capacity tightening 2024 | Multi-year treaties |

| Data vendors | High switching cost | In-house analytics |

| Agents/MGAs | Major SMB channel, fragmented | Direct/digital growth |

| Talent | Median actuary pay $108,350 (BLS May 2023) | Culture, tools |

What is included in the product

Provides a tailored Porter’s Five Forces analysis of AmTrust Financial Services, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive risks to its market position.

A clear, one-sheet Porter’s Five Forces summary for AmTrust Financial Services—instantly visualizes competitive pressure with an editable radar chart and clean layout, ready to drop into pitch decks or broader Excel dashboards.

Customers Bargaining Power

SMB price sensitivity

SMBs, which make up 99.9% of US firms, are highly price-sensitive and commonly shop carriers at renewal, increasing buyer leverage for AmTrust in the small-commercial market. Comparable coverage from multiple carriers intensifies this pressure, while AmTrust’s loss-control and risk-engineering services can offset pure price focus. Multi-policy bundling modestly raises switching costs but does not eliminate shopping behavior.

Broker-driven leverage

Brokers aggregate demand and run competitive remarketing across carriers, giving them leverage to steer accounts and exert downward pressure on pricing and terms; brokers handle over 50% of commercial placements in the U.S. market. Preferred carrier status and consistent service-level excellence secure placement priority and higher retention. Transparent, fast quoting—responses within 24–48 hours—has been shown to improve win rates by double digits.

Regulatory and mandated coverages

Workers’ compensation is mandated in most US states as of 2024, with Texas as an opt-out outlier, limiting employers’ ability to forgo coverage. State filings and NCCI models standardize coverages, narrowing product differentiation and easing carrier switching. Consequently, service quality and claims handling are primary tie-breakers for buyers, moderating but not eliminating buyer power.

Digital comparison and speed

- Rapid multi-quote bidding boosts price sensitivity

- ~30% digital purchase mix (2024) increases visibility

- Instant bind/endorsements improve retention

- Smooth UX cuts churn and preserves lifetime value

Large program and warranty clients

OEMs and large retailers for extended warranties demand bespoke terms and volume pricing, amplifying buyer power and compressing fees; they frequently insist on performance SLAs and loss-sharing arrangements that shift risk to insurers. Long-term partnerships and co-innovation can mitigate margin pressure by enabling joint product improvements and data-sharing.

- Scale => stronger negotiation

- SLA & loss-sharing demanded

- Volume pricing => fee compression risk

- Long-term co-innovation tempers margins

SMB price sensitivity (99.9%), brokers (> 50% placements), digital (~30%) pressure workers’ comp

SMBs (99.9% of US firms) are highly price-sensitive and frequently shop at renewal, raising buyer leverage; AmTrust’s loss-control services partially offset this. Brokers control >50% of commercial placements, steering accounts and pressuring price/terms. Digital channels reached ~30% of insurance purchases in 2024, increasing transparency. Workers’ comp is mandated in most states (Texas opt-out), limiting coverage avoidance.

| Driver | 2024 metric | Impact |

|---|---|---|

| SMB share | 99.9% | High price sensitivity |

| Brokers | >50% placements | Negotiation leverage |

| Digital | ~30% | Greater price transparency |

| Workers’ comp | Mandated (TX opt-out) | Reduced avoidance |

Same Document Delivered

AmTrust Financial Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for AmTrust Financial Services that you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download. What you see here is precisely the deliverable available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

AmTrust Financial Services faces moderate buyer power, concentrated distribution channels, and niche substitute risks that shape pricing and underwriting strategy; supplier influence is limited but regulatory pressure raises barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AmTrust’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance dependence

AmTrust depends on reinsurers to manage peak and catastrophe risk across workers’ comp and specialty lines, and in 2024 reinsurance costs remained elevated following recent catastrophe years. When reinsurance markets harden, pricing and terms tighten, raising ceded costs and constraining capacity. Large global reinsurers retain leverage over attachment points, exclusions, and collateral; diversified panels and multi-year treaties soften but do not remove that dependency.

Data and analytics vendors

Third-party data, modeling, and fraud-detection platforms are critical to AmTrust’s tech-driven underwriting and claims, and niche, high-accuracy datasets such as payroll and telematics give suppliers meaningful bargaining leverage. Switching vendors risks model disruption and costly retraining, creating vendor stickiness. Volume commitments and growing in-house analytics capabilities help AmTrust rebalance supplier terms.

Distribution intermediaries

Independent agents, brokers and MGAs serve as gatekeepers to AmTrust’s SMB book, with the company noting the majority of commercial premiums are placed through these intermediaries in recent filings. Aggregators holding concentrated books can extract higher commissions and favorable terms. The overall fragmentation of the SMB channel limits any single intermediary’s bargaining power, while growing direct and digital channels further dilute intermediary leverage.

Specialty service providers

Specialty service providers—medical networks, TPAs, repair networks, and warranty administrators—directly affect AmTrust’s loss costs and customer experience through network rates, claims processing speed, and repair quality.

Providers with niche expertise can command pricing power; AmTrust mitigates this via multi-vendor strategies, outcome-based contracts, and selective vertical integration in claims workflows.

- Supply categories: medical, TPA, repair, warranty

- Mitigants: multi-vendor, outcome contracts, vertical integration

- Impact: loss cost and CX drivers

Human capital and actuarial talent

Experienced underwriters, actuaries, and claims leaders remain scarce, pushing up compensation and retention costs; median actuary pay was $108,350 (BLS May 2023) and insurers reported elevated salary inflation into 2024. Talent hubs concentrate bargaining power, though remote hiring expands the candidate pool while insurtechs and large carriers keep competition high. AmTrust’s strong culture, proprietary tools, and clear career paths help mitigate turnover risk.

- Scarcity raises costs

- Hubs increase supplier power

- Remote hiring widens pool but competition persists

- Culture/tools reduce turnover

Insurer faces 2024 reinsurance cost surge, vendor stickiness and talent squeeze

AmTrust faces elevated 2024 reinsurance costs and capacity pressure from global reinsurers, maintaining dependency despite multi-year treaties. Critical data and fraud vendors create stickiness; switching risks model disruption while in-house analytics partially offsets leverage. Independent agents/MGAs gatekeep SMB flow but fragmented channels and growing direct digital sales limit concentrated power. Specialized TPAs, medical networks and talent scarcity drive loss costs and service risk.

| Supplier | 2024 Reality | Mitigant |

|---|---|---|

| Reinsurers | Elevated costs, capacity tightening 2024 | Multi-year treaties |

| Data vendors | High switching cost | In-house analytics |

| Agents/MGAs | Major SMB channel, fragmented | Direct/digital growth |

| Talent | Median actuary pay $108,350 (BLS May 2023) | Culture, tools |

What is included in the product

Provides a tailored Porter’s Five Forces analysis of AmTrust Financial Services, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive risks to its market position.

A clear, one-sheet Porter’s Five Forces summary for AmTrust Financial Services—instantly visualizes competitive pressure with an editable radar chart and clean layout, ready to drop into pitch decks or broader Excel dashboards.

Customers Bargaining Power

SMB price sensitivity

SMBs, which make up 99.9% of US firms, are highly price-sensitive and commonly shop carriers at renewal, increasing buyer leverage for AmTrust in the small-commercial market. Comparable coverage from multiple carriers intensifies this pressure, while AmTrust’s loss-control and risk-engineering services can offset pure price focus. Multi-policy bundling modestly raises switching costs but does not eliminate shopping behavior.

Broker-driven leverage

Brokers aggregate demand and run competitive remarketing across carriers, giving them leverage to steer accounts and exert downward pressure on pricing and terms; brokers handle over 50% of commercial placements in the U.S. market. Preferred carrier status and consistent service-level excellence secure placement priority and higher retention. Transparent, fast quoting—responses within 24–48 hours—has been shown to improve win rates by double digits.

Regulatory and mandated coverages

Workers’ compensation is mandated in most US states as of 2024, with Texas as an opt-out outlier, limiting employers’ ability to forgo coverage. State filings and NCCI models standardize coverages, narrowing product differentiation and easing carrier switching. Consequently, service quality and claims handling are primary tie-breakers for buyers, moderating but not eliminating buyer power.

Digital comparison and speed

- Rapid multi-quote bidding boosts price sensitivity

- ~30% digital purchase mix (2024) increases visibility

- Instant bind/endorsements improve retention

- Smooth UX cuts churn and preserves lifetime value

Large program and warranty clients

OEMs and large retailers for extended warranties demand bespoke terms and volume pricing, amplifying buyer power and compressing fees; they frequently insist on performance SLAs and loss-sharing arrangements that shift risk to insurers. Long-term partnerships and co-innovation can mitigate margin pressure by enabling joint product improvements and data-sharing.

- Scale => stronger negotiation

- SLA & loss-sharing demanded

- Volume pricing => fee compression risk

- Long-term co-innovation tempers margins

SMB price sensitivity (99.9%), brokers (> 50% placements), digital (~30%) pressure workers’ comp

SMBs (99.9% of US firms) are highly price-sensitive and frequently shop at renewal, raising buyer leverage; AmTrust’s loss-control services partially offset this. Brokers control >50% of commercial placements, steering accounts and pressuring price/terms. Digital channels reached ~30% of insurance purchases in 2024, increasing transparency. Workers’ comp is mandated in most states (Texas opt-out), limiting coverage avoidance.

| Driver | 2024 metric | Impact |

|---|---|---|

| SMB share | 99.9% | High price sensitivity |

| Brokers | >50% placements | Negotiation leverage |

| Digital | ~30% | Greater price transparency |

| Workers’ comp | Mandated (TX opt-out) | Reduced avoidance |

Same Document Delivered

AmTrust Financial Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for AmTrust Financial Services that you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download. What you see here is precisely the deliverable available instantly upon payment.