Aptiv Porter's Five Forces Analysis

From Overview to Strategy Blueprint

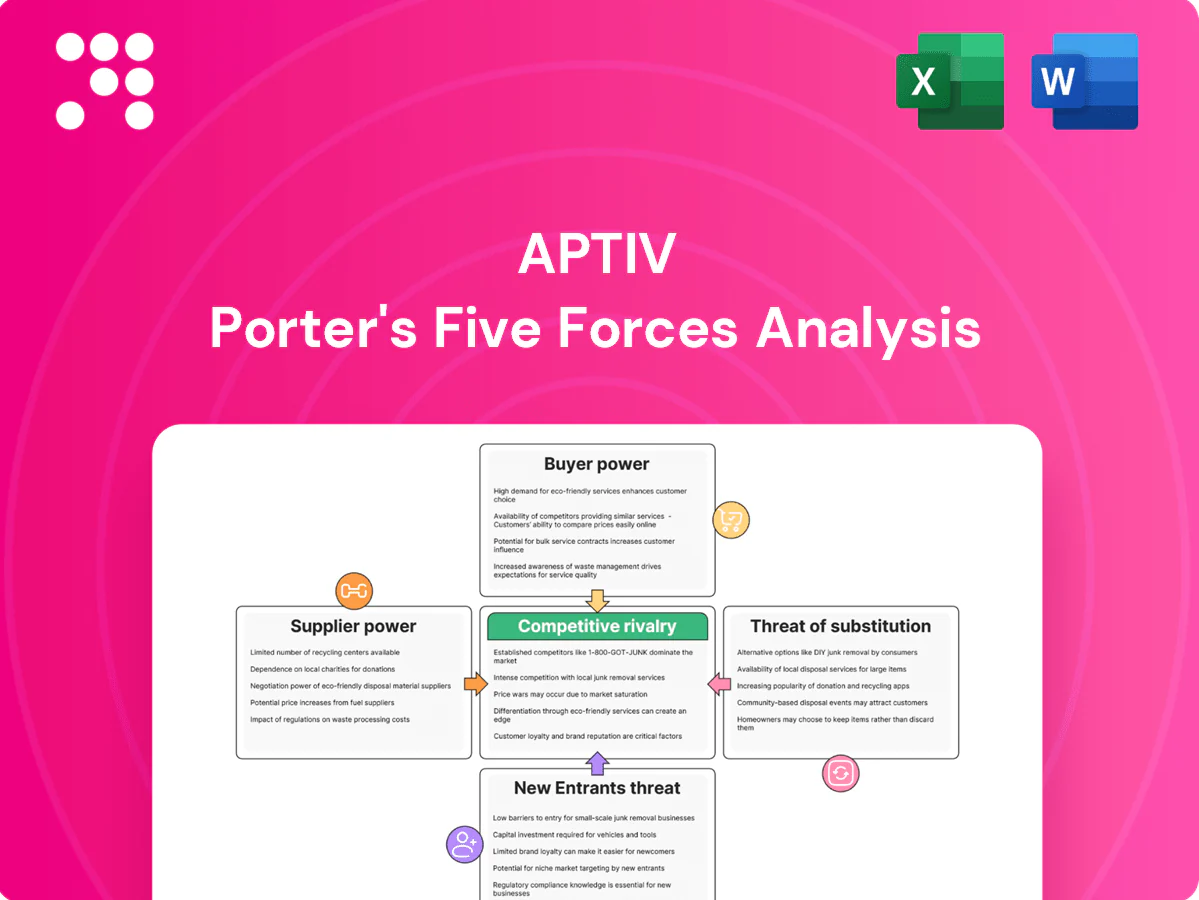

Aptiv navigates intense competitive rivalry, rising supplier leverage for advanced components, and shifting buyer demands driven by EV and autonomous trends; substitute threats and regulatory barriers further shape its strategic landscape. This brief snapshot highlights key pressures and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aptiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor sources

Advanced ADAS and central compute rely on a handful of chipmakers—TSMC controls roughly 60% of advanced-node capacity and the top 5 foundries account for over 80% of foundry revenue—giving suppliers outsized leverage. Allocation cycles and node constraints compress margins and delay deliveries, with automotive semiconductor content exceeding ~$1,000 per vehicle in 2024, raising stakes. Long-term supply agreements mitigate risk but redesigning systems for new silicon can take 12–24 months and spikes in upcycles or shortages sharply increase supplier bargaining power.

Critical raw materials volatility

Copper, aluminum, rare earths and specialized polymers drive harness and HV system costs — metals can be ~40% of material spend and rare-earths up to 15% for motors. 2024 LME copper averaged about 9,200 USD/tonne and neodymium rose ~12% in 2024, shifting bargaining power to upstream suppliers under ESG sourcing rules. Hedging and multi-sourcing mitigate but do not eliminate exposure; regionalization can add a 5–10% freight/tariff premium.

Specialized sensors and optics

High-performance radar, camera and LiDAR components come from niche vendors with strong IP moats, and in 2024 a handful of suppliers account for over 60% of high-end LiDAR/radar capacity. Qualification cycles of 12–36 months and tight tolerances limit switching. Co-development often locks vehicle architectures to specific partners. This raises dependence and gives key suppliers clear pricing leverage.

Software tools and talent scarcity

Autosar stacks, middleware and safety-certified toolchains are concentrated among a few providers (Vector, Elektrobit, Wind River in 2024), and ISO 26262 and ASPICE requirements constrain rapid supplier substitution, raising switching costs and certification lead times. Scarce embedded safety engineering talent drives up R&D costs and vendor reliance, while major cloud/data partners (AWS, Azure, GCP) add platform dependency and commercial lock-in.

- Concentrated suppliers: Vector, Elektrobit, Wind River (2024)

- Regulatory lock: ISO 26262, ASPICE limit quick substitution

- Talent squeeze: higher hiring costs, longer ramp times

- Cloud dependency: AWS/Azure/GCP platform lock-in

Geopolitical and logistics constraints

Export controls and tightening 2024 semiconductor restrictions raise preference for local suppliers, while regional content rules (often requiring ~30% local sourcing) and shipping bottlenecks privilege nearby vendors. Aptiv’s dual-continent footprint increases supplier coordination costs and can raise lead times by ~15–20%. Suppliers with regional capacity gain leverage in localization programs; political risk can rapidly flip bargaining power.

- 2024 export controls: higher local sourcing

- ~30% regional content thresholds

- Lead times +15–20% with cross-continental supply

- Regional suppliers hold negotiation leverage

Advanced-node foundry concentration ~60% in 2024 raises supplier power, costs, delays

Supplier power is high: concentrated advanced-node foundries (TSMC ~60% in 2024) and niche LiDAR/radar vendors control capacity, raising prices and delays. Commodities (copper ~$9,200/t in 2024; neodymium +12% y/y) and specialized polymers increase input leverage. Software/toolchain certification (ISO 26262/ASPICE) and long qualification (12–36 months) raise switching costs. Regional content rules (~30%) amplify local supplier power.

| Metric | 2024 |

|---|---|

| TSMC adv-node share | ~60% |

| Semiconductor content/vehicle | ~$1,000 |

| LME copper | $9,200/t |

| NdPr price change | +12% y/y |

| Regional content rule | ~30% |

What is included in the product

Concise Porter's Five Forces analysis of Aptiv highlighting competitive rivalry, supplier and buyer power, entry barriers, and substitute threats, with strategic insights on how these forces shape Aptiv’s pricing, margins, and growth prospects.

Clear, one-sheet Aptiv Porter’s Five Forces summary for rapid strategic decisions, with customizable pressure levels to mirror evolving automotive electrification and autonomy trends.

Customers Bargaining Power

OEM concentration and scale

Global automakers buy at scale and in 2024 the top 10 OEMs accounted for about 70% of light‑vehicle production, enabling aggressive negotiating power. Annual price‑downs (commonly 1–3%) and strict productivity clauses compress supplier margins. Platform‑wide awards hinge on cost, quality and delivery, and a handful of large buyers can swing Aptiv’s revenue materially—Aptiv’s top five customers made up roughly 45% of 2024 sales.

High switching costs, but dual-sourcing

Design-in and 18–36 month validation cycles create strong stickiness for awarded content, reinforcing Aptiv incumbency across programs. OEMs commonly dual-source critical systems—over 60% by supplier category—to retain leverage and negotiate price/performance. Incumbency still faces re-bids at each model refresh (typically every 4–7 years). Performance KPIs can trigger reallocations of roughly 5–15% of content annually.

Total cost and TCO scrutiny

Buyers now evaluate unit cost alongside weight, energy efficiency and lifecycle reliability, requiring suppliers to quantify TCO and energy-per-mile impacts; in 2024 procurement teams increasingly demanded line-item cost transparency. Zonal architectures and wiring simplification promise up to 60% wiring-length reduction and must show demonstrable TCO gains to justify switching. Failure to deliver measurable value erodes pricing power and invites aggressive cost benchmarking.

Software feature roadmaps

OEMs increasingly dictate software feature roadmaps and integration milestones; missed targets often trigger contractual penalties or scope reductions, and alignment to SDV timelines directly influences repeat business. Over-the-air enablement and UNECE R155/R156 cybersecurity compliance were mandatory considerations in 2024, making timely delivery critical.

- OEM-driven roadmaps

- Penalties for slippage

- OTA & R155/R156 compliance

- Rewards for SDV alignment

Localization and sustainability demands

Customers push localization and sustainability: regional sourcing and CSRD-driven carbon reporting (CSRD expands to roughly 50,000 EU firms in 2024) and recyclability targets are now award criteria, forcing suppliers to invest near customers to meet content rules; ESG ranks affect preferred-vendor status and can be leveraged in price negotiations.

- Regional sourcing pressure

- CSRD ~50,000 firms (2024)

- ESG influences awards & pricing

OEM concentration: 1-3% price-downs, >60% dual-sourcing

Large OEMs concentrate purchasing (top 10 ≈70% light‑vehicle production in 2024), giving buyers strong price leverage and annual price‑downs (≈1–3%) that compress supplier margins; Aptiv’s top five customers ≈45% of 2024 sales. Incumbency and long validation (18–36 months) limit churn, but dual‑sourcing (>60%) and KPI‑driven reallocations (5–15% annually) retain buyer leverage. Sustainability, localization and OT A/cyber rules (R155/R156) increasingly determine awards.

| Metric | 2024 Value |

|---|---|

| Top 10 OEM share | ≈70% |

| Aptiv top‑5 customers | ≈45% sales |

| Annual price‑down | 1–3% |

| Dual‑sourcing rate | >60% |

| KPI reallocation | 5–15%/yr |

| CSRD firms (EU) | ≈50,000 |

What You See Is What You Get

Aptiv Porter's Five Forces Analysis

This preview shows the exact Aptiv Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders. The document is fully formatted, professionally written, and ready to download. What you see here is exactly what you’ll get.

From Overview to Strategy Blueprint

Aptiv navigates intense competitive rivalry, rising supplier leverage for advanced components, and shifting buyer demands driven by EV and autonomous trends; substitute threats and regulatory barriers further shape its strategic landscape. This brief snapshot highlights key pressures and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aptiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor sources

Advanced ADAS and central compute rely on a handful of chipmakers—TSMC controls roughly 60% of advanced-node capacity and the top 5 foundries account for over 80% of foundry revenue—giving suppliers outsized leverage. Allocation cycles and node constraints compress margins and delay deliveries, with automotive semiconductor content exceeding ~$1,000 per vehicle in 2024, raising stakes. Long-term supply agreements mitigate risk but redesigning systems for new silicon can take 12–24 months and spikes in upcycles or shortages sharply increase supplier bargaining power.

Critical raw materials volatility

Copper, aluminum, rare earths and specialized polymers drive harness and HV system costs — metals can be ~40% of material spend and rare-earths up to 15% for motors. 2024 LME copper averaged about 9,200 USD/tonne and neodymium rose ~12% in 2024, shifting bargaining power to upstream suppliers under ESG sourcing rules. Hedging and multi-sourcing mitigate but do not eliminate exposure; regionalization can add a 5–10% freight/tariff premium.

Specialized sensors and optics

High-performance radar, camera and LiDAR components come from niche vendors with strong IP moats, and in 2024 a handful of suppliers account for over 60% of high-end LiDAR/radar capacity. Qualification cycles of 12–36 months and tight tolerances limit switching. Co-development often locks vehicle architectures to specific partners. This raises dependence and gives key suppliers clear pricing leverage.

Software tools and talent scarcity

Autosar stacks, middleware and safety-certified toolchains are concentrated among a few providers (Vector, Elektrobit, Wind River in 2024), and ISO 26262 and ASPICE requirements constrain rapid supplier substitution, raising switching costs and certification lead times. Scarce embedded safety engineering talent drives up R&D costs and vendor reliance, while major cloud/data partners (AWS, Azure, GCP) add platform dependency and commercial lock-in.

- Concentrated suppliers: Vector, Elektrobit, Wind River (2024)

- Regulatory lock: ISO 26262, ASPICE limit quick substitution

- Talent squeeze: higher hiring costs, longer ramp times

- Cloud dependency: AWS/Azure/GCP platform lock-in

Geopolitical and logistics constraints

Export controls and tightening 2024 semiconductor restrictions raise preference for local suppliers, while regional content rules (often requiring ~30% local sourcing) and shipping bottlenecks privilege nearby vendors. Aptiv’s dual-continent footprint increases supplier coordination costs and can raise lead times by ~15–20%. Suppliers with regional capacity gain leverage in localization programs; political risk can rapidly flip bargaining power.

- 2024 export controls: higher local sourcing

- ~30% regional content thresholds

- Lead times +15–20% with cross-continental supply

- Regional suppliers hold negotiation leverage

Advanced-node foundry concentration ~60% in 2024 raises supplier power, costs, delays

Supplier power is high: concentrated advanced-node foundries (TSMC ~60% in 2024) and niche LiDAR/radar vendors control capacity, raising prices and delays. Commodities (copper ~$9,200/t in 2024; neodymium +12% y/y) and specialized polymers increase input leverage. Software/toolchain certification (ISO 26262/ASPICE) and long qualification (12–36 months) raise switching costs. Regional content rules (~30%) amplify local supplier power.

| Metric | 2024 |

|---|---|

| TSMC adv-node share | ~60% |

| Semiconductor content/vehicle | ~$1,000 |

| LME copper | $9,200/t |

| NdPr price change | +12% y/y |

| Regional content rule | ~30% |

What is included in the product

Concise Porter's Five Forces analysis of Aptiv highlighting competitive rivalry, supplier and buyer power, entry barriers, and substitute threats, with strategic insights on how these forces shape Aptiv’s pricing, margins, and growth prospects.

Clear, one-sheet Aptiv Porter’s Five Forces summary for rapid strategic decisions, with customizable pressure levels to mirror evolving automotive electrification and autonomy trends.

Customers Bargaining Power

OEM concentration and scale

Global automakers buy at scale and in 2024 the top 10 OEMs accounted for about 70% of light‑vehicle production, enabling aggressive negotiating power. Annual price‑downs (commonly 1–3%) and strict productivity clauses compress supplier margins. Platform‑wide awards hinge on cost, quality and delivery, and a handful of large buyers can swing Aptiv’s revenue materially—Aptiv’s top five customers made up roughly 45% of 2024 sales.

High switching costs, but dual-sourcing

Design-in and 18–36 month validation cycles create strong stickiness for awarded content, reinforcing Aptiv incumbency across programs. OEMs commonly dual-source critical systems—over 60% by supplier category—to retain leverage and negotiate price/performance. Incumbency still faces re-bids at each model refresh (typically every 4–7 years). Performance KPIs can trigger reallocations of roughly 5–15% of content annually.

Total cost and TCO scrutiny

Buyers now evaluate unit cost alongside weight, energy efficiency and lifecycle reliability, requiring suppliers to quantify TCO and energy-per-mile impacts; in 2024 procurement teams increasingly demanded line-item cost transparency. Zonal architectures and wiring simplification promise up to 60% wiring-length reduction and must show demonstrable TCO gains to justify switching. Failure to deliver measurable value erodes pricing power and invites aggressive cost benchmarking.

Software feature roadmaps

OEMs increasingly dictate software feature roadmaps and integration milestones; missed targets often trigger contractual penalties or scope reductions, and alignment to SDV timelines directly influences repeat business. Over-the-air enablement and UNECE R155/R156 cybersecurity compliance were mandatory considerations in 2024, making timely delivery critical.

- OEM-driven roadmaps

- Penalties for slippage

- OTA & R155/R156 compliance

- Rewards for SDV alignment

Localization and sustainability demands

Customers push localization and sustainability: regional sourcing and CSRD-driven carbon reporting (CSRD expands to roughly 50,000 EU firms in 2024) and recyclability targets are now award criteria, forcing suppliers to invest near customers to meet content rules; ESG ranks affect preferred-vendor status and can be leveraged in price negotiations.

- Regional sourcing pressure

- CSRD ~50,000 firms (2024)

- ESG influences awards & pricing

OEM concentration: 1-3% price-downs, >60% dual-sourcing

Large OEMs concentrate purchasing (top 10 ≈70% light‑vehicle production in 2024), giving buyers strong price leverage and annual price‑downs (≈1–3%) that compress supplier margins; Aptiv’s top five customers ≈45% of 2024 sales. Incumbency and long validation (18–36 months) limit churn, but dual‑sourcing (>60%) and KPI‑driven reallocations (5–15% annually) retain buyer leverage. Sustainability, localization and OT A/cyber rules (R155/R156) increasingly determine awards.

| Metric | 2024 Value |

|---|---|

| Top 10 OEM share | ≈70% |

| Aptiv top‑5 customers | ≈45% sales |

| Annual price‑down | 1–3% |

| Dual‑sourcing rate | >60% |

| KPI reallocation | 5–15%/yr |

| CSRD firms (EU) | ≈50,000 |

What You See Is What You Get

Aptiv Porter's Five Forces Analysis

This preview shows the exact Aptiv Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders. The document is fully formatted, professionally written, and ready to download. What you see here is exactly what you’ll get.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Aptiv navigates intense competitive rivalry, rising supplier leverage for advanced components, and shifting buyer demands driven by EV and autonomous trends; substitute threats and regulatory barriers further shape its strategic landscape. This brief snapshot highlights key pressures and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aptiv’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor sources

Advanced ADAS and central compute rely on a handful of chipmakers—TSMC controls roughly 60% of advanced-node capacity and the top 5 foundries account for over 80% of foundry revenue—giving suppliers outsized leverage. Allocation cycles and node constraints compress margins and delay deliveries, with automotive semiconductor content exceeding ~$1,000 per vehicle in 2024, raising stakes. Long-term supply agreements mitigate risk but redesigning systems for new silicon can take 12–24 months and spikes in upcycles or shortages sharply increase supplier bargaining power.

Critical raw materials volatility

Copper, aluminum, rare earths and specialized polymers drive harness and HV system costs — metals can be ~40% of material spend and rare-earths up to 15% for motors. 2024 LME copper averaged about 9,200 USD/tonne and neodymium rose ~12% in 2024, shifting bargaining power to upstream suppliers under ESG sourcing rules. Hedging and multi-sourcing mitigate but do not eliminate exposure; regionalization can add a 5–10% freight/tariff premium.

Specialized sensors and optics

High-performance radar, camera and LiDAR components come from niche vendors with strong IP moats, and in 2024 a handful of suppliers account for over 60% of high-end LiDAR/radar capacity. Qualification cycles of 12–36 months and tight tolerances limit switching. Co-development often locks vehicle architectures to specific partners. This raises dependence and gives key suppliers clear pricing leverage.

Software tools and talent scarcity

Autosar stacks, middleware and safety-certified toolchains are concentrated among a few providers (Vector, Elektrobit, Wind River in 2024), and ISO 26262 and ASPICE requirements constrain rapid supplier substitution, raising switching costs and certification lead times. Scarce embedded safety engineering talent drives up R&D costs and vendor reliance, while major cloud/data partners (AWS, Azure, GCP) add platform dependency and commercial lock-in.

- Concentrated suppliers: Vector, Elektrobit, Wind River (2024)

- Regulatory lock: ISO 26262, ASPICE limit quick substitution

- Talent squeeze: higher hiring costs, longer ramp times

- Cloud dependency: AWS/Azure/GCP platform lock-in

Geopolitical and logistics constraints

Export controls and tightening 2024 semiconductor restrictions raise preference for local suppliers, while regional content rules (often requiring ~30% local sourcing) and shipping bottlenecks privilege nearby vendors. Aptiv’s dual-continent footprint increases supplier coordination costs and can raise lead times by ~15–20%. Suppliers with regional capacity gain leverage in localization programs; political risk can rapidly flip bargaining power.

- 2024 export controls: higher local sourcing

- ~30% regional content thresholds

- Lead times +15–20% with cross-continental supply

- Regional suppliers hold negotiation leverage

Advanced-node foundry concentration ~60% in 2024 raises supplier power, costs, delays

Supplier power is high: concentrated advanced-node foundries (TSMC ~60% in 2024) and niche LiDAR/radar vendors control capacity, raising prices and delays. Commodities (copper ~$9,200/t in 2024; neodymium +12% y/y) and specialized polymers increase input leverage. Software/toolchain certification (ISO 26262/ASPICE) and long qualification (12–36 months) raise switching costs. Regional content rules (~30%) amplify local supplier power.

| Metric | 2024 |

|---|---|

| TSMC adv-node share | ~60% |

| Semiconductor content/vehicle | ~$1,000 |

| LME copper | $9,200/t |

| NdPr price change | +12% y/y |

| Regional content rule | ~30% |

What is included in the product

Concise Porter's Five Forces analysis of Aptiv highlighting competitive rivalry, supplier and buyer power, entry barriers, and substitute threats, with strategic insights on how these forces shape Aptiv’s pricing, margins, and growth prospects.

Clear, one-sheet Aptiv Porter’s Five Forces summary for rapid strategic decisions, with customizable pressure levels to mirror evolving automotive electrification and autonomy trends.

Customers Bargaining Power

OEM concentration and scale

Global automakers buy at scale and in 2024 the top 10 OEMs accounted for about 70% of light‑vehicle production, enabling aggressive negotiating power. Annual price‑downs (commonly 1–3%) and strict productivity clauses compress supplier margins. Platform‑wide awards hinge on cost, quality and delivery, and a handful of large buyers can swing Aptiv’s revenue materially—Aptiv’s top five customers made up roughly 45% of 2024 sales.

High switching costs, but dual-sourcing

Design-in and 18–36 month validation cycles create strong stickiness for awarded content, reinforcing Aptiv incumbency across programs. OEMs commonly dual-source critical systems—over 60% by supplier category—to retain leverage and negotiate price/performance. Incumbency still faces re-bids at each model refresh (typically every 4–7 years). Performance KPIs can trigger reallocations of roughly 5–15% of content annually.

Total cost and TCO scrutiny

Buyers now evaluate unit cost alongside weight, energy efficiency and lifecycle reliability, requiring suppliers to quantify TCO and energy-per-mile impacts; in 2024 procurement teams increasingly demanded line-item cost transparency. Zonal architectures and wiring simplification promise up to 60% wiring-length reduction and must show demonstrable TCO gains to justify switching. Failure to deliver measurable value erodes pricing power and invites aggressive cost benchmarking.

Software feature roadmaps

OEMs increasingly dictate software feature roadmaps and integration milestones; missed targets often trigger contractual penalties or scope reductions, and alignment to SDV timelines directly influences repeat business. Over-the-air enablement and UNECE R155/R156 cybersecurity compliance were mandatory considerations in 2024, making timely delivery critical.

- OEM-driven roadmaps

- Penalties for slippage

- OTA & R155/R156 compliance

- Rewards for SDV alignment

Localization and sustainability demands

Customers push localization and sustainability: regional sourcing and CSRD-driven carbon reporting (CSRD expands to roughly 50,000 EU firms in 2024) and recyclability targets are now award criteria, forcing suppliers to invest near customers to meet content rules; ESG ranks affect preferred-vendor status and can be leveraged in price negotiations.

- Regional sourcing pressure

- CSRD ~50,000 firms (2024)

- ESG influences awards & pricing

OEM concentration: 1-3% price-downs, >60% dual-sourcing

Large OEMs concentrate purchasing (top 10 ≈70% light‑vehicle production in 2024), giving buyers strong price leverage and annual price‑downs (≈1–3%) that compress supplier margins; Aptiv’s top five customers ≈45% of 2024 sales. Incumbency and long validation (18–36 months) limit churn, but dual‑sourcing (>60%) and KPI‑driven reallocations (5–15% annually) retain buyer leverage. Sustainability, localization and OT A/cyber rules (R155/R156) increasingly determine awards.

| Metric | 2024 Value |

|---|---|

| Top 10 OEM share | ≈70% |

| Aptiv top‑5 customers | ≈45% sales |

| Annual price‑down | 1–3% |

| Dual‑sourcing rate | >60% |

| KPI reallocation | 5–15%/yr |

| CSRD firms (EU) | ≈50,000 |

What You See Is What You Get

Aptiv Porter's Five Forces Analysis

This preview shows the exact Aptiv Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders. The document is fully formatted, professionally written, and ready to download. What you see here is exactly what you’ll get.