APA Marketing Mix

Ready-Made Marketing Analysis, Ready to Use

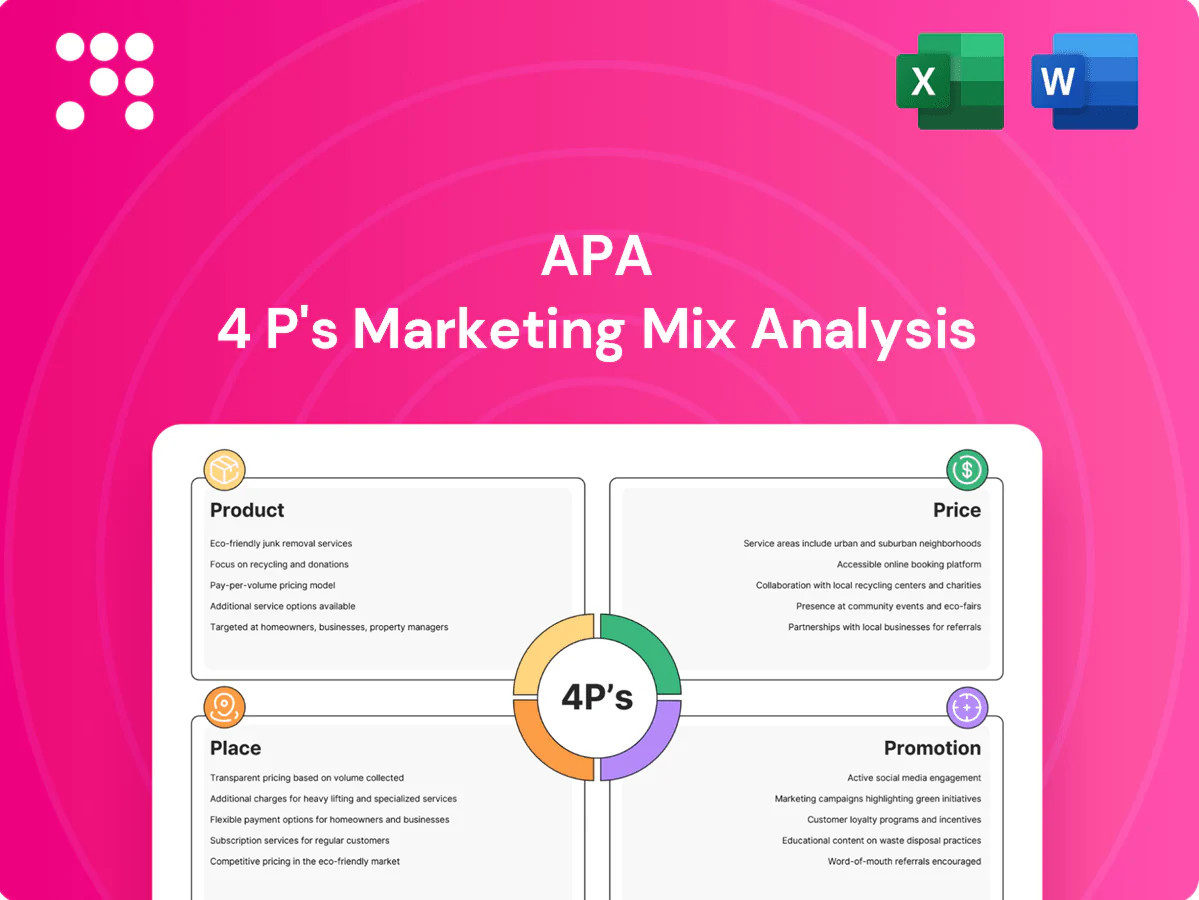

Unlock APA’s 4P’s Marketing Mix—concise insights on Product, Price, Place and Promotion that reveal how strategic choices create market advantage. Download the full, editable report for detailed data, templates and actionable recommendations. Save time and apply proven tactics today.

Product

Upstream oil

Crude from core fields in the U.S., Egypt and the U.K. drives revenue, with U.S. output about 13.2 million b/d in 2024 while Egypt and the U.K. each produce roughly 0.6 million b/d. Reservoir optimization, infill drilling and disciplined development sustain volumes and lower unit costs. Quality specs and strategic blending target premium realizations versus benchmarks, and strong reliability and safety record ensures consistent supply.

Natural gas and NGLs

Natural gas and NGLs complement crude oil by smoothing revenue through offsetting price cycles, with natural gas supplying about 38% of U.S. electricity generation in 2023. Processing and fractionation convert feedstocks into marketable NGL streams like ethane, propane and butane, supporting petrochemical and LPG markets. Portfolio exposure spans domestic power, industrial feedstock and rapidly growing export-linked LNG demand—U.S. export capacity exceeded 12 Bcf/d by 2024. Flexible sales points across hubs and terminals enable optimized value capture.

LNG and offtake

Select volumes are routed to LNG pathways via regional partnerships, leveraging a global seaborne market that exceeded about 380 mtpa in 2023 to secure scale and market access. Contracting spans term offtake, tolling, or marketing arrangements to balance cashflow and delivery risk. The commercial aim is to secure netbacks indexed to global gas benchmarks (TTF/JKM) while optionality enables arbitrage of regional price differentials.

EOR and CCS solutions

Enhanced oil recovery projects can extend field life and boost recoveries by roughly 5–20% depending on reservoir and method. Carbon capture, utilization and storage initiatives target lower emissions intensity, with global CCS capture capacity near 50 MtCO2/yr in 2024. Service and partnership models (JV, tolling, contracts) unlock fee-based and resource-value revenues and integration strengthens license-to-operate.

- Recovery uplift 5–20%

- Global CCS ≈50 MtCO2/yr (2024)

- JV/contract models create new revenue streams

- Integration improves social and regulatory license-to-operate

Subsurface tech and data

- Geoscience: +10–30% drilling success

- Real-time/automation: +5–15% uptime, −10–20% OPEX

- Data partnerships: −20–40% cycle time

- Tech adoption: −15–25% lifting costs

Crude, gas and CCUS lift margins; tech raises recovery 5-20% and cuts costs 15-25%

Crude (US 13.2m b/d 2024; Egypt/UK ~0.6m b/d) plus gas/NGLs (US gas 38% power 2023; LNG export >12 Bcf/d 2024) and EOR/CCUS (CCS ~50 MtCO2/yr 2024) shape product mix, margins via blending, processing and flexible offtake; tech raises recovery 5–20% and cuts lifting costs 15–25% improving netbacks.

| Metric | Value |

|---|---|

| US crude | 13.2m b/d (2024) |

| LNG cap | >12 Bcf/d (2024) |

| CCS | ~50 MtCO2/yr (2024) |

What is included in the product

Delivers a company-specific deep dive into the APA 4P’s—Product, Price, Place, Promotion—mapping real brand practices and competitive context to actionable positioning and tactical recommendations. Ideal for managers, consultants, and marketers needing a ready-to-use, report-quality marketing audit.

Condenses the APA 4P’s into a concise, plug-and-play summary that relieves decision paralysis and cross-team misalignment, making marketing trade-offs clear for faster, aligned action.

Place

U.S. basins

U.S. basins provide a core footprint in short-cycle shale and tight oil—the Permian alone produced about 5.4 million b/d within U.S. crude output of ~12.5 million b/d in 2024. Access to Gulf Coast refineries and NGL hubs (Gulf operable refining capacity ~9.3 million b/d) and export terminals (U.S. crude exports ≈4.0 million b/d) supports market access. Multiple pipeline and rail takeaway options (Cactus II, Gray Oak, EPIC) mitigate bottlenecks and proximity to dense service ecosystems improves drilling and completion efficiency.

Egypt presence

Western Desert assets under production-sharing contracts supply Egypt's domestic market, contributing to national gas output of about 6.5 Bcf/d (2024). Local processing hubs in the Western Desert and Nile Delta enable liquids and gas evacuation into domestic pipelines and export trunks. Close collaboration with EGAS and EGPC secures market access and offtake. Some volumes route into LNG export pathways, including the Idku 7.2 mtpa facility.

U.K. North Sea

U.K. North Sea offshore hubs tie into extensive pipeline networks and terminals (Forties, Brent, FLAGS), enabling ~0.9–1.1 million boe/d of UKCS sales into European markets in 2023–24. Mature infrastructure and export routes support reliable offtake, while the HSE and Offshore Installations regulations enforce strict HSE controls and incident reporting. Operators target >95% operational uptime through portfolio-led maintenance and planned shutdown coordination to optimize cash flow.

Midstream and terminals

Midstream and terminals link pipeline connections, processing plants and storage to ensure flow assurance; US Gulf Coast export terminals handled about 4.0 million barrels per day of crude and products in 2024, while Mediterranean hubs provide export optionality for Europe/Africa markets. Scheduling and nominations align production with demand centers, and firm contracts reduce basis risk and demurrage.

- Pipeline connections: onshore/offshore networks

- Storage/processing: flow assurance

- Gulf Coast exports ~4.0 mbpd (2024)

- Contracts: cut basis risk, limit demurrage

Direct B2B channels

Direct B2B channels sell to refiners, utilities and traders via term and spot deals tied to global oil demand of 101.6 million barrels per day (IEA 2024). Digital scheduling and EDI streamline confirmations and settlements, enabling faster cash flow and lower operational error rates. Market intelligence tools (real‑time pricing, AIS) guide destination choices while long‑standing relationships support rapid response to price signals.

- Channels: term & spot

- Scale: 101.6 mb/d (IEA 2024)

- Ops: digital scheduling, EDI

- Edge: market intel + relationships

Hubs to markets: Permian, Gulf Coast, Egypt and North Sea optimize supply and exports

Place optimizes proximity to demand hubs and export capacity to maximize realizations and uptime. US Permian, Gulf Coast terminals and pipelines enable scale and access to global markets. Local Egyptian hubs and LNG links secure domestic offtake; UK North Sea pipelines ensure stable European supply.

| Region | Key metric (2024) |

|---|---|

| US Permian/Gulf | Permian 5.4 mb/d; Gulf refining 9.3 mb/d; exports ~4.0 mb/d |

| Egypt | Gas ~6.5 Bcf/d; Idku 7.2 mtpa |

| UK North Sea | 0.9–1.1 mboe/d |

What You See Is What You Get

APA 4P's Marketing Mix Analysis

The APA 4P's Marketing Mix Analysis delivers a clear Product, Price, Place and Promotion review formatted to APA standards with actionable recommendations. The preview shown here is the actual document you’ll receive instantly after purchase—fully editable and ready to use. No samples or mockups; this is the final, comprehensive file you'll download immediately.

Ready-Made Marketing Analysis, Ready to Use

Unlock APA’s 4P’s Marketing Mix—concise insights on Product, Price, Place and Promotion that reveal how strategic choices create market advantage. Download the full, editable report for detailed data, templates and actionable recommendations. Save time and apply proven tactics today.

Product

Upstream oil

Crude from core fields in the U.S., Egypt and the U.K. drives revenue, with U.S. output about 13.2 million b/d in 2024 while Egypt and the U.K. each produce roughly 0.6 million b/d. Reservoir optimization, infill drilling and disciplined development sustain volumes and lower unit costs. Quality specs and strategic blending target premium realizations versus benchmarks, and strong reliability and safety record ensures consistent supply.

Natural gas and NGLs

Natural gas and NGLs complement crude oil by smoothing revenue through offsetting price cycles, with natural gas supplying about 38% of U.S. electricity generation in 2023. Processing and fractionation convert feedstocks into marketable NGL streams like ethane, propane and butane, supporting petrochemical and LPG markets. Portfolio exposure spans domestic power, industrial feedstock and rapidly growing export-linked LNG demand—U.S. export capacity exceeded 12 Bcf/d by 2024. Flexible sales points across hubs and terminals enable optimized value capture.

LNG and offtake

Select volumes are routed to LNG pathways via regional partnerships, leveraging a global seaborne market that exceeded about 380 mtpa in 2023 to secure scale and market access. Contracting spans term offtake, tolling, or marketing arrangements to balance cashflow and delivery risk. The commercial aim is to secure netbacks indexed to global gas benchmarks (TTF/JKM) while optionality enables arbitrage of regional price differentials.

EOR and CCS solutions

Enhanced oil recovery projects can extend field life and boost recoveries by roughly 5–20% depending on reservoir and method. Carbon capture, utilization and storage initiatives target lower emissions intensity, with global CCS capture capacity near 50 MtCO2/yr in 2024. Service and partnership models (JV, tolling, contracts) unlock fee-based and resource-value revenues and integration strengthens license-to-operate.

- Recovery uplift 5–20%

- Global CCS ≈50 MtCO2/yr (2024)

- JV/contract models create new revenue streams

- Integration improves social and regulatory license-to-operate

Subsurface tech and data

- Geoscience: +10–30% drilling success

- Real-time/automation: +5–15% uptime, −10–20% OPEX

- Data partnerships: −20–40% cycle time

- Tech adoption: −15–25% lifting costs

Crude, gas and CCUS lift margins; tech raises recovery 5-20% and cuts costs 15-25%

Crude (US 13.2m b/d 2024; Egypt/UK ~0.6m b/d) plus gas/NGLs (US gas 38% power 2023; LNG export >12 Bcf/d 2024) and EOR/CCUS (CCS ~50 MtCO2/yr 2024) shape product mix, margins via blending, processing and flexible offtake; tech raises recovery 5–20% and cuts lifting costs 15–25% improving netbacks.

| Metric | Value |

|---|---|

| US crude | 13.2m b/d (2024) |

| LNG cap | >12 Bcf/d (2024) |

| CCS | ~50 MtCO2/yr (2024) |

What is included in the product

Delivers a company-specific deep dive into the APA 4P’s—Product, Price, Place, Promotion—mapping real brand practices and competitive context to actionable positioning and tactical recommendations. Ideal for managers, consultants, and marketers needing a ready-to-use, report-quality marketing audit.

Condenses the APA 4P’s into a concise, plug-and-play summary that relieves decision paralysis and cross-team misalignment, making marketing trade-offs clear for faster, aligned action.

Place

U.S. basins

U.S. basins provide a core footprint in short-cycle shale and tight oil—the Permian alone produced about 5.4 million b/d within U.S. crude output of ~12.5 million b/d in 2024. Access to Gulf Coast refineries and NGL hubs (Gulf operable refining capacity ~9.3 million b/d) and export terminals (U.S. crude exports ≈4.0 million b/d) supports market access. Multiple pipeline and rail takeaway options (Cactus II, Gray Oak, EPIC) mitigate bottlenecks and proximity to dense service ecosystems improves drilling and completion efficiency.

Egypt presence

Western Desert assets under production-sharing contracts supply Egypt's domestic market, contributing to national gas output of about 6.5 Bcf/d (2024). Local processing hubs in the Western Desert and Nile Delta enable liquids and gas evacuation into domestic pipelines and export trunks. Close collaboration with EGAS and EGPC secures market access and offtake. Some volumes route into LNG export pathways, including the Idku 7.2 mtpa facility.

U.K. North Sea

U.K. North Sea offshore hubs tie into extensive pipeline networks and terminals (Forties, Brent, FLAGS), enabling ~0.9–1.1 million boe/d of UKCS sales into European markets in 2023–24. Mature infrastructure and export routes support reliable offtake, while the HSE and Offshore Installations regulations enforce strict HSE controls and incident reporting. Operators target >95% operational uptime through portfolio-led maintenance and planned shutdown coordination to optimize cash flow.

Midstream and terminals

Midstream and terminals link pipeline connections, processing plants and storage to ensure flow assurance; US Gulf Coast export terminals handled about 4.0 million barrels per day of crude and products in 2024, while Mediterranean hubs provide export optionality for Europe/Africa markets. Scheduling and nominations align production with demand centers, and firm contracts reduce basis risk and demurrage.

- Pipeline connections: onshore/offshore networks

- Storage/processing: flow assurance

- Gulf Coast exports ~4.0 mbpd (2024)

- Contracts: cut basis risk, limit demurrage

Direct B2B channels

Direct B2B channels sell to refiners, utilities and traders via term and spot deals tied to global oil demand of 101.6 million barrels per day (IEA 2024). Digital scheduling and EDI streamline confirmations and settlements, enabling faster cash flow and lower operational error rates. Market intelligence tools (real‑time pricing, AIS) guide destination choices while long‑standing relationships support rapid response to price signals.

- Channels: term & spot

- Scale: 101.6 mb/d (IEA 2024)

- Ops: digital scheduling, EDI

- Edge: market intel + relationships

Hubs to markets: Permian, Gulf Coast, Egypt and North Sea optimize supply and exports

Place optimizes proximity to demand hubs and export capacity to maximize realizations and uptime. US Permian, Gulf Coast terminals and pipelines enable scale and access to global markets. Local Egyptian hubs and LNG links secure domestic offtake; UK North Sea pipelines ensure stable European supply.

| Region | Key metric (2024) |

|---|---|

| US Permian/Gulf | Permian 5.4 mb/d; Gulf refining 9.3 mb/d; exports ~4.0 mb/d |

| Egypt | Gas ~6.5 Bcf/d; Idku 7.2 mtpa |

| UK North Sea | 0.9–1.1 mboe/d |

What You See Is What You Get

APA 4P's Marketing Mix Analysis

The APA 4P's Marketing Mix Analysis delivers a clear Product, Price, Place and Promotion review formatted to APA standards with actionable recommendations. The preview shown here is the actual document you’ll receive instantly after purchase—fully editable and ready to use. No samples or mockups; this is the final, comprehensive file you'll download immediately.

Original: $10.00

-65%$10.00

$3.50Description

Ready-Made Marketing Analysis, Ready to Use

Unlock APA’s 4P’s Marketing Mix—concise insights on Product, Price, Place and Promotion that reveal how strategic choices create market advantage. Download the full, editable report for detailed data, templates and actionable recommendations. Save time and apply proven tactics today.

Product

Upstream oil

Crude from core fields in the U.S., Egypt and the U.K. drives revenue, with U.S. output about 13.2 million b/d in 2024 while Egypt and the U.K. each produce roughly 0.6 million b/d. Reservoir optimization, infill drilling and disciplined development sustain volumes and lower unit costs. Quality specs and strategic blending target premium realizations versus benchmarks, and strong reliability and safety record ensures consistent supply.

Natural gas and NGLs

Natural gas and NGLs complement crude oil by smoothing revenue through offsetting price cycles, with natural gas supplying about 38% of U.S. electricity generation in 2023. Processing and fractionation convert feedstocks into marketable NGL streams like ethane, propane and butane, supporting petrochemical and LPG markets. Portfolio exposure spans domestic power, industrial feedstock and rapidly growing export-linked LNG demand—U.S. export capacity exceeded 12 Bcf/d by 2024. Flexible sales points across hubs and terminals enable optimized value capture.

LNG and offtake

Select volumes are routed to LNG pathways via regional partnerships, leveraging a global seaborne market that exceeded about 380 mtpa in 2023 to secure scale and market access. Contracting spans term offtake, tolling, or marketing arrangements to balance cashflow and delivery risk. The commercial aim is to secure netbacks indexed to global gas benchmarks (TTF/JKM) while optionality enables arbitrage of regional price differentials.

EOR and CCS solutions

Enhanced oil recovery projects can extend field life and boost recoveries by roughly 5–20% depending on reservoir and method. Carbon capture, utilization and storage initiatives target lower emissions intensity, with global CCS capture capacity near 50 MtCO2/yr in 2024. Service and partnership models (JV, tolling, contracts) unlock fee-based and resource-value revenues and integration strengthens license-to-operate.

- Recovery uplift 5–20%

- Global CCS ≈50 MtCO2/yr (2024)

- JV/contract models create new revenue streams

- Integration improves social and regulatory license-to-operate

Subsurface tech and data

- Geoscience: +10–30% drilling success

- Real-time/automation: +5–15% uptime, −10–20% OPEX

- Data partnerships: −20–40% cycle time

- Tech adoption: −15–25% lifting costs

Crude, gas and CCUS lift margins; tech raises recovery 5-20% and cuts costs 15-25%

Crude (US 13.2m b/d 2024; Egypt/UK ~0.6m b/d) plus gas/NGLs (US gas 38% power 2023; LNG export >12 Bcf/d 2024) and EOR/CCUS (CCS ~50 MtCO2/yr 2024) shape product mix, margins via blending, processing and flexible offtake; tech raises recovery 5–20% and cuts lifting costs 15–25% improving netbacks.

| Metric | Value |

|---|---|

| US crude | 13.2m b/d (2024) |

| LNG cap | >12 Bcf/d (2024) |

| CCS | ~50 MtCO2/yr (2024) |

What is included in the product

Delivers a company-specific deep dive into the APA 4P’s—Product, Price, Place, Promotion—mapping real brand practices and competitive context to actionable positioning and tactical recommendations. Ideal for managers, consultants, and marketers needing a ready-to-use, report-quality marketing audit.

Condenses the APA 4P’s into a concise, plug-and-play summary that relieves decision paralysis and cross-team misalignment, making marketing trade-offs clear for faster, aligned action.

Place

U.S. basins

U.S. basins provide a core footprint in short-cycle shale and tight oil—the Permian alone produced about 5.4 million b/d within U.S. crude output of ~12.5 million b/d in 2024. Access to Gulf Coast refineries and NGL hubs (Gulf operable refining capacity ~9.3 million b/d) and export terminals (U.S. crude exports ≈4.0 million b/d) supports market access. Multiple pipeline and rail takeaway options (Cactus II, Gray Oak, EPIC) mitigate bottlenecks and proximity to dense service ecosystems improves drilling and completion efficiency.

Egypt presence

Western Desert assets under production-sharing contracts supply Egypt's domestic market, contributing to national gas output of about 6.5 Bcf/d (2024). Local processing hubs in the Western Desert and Nile Delta enable liquids and gas evacuation into domestic pipelines and export trunks. Close collaboration with EGAS and EGPC secures market access and offtake. Some volumes route into LNG export pathways, including the Idku 7.2 mtpa facility.

U.K. North Sea

U.K. North Sea offshore hubs tie into extensive pipeline networks and terminals (Forties, Brent, FLAGS), enabling ~0.9–1.1 million boe/d of UKCS sales into European markets in 2023–24. Mature infrastructure and export routes support reliable offtake, while the HSE and Offshore Installations regulations enforce strict HSE controls and incident reporting. Operators target >95% operational uptime through portfolio-led maintenance and planned shutdown coordination to optimize cash flow.

Midstream and terminals

Midstream and terminals link pipeline connections, processing plants and storage to ensure flow assurance; US Gulf Coast export terminals handled about 4.0 million barrels per day of crude and products in 2024, while Mediterranean hubs provide export optionality for Europe/Africa markets. Scheduling and nominations align production with demand centers, and firm contracts reduce basis risk and demurrage.

- Pipeline connections: onshore/offshore networks

- Storage/processing: flow assurance

- Gulf Coast exports ~4.0 mbpd (2024)

- Contracts: cut basis risk, limit demurrage

Direct B2B channels

Direct B2B channels sell to refiners, utilities and traders via term and spot deals tied to global oil demand of 101.6 million barrels per day (IEA 2024). Digital scheduling and EDI streamline confirmations and settlements, enabling faster cash flow and lower operational error rates. Market intelligence tools (real‑time pricing, AIS) guide destination choices while long‑standing relationships support rapid response to price signals.

- Channels: term & spot

- Scale: 101.6 mb/d (IEA 2024)

- Ops: digital scheduling, EDI

- Edge: market intel + relationships

Hubs to markets: Permian, Gulf Coast, Egypt and North Sea optimize supply and exports

Place optimizes proximity to demand hubs and export capacity to maximize realizations and uptime. US Permian, Gulf Coast terminals and pipelines enable scale and access to global markets. Local Egyptian hubs and LNG links secure domestic offtake; UK North Sea pipelines ensure stable European supply.

| Region | Key metric (2024) |

|---|---|

| US Permian/Gulf | Permian 5.4 mb/d; Gulf refining 9.3 mb/d; exports ~4.0 mb/d |

| Egypt | Gas ~6.5 Bcf/d; Idku 7.2 mtpa |

| UK North Sea | 0.9–1.1 mboe/d |

What You See Is What You Get

APA 4P's Marketing Mix Analysis

The APA 4P's Marketing Mix Analysis delivers a clear Product, Price, Place and Promotion review formatted to APA standards with actionable recommendations. The preview shown here is the actual document you’ll receive instantly after purchase—fully editable and ready to use. No samples or mockups; this is the final, comprehensive file you'll download immediately.