Aon Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

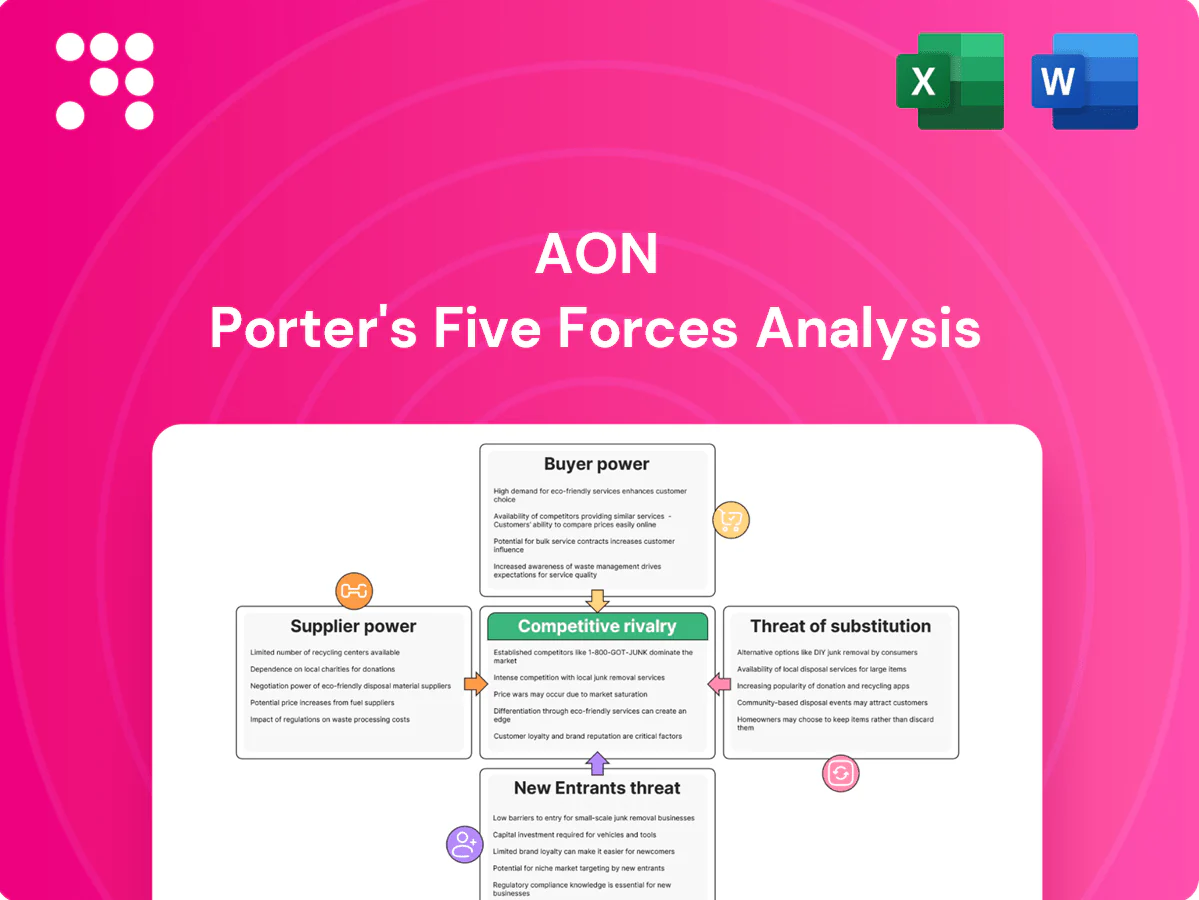

Aon's Porter's Five Forces snapshot highlights competitive rivalry, buyer and supplier power, threat of substitutes and entry, and regulatory influence shaping profitability. It identifies where Aon can leverage scale, distribution and advisory capabilities to mitigate risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Aon’s key suppliers are insurance and reinsurance carriers that provide placement capacity; with over 50,000 employees and global reach, Aon offsets supplier leverage through portfolio placements and preferred arrangements. Because capacity is concentrated—top reinsurers supply roughly 60% of specialty capacity—carriers can push harder on terms in tight markets. Market cycles drive pricing and coverage breadth swings, with specialty rates moving in double-digit percentages between hard and soft phases.

Supplier Power 2

Data and modeling vendors such as RMS, AIR and CoreLogic are critical inputs and their concentration raises supplier power through switching frictions; niche analytics limit alternatives. Aon offsets this by investing in proprietary analytics and data assets and by 2024 operating with ~50,000 employees to support in‑house capabilities. Interoperability and multi‑vendor strategies further temper lock‑in risk.

Supplier Power 3

Technology platforms and cloud providers are critical enablers for Aon; the top three cloud vendors hold about 65% of market share (AWS ~32%, Azure ~22%, GCP ~11%), giving large tech vendors pricing power offset by Aon’s long-term enterprise agreements. Aon’s build-vs-buy strategy limits single-vendor exposure and procurement risk. Rising cybersecurity and compliance needs—average breach cost around $4.45M—heighten reliance on high-quality suppliers.

Supplier Power 4

Human capital is the critical supplier for Aon—specialist brokers, actuaries and consultants drive advisory margins, and in 2024 Aon had around 50,000 employees globally. Scarcity of niche cyber, specialty lines and reinsurance talent elevates wage pressure and poaching risk. Aon mitigates this with clear career pathways, equity incentives and global mobility, while employer brand and culture materially reduce supplier bargaining power.

- Talent scarcity: niche cyber/reinsurance

- Retention: career paths, equity, mobility

- Scale: ~50,000 employees (2024)

Supplier Power 5

Healthcare networks, benefits administrators, and investment managers act as suppliers in health and retirement solutions. Concentration among administrators and large asset managers — BlackRock and Vanguard holding over $18 trillion combined AUM by 2024 — can increase fees or limit plan flexibility. Aon’s multi-carrier panels and fiduciary rigor enhance negotiating leverage, and outcome-based vendor performance frameworks (used by ~60% of large employers in 2024) rebalance power.

- Supplier concentration: high (top asset managers hold trillions AUM)

- Aon levers multi-carrier panels and fiduciary oversight

- Outcome-based contracts (~60% adoption among large employers 2024) shift risk to vendors

Concentrated supplier power strains broker: reinsurers, data vendors, cloud & talent gaps

Aon faces concentrated supplier power: top reinsurers supply ~60% specialty capacity, pressuring terms in hard markets. Data/model vendors (RMS, AIR, CoreLogic) create switching frictions. Top three cloud providers hold ~65% (AWS 32%, Azure 22%, GCP 11%). Human capital remains critical—Aon ~50,000 employees in 2024 amid niche talent scarcity.

| Supplier | Concentration | Aon levers |

|---|---|---|

| Reinsurers | ~60% specialty | Portfolio placements |

| Data vendors | High | Proprietary analytics |

| Cloud | ~65% | Long-term contracts |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Aon, detailing competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, plus disruptive forces and strategic implications for pricing and market positioning.

Aon Porter's Five Forces delivers a one-sheet, customizable radar that quickly diagnoses competitive pressures and pinpoints strategic pain points—easy to edit, share, and drop straight into decks or dashboards for faster, clearer decisions.

Customers Bargaining Power

Buyer Power 1

Large corporates, multinationals and governments increasingly run competitive RFPs—about 70% of Fortune 500 procurements are reported as formal RFPs—raising price pressure and driving many to multi-source among top brokers, which increases buyer bargaining power. Aon defends fees through global placement reach, analytics and claims advocacy, citing documented loss savings as high as 12–15% and TCO reductions near 8% in client case studies. These value metrics help shift procurement focus from headline price to total cost and risk-adjusted outcomes.

Buyer Power 2

Switching costs are moderate for Aon: deep client relationships and multi-year data repositories increase friction, yet market alternatives keep price pressure high. Standardized placements show higher price sensitivity while bespoke specialty work is stickier; Aon reported roughly $15.0B revenue in FY2024, reflecting strength in higher-margin specialty lines. Embedded tools, dashboards and risk-financing programs boost client stickiness and reported client retention near 92%, while SLAs and outcome KPIs further reduce churn incentives.

Buyer Power 3

Mid-market buyers are more fragmented, reducing individual bargaining power, though aggregators and buying groups can secure volume discounts and tilt leverage. By 2024, an estimated 65% of commercial buyers used digital quoting or comparison tools, raising fee scrutiny and pricing transparency. Aon counters with scaled package offerings and digital platforms to preserve margins while meeting price expectations.

Buyer Power 4

Reinsurance clients are sophisticated, price-aware and cycle-sensitive, benchmarking brokers tightly on placement success and market access; Aon reports strong traction in capital markets and ILS channels as of 2024. Aon’s proprietary capital markets access and alternative-capital placements (ILS capacity >120bn in 2024) reduce pure price competition and elevate advisory differentiation. Buyers retain high leverage but value differentiated distribution and structuring.

- Buyer sophistication: high

- ILS capacity 2024: >120bn

- Key leverage: placement success, market access

Buyer Power 5

Buyer Power 5: benefits and retirement clients increasingly pressure Aon for lower administration costs and outcome guarantees, leveraging regulatory fee scrutiny and fiduciary standards to demand better value.

Aon counters with performance-based pricing, outcome analytics and vendor consolidation to capture savings while long-term advisory mandates help stabilize fee erosion.

- Clients: push outcome guarantees, lower admin costs

- Regulation: fiduciary scrutiny strengthens buyer leverage

- Aon: performance-based fees, analytics, vendor consolidation

- Mitigator: long-term mandates temper annual fee compression

RFPs ~70%, digital quoting ~65%, ILS > $120bn push advisory value

Buyers are highly sophisticated: ~70% of Fortune 500 procure via RFPs and ~65% of commercial buyers used digital quoting in 2024, increasing price transparency. Aon defends fees via global placement, analytics and claims advocacy, reporting ~15.0B revenue (FY2024) and ~92% client retention. Reinsurance/ILS access (>120bn ILS capacity 2024) shifts competition toward advisory value.

| Metric | 2024 |

|---|---|

| Fortune 500 RFPs | ~70% |

| Digital quoting | ~65% |

| Aon revenue | $15.0B |

| Client retention | ~92% |

| ILS capacity | >$120bn |

Preview the Actual Deliverable

Aon Porter's Five Forces Analysis

This preview shows the exact Aon Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, comprehensive, and ready for download and use the moment you complete your payment. What you see is what you get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Aon's Porter's Five Forces snapshot highlights competitive rivalry, buyer and supplier power, threat of substitutes and entry, and regulatory influence shaping profitability. It identifies where Aon can leverage scale, distribution and advisory capabilities to mitigate risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Aon’s key suppliers are insurance and reinsurance carriers that provide placement capacity; with over 50,000 employees and global reach, Aon offsets supplier leverage through portfolio placements and preferred arrangements. Because capacity is concentrated—top reinsurers supply roughly 60% of specialty capacity—carriers can push harder on terms in tight markets. Market cycles drive pricing and coverage breadth swings, with specialty rates moving in double-digit percentages between hard and soft phases.

Supplier Power 2

Data and modeling vendors such as RMS, AIR and CoreLogic are critical inputs and their concentration raises supplier power through switching frictions; niche analytics limit alternatives. Aon offsets this by investing in proprietary analytics and data assets and by 2024 operating with ~50,000 employees to support in‑house capabilities. Interoperability and multi‑vendor strategies further temper lock‑in risk.

Supplier Power 3

Technology platforms and cloud providers are critical enablers for Aon; the top three cloud vendors hold about 65% of market share (AWS ~32%, Azure ~22%, GCP ~11%), giving large tech vendors pricing power offset by Aon’s long-term enterprise agreements. Aon’s build-vs-buy strategy limits single-vendor exposure and procurement risk. Rising cybersecurity and compliance needs—average breach cost around $4.45M—heighten reliance on high-quality suppliers.

Supplier Power 4

Human capital is the critical supplier for Aon—specialist brokers, actuaries and consultants drive advisory margins, and in 2024 Aon had around 50,000 employees globally. Scarcity of niche cyber, specialty lines and reinsurance talent elevates wage pressure and poaching risk. Aon mitigates this with clear career pathways, equity incentives and global mobility, while employer brand and culture materially reduce supplier bargaining power.

- Talent scarcity: niche cyber/reinsurance

- Retention: career paths, equity, mobility

- Scale: ~50,000 employees (2024)

Supplier Power 5

Healthcare networks, benefits administrators, and investment managers act as suppliers in health and retirement solutions. Concentration among administrators and large asset managers — BlackRock and Vanguard holding over $18 trillion combined AUM by 2024 — can increase fees or limit plan flexibility. Aon’s multi-carrier panels and fiduciary rigor enhance negotiating leverage, and outcome-based vendor performance frameworks (used by ~60% of large employers in 2024) rebalance power.

- Supplier concentration: high (top asset managers hold trillions AUM)

- Aon levers multi-carrier panels and fiduciary oversight

- Outcome-based contracts (~60% adoption among large employers 2024) shift risk to vendors

Concentrated supplier power strains broker: reinsurers, data vendors, cloud & talent gaps

Aon faces concentrated supplier power: top reinsurers supply ~60% specialty capacity, pressuring terms in hard markets. Data/model vendors (RMS, AIR, CoreLogic) create switching frictions. Top three cloud providers hold ~65% (AWS 32%, Azure 22%, GCP 11%). Human capital remains critical—Aon ~50,000 employees in 2024 amid niche talent scarcity.

| Supplier | Concentration | Aon levers |

|---|---|---|

| Reinsurers | ~60% specialty | Portfolio placements |

| Data vendors | High | Proprietary analytics |

| Cloud | ~65% | Long-term contracts |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Aon, detailing competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, plus disruptive forces and strategic implications for pricing and market positioning.

Aon Porter's Five Forces delivers a one-sheet, customizable radar that quickly diagnoses competitive pressures and pinpoints strategic pain points—easy to edit, share, and drop straight into decks or dashboards for faster, clearer decisions.

Customers Bargaining Power

Buyer Power 1

Large corporates, multinationals and governments increasingly run competitive RFPs—about 70% of Fortune 500 procurements are reported as formal RFPs—raising price pressure and driving many to multi-source among top brokers, which increases buyer bargaining power. Aon defends fees through global placement reach, analytics and claims advocacy, citing documented loss savings as high as 12–15% and TCO reductions near 8% in client case studies. These value metrics help shift procurement focus from headline price to total cost and risk-adjusted outcomes.

Buyer Power 2

Switching costs are moderate for Aon: deep client relationships and multi-year data repositories increase friction, yet market alternatives keep price pressure high. Standardized placements show higher price sensitivity while bespoke specialty work is stickier; Aon reported roughly $15.0B revenue in FY2024, reflecting strength in higher-margin specialty lines. Embedded tools, dashboards and risk-financing programs boost client stickiness and reported client retention near 92%, while SLAs and outcome KPIs further reduce churn incentives.

Buyer Power 3

Mid-market buyers are more fragmented, reducing individual bargaining power, though aggregators and buying groups can secure volume discounts and tilt leverage. By 2024, an estimated 65% of commercial buyers used digital quoting or comparison tools, raising fee scrutiny and pricing transparency. Aon counters with scaled package offerings and digital platforms to preserve margins while meeting price expectations.

Buyer Power 4

Reinsurance clients are sophisticated, price-aware and cycle-sensitive, benchmarking brokers tightly on placement success and market access; Aon reports strong traction in capital markets and ILS channels as of 2024. Aon’s proprietary capital markets access and alternative-capital placements (ILS capacity >120bn in 2024) reduce pure price competition and elevate advisory differentiation. Buyers retain high leverage but value differentiated distribution and structuring.

- Buyer sophistication: high

- ILS capacity 2024: >120bn

- Key leverage: placement success, market access

Buyer Power 5

Buyer Power 5: benefits and retirement clients increasingly pressure Aon for lower administration costs and outcome guarantees, leveraging regulatory fee scrutiny and fiduciary standards to demand better value.

Aon counters with performance-based pricing, outcome analytics and vendor consolidation to capture savings while long-term advisory mandates help stabilize fee erosion.

- Clients: push outcome guarantees, lower admin costs

- Regulation: fiduciary scrutiny strengthens buyer leverage

- Aon: performance-based fees, analytics, vendor consolidation

- Mitigator: long-term mandates temper annual fee compression

RFPs ~70%, digital quoting ~65%, ILS > $120bn push advisory value

Buyers are highly sophisticated: ~70% of Fortune 500 procure via RFPs and ~65% of commercial buyers used digital quoting in 2024, increasing price transparency. Aon defends fees via global placement, analytics and claims advocacy, reporting ~15.0B revenue (FY2024) and ~92% client retention. Reinsurance/ILS access (>120bn ILS capacity 2024) shifts competition toward advisory value.

| Metric | 2024 |

|---|---|

| Fortune 500 RFPs | ~70% |

| Digital quoting | ~65% |

| Aon revenue | $15.0B |

| Client retention | ~92% |

| ILS capacity | >$120bn |

Preview the Actual Deliverable

Aon Porter's Five Forces Analysis

This preview shows the exact Aon Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, comprehensive, and ready for download and use the moment you complete your payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Aon's Porter's Five Forces snapshot highlights competitive rivalry, buyer and supplier power, threat of substitutes and entry, and regulatory influence shaping profitability. It identifies where Aon can leverage scale, distribution and advisory capabilities to mitigate risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Aon’s key suppliers are insurance and reinsurance carriers that provide placement capacity; with over 50,000 employees and global reach, Aon offsets supplier leverage through portfolio placements and preferred arrangements. Because capacity is concentrated—top reinsurers supply roughly 60% of specialty capacity—carriers can push harder on terms in tight markets. Market cycles drive pricing and coverage breadth swings, with specialty rates moving in double-digit percentages between hard and soft phases.

Supplier Power 2

Data and modeling vendors such as RMS, AIR and CoreLogic are critical inputs and their concentration raises supplier power through switching frictions; niche analytics limit alternatives. Aon offsets this by investing in proprietary analytics and data assets and by 2024 operating with ~50,000 employees to support in‑house capabilities. Interoperability and multi‑vendor strategies further temper lock‑in risk.

Supplier Power 3

Technology platforms and cloud providers are critical enablers for Aon; the top three cloud vendors hold about 65% of market share (AWS ~32%, Azure ~22%, GCP ~11%), giving large tech vendors pricing power offset by Aon’s long-term enterprise agreements. Aon’s build-vs-buy strategy limits single-vendor exposure and procurement risk. Rising cybersecurity and compliance needs—average breach cost around $4.45M—heighten reliance on high-quality suppliers.

Supplier Power 4

Human capital is the critical supplier for Aon—specialist brokers, actuaries and consultants drive advisory margins, and in 2024 Aon had around 50,000 employees globally. Scarcity of niche cyber, specialty lines and reinsurance talent elevates wage pressure and poaching risk. Aon mitigates this with clear career pathways, equity incentives and global mobility, while employer brand and culture materially reduce supplier bargaining power.

- Talent scarcity: niche cyber/reinsurance

- Retention: career paths, equity, mobility

- Scale: ~50,000 employees (2024)

Supplier Power 5

Healthcare networks, benefits administrators, and investment managers act as suppliers in health and retirement solutions. Concentration among administrators and large asset managers — BlackRock and Vanguard holding over $18 trillion combined AUM by 2024 — can increase fees or limit plan flexibility. Aon’s multi-carrier panels and fiduciary rigor enhance negotiating leverage, and outcome-based vendor performance frameworks (used by ~60% of large employers in 2024) rebalance power.

- Supplier concentration: high (top asset managers hold trillions AUM)

- Aon levers multi-carrier panels and fiduciary oversight

- Outcome-based contracts (~60% adoption among large employers 2024) shift risk to vendors

Concentrated supplier power strains broker: reinsurers, data vendors, cloud & talent gaps

Aon faces concentrated supplier power: top reinsurers supply ~60% specialty capacity, pressuring terms in hard markets. Data/model vendors (RMS, AIR, CoreLogic) create switching frictions. Top three cloud providers hold ~65% (AWS 32%, Azure 22%, GCP 11%). Human capital remains critical—Aon ~50,000 employees in 2024 amid niche talent scarcity.

| Supplier | Concentration | Aon levers |

|---|---|---|

| Reinsurers | ~60% specialty | Portfolio placements |

| Data vendors | High | Proprietary analytics |

| Cloud | ~65% | Long-term contracts |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Aon, detailing competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, plus disruptive forces and strategic implications for pricing and market positioning.

Aon Porter's Five Forces delivers a one-sheet, customizable radar that quickly diagnoses competitive pressures and pinpoints strategic pain points—easy to edit, share, and drop straight into decks or dashboards for faster, clearer decisions.

Customers Bargaining Power

Buyer Power 1

Large corporates, multinationals and governments increasingly run competitive RFPs—about 70% of Fortune 500 procurements are reported as formal RFPs—raising price pressure and driving many to multi-source among top brokers, which increases buyer bargaining power. Aon defends fees through global placement reach, analytics and claims advocacy, citing documented loss savings as high as 12–15% and TCO reductions near 8% in client case studies. These value metrics help shift procurement focus from headline price to total cost and risk-adjusted outcomes.

Buyer Power 2

Switching costs are moderate for Aon: deep client relationships and multi-year data repositories increase friction, yet market alternatives keep price pressure high. Standardized placements show higher price sensitivity while bespoke specialty work is stickier; Aon reported roughly $15.0B revenue in FY2024, reflecting strength in higher-margin specialty lines. Embedded tools, dashboards and risk-financing programs boost client stickiness and reported client retention near 92%, while SLAs and outcome KPIs further reduce churn incentives.

Buyer Power 3

Mid-market buyers are more fragmented, reducing individual bargaining power, though aggregators and buying groups can secure volume discounts and tilt leverage. By 2024, an estimated 65% of commercial buyers used digital quoting or comparison tools, raising fee scrutiny and pricing transparency. Aon counters with scaled package offerings and digital platforms to preserve margins while meeting price expectations.

Buyer Power 4

Reinsurance clients are sophisticated, price-aware and cycle-sensitive, benchmarking brokers tightly on placement success and market access; Aon reports strong traction in capital markets and ILS channels as of 2024. Aon’s proprietary capital markets access and alternative-capital placements (ILS capacity >120bn in 2024) reduce pure price competition and elevate advisory differentiation. Buyers retain high leverage but value differentiated distribution and structuring.

- Buyer sophistication: high

- ILS capacity 2024: >120bn

- Key leverage: placement success, market access

Buyer Power 5

Buyer Power 5: benefits and retirement clients increasingly pressure Aon for lower administration costs and outcome guarantees, leveraging regulatory fee scrutiny and fiduciary standards to demand better value.

Aon counters with performance-based pricing, outcome analytics and vendor consolidation to capture savings while long-term advisory mandates help stabilize fee erosion.

- Clients: push outcome guarantees, lower admin costs

- Regulation: fiduciary scrutiny strengthens buyer leverage

- Aon: performance-based fees, analytics, vendor consolidation

- Mitigator: long-term mandates temper annual fee compression

RFPs ~70%, digital quoting ~65%, ILS > $120bn push advisory value

Buyers are highly sophisticated: ~70% of Fortune 500 procure via RFPs and ~65% of commercial buyers used digital quoting in 2024, increasing price transparency. Aon defends fees via global placement, analytics and claims advocacy, reporting ~15.0B revenue (FY2024) and ~92% client retention. Reinsurance/ILS access (>120bn ILS capacity 2024) shifts competition toward advisory value.

| Metric | 2024 |

|---|---|

| Fortune 500 RFPs | ~70% |

| Digital quoting | ~65% |

| Aon revenue | $15.0B |

| Client retention | ~92% |

| ILS capacity | >$120bn |

Preview the Actual Deliverable

Aon Porter's Five Forces Analysis

This preview shows the exact Aon Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, comprehensive, and ready for download and use the moment you complete your payment. What you see is what you get.