Arab Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Arab Bank—concise, evidence-based insights into political, economic, social, technological, legal and environmental forces shaping performance. Ideal for investors, advisors and executives, it highlights risks and growth levers you can act on immediately. Purchase the full report to download editable charts, data and actionable recommendations.

Political factors

Geopolitical volatility in MENA

Regional conflicts, political transitions, and policy shifts can disrupt operations, risk appetite, and client activity across Arab Bank’s 30+ country footprint.

Country risk premia, FX convertibility issues in markets such as Lebanon and Sudan, and supply-chain frictions affect credit quality and liquidity planning.

Scenario planning and diversified geographic exposure mitigate shocks, while continuous monitoring of sanctions and diplomatic developments remains essential.

Sanctions and cross-border compliance

Exposure in 30+ jurisdictions requires rigorous screening against OFAC SDN (14,000+ entries as of 2025), EU and UK lists; errors can trigger multi‑million fines, de‑risking of correspondent lines and reputational damage. Investment in KYC/AML systems and staff training is a strategic necessity, and proactive engagement with regulators preserves access to global payment rails.

Government banking relationships

Arab Banks sovereign and quasi-sovereign clients significantly shape its loan book, funding and fee income given the group's footprint in over 30 countries and legacy since 1930; policy-driven infrastructure programs across MENA can expand corporate pipelines but increase concentration risk that must be actively managed. Transparent pricing and strict risk-adjusted return thresholds are essential when handling public-sector mandates to protect capital and margins.

Regulatory harmonization and fragmentation

Operating across MENA, Europe and other markets means Arab Bank, present in over 30 countries, must navigate divergent prudential and consumer rules and differing implementations of Basel III and local liquidity regimes. Non-uniform capital and liquidity standards increase compliance complexity and overhead. Harmonization efforts can unlock efficiencies but progress remains uneven, so local partnerships and adaptive compliance frameworks reduce regulatory friction.

- Presence: over 30 countries

- Frameworks: Basel III + local variations

- Impact: higher compliance complexity and costs

- Mitigation: local partnerships, adaptive compliance

Public policy on financial inclusion

National agendas to digitize payments and bank the unbanked create clear growth avenues for Arab Bank; Jordan’s financial inclusion push targets significant account penetration increases and regional digital payments surged about 20% in 2023, expanding fee-light transaction volumes. Government incentives and guarantee schemes for SME lending—mobilizing billions regionally—support portfolio expansion but require prudent credit frameworks and robust risk analytics. Demonstrating measurable social impact improves regulatory standing and license-to-operate.

Sanctions, regional risk and compliance strain correspondent access amid rapid digital payment growth

Regional conflicts, policy shifts and sanctions exposure across 30+ jurisdictions materially affect Arab Bank’s credit, liquidity and correspondent access.

OFAC SDN list exceeds 14,000 entries (2025); non‑compliance risks multi‑million fines and de‑risking of lines.

Digital payments growth (~20% in 2023) and SME guarantee schemes present growth with concentration and compliance trade‑offs.

| Metric | Value |

|---|---|

| Jurisdictions | 30+ |

| OFAC SDN | 14,000+ |

| Digital payments growth (2023) | ~20% |

| Founded | 1930 |

What is included in the product

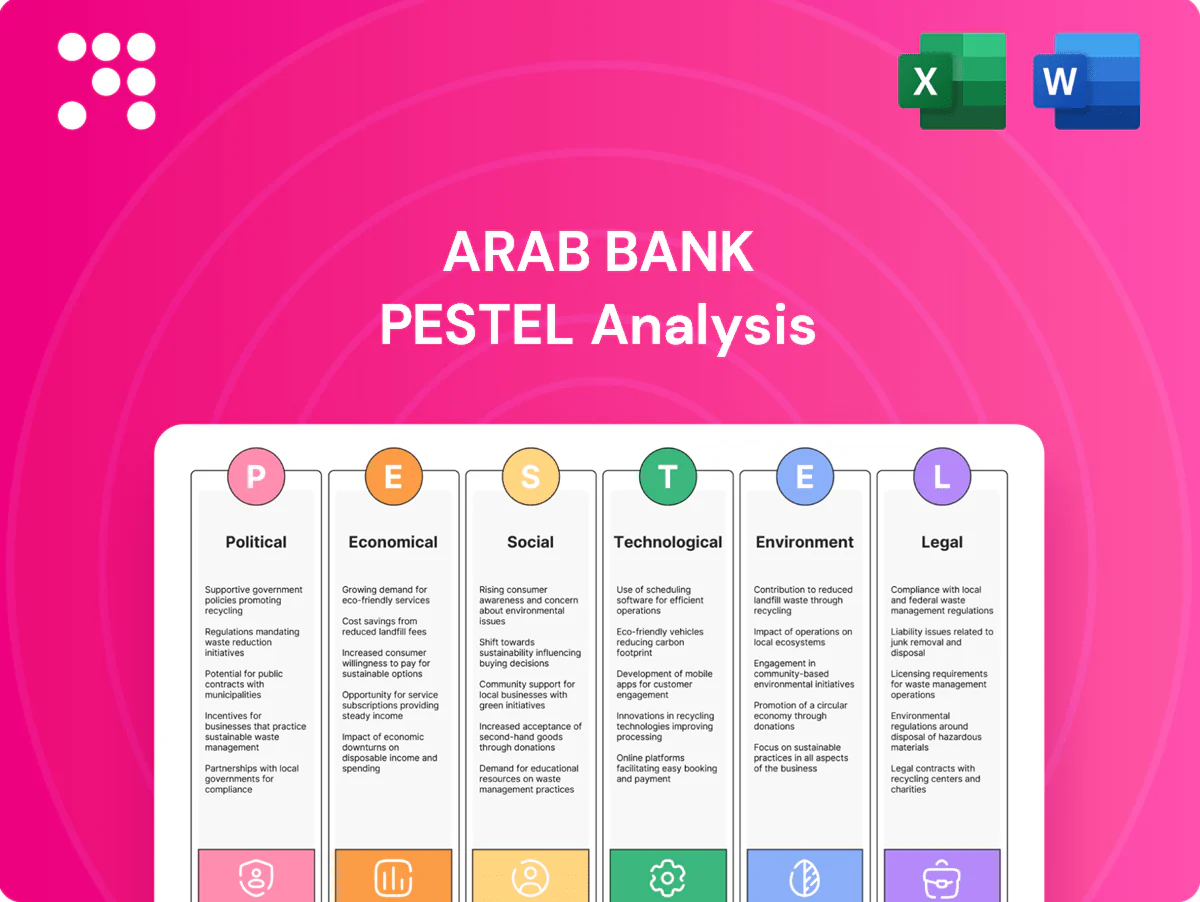

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Arab Bank, with data-backed trends and region-specific examples; designed for executives and investors to identify risks, opportunities and forward-looking scenarios for strategic planning and funding decisions.

A concise, visually segmented PESTLE summary of Arab Bank that distills regulatory, economic, social, technological, environmental and political risks into one-slide-ready notes, easily editable and shareable for teams, client reports and on-the-go reviews.

Economic factors

Oil price cycles and regional liquidity

Hydrocarbon revenues shape fiscal spending, deposit flows and corporate investment across Arab Bank’s core markets; Brent averaged about 88 USD/bbl in 2024 and traded roughly 80–95 USD/bbl in H1 2025. Higher prices lift fee and lending volumes while downturns compress liquidity and raise default risk. Balance-sheet flexibility and sector diversification are vital, and treasury strategies should use hedges and commodity-linked swaps to manage volatility.

Interest rate and FX dynamics

Global rate paths—US Fed funds at 5.25–5.50% (mid-2025)—drive NIM, funding costs and cross-currency loan demand; higher developed-market yields tighten emerging-market spreads. Pegged regimes (eg Jordan's stable peg to the US dollar) lower local volatility but transmit external shocks and funding repricing. Active ALM, duration management and prudent FX exposure limits preserve earnings; disciplined pricing sustains spread resilience.

Remittances and diaspora flows

Arab Bank’s 30+ country network with over 600 branches leverages strong remittance corridors into MENA, supporting high-volume payment flows that generate fee income and cross-sell opportunities.

World Bank analysis (2024) highlights remittances as a key external financing source for many MENA economies, but economic slowdowns in host countries can quickly compress flows.

Investment in competitive digital channels and transparent pricing helps Arab Bank retain share amid rising fintech competition.

SME and infrastructure demand

Regional development plans (eg GCC pipeline ~US$1.5tn to 2030) drive bank financing for transport, energy and social projects while SMEs in MENA face large working-capital and trade-finance needs; rigorous underwriting and guarantee schemes (eg EBRD/IFC facilities) reduce credit risk and blended finance/PPP structures improve returns.

- Infrastructure pipeline: US$1.5tn to 2030

- SME needs: working capital, trade finance, advisory

- Risk tools: guarantees, strict underwriting

- Return enhancers: blended finance, PPPs

Inflation and cost pressures

Imported inflation from 2022–23 commodity and energy shocks and widespread 2024 subsidy reforms in the region have tightened household affordability and elevated probability of default, while Arab Bank faces rising operating costs from increased compliance and digital-investment spend that compress margins. Dynamic repricing and strict cost discipline are required to sustain ROE, and credit models should incorporate real-income stress scenarios.

- Imported inflation & subsidy reforms → higher PDs

- Compliance + tech investments ↑ operating costs, pressure on NIMs

- Dynamic repricing + cost discipline to protect ROE

- Credit models must add real-income stress tests

Sanctions, regional risk and compliance strain correspondent access amid rapid digital payment growth

Hydrocarbon revenue swings (Brent avg 88 USD/bbl in 2024) drive fiscal spending, deposit flows and corporate lending; hedges and commodity swaps are essential. Global rates (US Fed funds 5.25–5.50% mid‑2025) and currency pegs shape NIM and funding costs; active ALM and FX limits preserve spreads. Remittances and a US$1.5tn GCC infrastructure pipeline to 2030 support fee income but imported inflation and subsidy reform raise PDs and operating costs.

| Indicator | Value |

|---|---|

| Brent (2024) | ~88 USD/bbl |

| Fed funds (mid‑2025) | 5.25–5.50% |

| GCC infra to 2030 | US$1.5tn |

| Arab Bank network | 600+ branches |

Preview Before You Purchase

Arab Bank PESTLE Analysis

The preview shown here is the exact Arab Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete content and professional structure. No placeholders or teasers—download the same file immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Arab Bank—concise, evidence-based insights into political, economic, social, technological, legal and environmental forces shaping performance. Ideal for investors, advisors and executives, it highlights risks and growth levers you can act on immediately. Purchase the full report to download editable charts, data and actionable recommendations.

Political factors

Geopolitical volatility in MENA

Regional conflicts, political transitions, and policy shifts can disrupt operations, risk appetite, and client activity across Arab Bank’s 30+ country footprint.

Country risk premia, FX convertibility issues in markets such as Lebanon and Sudan, and supply-chain frictions affect credit quality and liquidity planning.

Scenario planning and diversified geographic exposure mitigate shocks, while continuous monitoring of sanctions and diplomatic developments remains essential.

Sanctions and cross-border compliance

Exposure in 30+ jurisdictions requires rigorous screening against OFAC SDN (14,000+ entries as of 2025), EU and UK lists; errors can trigger multi‑million fines, de‑risking of correspondent lines and reputational damage. Investment in KYC/AML systems and staff training is a strategic necessity, and proactive engagement with regulators preserves access to global payment rails.

Government banking relationships

Arab Banks sovereign and quasi-sovereign clients significantly shape its loan book, funding and fee income given the group's footprint in over 30 countries and legacy since 1930; policy-driven infrastructure programs across MENA can expand corporate pipelines but increase concentration risk that must be actively managed. Transparent pricing and strict risk-adjusted return thresholds are essential when handling public-sector mandates to protect capital and margins.

Regulatory harmonization and fragmentation

Operating across MENA, Europe and other markets means Arab Bank, present in over 30 countries, must navigate divergent prudential and consumer rules and differing implementations of Basel III and local liquidity regimes. Non-uniform capital and liquidity standards increase compliance complexity and overhead. Harmonization efforts can unlock efficiencies but progress remains uneven, so local partnerships and adaptive compliance frameworks reduce regulatory friction.

- Presence: over 30 countries

- Frameworks: Basel III + local variations

- Impact: higher compliance complexity and costs

- Mitigation: local partnerships, adaptive compliance

Public policy on financial inclusion

National agendas to digitize payments and bank the unbanked create clear growth avenues for Arab Bank; Jordan’s financial inclusion push targets significant account penetration increases and regional digital payments surged about 20% in 2023, expanding fee-light transaction volumes. Government incentives and guarantee schemes for SME lending—mobilizing billions regionally—support portfolio expansion but require prudent credit frameworks and robust risk analytics. Demonstrating measurable social impact improves regulatory standing and license-to-operate.

Sanctions, regional risk and compliance strain correspondent access amid rapid digital payment growth

Regional conflicts, policy shifts and sanctions exposure across 30+ jurisdictions materially affect Arab Bank’s credit, liquidity and correspondent access.

OFAC SDN list exceeds 14,000 entries (2025); non‑compliance risks multi‑million fines and de‑risking of lines.

Digital payments growth (~20% in 2023) and SME guarantee schemes present growth with concentration and compliance trade‑offs.

| Metric | Value |

|---|---|

| Jurisdictions | 30+ |

| OFAC SDN | 14,000+ |

| Digital payments growth (2023) | ~20% |

| Founded | 1930 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Arab Bank, with data-backed trends and region-specific examples; designed for executives and investors to identify risks, opportunities and forward-looking scenarios for strategic planning and funding decisions.

A concise, visually segmented PESTLE summary of Arab Bank that distills regulatory, economic, social, technological, environmental and political risks into one-slide-ready notes, easily editable and shareable for teams, client reports and on-the-go reviews.

Economic factors

Oil price cycles and regional liquidity

Hydrocarbon revenues shape fiscal spending, deposit flows and corporate investment across Arab Bank’s core markets; Brent averaged about 88 USD/bbl in 2024 and traded roughly 80–95 USD/bbl in H1 2025. Higher prices lift fee and lending volumes while downturns compress liquidity and raise default risk. Balance-sheet flexibility and sector diversification are vital, and treasury strategies should use hedges and commodity-linked swaps to manage volatility.

Interest rate and FX dynamics

Global rate paths—US Fed funds at 5.25–5.50% (mid-2025)—drive NIM, funding costs and cross-currency loan demand; higher developed-market yields tighten emerging-market spreads. Pegged regimes (eg Jordan's stable peg to the US dollar) lower local volatility but transmit external shocks and funding repricing. Active ALM, duration management and prudent FX exposure limits preserve earnings; disciplined pricing sustains spread resilience.

Remittances and diaspora flows

Arab Bank’s 30+ country network with over 600 branches leverages strong remittance corridors into MENA, supporting high-volume payment flows that generate fee income and cross-sell opportunities.

World Bank analysis (2024) highlights remittances as a key external financing source for many MENA economies, but economic slowdowns in host countries can quickly compress flows.

Investment in competitive digital channels and transparent pricing helps Arab Bank retain share amid rising fintech competition.

SME and infrastructure demand

Regional development plans (eg GCC pipeline ~US$1.5tn to 2030) drive bank financing for transport, energy and social projects while SMEs in MENA face large working-capital and trade-finance needs; rigorous underwriting and guarantee schemes (eg EBRD/IFC facilities) reduce credit risk and blended finance/PPP structures improve returns.

- Infrastructure pipeline: US$1.5tn to 2030

- SME needs: working capital, trade finance, advisory

- Risk tools: guarantees, strict underwriting

- Return enhancers: blended finance, PPPs

Inflation and cost pressures

Imported inflation from 2022–23 commodity and energy shocks and widespread 2024 subsidy reforms in the region have tightened household affordability and elevated probability of default, while Arab Bank faces rising operating costs from increased compliance and digital-investment spend that compress margins. Dynamic repricing and strict cost discipline are required to sustain ROE, and credit models should incorporate real-income stress scenarios.

- Imported inflation & subsidy reforms → higher PDs

- Compliance + tech investments ↑ operating costs, pressure on NIMs

- Dynamic repricing + cost discipline to protect ROE

- Credit models must add real-income stress tests

Sanctions, regional risk and compliance strain correspondent access amid rapid digital payment growth

Hydrocarbon revenue swings (Brent avg 88 USD/bbl in 2024) drive fiscal spending, deposit flows and corporate lending; hedges and commodity swaps are essential. Global rates (US Fed funds 5.25–5.50% mid‑2025) and currency pegs shape NIM and funding costs; active ALM and FX limits preserve spreads. Remittances and a US$1.5tn GCC infrastructure pipeline to 2030 support fee income but imported inflation and subsidy reform raise PDs and operating costs.

| Indicator | Value |

|---|---|

| Brent (2024) | ~88 USD/bbl |

| Fed funds (mid‑2025) | 5.25–5.50% |

| GCC infra to 2030 | US$1.5tn |

| Arab Bank network | 600+ branches |

Preview Before You Purchase

Arab Bank PESTLE Analysis

The preview shown here is the exact Arab Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete content and professional structure. No placeholders or teasers—download the same file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Arab Bank—concise, evidence-based insights into political, economic, social, technological, legal and environmental forces shaping performance. Ideal for investors, advisors and executives, it highlights risks and growth levers you can act on immediately. Purchase the full report to download editable charts, data and actionable recommendations.

Political factors

Geopolitical volatility in MENA

Regional conflicts, political transitions, and policy shifts can disrupt operations, risk appetite, and client activity across Arab Bank’s 30+ country footprint.

Country risk premia, FX convertibility issues in markets such as Lebanon and Sudan, and supply-chain frictions affect credit quality and liquidity planning.

Scenario planning and diversified geographic exposure mitigate shocks, while continuous monitoring of sanctions and diplomatic developments remains essential.

Sanctions and cross-border compliance

Exposure in 30+ jurisdictions requires rigorous screening against OFAC SDN (14,000+ entries as of 2025), EU and UK lists; errors can trigger multi‑million fines, de‑risking of correspondent lines and reputational damage. Investment in KYC/AML systems and staff training is a strategic necessity, and proactive engagement with regulators preserves access to global payment rails.

Government banking relationships

Arab Banks sovereign and quasi-sovereign clients significantly shape its loan book, funding and fee income given the group's footprint in over 30 countries and legacy since 1930; policy-driven infrastructure programs across MENA can expand corporate pipelines but increase concentration risk that must be actively managed. Transparent pricing and strict risk-adjusted return thresholds are essential when handling public-sector mandates to protect capital and margins.

Regulatory harmonization and fragmentation

Operating across MENA, Europe and other markets means Arab Bank, present in over 30 countries, must navigate divergent prudential and consumer rules and differing implementations of Basel III and local liquidity regimes. Non-uniform capital and liquidity standards increase compliance complexity and overhead. Harmonization efforts can unlock efficiencies but progress remains uneven, so local partnerships and adaptive compliance frameworks reduce regulatory friction.

- Presence: over 30 countries

- Frameworks: Basel III + local variations

- Impact: higher compliance complexity and costs

- Mitigation: local partnerships, adaptive compliance

Public policy on financial inclusion

National agendas to digitize payments and bank the unbanked create clear growth avenues for Arab Bank; Jordan’s financial inclusion push targets significant account penetration increases and regional digital payments surged about 20% in 2023, expanding fee-light transaction volumes. Government incentives and guarantee schemes for SME lending—mobilizing billions regionally—support portfolio expansion but require prudent credit frameworks and robust risk analytics. Demonstrating measurable social impact improves regulatory standing and license-to-operate.

Sanctions, regional risk and compliance strain correspondent access amid rapid digital payment growth

Regional conflicts, policy shifts and sanctions exposure across 30+ jurisdictions materially affect Arab Bank’s credit, liquidity and correspondent access.

OFAC SDN list exceeds 14,000 entries (2025); non‑compliance risks multi‑million fines and de‑risking of lines.

Digital payments growth (~20% in 2023) and SME guarantee schemes present growth with concentration and compliance trade‑offs.

| Metric | Value |

|---|---|

| Jurisdictions | 30+ |

| OFAC SDN | 14,000+ |

| Digital payments growth (2023) | ~20% |

| Founded | 1930 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Arab Bank, with data-backed trends and region-specific examples; designed for executives and investors to identify risks, opportunities and forward-looking scenarios for strategic planning and funding decisions.

A concise, visually segmented PESTLE summary of Arab Bank that distills regulatory, economic, social, technological, environmental and political risks into one-slide-ready notes, easily editable and shareable for teams, client reports and on-the-go reviews.

Economic factors

Oil price cycles and regional liquidity

Hydrocarbon revenues shape fiscal spending, deposit flows and corporate investment across Arab Bank’s core markets; Brent averaged about 88 USD/bbl in 2024 and traded roughly 80–95 USD/bbl in H1 2025. Higher prices lift fee and lending volumes while downturns compress liquidity and raise default risk. Balance-sheet flexibility and sector diversification are vital, and treasury strategies should use hedges and commodity-linked swaps to manage volatility.

Interest rate and FX dynamics

Global rate paths—US Fed funds at 5.25–5.50% (mid-2025)—drive NIM, funding costs and cross-currency loan demand; higher developed-market yields tighten emerging-market spreads. Pegged regimes (eg Jordan's stable peg to the US dollar) lower local volatility but transmit external shocks and funding repricing. Active ALM, duration management and prudent FX exposure limits preserve earnings; disciplined pricing sustains spread resilience.

Remittances and diaspora flows

Arab Bank’s 30+ country network with over 600 branches leverages strong remittance corridors into MENA, supporting high-volume payment flows that generate fee income and cross-sell opportunities.

World Bank analysis (2024) highlights remittances as a key external financing source for many MENA economies, but economic slowdowns in host countries can quickly compress flows.

Investment in competitive digital channels and transparent pricing helps Arab Bank retain share amid rising fintech competition.

SME and infrastructure demand

Regional development plans (eg GCC pipeline ~US$1.5tn to 2030) drive bank financing for transport, energy and social projects while SMEs in MENA face large working-capital and trade-finance needs; rigorous underwriting and guarantee schemes (eg EBRD/IFC facilities) reduce credit risk and blended finance/PPP structures improve returns.

- Infrastructure pipeline: US$1.5tn to 2030

- SME needs: working capital, trade finance, advisory

- Risk tools: guarantees, strict underwriting

- Return enhancers: blended finance, PPPs

Inflation and cost pressures

Imported inflation from 2022–23 commodity and energy shocks and widespread 2024 subsidy reforms in the region have tightened household affordability and elevated probability of default, while Arab Bank faces rising operating costs from increased compliance and digital-investment spend that compress margins. Dynamic repricing and strict cost discipline are required to sustain ROE, and credit models should incorporate real-income stress scenarios.

- Imported inflation & subsidy reforms → higher PDs

- Compliance + tech investments ↑ operating costs, pressure on NIMs

- Dynamic repricing + cost discipline to protect ROE

- Credit models must add real-income stress tests

Sanctions, regional risk and compliance strain correspondent access amid rapid digital payment growth

Hydrocarbon revenue swings (Brent avg 88 USD/bbl in 2024) drive fiscal spending, deposit flows and corporate lending; hedges and commodity swaps are essential. Global rates (US Fed funds 5.25–5.50% mid‑2025) and currency pegs shape NIM and funding costs; active ALM and FX limits preserve spreads. Remittances and a US$1.5tn GCC infrastructure pipeline to 2030 support fee income but imported inflation and subsidy reform raise PDs and operating costs.

| Indicator | Value |

|---|---|

| Brent (2024) | ~88 USD/bbl |

| Fed funds (mid‑2025) | 5.25–5.50% |

| GCC infra to 2030 | US$1.5tn |

| Arab Bank network | 600+ branches |

Preview Before You Purchase

Arab Bank PESTLE Analysis

The preview shown here is the exact Arab Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete content and professional structure. No placeholders or teasers—download the same file immediately after checkout.