Anora Porter's Five Forces Analysis

From Overview to Strategy Blueprint

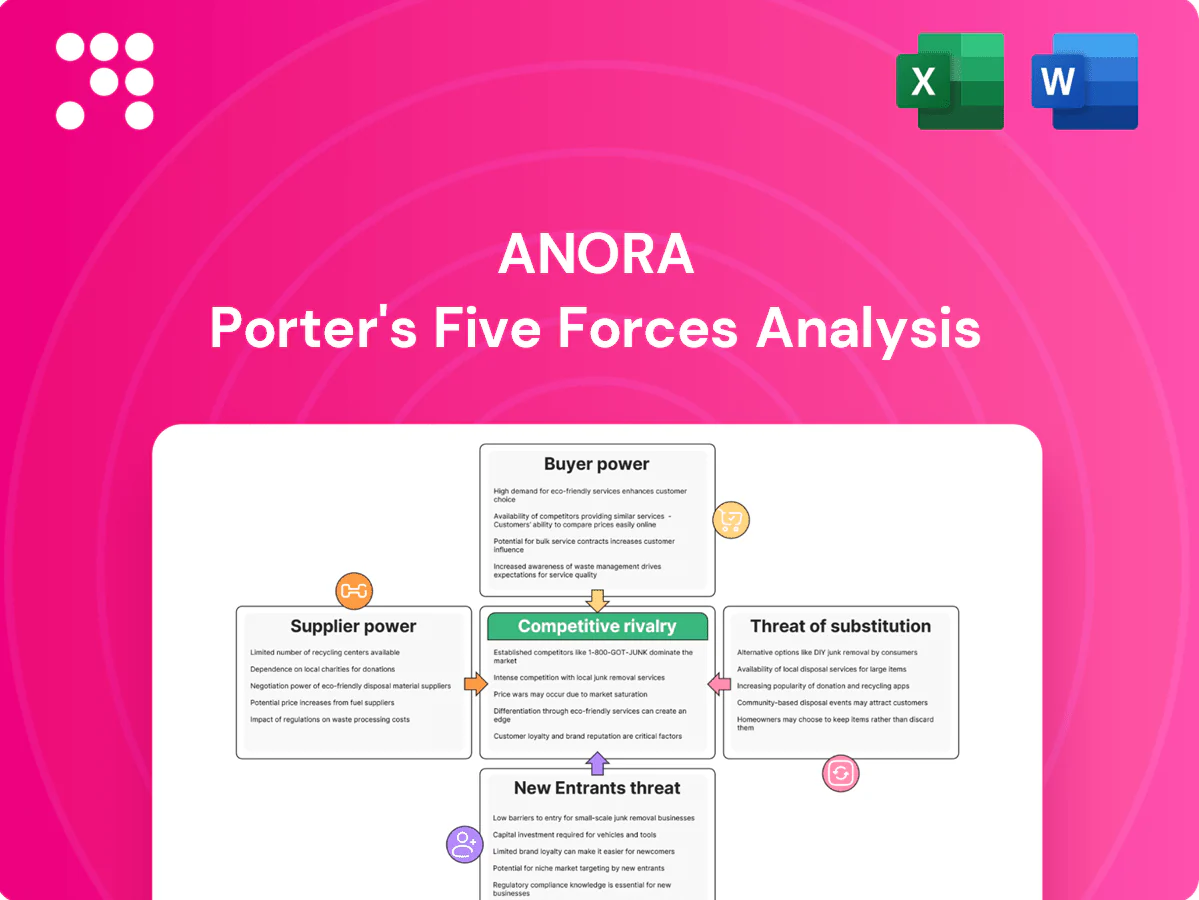

Anora’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes, and industry rivalry—all key to assessing strategic risk and value creation. This brief view outlines immediate pressures and strategic levers for Anora’s market position. Unlock the full Porter's Five Forces Analysis to explore Anora’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented agricultural inputs

Anora sources grains, grapes, botanicals and sugar from a wide base of farmers and growers, keeping individual supplier power relatively low. Commoditized grain and neutral spirit inputs remain widely substitutable across suppliers, reducing bargaining leverage. Premium appellation wines and specialty botanicals tighten options and can raise supplier leverage. Climate variability in 2024 produced periodic yield shocks that temporarily elevated supplier influence.

Concentrated packaging and glass

European container glass remains concentrated among Ardagh, Verallia, Vetropack and Owens-Illinois; closures and limited new capacity since 2022, plus energy-cost shocks, have tightened supply and raised switching costs and procurement risk. The EU glass recycling rate is about 74%, and lightweighting helps only if compatible suppliers are available. Any glass shortages or price spikes can materially hit margins and service levels.

Logistics and energy exposure

Transportation, warehousing and energy are critical inputs with few substitutes in the Nordics, where 2024 Nord Pool average prices hovered near €50/MWh and Brent averaged about $85/bbl, increasing supplier leverage. Volatile fuel and power spikes in 2024 elevated episodic supplier influence on margins. Long lead times for imported wines heighten dependence on freight partners amid 2024 container rate normalization. Multi-year logistics contracts and fuel hedging partially offset bargaining disadvantages.

Quality and sustainability requirements

Anora’s strict sustainability standards—certifications, ingredient traceability and eco-packaging targets (100% recyclable packaging target by 2030)—narrow the approved supplier pool, strengthening supplier bargaining power in the short term while raising switching costs. These standards also foster deeper partnerships that lower long‑term supply risk; co-investments in greener materials and joint CAPEX can align incentives and moderate supplier leverage.

- Fewer compliant suppliers increases short-term negotiation leverage

- Certification and traceability raise switching costs

- Co-investment reduces long-run supplier power

Partner brand principals

Global spirits and wine owners whose brands Anora distributes act as quasi-suppliers with strong bargaining positions, leveraging brand equity and alternative route-to-market options to press for favorable terms; in 2024 several principal agreements cited by industry reports show margin renegotiations moving 2–4 percentage points on renewal.

Contract renewals and detailed performance clauses materially affect Anora’s margin split and predictability of earnings, while Anora’s Nordic scale—distribution across four core Nordic markets and a documented execution record—partially counterbalances but does not fully neutralize supplier leverage.

Glass concentration, energy spikes squeeze margins; renewals: 2-4 pp

Anora faces low supplier power for commoditized grains and neutral spirit but high leverage from concentrated EU glass suppliers (Ardagh, Verallia, Vetropack, O-I), logistics and brand owners; 2024 Nord Pool ~€50/MWh and Brent ~$85/bbl elevated episodic supplier influence; renewals shifted margins ~2–4 pp; sustainability narrows approved suppliers but enables long-term co‑investment.

| Input | 2024 metric | Power |

|---|---|---|

| Commodities | High substitutability | Low |

| Glass | 4 major suppliers | High |

| Energy | €50/MWh; $85/bbl | Medium |

| Recycling/packaging | EU recycle 74%; target 100% by 2030 | Rising |

| Renewals | Margin shift 2–4 pp | Material |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threats from substitutes and new entrants, and strategic vulnerabilities for Anora Porter; detailed, data-backed commentary highlighting disruptive forces and market entry barriers to inform investor materials and strategy decks.

A single-sheet Five Forces summary with adjustable pressure sliders and an instant radar visualization—streamlines strategic decisions, fits in decks, and requires no macros so non-finance users can tailor scenarios and integrate into reports.

Customers Bargaining Power

Nordic retail monopolies

Systembolaget, Vinmonopolet and Alko are state retail monopolies that centrally run tender-based procurement and category management, giving them decisive leverage over price, listings and volumes across off‑trade channels. Their scale enables prioritising private‑label rollouts, squeezing branded margins, while strict compliance, documented sustainability and assured availability are mandatory criteria to win framework agreements.

HoReCa and wholesalers

Bars, restaurants and on-trade distributors press hard for discounts and promotional support, with key chains and groups often accounting for 20–30% of listings and therefore wielding disproportionate leverage. Menu placements and pour agreements are critical battlegrounds influencing share-of-pour and pricing. Seasonality and tourism drive order volatility, producing peak-to-trough order swings commonly in the 30–50% range, forcing flexible trade terms and inventory planning.

Price transparency and taxation

High excise duties in Nordic markets and transparent shelf pricing heighten consumer price sensitivity in 2024, driving purchase decisions more by excise-inflated shelf price than by product attributes. State retail monopolies like Alko (exclusive off‑premise retailer for >5.5% ABV in Finland) standardize pricing, compressing room for premiumization unless brand equity is strong. Buyers increasingly demand clear value tiers and promotional mechanics within regulatory bounds, and consumer trade-down during slower economic periods strengthens buyer negotiating stance.

Switching ease within categories

- SKU rationalization

- Tender-driven pricing

- Local brand resilience

Industrial and B2B customers

Anora’s industrial and B2B customers are often segment-concentrated, increasing buyer influence over volumes and specifications.

Contracted volumes and tight quality specs give buyers negotiation leverage while multi-sourcing remains common, pressuring pricing and margins.

Long-term supply agreements and co-development partnerships can secure supply and shift bargaining power toward more balanced commercial terms.

- Concentration: segment-specific buyer clusters

- Contracts: volume and spec-driven leverage

- Sourcing: multi-vendor purchasing pressures

- Mitigation: long-term supply and co-development

Retail monopolies control off‑trade; on‑trade drive 20–30% listings; seasonality 30–50% swings

State retail monopolies control off‑trade procurement and listings; key on‑trade chains drive 20–30% of listings; seasonality causes 30–50% order swings; Alko holds exclusive off‑premise for >5.5% ABV; high excise in 2024 raises price sensitivity and SKU rationalization.

| Buyer | Metric | 2024 |

|---|---|---|

| On‑trade chains | Listing share | 20–30% |

| Order volatility | Peak‑to‑trough swing | 30–50% |

| Alko | Exclusive >ABV | >5.5% |

Preview the Actual Deliverable

Anora Porter's Five Forces Analysis

This preview displays the exact Anora Porter Five Forces analysis you will receive after purchase—no placeholders or mockups. It is the final, professionally written and fully formatted document, ready for immediate download and use. Upon completing payment you’ll get instant access to this same file. Use it as-is for decision making or reporting.

From Overview to Strategy Blueprint

Anora’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes, and industry rivalry—all key to assessing strategic risk and value creation. This brief view outlines immediate pressures and strategic levers for Anora’s market position. Unlock the full Porter's Five Forces Analysis to explore Anora’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented agricultural inputs

Anora sources grains, grapes, botanicals and sugar from a wide base of farmers and growers, keeping individual supplier power relatively low. Commoditized grain and neutral spirit inputs remain widely substitutable across suppliers, reducing bargaining leverage. Premium appellation wines and specialty botanicals tighten options and can raise supplier leverage. Climate variability in 2024 produced periodic yield shocks that temporarily elevated supplier influence.

Concentrated packaging and glass

European container glass remains concentrated among Ardagh, Verallia, Vetropack and Owens-Illinois; closures and limited new capacity since 2022, plus energy-cost shocks, have tightened supply and raised switching costs and procurement risk. The EU glass recycling rate is about 74%, and lightweighting helps only if compatible suppliers are available. Any glass shortages or price spikes can materially hit margins and service levels.

Logistics and energy exposure

Transportation, warehousing and energy are critical inputs with few substitutes in the Nordics, where 2024 Nord Pool average prices hovered near €50/MWh and Brent averaged about $85/bbl, increasing supplier leverage. Volatile fuel and power spikes in 2024 elevated episodic supplier influence on margins. Long lead times for imported wines heighten dependence on freight partners amid 2024 container rate normalization. Multi-year logistics contracts and fuel hedging partially offset bargaining disadvantages.

Quality and sustainability requirements

Anora’s strict sustainability standards—certifications, ingredient traceability and eco-packaging targets (100% recyclable packaging target by 2030)—narrow the approved supplier pool, strengthening supplier bargaining power in the short term while raising switching costs. These standards also foster deeper partnerships that lower long‑term supply risk; co-investments in greener materials and joint CAPEX can align incentives and moderate supplier leverage.

- Fewer compliant suppliers increases short-term negotiation leverage

- Certification and traceability raise switching costs

- Co-investment reduces long-run supplier power

Partner brand principals

Global spirits and wine owners whose brands Anora distributes act as quasi-suppliers with strong bargaining positions, leveraging brand equity and alternative route-to-market options to press for favorable terms; in 2024 several principal agreements cited by industry reports show margin renegotiations moving 2–4 percentage points on renewal.

Contract renewals and detailed performance clauses materially affect Anora’s margin split and predictability of earnings, while Anora’s Nordic scale—distribution across four core Nordic markets and a documented execution record—partially counterbalances but does not fully neutralize supplier leverage.

Glass concentration, energy spikes squeeze margins; renewals: 2-4 pp

Anora faces low supplier power for commoditized grains and neutral spirit but high leverage from concentrated EU glass suppliers (Ardagh, Verallia, Vetropack, O-I), logistics and brand owners; 2024 Nord Pool ~€50/MWh and Brent ~$85/bbl elevated episodic supplier influence; renewals shifted margins ~2–4 pp; sustainability narrows approved suppliers but enables long-term co‑investment.

| Input | 2024 metric | Power |

|---|---|---|

| Commodities | High substitutability | Low |

| Glass | 4 major suppliers | High |

| Energy | €50/MWh; $85/bbl | Medium |

| Recycling/packaging | EU recycle 74%; target 100% by 2030 | Rising |

| Renewals | Margin shift 2–4 pp | Material |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threats from substitutes and new entrants, and strategic vulnerabilities for Anora Porter; detailed, data-backed commentary highlighting disruptive forces and market entry barriers to inform investor materials and strategy decks.

A single-sheet Five Forces summary with adjustable pressure sliders and an instant radar visualization—streamlines strategic decisions, fits in decks, and requires no macros so non-finance users can tailor scenarios and integrate into reports.

Customers Bargaining Power

Nordic retail monopolies

Systembolaget, Vinmonopolet and Alko are state retail monopolies that centrally run tender-based procurement and category management, giving them decisive leverage over price, listings and volumes across off‑trade channels. Their scale enables prioritising private‑label rollouts, squeezing branded margins, while strict compliance, documented sustainability and assured availability are mandatory criteria to win framework agreements.

HoReCa and wholesalers

Bars, restaurants and on-trade distributors press hard for discounts and promotional support, with key chains and groups often accounting for 20–30% of listings and therefore wielding disproportionate leverage. Menu placements and pour agreements are critical battlegrounds influencing share-of-pour and pricing. Seasonality and tourism drive order volatility, producing peak-to-trough order swings commonly in the 30–50% range, forcing flexible trade terms and inventory planning.

Price transparency and taxation

High excise duties in Nordic markets and transparent shelf pricing heighten consumer price sensitivity in 2024, driving purchase decisions more by excise-inflated shelf price than by product attributes. State retail monopolies like Alko (exclusive off‑premise retailer for >5.5% ABV in Finland) standardize pricing, compressing room for premiumization unless brand equity is strong. Buyers increasingly demand clear value tiers and promotional mechanics within regulatory bounds, and consumer trade-down during slower economic periods strengthens buyer negotiating stance.

Switching ease within categories

- SKU rationalization

- Tender-driven pricing

- Local brand resilience

Industrial and B2B customers

Anora’s industrial and B2B customers are often segment-concentrated, increasing buyer influence over volumes and specifications.

Contracted volumes and tight quality specs give buyers negotiation leverage while multi-sourcing remains common, pressuring pricing and margins.

Long-term supply agreements and co-development partnerships can secure supply and shift bargaining power toward more balanced commercial terms.

- Concentration: segment-specific buyer clusters

- Contracts: volume and spec-driven leverage

- Sourcing: multi-vendor purchasing pressures

- Mitigation: long-term supply and co-development

Retail monopolies control off‑trade; on‑trade drive 20–30% listings; seasonality 30–50% swings

State retail monopolies control off‑trade procurement and listings; key on‑trade chains drive 20–30% of listings; seasonality causes 30–50% order swings; Alko holds exclusive off‑premise for >5.5% ABV; high excise in 2024 raises price sensitivity and SKU rationalization.

| Buyer | Metric | 2024 |

|---|---|---|

| On‑trade chains | Listing share | 20–30% |

| Order volatility | Peak‑to‑trough swing | 30–50% |

| Alko | Exclusive >ABV | >5.5% |

Preview the Actual Deliverable

Anora Porter's Five Forces Analysis

This preview displays the exact Anora Porter Five Forces analysis you will receive after purchase—no placeholders or mockups. It is the final, professionally written and fully formatted document, ready for immediate download and use. Upon completing payment you’ll get instant access to this same file. Use it as-is for decision making or reporting.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Anora’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of new entrants and substitutes, and industry rivalry—all key to assessing strategic risk and value creation. This brief view outlines immediate pressures and strategic levers for Anora’s market position. Unlock the full Porter's Five Forces Analysis to explore Anora’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented agricultural inputs

Anora sources grains, grapes, botanicals and sugar from a wide base of farmers and growers, keeping individual supplier power relatively low. Commoditized grain and neutral spirit inputs remain widely substitutable across suppliers, reducing bargaining leverage. Premium appellation wines and specialty botanicals tighten options and can raise supplier leverage. Climate variability in 2024 produced periodic yield shocks that temporarily elevated supplier influence.

Concentrated packaging and glass

European container glass remains concentrated among Ardagh, Verallia, Vetropack and Owens-Illinois; closures and limited new capacity since 2022, plus energy-cost shocks, have tightened supply and raised switching costs and procurement risk. The EU glass recycling rate is about 74%, and lightweighting helps only if compatible suppliers are available. Any glass shortages or price spikes can materially hit margins and service levels.

Logistics and energy exposure

Transportation, warehousing and energy are critical inputs with few substitutes in the Nordics, where 2024 Nord Pool average prices hovered near €50/MWh and Brent averaged about $85/bbl, increasing supplier leverage. Volatile fuel and power spikes in 2024 elevated episodic supplier influence on margins. Long lead times for imported wines heighten dependence on freight partners amid 2024 container rate normalization. Multi-year logistics contracts and fuel hedging partially offset bargaining disadvantages.

Quality and sustainability requirements

Anora’s strict sustainability standards—certifications, ingredient traceability and eco-packaging targets (100% recyclable packaging target by 2030)—narrow the approved supplier pool, strengthening supplier bargaining power in the short term while raising switching costs. These standards also foster deeper partnerships that lower long‑term supply risk; co-investments in greener materials and joint CAPEX can align incentives and moderate supplier leverage.

- Fewer compliant suppliers increases short-term negotiation leverage

- Certification and traceability raise switching costs

- Co-investment reduces long-run supplier power

Partner brand principals

Global spirits and wine owners whose brands Anora distributes act as quasi-suppliers with strong bargaining positions, leveraging brand equity and alternative route-to-market options to press for favorable terms; in 2024 several principal agreements cited by industry reports show margin renegotiations moving 2–4 percentage points on renewal.

Contract renewals and detailed performance clauses materially affect Anora’s margin split and predictability of earnings, while Anora’s Nordic scale—distribution across four core Nordic markets and a documented execution record—partially counterbalances but does not fully neutralize supplier leverage.

Glass concentration, energy spikes squeeze margins; renewals: 2-4 pp

Anora faces low supplier power for commoditized grains and neutral spirit but high leverage from concentrated EU glass suppliers (Ardagh, Verallia, Vetropack, O-I), logistics and brand owners; 2024 Nord Pool ~€50/MWh and Brent ~$85/bbl elevated episodic supplier influence; renewals shifted margins ~2–4 pp; sustainability narrows approved suppliers but enables long-term co‑investment.

| Input | 2024 metric | Power |

|---|---|---|

| Commodities | High substitutability | Low |

| Glass | 4 major suppliers | High |

| Energy | €50/MWh; $85/bbl | Medium |

| Recycling/packaging | EU recycle 74%; target 100% by 2030 | Rising |

| Renewals | Margin shift 2–4 pp | Material |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threats from substitutes and new entrants, and strategic vulnerabilities for Anora Porter; detailed, data-backed commentary highlighting disruptive forces and market entry barriers to inform investor materials and strategy decks.

A single-sheet Five Forces summary with adjustable pressure sliders and an instant radar visualization—streamlines strategic decisions, fits in decks, and requires no macros so non-finance users can tailor scenarios and integrate into reports.

Customers Bargaining Power

Nordic retail monopolies

Systembolaget, Vinmonopolet and Alko are state retail monopolies that centrally run tender-based procurement and category management, giving them decisive leverage over price, listings and volumes across off‑trade channels. Their scale enables prioritising private‑label rollouts, squeezing branded margins, while strict compliance, documented sustainability and assured availability are mandatory criteria to win framework agreements.

HoReCa and wholesalers

Bars, restaurants and on-trade distributors press hard for discounts and promotional support, with key chains and groups often accounting for 20–30% of listings and therefore wielding disproportionate leverage. Menu placements and pour agreements are critical battlegrounds influencing share-of-pour and pricing. Seasonality and tourism drive order volatility, producing peak-to-trough order swings commonly in the 30–50% range, forcing flexible trade terms and inventory planning.

Price transparency and taxation

High excise duties in Nordic markets and transparent shelf pricing heighten consumer price sensitivity in 2024, driving purchase decisions more by excise-inflated shelf price than by product attributes. State retail monopolies like Alko (exclusive off‑premise retailer for >5.5% ABV in Finland) standardize pricing, compressing room for premiumization unless brand equity is strong. Buyers increasingly demand clear value tiers and promotional mechanics within regulatory bounds, and consumer trade-down during slower economic periods strengthens buyer negotiating stance.

Switching ease within categories

- SKU rationalization

- Tender-driven pricing

- Local brand resilience

Industrial and B2B customers

Anora’s industrial and B2B customers are often segment-concentrated, increasing buyer influence over volumes and specifications.

Contracted volumes and tight quality specs give buyers negotiation leverage while multi-sourcing remains common, pressuring pricing and margins.

Long-term supply agreements and co-development partnerships can secure supply and shift bargaining power toward more balanced commercial terms.

- Concentration: segment-specific buyer clusters

- Contracts: volume and spec-driven leverage

- Sourcing: multi-vendor purchasing pressures

- Mitigation: long-term supply and co-development

Retail monopolies control off‑trade; on‑trade drive 20–30% listings; seasonality 30–50% swings

State retail monopolies control off‑trade procurement and listings; key on‑trade chains drive 20–30% of listings; seasonality causes 30–50% order swings; Alko holds exclusive off‑premise for >5.5% ABV; high excise in 2024 raises price sensitivity and SKU rationalization.

| Buyer | Metric | 2024 |

|---|---|---|

| On‑trade chains | Listing share | 20–30% |

| Order volatility | Peak‑to‑trough swing | 30–50% |

| Alko | Exclusive >ABV | >5.5% |

Preview the Actual Deliverable

Anora Porter's Five Forces Analysis

This preview displays the exact Anora Porter Five Forces analysis you will receive after purchase—no placeholders or mockups. It is the final, professionally written and fully formatted document, ready for immediate download and use. Upon completing payment you’ll get instant access to this same file. Use it as-is for decision making or reporting.