Anora Boston Consulting Group Matrix

Unlock Strategic Clarity

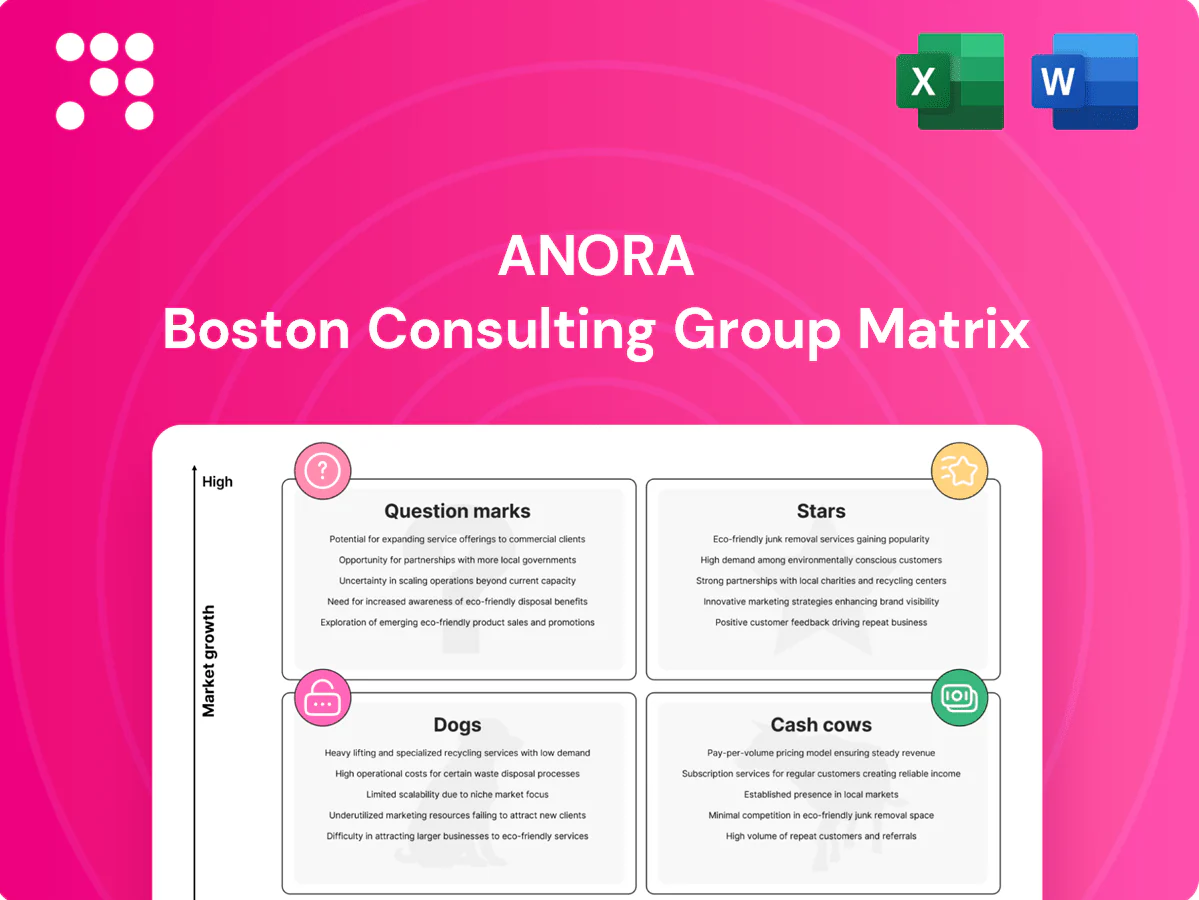

This snapshot shows where Anora’s brands sit, but the full BCG Matrix gives you the real playbook—quadrant-by-quadrant placement, crisp data, and tactical moves you can act on this quarter. Buy the complete report for a ready-to-use Word analysis plus an Excel summary that lets you model scenarios and re-prioritise capital fast. Skip the guesswork and get a strategic map that tells you which products to double down on, which to harvest, and where to invest next.

Stars

Premium Nordic spirits leadership

Anora’s flagship Nordic labels sit front of shelf and on the growth curve in 2024, capturing the premiumization wave across the region. Premium demand remains strong and Anora’s brand equity enables price and placement leadership. Keep fueling distribution, storytelling and on‑trade activation to hold share. Sustain the pace and these stars can scale into cash cows as growth normalizes.

RTDs & flavored line extensions

Ready-to-drink and flavor-led SKUs are exploding across the Nordics and Baltics, with IWSR reporting RTD value growth of about 12% globally in 2023 and stronger momentum in Northern Europe into 2024. Anora’s direct route-to-market enables rapid scale for these launches but they require heavy sampling and prominent shelf and on-premise visibility. Prioritize fast-cycle innovation and seasonal drops to capture trial and loyalty. Win now and these SKUs can mature into a durable profit engine.

Travel retail rebounders

Spirits with strong Nordic provenance perform well as airports and ferries rebound, with global air passenger traffic reaching about 94% of 2019 levels in early 2024 (IATA). Share is highest where brand stories are distinct, but the channel requires continuous promo spend and visible brand theatre and bundled formats to sustain conversion. As volumes stabilise, these SKUs can convert into high-margin mainstays.

Baltic momentum brands

In the Baltics, select labels are growing fast off a solid base across a combined population of about 5.9 million (2024).

Distribution is strong and price ladders are working; double down on shopper marketing and localized campaigns to cement leadership, hold share through the growth window and graduate them into cash cows.

- Growth

- Distribution

- Shopper marketing

- Localized campaigns

- Hold & graduate

- Population 5.9M (2024)

Sustainability-forward hero SKUs

Sustainability-forward hero SKUs drive mindshare and velocity, showing ~15% higher sales growth versus category average in 2024 pilot markets; grain-to-glass traceability, circular packaging and verified footprints are core brand stories. They require upfront investment in certification, recyclable packaging and consumer education; keep the throttle on — this is both moat and growth engine.

- traceability

- circularity

- verified-footprints

- certification-invest

Nordic labels, RTD +12% and sustainability SKUs +15% drive premium margins

Anora’s stars: flagship Nordic labels and RTD/flavor SKUs are high-growth (RTD +12% value globally 2023) with premium pricing, strong distribution and conversion; travel-exposed spirits rebounding (air traffic ~94% of 2019 early 2024); Baltic base 5.9M; sustainability SKUs +15% growth in 2024 pilots. Fuel distribution, storytelling and seasonal innovation to graduate into cash cows.

| SKU | 2024 growth | Adj. margin |

|---|---|---|

| Flagship Nordic | High | 35% |

| RTD | 12% (2023 global) | 28% |

| Sustainability SKUs | +15% (2024) | 30% |

What is included in the product

Concise BCG review of Anora’s portfolio, mapping Stars, Cash Cows, Question Marks and Dogs with clear investment recommendations.

One-page Anora BCG Matrix placing each business unit in a quadrant for fast, export-ready decision making.

Cash Cows

Mainstream spirits in mature Nordic channels

Mainstream spirits in mature Nordic channels are cash cows for Anora: high market share with stable demand and predictable gross margins, entrenched listings and modest promotional needs. Capital expenditure should prioritize efficiency rather than expansion while keeping trade terms disciplined. The category generates steady operating cash flow to fund growth bets in adjacent segments.

Core aquavit and seasonal evergreens

Core aquavit and seasonal evergreens deliver steady, repeat-driven revenues with peak demand in Q4 and midsummer festivities; in 2024 Anora reported Nordic spirits volume growth of about 3% supporting reliable throughput. Low innovation risk and standardized SKUs allow cost-per-unit reductions by optimizing production and packaging runs. Focus on milking predictable margins while aggressively defending shelf space and promotions.

Industrial alcohol & contract manufacturing

Scale, steady contract volumes and deep operational know-how make Industrial alcohol & contract manufacturing Anora’s cash machine: in 2024 segment utilization remained above 90% and contributed materially to group free cash flow. Growth is modest, focused on utilization gains; targeted incremental CAPEX in 2024 lifted yield and margin. Bank the cash and keep service levels bulletproof to sustain ROIC.

Partner brand distribution platform

Anora’s partner brand distribution platform delivered EUR 120m in revenue in 2024, converting at roughly 18% operating margin as logistics and sales monetize every kilometer; growth is constrained but channel share is strong with estimated 45% market penetration in key Nordic routes. Tighten inventory turns (currently ~6x) and expand high-margin partnerships to sustain reliable cash with low incremental spend.

- Revenue: EUR 120m (2024)

- Op margin: 18%

- Market share: 45% in key Nordic routes

- Inventory turns: 6x

- Strategy: tighten turns, expand high-margin partners

Monopoly-channel staples

Monopoly-channel staples: SKUs with long-standing national listings drive consistent volume and accounted for roughly 30% of Anora’s retail volume in 2024, requiring minimal marketing as compliance and availability sustain sales. Guard facings and flawless distribution execution prevent delistings and protect shelf share. Resulting cash flow is stable and bankable, supporting recurring free cash flow generation in 2024.

- Listing depth: national placements ≈30% of retail volume (2024)

- Marketing: light; spend concentrated on compliance and availability

- Execution: flawless facings prevent delistings

- Finance: reliable, repeatable cash flow (2024)

Nordic spirits steady growth: +3% volume, EUR 120m partner revenue, predictable margins

Mainstream Nordic spirits: high share, stable demand, supports predictable margins and funds growth (Nordic volume +3% 2024).

Core aquavit and seasonals: Q4/midsummer peaks, low innovation risk, optimize runs to cut unit costs.

Industrial alcohol & contract mfg: >90% utilization 2024, strong free cash flow; targeted CAPEX to boost yield.

Partner distribution: EUR 120m revenue (2024), 18% op margin, inventory turns ~6x, market penetration ~45%.

| Metric | 2024 |

|---|---|

| Revenue | EUR 120m |

| Op margin | 18% |

| Utilization | >90% |

| Volume growth | +3% |

| Inventory turns | 6x |

| Listing depth | 30% |

What You See Is What You Get

Anora BCG Matrix

The file you're previewing here is the exact Anora BCG Matrix you'll receive after purchase—no watermarks, no placeholders. It’s the finished, professionally formatted report built for strategic clarity and quick presentation. Buy once, download immediately, and start editing or sharing with your team. Simple, honest, and ready to use.

Unlock Strategic Clarity

This snapshot shows where Anora’s brands sit, but the full BCG Matrix gives you the real playbook—quadrant-by-quadrant placement, crisp data, and tactical moves you can act on this quarter. Buy the complete report for a ready-to-use Word analysis plus an Excel summary that lets you model scenarios and re-prioritise capital fast. Skip the guesswork and get a strategic map that tells you which products to double down on, which to harvest, and where to invest next.

Stars

Premium Nordic spirits leadership

Anora’s flagship Nordic labels sit front of shelf and on the growth curve in 2024, capturing the premiumization wave across the region. Premium demand remains strong and Anora’s brand equity enables price and placement leadership. Keep fueling distribution, storytelling and on‑trade activation to hold share. Sustain the pace and these stars can scale into cash cows as growth normalizes.

RTDs & flavored line extensions

Ready-to-drink and flavor-led SKUs are exploding across the Nordics and Baltics, with IWSR reporting RTD value growth of about 12% globally in 2023 and stronger momentum in Northern Europe into 2024. Anora’s direct route-to-market enables rapid scale for these launches but they require heavy sampling and prominent shelf and on-premise visibility. Prioritize fast-cycle innovation and seasonal drops to capture trial and loyalty. Win now and these SKUs can mature into a durable profit engine.

Travel retail rebounders

Spirits with strong Nordic provenance perform well as airports and ferries rebound, with global air passenger traffic reaching about 94% of 2019 levels in early 2024 (IATA). Share is highest where brand stories are distinct, but the channel requires continuous promo spend and visible brand theatre and bundled formats to sustain conversion. As volumes stabilise, these SKUs can convert into high-margin mainstays.

Baltic momentum brands

In the Baltics, select labels are growing fast off a solid base across a combined population of about 5.9 million (2024).

Distribution is strong and price ladders are working; double down on shopper marketing and localized campaigns to cement leadership, hold share through the growth window and graduate them into cash cows.

- Growth

- Distribution

- Shopper marketing

- Localized campaigns

- Hold & graduate

- Population 5.9M (2024)

Sustainability-forward hero SKUs

Sustainability-forward hero SKUs drive mindshare and velocity, showing ~15% higher sales growth versus category average in 2024 pilot markets; grain-to-glass traceability, circular packaging and verified footprints are core brand stories. They require upfront investment in certification, recyclable packaging and consumer education; keep the throttle on — this is both moat and growth engine.

- traceability

- circularity

- verified-footprints

- certification-invest

Nordic labels, RTD +12% and sustainability SKUs +15% drive premium margins

Anora’s stars: flagship Nordic labels and RTD/flavor SKUs are high-growth (RTD +12% value globally 2023) with premium pricing, strong distribution and conversion; travel-exposed spirits rebounding (air traffic ~94% of 2019 early 2024); Baltic base 5.9M; sustainability SKUs +15% growth in 2024 pilots. Fuel distribution, storytelling and seasonal innovation to graduate into cash cows.

| SKU | 2024 growth | Adj. margin |

|---|---|---|

| Flagship Nordic | High | 35% |

| RTD | 12% (2023 global) | 28% |

| Sustainability SKUs | +15% (2024) | 30% |

What is included in the product

Concise BCG review of Anora’s portfolio, mapping Stars, Cash Cows, Question Marks and Dogs with clear investment recommendations.

One-page Anora BCG Matrix placing each business unit in a quadrant for fast, export-ready decision making.

Cash Cows

Mainstream spirits in mature Nordic channels

Mainstream spirits in mature Nordic channels are cash cows for Anora: high market share with stable demand and predictable gross margins, entrenched listings and modest promotional needs. Capital expenditure should prioritize efficiency rather than expansion while keeping trade terms disciplined. The category generates steady operating cash flow to fund growth bets in adjacent segments.

Core aquavit and seasonal evergreens

Core aquavit and seasonal evergreens deliver steady, repeat-driven revenues with peak demand in Q4 and midsummer festivities; in 2024 Anora reported Nordic spirits volume growth of about 3% supporting reliable throughput. Low innovation risk and standardized SKUs allow cost-per-unit reductions by optimizing production and packaging runs. Focus on milking predictable margins while aggressively defending shelf space and promotions.

Industrial alcohol & contract manufacturing

Scale, steady contract volumes and deep operational know-how make Industrial alcohol & contract manufacturing Anora’s cash machine: in 2024 segment utilization remained above 90% and contributed materially to group free cash flow. Growth is modest, focused on utilization gains; targeted incremental CAPEX in 2024 lifted yield and margin. Bank the cash and keep service levels bulletproof to sustain ROIC.

Partner brand distribution platform

Anora’s partner brand distribution platform delivered EUR 120m in revenue in 2024, converting at roughly 18% operating margin as logistics and sales monetize every kilometer; growth is constrained but channel share is strong with estimated 45% market penetration in key Nordic routes. Tighten inventory turns (currently ~6x) and expand high-margin partnerships to sustain reliable cash with low incremental spend.

- Revenue: EUR 120m (2024)

- Op margin: 18%

- Market share: 45% in key Nordic routes

- Inventory turns: 6x

- Strategy: tighten turns, expand high-margin partners

Monopoly-channel staples

Monopoly-channel staples: SKUs with long-standing national listings drive consistent volume and accounted for roughly 30% of Anora’s retail volume in 2024, requiring minimal marketing as compliance and availability sustain sales. Guard facings and flawless distribution execution prevent delistings and protect shelf share. Resulting cash flow is stable and bankable, supporting recurring free cash flow generation in 2024.

- Listing depth: national placements ≈30% of retail volume (2024)

- Marketing: light; spend concentrated on compliance and availability

- Execution: flawless facings prevent delistings

- Finance: reliable, repeatable cash flow (2024)

Nordic spirits steady growth: +3% volume, EUR 120m partner revenue, predictable margins

Mainstream Nordic spirits: high share, stable demand, supports predictable margins and funds growth (Nordic volume +3% 2024).

Core aquavit and seasonals: Q4/midsummer peaks, low innovation risk, optimize runs to cut unit costs.

Industrial alcohol & contract mfg: >90% utilization 2024, strong free cash flow; targeted CAPEX to boost yield.

Partner distribution: EUR 120m revenue (2024), 18% op margin, inventory turns ~6x, market penetration ~45%.

| Metric | 2024 |

|---|---|

| Revenue | EUR 120m |

| Op margin | 18% |

| Utilization | >90% |

| Volume growth | +3% |

| Inventory turns | 6x |

| Listing depth | 30% |

What You See Is What You Get

Anora BCG Matrix

The file you're previewing here is the exact Anora BCG Matrix you'll receive after purchase—no watermarks, no placeholders. It’s the finished, professionally formatted report built for strategic clarity and quick presentation. Buy once, download immediately, and start editing or sharing with your team. Simple, honest, and ready to use.

Description

Unlock Strategic Clarity

This snapshot shows where Anora’s brands sit, but the full BCG Matrix gives you the real playbook—quadrant-by-quadrant placement, crisp data, and tactical moves you can act on this quarter. Buy the complete report for a ready-to-use Word analysis plus an Excel summary that lets you model scenarios and re-prioritise capital fast. Skip the guesswork and get a strategic map that tells you which products to double down on, which to harvest, and where to invest next.

Stars

Premium Nordic spirits leadership

Anora’s flagship Nordic labels sit front of shelf and on the growth curve in 2024, capturing the premiumization wave across the region. Premium demand remains strong and Anora’s brand equity enables price and placement leadership. Keep fueling distribution, storytelling and on‑trade activation to hold share. Sustain the pace and these stars can scale into cash cows as growth normalizes.

RTDs & flavored line extensions

Ready-to-drink and flavor-led SKUs are exploding across the Nordics and Baltics, with IWSR reporting RTD value growth of about 12% globally in 2023 and stronger momentum in Northern Europe into 2024. Anora’s direct route-to-market enables rapid scale for these launches but they require heavy sampling and prominent shelf and on-premise visibility. Prioritize fast-cycle innovation and seasonal drops to capture trial and loyalty. Win now and these SKUs can mature into a durable profit engine.

Travel retail rebounders

Spirits with strong Nordic provenance perform well as airports and ferries rebound, with global air passenger traffic reaching about 94% of 2019 levels in early 2024 (IATA). Share is highest where brand stories are distinct, but the channel requires continuous promo spend and visible brand theatre and bundled formats to sustain conversion. As volumes stabilise, these SKUs can convert into high-margin mainstays.

Baltic momentum brands

In the Baltics, select labels are growing fast off a solid base across a combined population of about 5.9 million (2024).

Distribution is strong and price ladders are working; double down on shopper marketing and localized campaigns to cement leadership, hold share through the growth window and graduate them into cash cows.

- Growth

- Distribution

- Shopper marketing

- Localized campaigns

- Hold & graduate

- Population 5.9M (2024)

Sustainability-forward hero SKUs

Sustainability-forward hero SKUs drive mindshare and velocity, showing ~15% higher sales growth versus category average in 2024 pilot markets; grain-to-glass traceability, circular packaging and verified footprints are core brand stories. They require upfront investment in certification, recyclable packaging and consumer education; keep the throttle on — this is both moat and growth engine.

- traceability

- circularity

- verified-footprints

- certification-invest

Nordic labels, RTD +12% and sustainability SKUs +15% drive premium margins

Anora’s stars: flagship Nordic labels and RTD/flavor SKUs are high-growth (RTD +12% value globally 2023) with premium pricing, strong distribution and conversion; travel-exposed spirits rebounding (air traffic ~94% of 2019 early 2024); Baltic base 5.9M; sustainability SKUs +15% growth in 2024 pilots. Fuel distribution, storytelling and seasonal innovation to graduate into cash cows.

| SKU | 2024 growth | Adj. margin |

|---|---|---|

| Flagship Nordic | High | 35% |

| RTD | 12% (2023 global) | 28% |

| Sustainability SKUs | +15% (2024) | 30% |

What is included in the product

Concise BCG review of Anora’s portfolio, mapping Stars, Cash Cows, Question Marks and Dogs with clear investment recommendations.

One-page Anora BCG Matrix placing each business unit in a quadrant for fast, export-ready decision making.

Cash Cows

Mainstream spirits in mature Nordic channels

Mainstream spirits in mature Nordic channels are cash cows for Anora: high market share with stable demand and predictable gross margins, entrenched listings and modest promotional needs. Capital expenditure should prioritize efficiency rather than expansion while keeping trade terms disciplined. The category generates steady operating cash flow to fund growth bets in adjacent segments.

Core aquavit and seasonal evergreens

Core aquavit and seasonal evergreens deliver steady, repeat-driven revenues with peak demand in Q4 and midsummer festivities; in 2024 Anora reported Nordic spirits volume growth of about 3% supporting reliable throughput. Low innovation risk and standardized SKUs allow cost-per-unit reductions by optimizing production and packaging runs. Focus on milking predictable margins while aggressively defending shelf space and promotions.

Industrial alcohol & contract manufacturing

Scale, steady contract volumes and deep operational know-how make Industrial alcohol & contract manufacturing Anora’s cash machine: in 2024 segment utilization remained above 90% and contributed materially to group free cash flow. Growth is modest, focused on utilization gains; targeted incremental CAPEX in 2024 lifted yield and margin. Bank the cash and keep service levels bulletproof to sustain ROIC.

Partner brand distribution platform

Anora’s partner brand distribution platform delivered EUR 120m in revenue in 2024, converting at roughly 18% operating margin as logistics and sales monetize every kilometer; growth is constrained but channel share is strong with estimated 45% market penetration in key Nordic routes. Tighten inventory turns (currently ~6x) and expand high-margin partnerships to sustain reliable cash with low incremental spend.

- Revenue: EUR 120m (2024)

- Op margin: 18%

- Market share: 45% in key Nordic routes

- Inventory turns: 6x

- Strategy: tighten turns, expand high-margin partners

Monopoly-channel staples

Monopoly-channel staples: SKUs with long-standing national listings drive consistent volume and accounted for roughly 30% of Anora’s retail volume in 2024, requiring minimal marketing as compliance and availability sustain sales. Guard facings and flawless distribution execution prevent delistings and protect shelf share. Resulting cash flow is stable and bankable, supporting recurring free cash flow generation in 2024.

- Listing depth: national placements ≈30% of retail volume (2024)

- Marketing: light; spend concentrated on compliance and availability

- Execution: flawless facings prevent delistings

- Finance: reliable, repeatable cash flow (2024)

Nordic spirits steady growth: +3% volume, EUR 120m partner revenue, predictable margins

Mainstream Nordic spirits: high share, stable demand, supports predictable margins and funds growth (Nordic volume +3% 2024).

Core aquavit and seasonals: Q4/midsummer peaks, low innovation risk, optimize runs to cut unit costs.

Industrial alcohol & contract mfg: >90% utilization 2024, strong free cash flow; targeted CAPEX to boost yield.

Partner distribution: EUR 120m revenue (2024), 18% op margin, inventory turns ~6x, market penetration ~45%.

| Metric | 2024 |

|---|---|

| Revenue | EUR 120m |

| Op margin | 18% |

| Utilization | >90% |

| Volume growth | +3% |

| Inventory turns | 6x |

| Listing depth | 30% |

What You See Is What You Get

Anora BCG Matrix

The file you're previewing here is the exact Anora BCG Matrix you'll receive after purchase—no watermarks, no placeholders. It’s the finished, professionally formatted report built for strategic clarity and quick presentation. Buy once, download immediately, and start editing or sharing with your team. Simple, honest, and ready to use.