Angi PESTLE Analysis

Skip the Research. Get the Strategy.

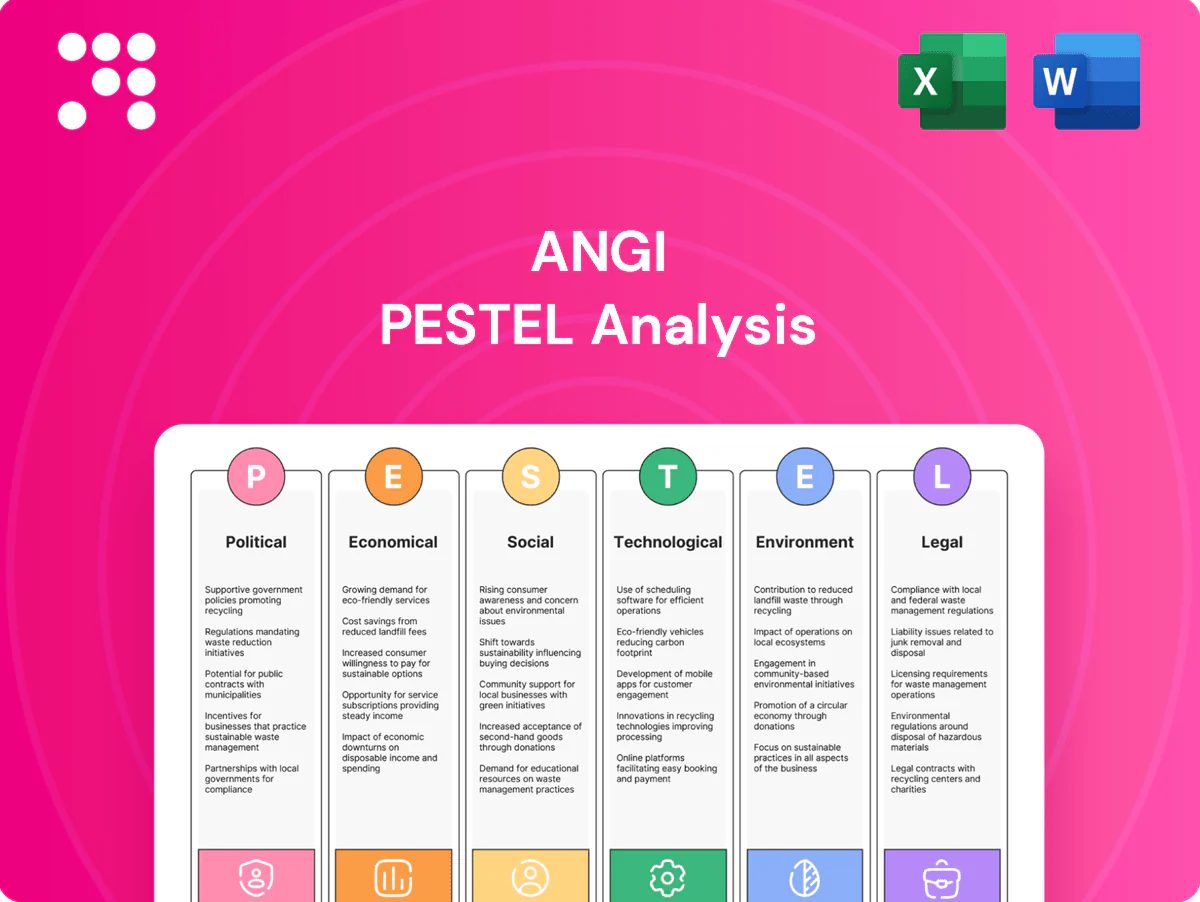

Unlock strategic advantage with our targeted PESTLE analysis of Angi. We map political, economic, social, technological, legal, and environmental forces shaping its growth and risks. Ideal for investors, advisors, and strategy teams seeking actionable insights. Download the full report now for the complete intelligence you need.

Political factors

Local housing and permitting policies

City and state permitting timelines and housing codes directly affect Angi by shaping project demand and completion risk; U.S. jurisdictions adopting e-permitting reported approval-time reductions of up to 30% in pilot studies through 2024, speeding bookings and reducing contractor idle time.

Contractor licensing and enforcement priorities

State-level shifts in contractor licensing reshape Angi’s addressable pro base and vetting costs; US construction employment was about 7.6 million in 2024 (BLS), so tighter rules could meaningfully cut supply. Strong enforcement tends to boost service quality but can raise prices. Greater reciprocity across states reduces onboarding friction for multi-state pros. Angi must update verification workflows as rules evolve.

Public infrastructure and home resilience funding

IRA's roughly $369 billion in clean energy tax credits and the $1.2 trillion Bipartisan Infrastructure Law have spurred demand on Angi for HVAC, insulation and electrification projects by subsidizing upgrades. Federal/state weatherization and energy-efficiency grants channel subsidy-driven leads that targeted campaigns can capture. Anticipated policy roll-offs create demand cliffs requiring rapid service-mix shifts to sustain revenue.

Small business support and taxation

Tax credits, expanded SBA lending (SBA guaranteed lending topped $30B in FY2024) and contractor relief programs have improved liquidity and capacity for Angi’s supply-side partners, boosting service participation and marketing spend on the platform.

New payroll and proposed digital services taxes in several U.S. jurisdictions increase operating costs and compress Angi’s take rate; sustained advocacy is key to preserving a healthy local‑services ecosystem and platform economics.

- SBA lending: >$30B (FY2024)

- Effect: higher supply participation and marketing spend

- Risk: payroll/digital services taxes pressure take rate

- Mitigation: industry advocacy to protect local services

Trade and tariff impacts on materials

Tariffs on lumber, steel and fixtures raise project costs and can deter homeowners—US Section 232 steel tariffs remain at 25% and aluminum at 10%, while Canadian softwood duties have ranged up to ~20%—increasing bid prices and reducing willingness to proceed. Volatile material pricing complicates fixed-price quotes and completion rates. Sourcing diversification and clear, timely cost-driver communication help reduce cancellations.

- 25% US steel tariff

- 10% US aluminum tariff

- Softwood duties up to ~20%

- Supplier diversification lowers import exposure

- Transparent cost drivers cut cancellation risk

E-permits cut approvals 30%; IRA/BIL subsidies spur retrofit demand

Permitting reform (e-permits cut approvals up to 30% in pilots) and state licensing changes (US construction employment ~7.6M in 2024) alter Angi’s supply and booking speed. IRA ($369B) and BIL ($1.2T) subsidies drive retrofit demand while SBA lending (> $30B FY2024) boosts pro capacity; tariffs (US steel 25%, aluminum 10%, softwood ~20%) raise costs and cancellations.

| Factor | Key number |

|---|---|

| E-permits | -30% approval time |

| Construction jobs | 7.6M (2024) |

| IRA/BIL | $369B / $1.2T |

| SBA lending | >$30B (FY24) |

| Tariffs | Steel 25% / Al 10% / Softwood ~20% |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Angi, with data-backed trends and forward-looking insights to help executives, investors, and strategists identify risks and opportunities.

A compact, visually segmented PESTLE summary for Angi that simplifies external risk assessment and market positioning, easily dropped into presentations or shared across teams for quick alignment and decision-making.

Economic factors

Housing cycle and home equity

Home price appreciation and record tappable equity—CoreLogic reported tappable equity exceeded 10 trillion USD in 2023—correlate with larger-ticket remodeling spend, boosting average project values. Downturns or negative equity reduce discretionary projects and pivot demand toward repairs. Angi can prioritize essential services during slow cycles to stabilize volumes. Targeted marketing and point-of-sale financing in equity-rich metros can lift conversions.

Interest rates and financing availability

Higher 30-year mortgage and HELOC rates—around 6.7% for the 30-year fixed in mid-2025 after a ~7.8% peak in 2023—suppress move-up buying and large remodels while shifting demand to repair/maintenance. Rate cuts historically revive renovation intent and lift conversion on bigger projects. Embedded checkout financing, which can boost conversion by up to 25% per industry reports, helps offset macro headwinds. Sensitivity testing of price and rate scenarios guides category investment.

Labor availability and wage inflation

Skilled-trades shortages elevate labor costs and extend lead times for Angi, with NAHB reporting 78% of builders faced staffing shortages and BLS showing construction average hourly earnings up about 5.1% year-over-year in 2024, increasing cancellations and lower satisfaction. Wage inflation pressures pros to raise prices, reducing conversion rates on leads. Supply-building initiatives and schedule optimization can trim lead times, while transparent pricing tools set clear homeowner expectations and reduce churn.

Consumer confidence and discretionary spend

Consumer confidence dips reduce bookings for non-urgent projects and raise price sensitivity, while promotions and fixed-price SKUs help maintain throughput; strong labor markets and housing/wealth effects unlock upsell opportunities. Category elasticity dictates where Angi should allocate marketing ROI to maximize conversion and margin.

- Confidence dips → fewer non-urgent bookings; higher price sensitivity

- Promotions & fixed-price SKUs preserve throughput

- Labor market strength (US unemployment ~3.7% mid-2025) + housing wealth aid upsells

- Category elasticity guides marketing ROI allocation

SMB advertising and CAC dynamics

Local pros cut ad budgets in recessions, pressuring Angi’s lead-gen revenue, while performance-based pricing and ROI dashboards have kept retention higher by linking spend to outcomes; diversifying into direct bookings and subscriptions reduces cyclicality, and lower CAC windows in downturns enable efficient share gains.

E-permits cut approvals 30%; IRA/BIL subsidies spur retrofit demand

High tappable equity (>$10T in 2023) and housing wealth lift remodeling spend, while 30-year rates ~6.7% mid-2025 curb large projects; unemployment ~3.7% (mid-2025) supports maintenance demand. Skilled-trade shortages (78% builders) and construction wages +5.1% YoY (2024) raise costs, pressuring pros' ad budgets and Angi lead revenue.

| Metric | Value |

|---|---|

| Tappable equity | >$10T (2023) |

| 30-yr mortgage | ~6.7% (mid-2025) |

| Unemployment | ~3.7% (mid-2025) |

| Wage inflation | +5.1% YoY (2024) |

| Builders with shortages | 78% (NAHB) |

Preview the Actual Deliverable

Angi PESTLE Analysis

The preview shown here is the exact Angi PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. After checkout you’ll instantly receive this finished, professionally structured report.

Skip the Research. Get the Strategy.

Unlock strategic advantage with our targeted PESTLE analysis of Angi. We map political, economic, social, technological, legal, and environmental forces shaping its growth and risks. Ideal for investors, advisors, and strategy teams seeking actionable insights. Download the full report now for the complete intelligence you need.

Political factors

Local housing and permitting policies

City and state permitting timelines and housing codes directly affect Angi by shaping project demand and completion risk; U.S. jurisdictions adopting e-permitting reported approval-time reductions of up to 30% in pilot studies through 2024, speeding bookings and reducing contractor idle time.

Contractor licensing and enforcement priorities

State-level shifts in contractor licensing reshape Angi’s addressable pro base and vetting costs; US construction employment was about 7.6 million in 2024 (BLS), so tighter rules could meaningfully cut supply. Strong enforcement tends to boost service quality but can raise prices. Greater reciprocity across states reduces onboarding friction for multi-state pros. Angi must update verification workflows as rules evolve.

Public infrastructure and home resilience funding

IRA's roughly $369 billion in clean energy tax credits and the $1.2 trillion Bipartisan Infrastructure Law have spurred demand on Angi for HVAC, insulation and electrification projects by subsidizing upgrades. Federal/state weatherization and energy-efficiency grants channel subsidy-driven leads that targeted campaigns can capture. Anticipated policy roll-offs create demand cliffs requiring rapid service-mix shifts to sustain revenue.

Small business support and taxation

Tax credits, expanded SBA lending (SBA guaranteed lending topped $30B in FY2024) and contractor relief programs have improved liquidity and capacity for Angi’s supply-side partners, boosting service participation and marketing spend on the platform.

New payroll and proposed digital services taxes in several U.S. jurisdictions increase operating costs and compress Angi’s take rate; sustained advocacy is key to preserving a healthy local‑services ecosystem and platform economics.

- SBA lending: >$30B (FY2024)

- Effect: higher supply participation and marketing spend

- Risk: payroll/digital services taxes pressure take rate

- Mitigation: industry advocacy to protect local services

Trade and tariff impacts on materials

Tariffs on lumber, steel and fixtures raise project costs and can deter homeowners—US Section 232 steel tariffs remain at 25% and aluminum at 10%, while Canadian softwood duties have ranged up to ~20%—increasing bid prices and reducing willingness to proceed. Volatile material pricing complicates fixed-price quotes and completion rates. Sourcing diversification and clear, timely cost-driver communication help reduce cancellations.

- 25% US steel tariff

- 10% US aluminum tariff

- Softwood duties up to ~20%

- Supplier diversification lowers import exposure

- Transparent cost drivers cut cancellation risk

E-permits cut approvals 30%; IRA/BIL subsidies spur retrofit demand

Permitting reform (e-permits cut approvals up to 30% in pilots) and state licensing changes (US construction employment ~7.6M in 2024) alter Angi’s supply and booking speed. IRA ($369B) and BIL ($1.2T) subsidies drive retrofit demand while SBA lending (> $30B FY2024) boosts pro capacity; tariffs (US steel 25%, aluminum 10%, softwood ~20%) raise costs and cancellations.

| Factor | Key number |

|---|---|

| E-permits | -30% approval time |

| Construction jobs | 7.6M (2024) |

| IRA/BIL | $369B / $1.2T |

| SBA lending | >$30B (FY24) |

| Tariffs | Steel 25% / Al 10% / Softwood ~20% |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Angi, with data-backed trends and forward-looking insights to help executives, investors, and strategists identify risks and opportunities.

A compact, visually segmented PESTLE summary for Angi that simplifies external risk assessment and market positioning, easily dropped into presentations or shared across teams for quick alignment and decision-making.

Economic factors

Housing cycle and home equity

Home price appreciation and record tappable equity—CoreLogic reported tappable equity exceeded 10 trillion USD in 2023—correlate with larger-ticket remodeling spend, boosting average project values. Downturns or negative equity reduce discretionary projects and pivot demand toward repairs. Angi can prioritize essential services during slow cycles to stabilize volumes. Targeted marketing and point-of-sale financing in equity-rich metros can lift conversions.

Interest rates and financing availability

Higher 30-year mortgage and HELOC rates—around 6.7% for the 30-year fixed in mid-2025 after a ~7.8% peak in 2023—suppress move-up buying and large remodels while shifting demand to repair/maintenance. Rate cuts historically revive renovation intent and lift conversion on bigger projects. Embedded checkout financing, which can boost conversion by up to 25% per industry reports, helps offset macro headwinds. Sensitivity testing of price and rate scenarios guides category investment.

Labor availability and wage inflation

Skilled-trades shortages elevate labor costs and extend lead times for Angi, with NAHB reporting 78% of builders faced staffing shortages and BLS showing construction average hourly earnings up about 5.1% year-over-year in 2024, increasing cancellations and lower satisfaction. Wage inflation pressures pros to raise prices, reducing conversion rates on leads. Supply-building initiatives and schedule optimization can trim lead times, while transparent pricing tools set clear homeowner expectations and reduce churn.

Consumer confidence and discretionary spend

Consumer confidence dips reduce bookings for non-urgent projects and raise price sensitivity, while promotions and fixed-price SKUs help maintain throughput; strong labor markets and housing/wealth effects unlock upsell opportunities. Category elasticity dictates where Angi should allocate marketing ROI to maximize conversion and margin.

- Confidence dips → fewer non-urgent bookings; higher price sensitivity

- Promotions & fixed-price SKUs preserve throughput

- Labor market strength (US unemployment ~3.7% mid-2025) + housing wealth aid upsells

- Category elasticity guides marketing ROI allocation

SMB advertising and CAC dynamics

Local pros cut ad budgets in recessions, pressuring Angi’s lead-gen revenue, while performance-based pricing and ROI dashboards have kept retention higher by linking spend to outcomes; diversifying into direct bookings and subscriptions reduces cyclicality, and lower CAC windows in downturns enable efficient share gains.

E-permits cut approvals 30%; IRA/BIL subsidies spur retrofit demand

High tappable equity (>$10T in 2023) and housing wealth lift remodeling spend, while 30-year rates ~6.7% mid-2025 curb large projects; unemployment ~3.7% (mid-2025) supports maintenance demand. Skilled-trade shortages (78% builders) and construction wages +5.1% YoY (2024) raise costs, pressuring pros' ad budgets and Angi lead revenue.

| Metric | Value |

|---|---|

| Tappable equity | >$10T (2023) |

| 30-yr mortgage | ~6.7% (mid-2025) |

| Unemployment | ~3.7% (mid-2025) |

| Wage inflation | +5.1% YoY (2024) |

| Builders with shortages | 78% (NAHB) |

Preview the Actual Deliverable

Angi PESTLE Analysis

The preview shown here is the exact Angi PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. After checkout you’ll instantly receive this finished, professionally structured report.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic advantage with our targeted PESTLE analysis of Angi. We map political, economic, social, technological, legal, and environmental forces shaping its growth and risks. Ideal for investors, advisors, and strategy teams seeking actionable insights. Download the full report now for the complete intelligence you need.

Political factors

Local housing and permitting policies

City and state permitting timelines and housing codes directly affect Angi by shaping project demand and completion risk; U.S. jurisdictions adopting e-permitting reported approval-time reductions of up to 30% in pilot studies through 2024, speeding bookings and reducing contractor idle time.

Contractor licensing and enforcement priorities

State-level shifts in contractor licensing reshape Angi’s addressable pro base and vetting costs; US construction employment was about 7.6 million in 2024 (BLS), so tighter rules could meaningfully cut supply. Strong enforcement tends to boost service quality but can raise prices. Greater reciprocity across states reduces onboarding friction for multi-state pros. Angi must update verification workflows as rules evolve.

Public infrastructure and home resilience funding

IRA's roughly $369 billion in clean energy tax credits and the $1.2 trillion Bipartisan Infrastructure Law have spurred demand on Angi for HVAC, insulation and electrification projects by subsidizing upgrades. Federal/state weatherization and energy-efficiency grants channel subsidy-driven leads that targeted campaigns can capture. Anticipated policy roll-offs create demand cliffs requiring rapid service-mix shifts to sustain revenue.

Small business support and taxation

Tax credits, expanded SBA lending (SBA guaranteed lending topped $30B in FY2024) and contractor relief programs have improved liquidity and capacity for Angi’s supply-side partners, boosting service participation and marketing spend on the platform.

New payroll and proposed digital services taxes in several U.S. jurisdictions increase operating costs and compress Angi’s take rate; sustained advocacy is key to preserving a healthy local‑services ecosystem and platform economics.

- SBA lending: >$30B (FY2024)

- Effect: higher supply participation and marketing spend

- Risk: payroll/digital services taxes pressure take rate

- Mitigation: industry advocacy to protect local services

Trade and tariff impacts on materials

Tariffs on lumber, steel and fixtures raise project costs and can deter homeowners—US Section 232 steel tariffs remain at 25% and aluminum at 10%, while Canadian softwood duties have ranged up to ~20%—increasing bid prices and reducing willingness to proceed. Volatile material pricing complicates fixed-price quotes and completion rates. Sourcing diversification and clear, timely cost-driver communication help reduce cancellations.

- 25% US steel tariff

- 10% US aluminum tariff

- Softwood duties up to ~20%

- Supplier diversification lowers import exposure

- Transparent cost drivers cut cancellation risk

E-permits cut approvals 30%; IRA/BIL subsidies spur retrofit demand

Permitting reform (e-permits cut approvals up to 30% in pilots) and state licensing changes (US construction employment ~7.6M in 2024) alter Angi’s supply and booking speed. IRA ($369B) and BIL ($1.2T) subsidies drive retrofit demand while SBA lending (> $30B FY2024) boosts pro capacity; tariffs (US steel 25%, aluminum 10%, softwood ~20%) raise costs and cancellations.

| Factor | Key number |

|---|---|

| E-permits | -30% approval time |

| Construction jobs | 7.6M (2024) |

| IRA/BIL | $369B / $1.2T |

| SBA lending | >$30B (FY24) |

| Tariffs | Steel 25% / Al 10% / Softwood ~20% |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely impact Angi, with data-backed trends and forward-looking insights to help executives, investors, and strategists identify risks and opportunities.

A compact, visually segmented PESTLE summary for Angi that simplifies external risk assessment and market positioning, easily dropped into presentations or shared across teams for quick alignment and decision-making.

Economic factors

Housing cycle and home equity

Home price appreciation and record tappable equity—CoreLogic reported tappable equity exceeded 10 trillion USD in 2023—correlate with larger-ticket remodeling spend, boosting average project values. Downturns or negative equity reduce discretionary projects and pivot demand toward repairs. Angi can prioritize essential services during slow cycles to stabilize volumes. Targeted marketing and point-of-sale financing in equity-rich metros can lift conversions.

Interest rates and financing availability

Higher 30-year mortgage and HELOC rates—around 6.7% for the 30-year fixed in mid-2025 after a ~7.8% peak in 2023—suppress move-up buying and large remodels while shifting demand to repair/maintenance. Rate cuts historically revive renovation intent and lift conversion on bigger projects. Embedded checkout financing, which can boost conversion by up to 25% per industry reports, helps offset macro headwinds. Sensitivity testing of price and rate scenarios guides category investment.

Labor availability and wage inflation

Skilled-trades shortages elevate labor costs and extend lead times for Angi, with NAHB reporting 78% of builders faced staffing shortages and BLS showing construction average hourly earnings up about 5.1% year-over-year in 2024, increasing cancellations and lower satisfaction. Wage inflation pressures pros to raise prices, reducing conversion rates on leads. Supply-building initiatives and schedule optimization can trim lead times, while transparent pricing tools set clear homeowner expectations and reduce churn.

Consumer confidence and discretionary spend

Consumer confidence dips reduce bookings for non-urgent projects and raise price sensitivity, while promotions and fixed-price SKUs help maintain throughput; strong labor markets and housing/wealth effects unlock upsell opportunities. Category elasticity dictates where Angi should allocate marketing ROI to maximize conversion and margin.

- Confidence dips → fewer non-urgent bookings; higher price sensitivity

- Promotions & fixed-price SKUs preserve throughput

- Labor market strength (US unemployment ~3.7% mid-2025) + housing wealth aid upsells

- Category elasticity guides marketing ROI allocation

SMB advertising and CAC dynamics

Local pros cut ad budgets in recessions, pressuring Angi’s lead-gen revenue, while performance-based pricing and ROI dashboards have kept retention higher by linking spend to outcomes; diversifying into direct bookings and subscriptions reduces cyclicality, and lower CAC windows in downturns enable efficient share gains.

E-permits cut approvals 30%; IRA/BIL subsidies spur retrofit demand

High tappable equity (>$10T in 2023) and housing wealth lift remodeling spend, while 30-year rates ~6.7% mid-2025 curb large projects; unemployment ~3.7% (mid-2025) supports maintenance demand. Skilled-trade shortages (78% builders) and construction wages +5.1% YoY (2024) raise costs, pressuring pros' ad budgets and Angi lead revenue.

| Metric | Value |

|---|---|

| Tappable equity | >$10T (2023) |

| 30-yr mortgage | ~6.7% (mid-2025) |

| Unemployment | ~3.7% (mid-2025) |

| Wage inflation | +5.1% YoY (2024) |

| Builders with shortages | 78% (NAHB) |

Preview the Actual Deliverable

Angi PESTLE Analysis

The preview shown here is the exact Angi PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. After checkout you’ll instantly receive this finished, professionally structured report.