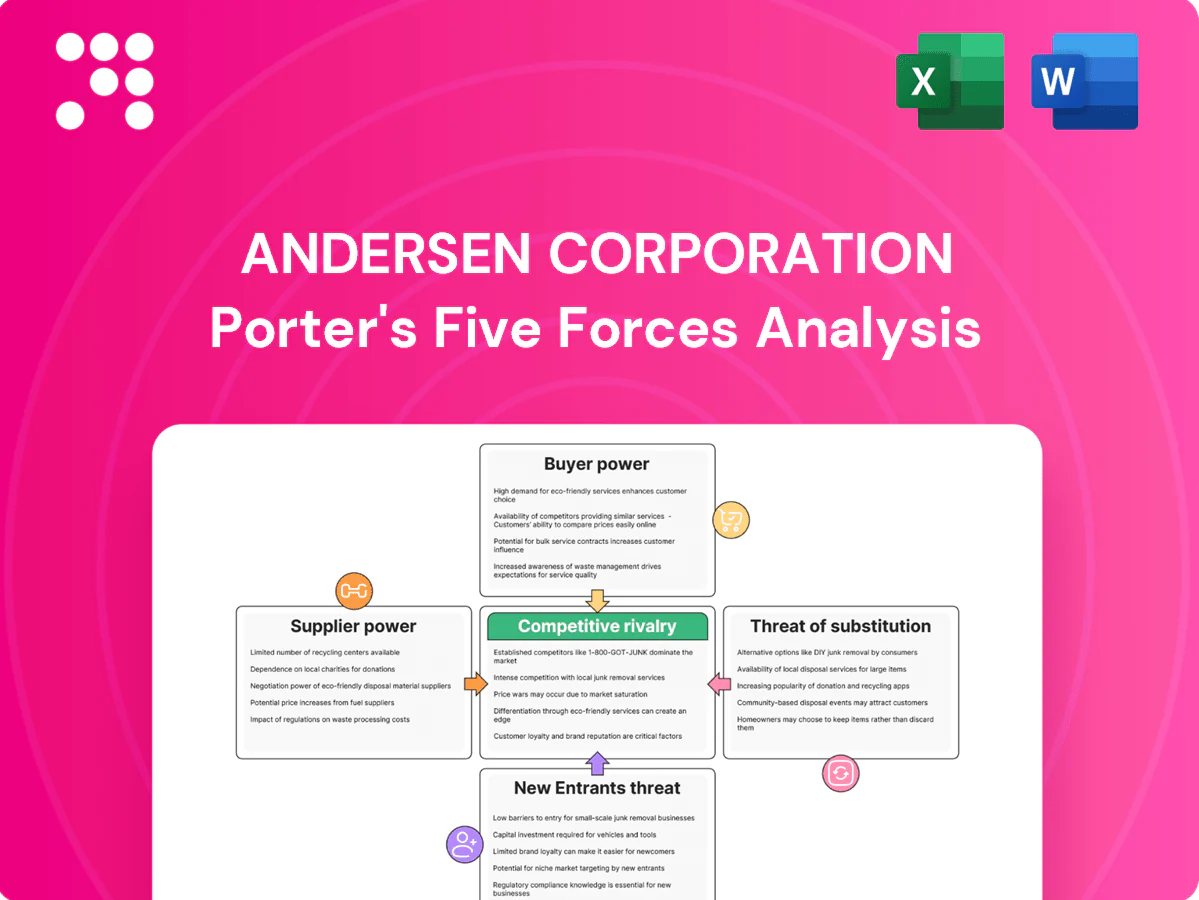

Andersen Corporation Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Andersen Corporation faces moderate buyer power, concentrated suppliers for specialized materials, steady rivalry among established manufacturers, manageable threats from substitutes, and entry barriers driven by scale and distribution. This snapshot highlights key competitive dynamics and strategic pressures. Ready for deeper, data-driven insights? Unlock the full Porter's Five Forces Analysis to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration in key inputs

Concentration among glass, resins/vinyl, wood, aluminum and hardware suppliers gives these vendors elevated leverage over pricing and allocations, pressuring Andersen’s margins. Insulated glass units and low-E coatings come from specialized vendors, so disruptions can quickly ripple through capacity planning and delivery times. Andersen mitigates risk through multi-sourcing and inventory buffers but remains exposed on specialty components.

Specialized technology components

High-performance glazing, coatings, seals and hardware for Andersen require tight specs and certifications, giving suppliers of proprietary chemistries or tooling leverage to command premiums. Switching suppliers triggers lengthy requalification, testing and potential warranty exposure, raising switching costs. Dependence on niche suppliers therefore elevates their bargaining power in Andersen’s supply chain.

Logistics and energy sensitivity

Transportation, energy, and commodity volatility pass through supplier quotes, with fuel surcharges averaging about 8% of freight invoices in 2024 and diesel retail prices near $3.90/gal (EIA 2024). Bulky, fragile glass increases handling costs and drives damage claims—industry data showed glass-related claims around 2% of shipments in 2024. Lane scarcity and surge pricing can lift spot rates 15–30% quickly, while suppliers used lead-time control to extend transit windows by roughly 15% in tight markets.

Switching costs and requalification

Revalidating suppliers for Andersen requires ASTM/AAMA testing cycles often taking 4–12 weeks, third-party audits, and line requalification, creating lead-time and cost barriers. Tooling and die investments commonly exceed $100,000 per part, locking production to incumbent vendors. Warranty and long-term performance commitments tie Andersen to suppliers, discouraging rapid supplier changes and raising supplier bargaining power.

- Testing lead-time: 4–12 weeks

- Tooling cost: >$100,000 per part

- Audit/requalification: third-party required

- Warranty ties: multi-year obligations

Sustainability and certified materials

Sustainability requirements — FSC wood, low‑VOC components and energy‑efficient glass — shrink Andersen Corporation’s qualified supplier pool, raising procurement complexity and costs; industry premiums for certified materials commonly range 5–15% and Andersen’s scale (~$2.5B revenue) increases reliance on a narrower set of vetted vendors. Environmental traceability mandates add compliance burden, but preferred green suppliers can secure stronger commercial terms while sustainability alignment fosters deeper strategic partnerships over time.

- FSC wood narrows sources

- Low‑VOC & glass raise costs 5–15%

- Traceability adds compliance complexity

- Preferred green suppliers gain negotiating power

- Long‑term partnerships improve supply stability

Concentrated suppliers, tooling >$100,000 and 4-12 week testing raise costs and barriers

Concentrated suppliers for glass, coatings, hardware and FSC wood give vendors strong leverage, pressuring Andersen’s margins despite multi-sourcing; tooling costs >$100,000 and ASTM/AAMA tests (4–12 weeks) raise switching costs. Commodity and transport pass‑throughs (fuel surcharge ~8%, diesel ~$3.90/gal) plus certified-material premiums (5–15%) further boost supplier power.

| Metric | Value |

|---|---|

| Revenue | $2.5B |

| Tooling cost | >$100,000/part |

| Testing lead-time | 4–12 weeks |

| Fuel surcharge | ~8% |

| Diesel (2024) | $3.90/gal |

| Certified premium | 5–15% |

| Glass claims | ~2% shipments |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, highlighting Andersen Corporation's strengths in brand, scale, distribution and innovation, plus supplier relationships and customer dynamics that shape pricing, margins and strategic vulnerability.

A concise, one-sheet Porter's Five Forces for Andersen Corporation that instantly highlights supplier power, buyer leverage, substitute and entrant threats, and competitive rivalry—streamlining strategic decisions and boardroom discussions.

Customers Bargaining Power

Channel leverage of big retailers

Large home-improvement chains exert pricing, placement and payment-term pressure on Andersen; Home Depot and Lowe's together control roughly 60% of U.S. home-improvement retail (2024), giving them scale to demand lower prices and favorable terms. Their volume enables aggressive private-label threats and bargaining on assortment. Slotting, returns and merchandising demands raise supplier costs. Andersen offsets this with strong brand pull and product differentiation.

Professional builders and contractors

Professional builders buy windows in large volumes and in 2024 negotiated rebates and tiered discounts, leveraging purchase scale to squeeze unit pricing. They prioritize on-time delivery, reliable service and consistent specs, creating strong switching inertia that benefits incumbent suppliers. Competitive bid processes keep margin pressure high, while approved vendor lists can both lock in suppliers and lock out competitors, concentrating purchasing power among a few large builders.

End-customer price sensitivity

Remodeling and replacement buyers weigh performance versus budget closely, with U.S. remodeling spending in 2024 near $420 billion driving price-conscious decisions. Promotions and point-of-sale financing (often covering 20–30% of projects) shift demand among brands. Online reviews and configurators increase transparency and shorten decision cycles. Differentiated aesthetics and 10+ year warranties temper pure price comparisons.

Product differentiation and brand

Andersen’s strong brand and patented features (ENERGY STAR certified lines) support premium pricing and reduce buyer power; the company reported roughly $3B revenue in 2023 and ~13,000 employees, underscoring scale advantages. Look‑alike vinyl competitors narrow perceived differentiation, making service quality and a certified installer network decisive.

- Brand equity: supports premium pricing

- Patents/energy ratings: defensibility (ENERGY STAR)

- Look‑alikes: compress gaps

- Installer/service: key tie‑breaker

Switching and installation costs

Changing brands often requires retraining installers and adapting to different sizes and hardware, and in 2024 tight labor markets and schedule pressure made costly callbacks and delays more impactful, creating practical friction that moderates buyer bargaining. Standardized openings and common SKUs, however, limit supplier lock-in in many retrofit and new-build segments.

- Installer retraining raises switching friction

- Callbacks and delays amplify cost sensitivity

- Standard SKUs reduce lock-in in some segments

Retail giants 60% share squeeze margins; remodelers $420B seek warranties

Large retailers (Home Depot/Lowe's ~60% U.S. share in 2024) and big builders exert strong price and terms pressure; remodelers (U.S. remodeling spend ~$420B in 2024) are price-sensitive but seek warranties; Andersen (≈$3B revenue in 2023, ~13,000 employees) offsets pressure with brand, ENERGY STAR lines and installer networks, though vinyl look‑alikes compress differentiation.

| Buyer segment | 2024 metric | Bargaining power |

|---|---|---|

| Retail chains | 60% market control | High |

| Builders | Tiered rebates | High |

| Remodelers | $420B spend | Medium |

| Andersen | $3B rev, 13k emp | Moderate defense |

Preview Before You Purchase

Andersen Corporation Porter's Five Forces Analysis

This preview shows the exact Andersen Corporation Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the full, professionally formatted analysis, ready for download and use the moment you buy. You're viewing the final deliverable, instantly accessible upon payment.

Don't Miss the Bigger Picture

Andersen Corporation faces moderate buyer power, concentrated suppliers for specialized materials, steady rivalry among established manufacturers, manageable threats from substitutes, and entry barriers driven by scale and distribution. This snapshot highlights key competitive dynamics and strategic pressures. Ready for deeper, data-driven insights? Unlock the full Porter's Five Forces Analysis to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration in key inputs

Concentration among glass, resins/vinyl, wood, aluminum and hardware suppliers gives these vendors elevated leverage over pricing and allocations, pressuring Andersen’s margins. Insulated glass units and low-E coatings come from specialized vendors, so disruptions can quickly ripple through capacity planning and delivery times. Andersen mitigates risk through multi-sourcing and inventory buffers but remains exposed on specialty components.

Specialized technology components

High-performance glazing, coatings, seals and hardware for Andersen require tight specs and certifications, giving suppliers of proprietary chemistries or tooling leverage to command premiums. Switching suppliers triggers lengthy requalification, testing and potential warranty exposure, raising switching costs. Dependence on niche suppliers therefore elevates their bargaining power in Andersen’s supply chain.

Logistics and energy sensitivity

Transportation, energy, and commodity volatility pass through supplier quotes, with fuel surcharges averaging about 8% of freight invoices in 2024 and diesel retail prices near $3.90/gal (EIA 2024). Bulky, fragile glass increases handling costs and drives damage claims—industry data showed glass-related claims around 2% of shipments in 2024. Lane scarcity and surge pricing can lift spot rates 15–30% quickly, while suppliers used lead-time control to extend transit windows by roughly 15% in tight markets.

Switching costs and requalification

Revalidating suppliers for Andersen requires ASTM/AAMA testing cycles often taking 4–12 weeks, third-party audits, and line requalification, creating lead-time and cost barriers. Tooling and die investments commonly exceed $100,000 per part, locking production to incumbent vendors. Warranty and long-term performance commitments tie Andersen to suppliers, discouraging rapid supplier changes and raising supplier bargaining power.

- Testing lead-time: 4–12 weeks

- Tooling cost: >$100,000 per part

- Audit/requalification: third-party required

- Warranty ties: multi-year obligations

Sustainability and certified materials

Sustainability requirements — FSC wood, low‑VOC components and energy‑efficient glass — shrink Andersen Corporation’s qualified supplier pool, raising procurement complexity and costs; industry premiums for certified materials commonly range 5–15% and Andersen’s scale (~$2.5B revenue) increases reliance on a narrower set of vetted vendors. Environmental traceability mandates add compliance burden, but preferred green suppliers can secure stronger commercial terms while sustainability alignment fosters deeper strategic partnerships over time.

- FSC wood narrows sources

- Low‑VOC & glass raise costs 5–15%

- Traceability adds compliance complexity

- Preferred green suppliers gain negotiating power

- Long‑term partnerships improve supply stability

Concentrated suppliers, tooling >$100,000 and 4-12 week testing raise costs and barriers

Concentrated suppliers for glass, coatings, hardware and FSC wood give vendors strong leverage, pressuring Andersen’s margins despite multi-sourcing; tooling costs >$100,000 and ASTM/AAMA tests (4–12 weeks) raise switching costs. Commodity and transport pass‑throughs (fuel surcharge ~8%, diesel ~$3.90/gal) plus certified-material premiums (5–15%) further boost supplier power.

| Metric | Value |

|---|---|

| Revenue | $2.5B |

| Tooling cost | >$100,000/part |

| Testing lead-time | 4–12 weeks |

| Fuel surcharge | ~8% |

| Diesel (2024) | $3.90/gal |

| Certified premium | 5–15% |

| Glass claims | ~2% shipments |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, highlighting Andersen Corporation's strengths in brand, scale, distribution and innovation, plus supplier relationships and customer dynamics that shape pricing, margins and strategic vulnerability.

A concise, one-sheet Porter's Five Forces for Andersen Corporation that instantly highlights supplier power, buyer leverage, substitute and entrant threats, and competitive rivalry—streamlining strategic decisions and boardroom discussions.

Customers Bargaining Power

Channel leverage of big retailers

Large home-improvement chains exert pricing, placement and payment-term pressure on Andersen; Home Depot and Lowe's together control roughly 60% of U.S. home-improvement retail (2024), giving them scale to demand lower prices and favorable terms. Their volume enables aggressive private-label threats and bargaining on assortment. Slotting, returns and merchandising demands raise supplier costs. Andersen offsets this with strong brand pull and product differentiation.

Professional builders and contractors

Professional builders buy windows in large volumes and in 2024 negotiated rebates and tiered discounts, leveraging purchase scale to squeeze unit pricing. They prioritize on-time delivery, reliable service and consistent specs, creating strong switching inertia that benefits incumbent suppliers. Competitive bid processes keep margin pressure high, while approved vendor lists can both lock in suppliers and lock out competitors, concentrating purchasing power among a few large builders.

End-customer price sensitivity

Remodeling and replacement buyers weigh performance versus budget closely, with U.S. remodeling spending in 2024 near $420 billion driving price-conscious decisions. Promotions and point-of-sale financing (often covering 20–30% of projects) shift demand among brands. Online reviews and configurators increase transparency and shorten decision cycles. Differentiated aesthetics and 10+ year warranties temper pure price comparisons.

Product differentiation and brand

Andersen’s strong brand and patented features (ENERGY STAR certified lines) support premium pricing and reduce buyer power; the company reported roughly $3B revenue in 2023 and ~13,000 employees, underscoring scale advantages. Look‑alike vinyl competitors narrow perceived differentiation, making service quality and a certified installer network decisive.

- Brand equity: supports premium pricing

- Patents/energy ratings: defensibility (ENERGY STAR)

- Look‑alikes: compress gaps

- Installer/service: key tie‑breaker

Switching and installation costs

Changing brands often requires retraining installers and adapting to different sizes and hardware, and in 2024 tight labor markets and schedule pressure made costly callbacks and delays more impactful, creating practical friction that moderates buyer bargaining. Standardized openings and common SKUs, however, limit supplier lock-in in many retrofit and new-build segments.

- Installer retraining raises switching friction

- Callbacks and delays amplify cost sensitivity

- Standard SKUs reduce lock-in in some segments

Retail giants 60% share squeeze margins; remodelers $420B seek warranties

Large retailers (Home Depot/Lowe's ~60% U.S. share in 2024) and big builders exert strong price and terms pressure; remodelers (U.S. remodeling spend ~$420B in 2024) are price-sensitive but seek warranties; Andersen (≈$3B revenue in 2023, ~13,000 employees) offsets pressure with brand, ENERGY STAR lines and installer networks, though vinyl look‑alikes compress differentiation.

| Buyer segment | 2024 metric | Bargaining power |

|---|---|---|

| Retail chains | 60% market control | High |

| Builders | Tiered rebates | High |

| Remodelers | $420B spend | Medium |

| Andersen | $3B rev, 13k emp | Moderate defense |

Preview Before You Purchase

Andersen Corporation Porter's Five Forces Analysis

This preview shows the exact Andersen Corporation Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the full, professionally formatted analysis, ready for download and use the moment you buy. You're viewing the final deliverable, instantly accessible upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Andersen Corporation faces moderate buyer power, concentrated suppliers for specialized materials, steady rivalry among established manufacturers, manageable threats from substitutes, and entry barriers driven by scale and distribution. This snapshot highlights key competitive dynamics and strategic pressures. Ready for deeper, data-driven insights? Unlock the full Porter's Five Forces Analysis to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration in key inputs

Concentration among glass, resins/vinyl, wood, aluminum and hardware suppliers gives these vendors elevated leverage over pricing and allocations, pressuring Andersen’s margins. Insulated glass units and low-E coatings come from specialized vendors, so disruptions can quickly ripple through capacity planning and delivery times. Andersen mitigates risk through multi-sourcing and inventory buffers but remains exposed on specialty components.

Specialized technology components

High-performance glazing, coatings, seals and hardware for Andersen require tight specs and certifications, giving suppliers of proprietary chemistries or tooling leverage to command premiums. Switching suppliers triggers lengthy requalification, testing and potential warranty exposure, raising switching costs. Dependence on niche suppliers therefore elevates their bargaining power in Andersen’s supply chain.

Logistics and energy sensitivity

Transportation, energy, and commodity volatility pass through supplier quotes, with fuel surcharges averaging about 8% of freight invoices in 2024 and diesel retail prices near $3.90/gal (EIA 2024). Bulky, fragile glass increases handling costs and drives damage claims—industry data showed glass-related claims around 2% of shipments in 2024. Lane scarcity and surge pricing can lift spot rates 15–30% quickly, while suppliers used lead-time control to extend transit windows by roughly 15% in tight markets.

Switching costs and requalification

Revalidating suppliers for Andersen requires ASTM/AAMA testing cycles often taking 4–12 weeks, third-party audits, and line requalification, creating lead-time and cost barriers. Tooling and die investments commonly exceed $100,000 per part, locking production to incumbent vendors. Warranty and long-term performance commitments tie Andersen to suppliers, discouraging rapid supplier changes and raising supplier bargaining power.

- Testing lead-time: 4–12 weeks

- Tooling cost: >$100,000 per part

- Audit/requalification: third-party required

- Warranty ties: multi-year obligations

Sustainability and certified materials

Sustainability requirements — FSC wood, low‑VOC components and energy‑efficient glass — shrink Andersen Corporation’s qualified supplier pool, raising procurement complexity and costs; industry premiums for certified materials commonly range 5–15% and Andersen’s scale (~$2.5B revenue) increases reliance on a narrower set of vetted vendors. Environmental traceability mandates add compliance burden, but preferred green suppliers can secure stronger commercial terms while sustainability alignment fosters deeper strategic partnerships over time.

- FSC wood narrows sources

- Low‑VOC & glass raise costs 5–15%

- Traceability adds compliance complexity

- Preferred green suppliers gain negotiating power

- Long‑term partnerships improve supply stability

Concentrated suppliers, tooling >$100,000 and 4-12 week testing raise costs and barriers

Concentrated suppliers for glass, coatings, hardware and FSC wood give vendors strong leverage, pressuring Andersen’s margins despite multi-sourcing; tooling costs >$100,000 and ASTM/AAMA tests (4–12 weeks) raise switching costs. Commodity and transport pass‑throughs (fuel surcharge ~8%, diesel ~$3.90/gal) plus certified-material premiums (5–15%) further boost supplier power.

| Metric | Value |

|---|---|

| Revenue | $2.5B |

| Tooling cost | >$100,000/part |

| Testing lead-time | 4–12 weeks |

| Fuel surcharge | ~8% |

| Diesel (2024) | $3.90/gal |

| Certified premium | 5–15% |

| Glass claims | ~2% shipments |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, highlighting Andersen Corporation's strengths in brand, scale, distribution and innovation, plus supplier relationships and customer dynamics that shape pricing, margins and strategic vulnerability.

A concise, one-sheet Porter's Five Forces for Andersen Corporation that instantly highlights supplier power, buyer leverage, substitute and entrant threats, and competitive rivalry—streamlining strategic decisions and boardroom discussions.

Customers Bargaining Power

Channel leverage of big retailers

Large home-improvement chains exert pricing, placement and payment-term pressure on Andersen; Home Depot and Lowe's together control roughly 60% of U.S. home-improvement retail (2024), giving them scale to demand lower prices and favorable terms. Their volume enables aggressive private-label threats and bargaining on assortment. Slotting, returns and merchandising demands raise supplier costs. Andersen offsets this with strong brand pull and product differentiation.

Professional builders and contractors

Professional builders buy windows in large volumes and in 2024 negotiated rebates and tiered discounts, leveraging purchase scale to squeeze unit pricing. They prioritize on-time delivery, reliable service and consistent specs, creating strong switching inertia that benefits incumbent suppliers. Competitive bid processes keep margin pressure high, while approved vendor lists can both lock in suppliers and lock out competitors, concentrating purchasing power among a few large builders.

End-customer price sensitivity

Remodeling and replacement buyers weigh performance versus budget closely, with U.S. remodeling spending in 2024 near $420 billion driving price-conscious decisions. Promotions and point-of-sale financing (often covering 20–30% of projects) shift demand among brands. Online reviews and configurators increase transparency and shorten decision cycles. Differentiated aesthetics and 10+ year warranties temper pure price comparisons.

Product differentiation and brand

Andersen’s strong brand and patented features (ENERGY STAR certified lines) support premium pricing and reduce buyer power; the company reported roughly $3B revenue in 2023 and ~13,000 employees, underscoring scale advantages. Look‑alike vinyl competitors narrow perceived differentiation, making service quality and a certified installer network decisive.

- Brand equity: supports premium pricing

- Patents/energy ratings: defensibility (ENERGY STAR)

- Look‑alikes: compress gaps

- Installer/service: key tie‑breaker

Switching and installation costs

Changing brands often requires retraining installers and adapting to different sizes and hardware, and in 2024 tight labor markets and schedule pressure made costly callbacks and delays more impactful, creating practical friction that moderates buyer bargaining. Standardized openings and common SKUs, however, limit supplier lock-in in many retrofit and new-build segments.

- Installer retraining raises switching friction

- Callbacks and delays amplify cost sensitivity

- Standard SKUs reduce lock-in in some segments

Retail giants 60% share squeeze margins; remodelers $420B seek warranties

Large retailers (Home Depot/Lowe's ~60% U.S. share in 2024) and big builders exert strong price and terms pressure; remodelers (U.S. remodeling spend ~$420B in 2024) are price-sensitive but seek warranties; Andersen (≈$3B revenue in 2023, ~13,000 employees) offsets pressure with brand, ENERGY STAR lines and installer networks, though vinyl look‑alikes compress differentiation.

| Buyer segment | 2024 metric | Bargaining power |

|---|---|---|

| Retail chains | 60% market control | High |

| Builders | Tiered rebates | High |

| Remodelers | $420B spend | Medium |

| Andersen | $3B rev, 13k emp | Moderate defense |

Preview Before You Purchase

Andersen Corporation Porter's Five Forces Analysis

This preview shows the exact Andersen Corporation Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the full, professionally formatted analysis, ready for download and use the moment you buy. You're viewing the final deliverable, instantly accessible upon payment.