Anuvu SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Anuvu’s SWOT snapshot highlights unique strengths in satellite connectivity and niche market reach, balanced by cyclical maritime demand and regulatory complexities. Our full SWOT dives deeper into financials, competitive threats, and strategic opportunities. Purchase the complete, editable report to access expert analysis, actionable recommendations, and Excel tools for investor-ready planning.

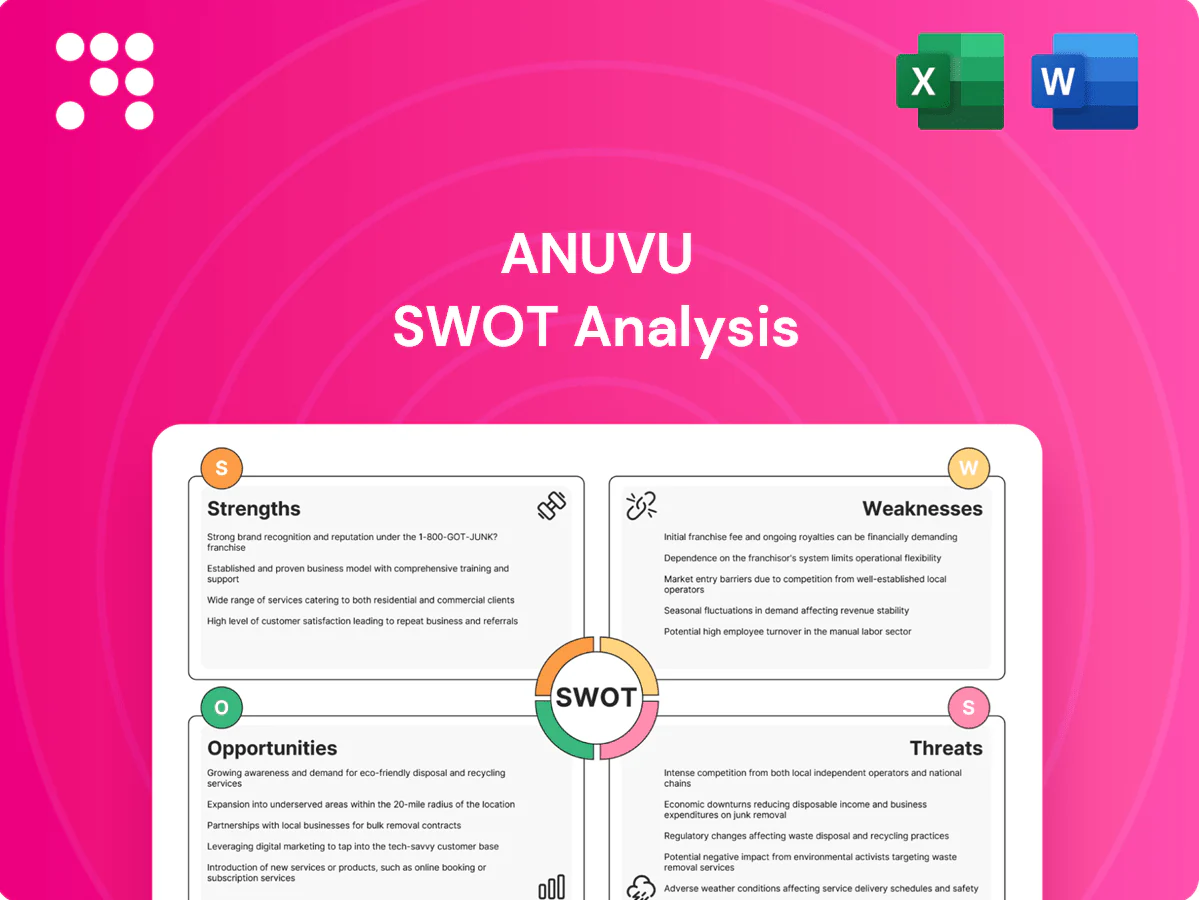

Strengths

Integrated connectivity + IFE portfolio

Anuvu bundles high-speed connectivity with a rich IFE portfolio, letting airlines simplify vendor management and offer integrated passenger experiences. The combined stack creates clear cross-sell and upsell paths and raises switching costs versus single-line vendors. It enables differentiated service tiers and varied monetization models for ancillary revenue growth.

Diversified mobility end-markets

Diversified end-markets—airlines, maritime and other transport—smooth revenue swings as 2024 airline traffic recovered to roughly pre‑pandemic levels per IATA, while maritime connectivity demand remained steady, expanding Anuvu’s TAM and contract pipeline; multi‑vertical exposure offsets sector shocks and boosts resilience across cycles.

Global satellite capacity and partnerships

Access to multi-satellite capacity and partner networks gives Anuvu broad global coverage and route flexibility, enabling service across transoceanic and remote air corridors. Multi-orbit and multi-band capabilities allow routing to optimize cost and performance by region and use case, improving throughput and latency for priority traffic. This footprint supports meeting stringent SLAs for premium airline customers and enables rapid scaling when winning new airline or fleet contracts.

Content licensing and operations expertise

Deep relationships with over 20 studios and global distributors streamline content licensing and cross‑jurisdiction compliance, enabling faster rights clearance and regional tailoring; operational support including encoding, curation and weekly refresh cycles keeps catalogs fresh and reduces operator workload while maintaining consistent quality.

- Network: 20+ studio/distributor partners

- Refresh cadence: weekly catalog updates

- Benefit: lowers operator OPEX and ensures uniform IFE quality

- Moat: integrated rights management and end‑to‑end IFE workflows

Service reliability and data-driven optimization

Network monitoring, analytics and operational playbooks drive >99.5% reported operational uptime, improving passenger experience across hundreds of aircraft and maritime vessels; real-time telemetry enables dynamic bandwidth allocation, content personalization and predictive maintenance, reducing outages and cost-per-EBITDA. Measurable QoS supports premium pricing and multi-year contracts, strengthening trust with airlines, cruise lines and ferry operators.

- Network monitoring: real-time telemetry

- Uptime: >99.5%

- Benefits: bandwidth optimization, predictive maintenance

- Commercial: premium pricing, long-term supply contracts

Bundled high-speed connectivity + IFE, multi-vertical reach, >99.5% uptime

Anuvu bundles high‑speed connectivity and IFE, creating cross‑sell paths and higher switching costs. Multi‑vertical exposure—airlines (traffic ~pre‑pandemic in 2024 per IATA), maritime—diversifies revenue. Multi‑satellite footprint and >99.5% uptime support premium SLAs and long‑term contracts.

| Metric | Value |

|---|---|

| Studios | 20+ |

| Uptime | >99.5% |

What is included in the product

Provides a strategic overview of Anuvu’s internal strengths and weaknesses and external opportunities and threats, assessing its competitive position in satellite connectivity, in-flight entertainment, and maritime markets to identify growth drivers, operational gaps, and risk factors shaping future performance.

Provides a concise SWOT matrix tailored to Anuvu for fast, visual strategy alignment and stakeholder briefings; editable format enables quick updates as market conditions and priorities shift.

Weaknesses

Capital intensity and capacity costs

Leased satellite capacity, ground infrastructure and equipment subsidies strain Anuvu's cash flows; satellite capacity leases can run into tens of millions annually and in-flight retrofit costs commonly range $150,000–$500,000 per aircraft, lengthening payback. Upfront installs and retrofits often extend payback beyond several years, limiting pricing agility and compressing margins during demand dips. Exposure to vendor terms and annual price escalators raises cost volatility.

Exposure to airline cycles and procurement

Airline budget cycles (typically 3–5 years), drawn-out certification/STC processes (6–12 months) and RFP timelines (6–18 months) slow Anuvu sales velocity and backlog conversion. Fleet groundings or route changes can defer installs and revenue recognition for quarters. Carrier financial stress — despite IATA's modest industry profit forecast of $9.7B for 2024 — drives renegotiations and price pressure. High concentration in large airline accounts elevates contract risk.

Legacy footprints and integration complexity

Managing mixed hardware generations and software stacks raises support costs—often cited as up to 25% higher for operators with fragmented fleets—while integrating connectivity across diverse IFE platforms and CMS adds operational complexity and certification overhead. Accumulated technical debt slows rollout of new features and multi-orbit capabilities, hindering uniform service quality across fleets.

Bandwidth commoditization pressure

Bandwidth commoditization pressures drive price competition on raw Mbps, eroding differentiation when customers focus on cost; rivals with vertical integration into space assets can undercut pricing, squeezing Anuvu’s margins unless offset by higher-value services.

This dynamic forces continual innovation in service packaging and stricter SLAs to protect yields and retain enterprise and maritime customers.

- Revenue mix shift risk

- Margin compression vs integrated competitors

- Need for value-added service growth

- Continuous SLA/packaging innovation required

Regulatory and content compliance overhead

Regulatory and content compliance across multi-country spectrum, aviation, and maritime regimes increases operational friction for Anuvu, requiring specialized processes and approvals. Managing content rights windows, censorship rules, and localization inflates operational workload and legal oversight. Failures can trigger fines, takedowns, or loss of service contracts, raising SG&A and slowing market entry.

- Multi-jurisdictional spectrum & safety rules

- Content rights windows, censorship, localization

- Risk: fines, takedowns, contract loss

- Outcome: higher SG&A, slower entry

Fixed costs, long sales cycles, retrofits $150k–$500k squeeze margins

High fixed costs from leased satellite capacity (tens of millions annually) and retrofits ($150k–$500k/aircraft) compress cash flow and extend payback beyond several years. Slow airline sales cycles (3–5 years), STC/RFP delays (6–18 months) and high account concentration raise backlog and contract risk. Support complexity (+~25% cost), multi-jurisdiction compliance and bandwidth commoditization erode margins versus integrated rivals.

| Metric | Value |

|---|---|

| Retrofit cost | $150k–$500k/aircraft |

| Support cost uplift | ~25% |

| STC/RFP lead time | 6–18 months |

| Industry profit (IATA 2024) | $9.7B |

Same Document Delivered

Anuvu SWOT Analysis

This is the actual Anuvu SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the entire, editable version. You’re viewing a live preview of the real file—complete, structured, and ready to download after checkout.

Elevate Your Analysis with the Complete SWOT Report

Anuvu’s SWOT snapshot highlights unique strengths in satellite connectivity and niche market reach, balanced by cyclical maritime demand and regulatory complexities. Our full SWOT dives deeper into financials, competitive threats, and strategic opportunities. Purchase the complete, editable report to access expert analysis, actionable recommendations, and Excel tools for investor-ready planning.

Strengths

Integrated connectivity + IFE portfolio

Anuvu bundles high-speed connectivity with a rich IFE portfolio, letting airlines simplify vendor management and offer integrated passenger experiences. The combined stack creates clear cross-sell and upsell paths and raises switching costs versus single-line vendors. It enables differentiated service tiers and varied monetization models for ancillary revenue growth.

Diversified mobility end-markets

Diversified end-markets—airlines, maritime and other transport—smooth revenue swings as 2024 airline traffic recovered to roughly pre‑pandemic levels per IATA, while maritime connectivity demand remained steady, expanding Anuvu’s TAM and contract pipeline; multi‑vertical exposure offsets sector shocks and boosts resilience across cycles.

Global satellite capacity and partnerships

Access to multi-satellite capacity and partner networks gives Anuvu broad global coverage and route flexibility, enabling service across transoceanic and remote air corridors. Multi-orbit and multi-band capabilities allow routing to optimize cost and performance by region and use case, improving throughput and latency for priority traffic. This footprint supports meeting stringent SLAs for premium airline customers and enables rapid scaling when winning new airline or fleet contracts.

Content licensing and operations expertise

Deep relationships with over 20 studios and global distributors streamline content licensing and cross‑jurisdiction compliance, enabling faster rights clearance and regional tailoring; operational support including encoding, curation and weekly refresh cycles keeps catalogs fresh and reduces operator workload while maintaining consistent quality.

- Network: 20+ studio/distributor partners

- Refresh cadence: weekly catalog updates

- Benefit: lowers operator OPEX and ensures uniform IFE quality

- Moat: integrated rights management and end‑to‑end IFE workflows

Service reliability and data-driven optimization

Network monitoring, analytics and operational playbooks drive >99.5% reported operational uptime, improving passenger experience across hundreds of aircraft and maritime vessels; real-time telemetry enables dynamic bandwidth allocation, content personalization and predictive maintenance, reducing outages and cost-per-EBITDA. Measurable QoS supports premium pricing and multi-year contracts, strengthening trust with airlines, cruise lines and ferry operators.

- Network monitoring: real-time telemetry

- Uptime: >99.5%

- Benefits: bandwidth optimization, predictive maintenance

- Commercial: premium pricing, long-term supply contracts

Bundled high-speed connectivity + IFE, multi-vertical reach, >99.5% uptime

Anuvu bundles high‑speed connectivity and IFE, creating cross‑sell paths and higher switching costs. Multi‑vertical exposure—airlines (traffic ~pre‑pandemic in 2024 per IATA), maritime—diversifies revenue. Multi‑satellite footprint and >99.5% uptime support premium SLAs and long‑term contracts.

| Metric | Value |

|---|---|

| Studios | 20+ |

| Uptime | >99.5% |

What is included in the product

Provides a strategic overview of Anuvu’s internal strengths and weaknesses and external opportunities and threats, assessing its competitive position in satellite connectivity, in-flight entertainment, and maritime markets to identify growth drivers, operational gaps, and risk factors shaping future performance.

Provides a concise SWOT matrix tailored to Anuvu for fast, visual strategy alignment and stakeholder briefings; editable format enables quick updates as market conditions and priorities shift.

Weaknesses

Capital intensity and capacity costs

Leased satellite capacity, ground infrastructure and equipment subsidies strain Anuvu's cash flows; satellite capacity leases can run into tens of millions annually and in-flight retrofit costs commonly range $150,000–$500,000 per aircraft, lengthening payback. Upfront installs and retrofits often extend payback beyond several years, limiting pricing agility and compressing margins during demand dips. Exposure to vendor terms and annual price escalators raises cost volatility.

Exposure to airline cycles and procurement

Airline budget cycles (typically 3–5 years), drawn-out certification/STC processes (6–12 months) and RFP timelines (6–18 months) slow Anuvu sales velocity and backlog conversion. Fleet groundings or route changes can defer installs and revenue recognition for quarters. Carrier financial stress — despite IATA's modest industry profit forecast of $9.7B for 2024 — drives renegotiations and price pressure. High concentration in large airline accounts elevates contract risk.

Legacy footprints and integration complexity

Managing mixed hardware generations and software stacks raises support costs—often cited as up to 25% higher for operators with fragmented fleets—while integrating connectivity across diverse IFE platforms and CMS adds operational complexity and certification overhead. Accumulated technical debt slows rollout of new features and multi-orbit capabilities, hindering uniform service quality across fleets.

Bandwidth commoditization pressure

Bandwidth commoditization pressures drive price competition on raw Mbps, eroding differentiation when customers focus on cost; rivals with vertical integration into space assets can undercut pricing, squeezing Anuvu’s margins unless offset by higher-value services.

This dynamic forces continual innovation in service packaging and stricter SLAs to protect yields and retain enterprise and maritime customers.

- Revenue mix shift risk

- Margin compression vs integrated competitors

- Need for value-added service growth

- Continuous SLA/packaging innovation required

Regulatory and content compliance overhead

Regulatory and content compliance across multi-country spectrum, aviation, and maritime regimes increases operational friction for Anuvu, requiring specialized processes and approvals. Managing content rights windows, censorship rules, and localization inflates operational workload and legal oversight. Failures can trigger fines, takedowns, or loss of service contracts, raising SG&A and slowing market entry.

- Multi-jurisdictional spectrum & safety rules

- Content rights windows, censorship, localization

- Risk: fines, takedowns, contract loss

- Outcome: higher SG&A, slower entry

Fixed costs, long sales cycles, retrofits $150k–$500k squeeze margins

High fixed costs from leased satellite capacity (tens of millions annually) and retrofits ($150k–$500k/aircraft) compress cash flow and extend payback beyond several years. Slow airline sales cycles (3–5 years), STC/RFP delays (6–18 months) and high account concentration raise backlog and contract risk. Support complexity (+~25% cost), multi-jurisdiction compliance and bandwidth commoditization erode margins versus integrated rivals.

| Metric | Value |

|---|---|

| Retrofit cost | $150k–$500k/aircraft |

| Support cost uplift | ~25% |

| STC/RFP lead time | 6–18 months |

| Industry profit (IATA 2024) | $9.7B |

Same Document Delivered

Anuvu SWOT Analysis

This is the actual Anuvu SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the entire, editable version. You’re viewing a live preview of the real file—complete, structured, and ready to download after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Anuvu’s SWOT snapshot highlights unique strengths in satellite connectivity and niche market reach, balanced by cyclical maritime demand and regulatory complexities. Our full SWOT dives deeper into financials, competitive threats, and strategic opportunities. Purchase the complete, editable report to access expert analysis, actionable recommendations, and Excel tools for investor-ready planning.

Strengths

Integrated connectivity + IFE portfolio

Anuvu bundles high-speed connectivity with a rich IFE portfolio, letting airlines simplify vendor management and offer integrated passenger experiences. The combined stack creates clear cross-sell and upsell paths and raises switching costs versus single-line vendors. It enables differentiated service tiers and varied monetization models for ancillary revenue growth.

Diversified mobility end-markets

Diversified end-markets—airlines, maritime and other transport—smooth revenue swings as 2024 airline traffic recovered to roughly pre‑pandemic levels per IATA, while maritime connectivity demand remained steady, expanding Anuvu’s TAM and contract pipeline; multi‑vertical exposure offsets sector shocks and boosts resilience across cycles.

Global satellite capacity and partnerships

Access to multi-satellite capacity and partner networks gives Anuvu broad global coverage and route flexibility, enabling service across transoceanic and remote air corridors. Multi-orbit and multi-band capabilities allow routing to optimize cost and performance by region and use case, improving throughput and latency for priority traffic. This footprint supports meeting stringent SLAs for premium airline customers and enables rapid scaling when winning new airline or fleet contracts.

Content licensing and operations expertise

Deep relationships with over 20 studios and global distributors streamline content licensing and cross‑jurisdiction compliance, enabling faster rights clearance and regional tailoring; operational support including encoding, curation and weekly refresh cycles keeps catalogs fresh and reduces operator workload while maintaining consistent quality.

- Network: 20+ studio/distributor partners

- Refresh cadence: weekly catalog updates

- Benefit: lowers operator OPEX and ensures uniform IFE quality

- Moat: integrated rights management and end‑to‑end IFE workflows

Service reliability and data-driven optimization

Network monitoring, analytics and operational playbooks drive >99.5% reported operational uptime, improving passenger experience across hundreds of aircraft and maritime vessels; real-time telemetry enables dynamic bandwidth allocation, content personalization and predictive maintenance, reducing outages and cost-per-EBITDA. Measurable QoS supports premium pricing and multi-year contracts, strengthening trust with airlines, cruise lines and ferry operators.

- Network monitoring: real-time telemetry

- Uptime: >99.5%

- Benefits: bandwidth optimization, predictive maintenance

- Commercial: premium pricing, long-term supply contracts

Bundled high-speed connectivity + IFE, multi-vertical reach, >99.5% uptime

Anuvu bundles high‑speed connectivity and IFE, creating cross‑sell paths and higher switching costs. Multi‑vertical exposure—airlines (traffic ~pre‑pandemic in 2024 per IATA), maritime—diversifies revenue. Multi‑satellite footprint and >99.5% uptime support premium SLAs and long‑term contracts.

| Metric | Value |

|---|---|

| Studios | 20+ |

| Uptime | >99.5% |

What is included in the product

Provides a strategic overview of Anuvu’s internal strengths and weaknesses and external opportunities and threats, assessing its competitive position in satellite connectivity, in-flight entertainment, and maritime markets to identify growth drivers, operational gaps, and risk factors shaping future performance.

Provides a concise SWOT matrix tailored to Anuvu for fast, visual strategy alignment and stakeholder briefings; editable format enables quick updates as market conditions and priorities shift.

Weaknesses

Capital intensity and capacity costs

Leased satellite capacity, ground infrastructure and equipment subsidies strain Anuvu's cash flows; satellite capacity leases can run into tens of millions annually and in-flight retrofit costs commonly range $150,000–$500,000 per aircraft, lengthening payback. Upfront installs and retrofits often extend payback beyond several years, limiting pricing agility and compressing margins during demand dips. Exposure to vendor terms and annual price escalators raises cost volatility.

Exposure to airline cycles and procurement

Airline budget cycles (typically 3–5 years), drawn-out certification/STC processes (6–12 months) and RFP timelines (6–18 months) slow Anuvu sales velocity and backlog conversion. Fleet groundings or route changes can defer installs and revenue recognition for quarters. Carrier financial stress — despite IATA's modest industry profit forecast of $9.7B for 2024 — drives renegotiations and price pressure. High concentration in large airline accounts elevates contract risk.

Legacy footprints and integration complexity

Managing mixed hardware generations and software stacks raises support costs—often cited as up to 25% higher for operators with fragmented fleets—while integrating connectivity across diverse IFE platforms and CMS adds operational complexity and certification overhead. Accumulated technical debt slows rollout of new features and multi-orbit capabilities, hindering uniform service quality across fleets.

Bandwidth commoditization pressure

Bandwidth commoditization pressures drive price competition on raw Mbps, eroding differentiation when customers focus on cost; rivals with vertical integration into space assets can undercut pricing, squeezing Anuvu’s margins unless offset by higher-value services.

This dynamic forces continual innovation in service packaging and stricter SLAs to protect yields and retain enterprise and maritime customers.

- Revenue mix shift risk

- Margin compression vs integrated competitors

- Need for value-added service growth

- Continuous SLA/packaging innovation required

Regulatory and content compliance overhead

Regulatory and content compliance across multi-country spectrum, aviation, and maritime regimes increases operational friction for Anuvu, requiring specialized processes and approvals. Managing content rights windows, censorship rules, and localization inflates operational workload and legal oversight. Failures can trigger fines, takedowns, or loss of service contracts, raising SG&A and slowing market entry.

- Multi-jurisdictional spectrum & safety rules

- Content rights windows, censorship, localization

- Risk: fines, takedowns, contract loss

- Outcome: higher SG&A, slower entry

Fixed costs, long sales cycles, retrofits $150k–$500k squeeze margins

High fixed costs from leased satellite capacity (tens of millions annually) and retrofits ($150k–$500k/aircraft) compress cash flow and extend payback beyond several years. Slow airline sales cycles (3–5 years), STC/RFP delays (6–18 months) and high account concentration raise backlog and contract risk. Support complexity (+~25% cost), multi-jurisdiction compliance and bandwidth commoditization erode margins versus integrated rivals.

| Metric | Value |

|---|---|

| Retrofit cost | $150k–$500k/aircraft |

| Support cost uplift | ~25% |

| STC/RFP lead time | 6–18 months |

| Industry profit (IATA 2024) | $9.7B |

Same Document Delivered

Anuvu SWOT Analysis

This is the actual Anuvu SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the entire, editable version. You’re viewing a live preview of the real file—complete, structured, and ready to download after checkout.