ARB Corp Porter's Five Forces Analysis

From Overview to Strategy Blueprint

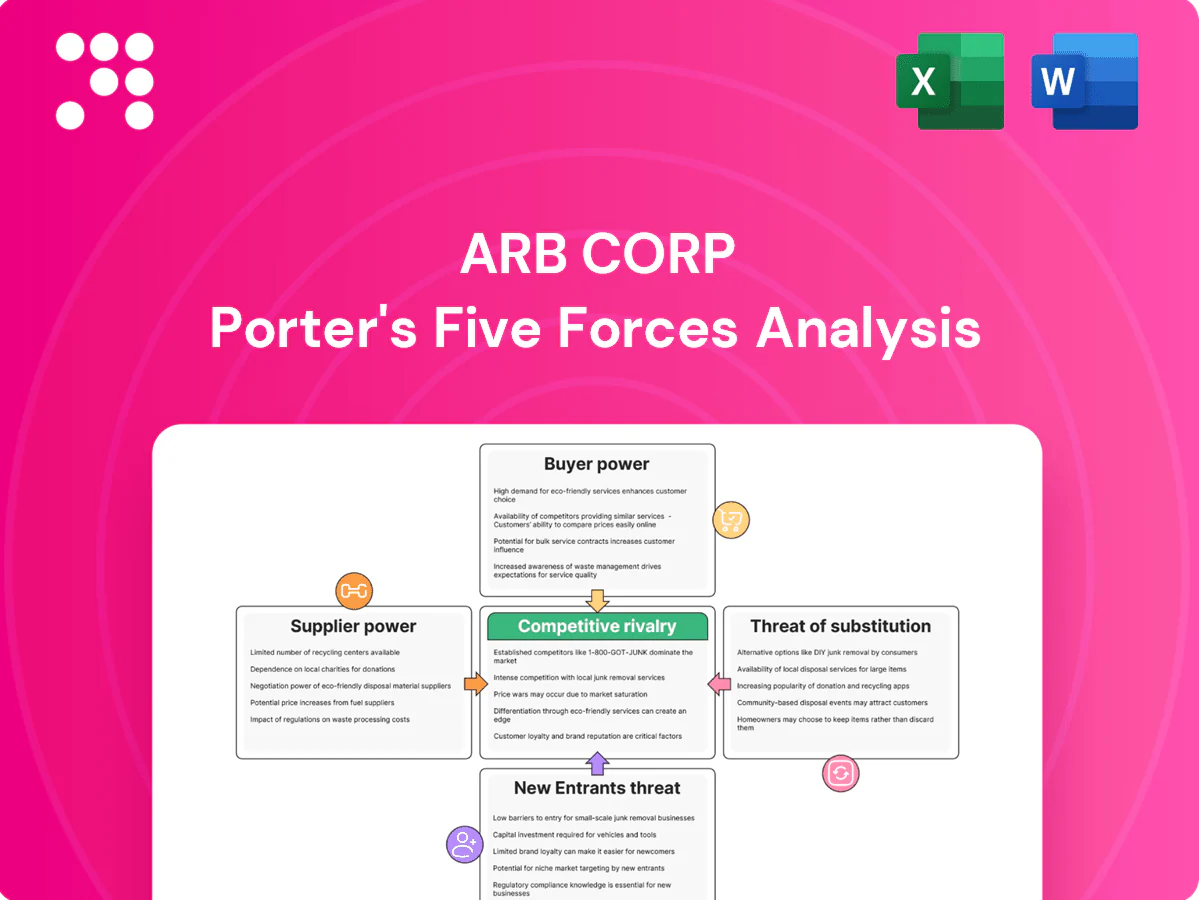

ARB Corp faces intense rivalry in the aftermarket 4x4 accessories market, driven by strong brand loyalty, channel partnerships and evolving consumer preferences, while supplier power and substitute threats shape margin pressure and innovation demands. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for ARB Corp.

Suppliers Bargaining Power

Concentrated specialty inputs

ARB depends on specialty steel, aluminum extrusions, precision castings, shock internals and electronics where qualified suppliers are limited, creating concentrated supplier power. Single-source tooling for bull bars, lockers and compressors raises switching costs and gives niche suppliers leverage over pricing and lead times. ARB mitigates this by multi-sourcing where feasible and securing long-term supply agreements.

Commodity price volatility

Fluctuations in steel (H1 2024 down ~15% year-on-year), aluminum (H1 2024 up ~5%) and freight rates create margin pressure that can force ARB to adjust selling prices. Suppliers have passed surcharges during tight pockets in 2024, strengthening their bargaining position. Hedging and forward contracts have partially stabilized input costs. Design-to-cost and material substitution reduce exposure to raw-material spikes.

Quality and certification dependencies

ARB’s products must meet strict safety and off-road performance standards, including Australian Design Rules and crash compatibility, so only a limited set of qualified vendors can meet ARB’s tolerances and validation, increasing supplier power. Requalification of new suppliers is time-consuming and costly, often requiring extensive testing and validation. ARB’s strategic supplier development programs gradually reduce this concentrated risk over time.

Global logistics and lead-time risk

Extended supply chains across Asia-Pacific, Europe and the US expose ARB to shipping disruptions and port congestion, giving carriers and key components suppliers increased leverage when freight capacity tightens; inventory buffers and nearshoring mitigate risk but raise working capital requirements, and scenario planning strengthens continuity.

- Supply footprint: Asia-Pacific, Europe, US

- Risk: carriers gain leverage when capacity tightens

- Mitigants: inventory buffers, nearshoring, scenario planning

Brand reputation reliance

ARB (ASX: ARB) bases brand on durability; if critical suppliers falter, warranty exposure and reputational damage threaten product credibility in 2024. Dependence can force ARB to absorb higher input costs to secure quality, while preferred-supplier agreements trade price concessions for reliability. Joint R&D partnerships align incentives and reduce supplier leverage.

- supplier risk: warranty/reputation

- costs: higher to secure quality

- preferred-supplier: price for reliability

- joint R&D: aligns incentives, lowers supplier power

Supplier concentration raises costs; steel -15%, aluminium +5%

ARB faces concentrated supplier power for specialty steels, aluminium extrusions, precision castings and electronics; single-source tooling raises switching costs and validation time. H1 2024: steel input prices down ~15% y/y, aluminium up ~5%; suppliers passed surcharges in tight pockets. Mitigants include multi-sourcing, long-term contracts, hedging and supplier development.

| Metric | 2024 |

|---|---|

| Steel price | -15% H1 2024 |

| Aluminium price | +5% H1 2024 |

| Freight | Surcharges in tight pockets 2024 |

What is included in the product

Comprehensive Porter’s Five Forces analysis of ARB Corp, assessing competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and identifying strategic levers and disruptive risks that influence pricing, margins and market share.

A concise one-sheet Porter's Five Forces for ARB Corp that maps supplier/customer power, rivalry and entry/substitution threats with customizable pressure levels and an instant spider chart—copy-ready for decks, integrates into Excel dashboards and speeds strategic decisions.

Customers Bargaining Power

Diverse customer mix

Customers span retail 4x4 enthusiasts, fleets, mining, government and export dealers, and ARB exports to over 100 countries, diluting single-buyer risk. Fragmented retail buyers have limited individual power, while fleet tendering and large mining contracts increase buyer leverage. ARB’s company stores and dealer network reduce channel dependence. A shift toward fleet sales in 2024 would raise average buyer power and contract pressure.

High information transparency

High information transparency lets ~90% of buyers consult online reviews and forums (2024), making price-performance comparisons and cross-shopping between ARB, Ironman 4x4, TJM, Rhino-Rack and global brands routine. This visibility raises price sensitivity, especially in commoditized accessories like roof racks and recovery gear. ARB’s strong brand equity and warranty offerings, cited frequently in reviews, help blunt pure price-based switching.

Product differentiation and switching costs

ARB’s proprietary products like Air Locker and engineered bull bars create perceived switching costs by fitting specific vehicle architectures and supporting integrated accessory ecosystems, which raises customer lock-in and reduces bargaining leverage.

For commoditised lines such as roof racks, auxiliary lights and camping gear, switching is easier and customer price sensitivity increases, elevating bargaining power in those segments.

Bundled fitment services and point-of-sale finance offers lower buyers’ effective price resistance and friction for switching, further diminishing customer bargaining power for core, high-margin accessories.

After-sales and installer influence

After-sales fitment quality and nationwide service are critical for safety-critical parts, so installers and dealers often steer buyer choice and reduce direct end-user bargaining; ARB (ASX: ARB) leverages a mix of company and franchised stores to capture margin and influence demand. Service SLAs and warranties in FY2024 reinforced loyalty, shifting competition from price to reliability.

- Installers drive choice

- Nationwide service = safety trust

- ARB retail footprint captures margin

- SLAs/warranties reduce price haggling

Macro sensitivity and discretionary spend

Accessories are partly discretionary and cyclical, increasing discount pressure in downturns as households curb non-essentials; with Australia’s CPI around 4% in 2024, buyers tightened spend and negotiated harder when fuel and living-cost pressures rose. Premium 4x4 buyers remain less elastic but still seek value, while targeted financing and promotions in 2024 helped stabilise conversions without deep blanket price cuts.

- Discretionary mix raises price sensitivity

- Higher fuel/CPI in 2024 boosted buyer leverage

- Premium segment: lower elasticity, higher value-seeking

- Financing/promotions reduce need for deep discounts

Exports to >100 countries; ~90% consult online, increasing price sensitivity

Customers range from fragmented retail 4x4 buyers to fleets/mining/government; exports >100 countries dilute single-buyer risk while large tenders increase leverage. About 90% consult online in 2024, raising price sensitivity though ARB’s brand, warranties and proprietary items increase switching costs. Commoditised lines carry higher buyer power; FY2024 SLAs/stores reduce direct bargaining amid ~4% CPI.

| Metric | 2024 | Impact |

|---|---|---|

| Online research | ~90% | Higher price sensitivity |

| Exports | >100 countries | Lower single-buyer risk |

| Australia CPI | ~4% | Increased negotiation |

Preview Before You Purchase

ARB Corp Porter's Five Forces Analysis

This preview shows the exact ARB Corp Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no mockups. It is the fully formatted, ready-to-use document covering competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants. Instant download upon payment; the content is identical to what you see here.

From Overview to Strategy Blueprint

ARB Corp faces intense rivalry in the aftermarket 4x4 accessories market, driven by strong brand loyalty, channel partnerships and evolving consumer preferences, while supplier power and substitute threats shape margin pressure and innovation demands. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for ARB Corp.

Suppliers Bargaining Power

Concentrated specialty inputs

ARB depends on specialty steel, aluminum extrusions, precision castings, shock internals and electronics where qualified suppliers are limited, creating concentrated supplier power. Single-source tooling for bull bars, lockers and compressors raises switching costs and gives niche suppliers leverage over pricing and lead times. ARB mitigates this by multi-sourcing where feasible and securing long-term supply agreements.

Commodity price volatility

Fluctuations in steel (H1 2024 down ~15% year-on-year), aluminum (H1 2024 up ~5%) and freight rates create margin pressure that can force ARB to adjust selling prices. Suppliers have passed surcharges during tight pockets in 2024, strengthening their bargaining position. Hedging and forward contracts have partially stabilized input costs. Design-to-cost and material substitution reduce exposure to raw-material spikes.

Quality and certification dependencies

ARB’s products must meet strict safety and off-road performance standards, including Australian Design Rules and crash compatibility, so only a limited set of qualified vendors can meet ARB’s tolerances and validation, increasing supplier power. Requalification of new suppliers is time-consuming and costly, often requiring extensive testing and validation. ARB’s strategic supplier development programs gradually reduce this concentrated risk over time.

Global logistics and lead-time risk

Extended supply chains across Asia-Pacific, Europe and the US expose ARB to shipping disruptions and port congestion, giving carriers and key components suppliers increased leverage when freight capacity tightens; inventory buffers and nearshoring mitigate risk but raise working capital requirements, and scenario planning strengthens continuity.

- Supply footprint: Asia-Pacific, Europe, US

- Risk: carriers gain leverage when capacity tightens

- Mitigants: inventory buffers, nearshoring, scenario planning

Brand reputation reliance

ARB (ASX: ARB) bases brand on durability; if critical suppliers falter, warranty exposure and reputational damage threaten product credibility in 2024. Dependence can force ARB to absorb higher input costs to secure quality, while preferred-supplier agreements trade price concessions for reliability. Joint R&D partnerships align incentives and reduce supplier leverage.

- supplier risk: warranty/reputation

- costs: higher to secure quality

- preferred-supplier: price for reliability

- joint R&D: aligns incentives, lowers supplier power

Supplier concentration raises costs; steel -15%, aluminium +5%

ARB faces concentrated supplier power for specialty steels, aluminium extrusions, precision castings and electronics; single-source tooling raises switching costs and validation time. H1 2024: steel input prices down ~15% y/y, aluminium up ~5%; suppliers passed surcharges in tight pockets. Mitigants include multi-sourcing, long-term contracts, hedging and supplier development.

| Metric | 2024 |

|---|---|

| Steel price | -15% H1 2024 |

| Aluminium price | +5% H1 2024 |

| Freight | Surcharges in tight pockets 2024 |

What is included in the product

Comprehensive Porter’s Five Forces analysis of ARB Corp, assessing competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and identifying strategic levers and disruptive risks that influence pricing, margins and market share.

A concise one-sheet Porter's Five Forces for ARB Corp that maps supplier/customer power, rivalry and entry/substitution threats with customizable pressure levels and an instant spider chart—copy-ready for decks, integrates into Excel dashboards and speeds strategic decisions.

Customers Bargaining Power

Diverse customer mix

Customers span retail 4x4 enthusiasts, fleets, mining, government and export dealers, and ARB exports to over 100 countries, diluting single-buyer risk. Fragmented retail buyers have limited individual power, while fleet tendering and large mining contracts increase buyer leverage. ARB’s company stores and dealer network reduce channel dependence. A shift toward fleet sales in 2024 would raise average buyer power and contract pressure.

High information transparency

High information transparency lets ~90% of buyers consult online reviews and forums (2024), making price-performance comparisons and cross-shopping between ARB, Ironman 4x4, TJM, Rhino-Rack and global brands routine. This visibility raises price sensitivity, especially in commoditized accessories like roof racks and recovery gear. ARB’s strong brand equity and warranty offerings, cited frequently in reviews, help blunt pure price-based switching.

Product differentiation and switching costs

ARB’s proprietary products like Air Locker and engineered bull bars create perceived switching costs by fitting specific vehicle architectures and supporting integrated accessory ecosystems, which raises customer lock-in and reduces bargaining leverage.

For commoditised lines such as roof racks, auxiliary lights and camping gear, switching is easier and customer price sensitivity increases, elevating bargaining power in those segments.

Bundled fitment services and point-of-sale finance offers lower buyers’ effective price resistance and friction for switching, further diminishing customer bargaining power for core, high-margin accessories.

After-sales and installer influence

After-sales fitment quality and nationwide service are critical for safety-critical parts, so installers and dealers often steer buyer choice and reduce direct end-user bargaining; ARB (ASX: ARB) leverages a mix of company and franchised stores to capture margin and influence demand. Service SLAs and warranties in FY2024 reinforced loyalty, shifting competition from price to reliability.

- Installers drive choice

- Nationwide service = safety trust

- ARB retail footprint captures margin

- SLAs/warranties reduce price haggling

Macro sensitivity and discretionary spend

Accessories are partly discretionary and cyclical, increasing discount pressure in downturns as households curb non-essentials; with Australia’s CPI around 4% in 2024, buyers tightened spend and negotiated harder when fuel and living-cost pressures rose. Premium 4x4 buyers remain less elastic but still seek value, while targeted financing and promotions in 2024 helped stabilise conversions without deep blanket price cuts.

- Discretionary mix raises price sensitivity

- Higher fuel/CPI in 2024 boosted buyer leverage

- Premium segment: lower elasticity, higher value-seeking

- Financing/promotions reduce need for deep discounts

Exports to >100 countries; ~90% consult online, increasing price sensitivity

Customers range from fragmented retail 4x4 buyers to fleets/mining/government; exports >100 countries dilute single-buyer risk while large tenders increase leverage. About 90% consult online in 2024, raising price sensitivity though ARB’s brand, warranties and proprietary items increase switching costs. Commoditised lines carry higher buyer power; FY2024 SLAs/stores reduce direct bargaining amid ~4% CPI.

| Metric | 2024 | Impact |

|---|---|---|

| Online research | ~90% | Higher price sensitivity |

| Exports | >100 countries | Lower single-buyer risk |

| Australia CPI | ~4% | Increased negotiation |

Preview Before You Purchase

ARB Corp Porter's Five Forces Analysis

This preview shows the exact ARB Corp Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no mockups. It is the fully formatted, ready-to-use document covering competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants. Instant download upon payment; the content is identical to what you see here.

Description

From Overview to Strategy Blueprint

ARB Corp faces intense rivalry in the aftermarket 4x4 accessories market, driven by strong brand loyalty, channel partnerships and evolving consumer preferences, while supplier power and substitute threats shape margin pressure and innovation demands. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for ARB Corp.

Suppliers Bargaining Power

Concentrated specialty inputs

ARB depends on specialty steel, aluminum extrusions, precision castings, shock internals and electronics where qualified suppliers are limited, creating concentrated supplier power. Single-source tooling for bull bars, lockers and compressors raises switching costs and gives niche suppliers leverage over pricing and lead times. ARB mitigates this by multi-sourcing where feasible and securing long-term supply agreements.

Commodity price volatility

Fluctuations in steel (H1 2024 down ~15% year-on-year), aluminum (H1 2024 up ~5%) and freight rates create margin pressure that can force ARB to adjust selling prices. Suppliers have passed surcharges during tight pockets in 2024, strengthening their bargaining position. Hedging and forward contracts have partially stabilized input costs. Design-to-cost and material substitution reduce exposure to raw-material spikes.

Quality and certification dependencies

ARB’s products must meet strict safety and off-road performance standards, including Australian Design Rules and crash compatibility, so only a limited set of qualified vendors can meet ARB’s tolerances and validation, increasing supplier power. Requalification of new suppliers is time-consuming and costly, often requiring extensive testing and validation. ARB’s strategic supplier development programs gradually reduce this concentrated risk over time.

Global logistics and lead-time risk

Extended supply chains across Asia-Pacific, Europe and the US expose ARB to shipping disruptions and port congestion, giving carriers and key components suppliers increased leverage when freight capacity tightens; inventory buffers and nearshoring mitigate risk but raise working capital requirements, and scenario planning strengthens continuity.

- Supply footprint: Asia-Pacific, Europe, US

- Risk: carriers gain leverage when capacity tightens

- Mitigants: inventory buffers, nearshoring, scenario planning

Brand reputation reliance

ARB (ASX: ARB) bases brand on durability; if critical suppliers falter, warranty exposure and reputational damage threaten product credibility in 2024. Dependence can force ARB to absorb higher input costs to secure quality, while preferred-supplier agreements trade price concessions for reliability. Joint R&D partnerships align incentives and reduce supplier leverage.

- supplier risk: warranty/reputation

- costs: higher to secure quality

- preferred-supplier: price for reliability

- joint R&D: aligns incentives, lowers supplier power

Supplier concentration raises costs; steel -15%, aluminium +5%

ARB faces concentrated supplier power for specialty steels, aluminium extrusions, precision castings and electronics; single-source tooling raises switching costs and validation time. H1 2024: steel input prices down ~15% y/y, aluminium up ~5%; suppliers passed surcharges in tight pockets. Mitigants include multi-sourcing, long-term contracts, hedging and supplier development.

| Metric | 2024 |

|---|---|

| Steel price | -15% H1 2024 |

| Aluminium price | +5% H1 2024 |

| Freight | Surcharges in tight pockets 2024 |

What is included in the product

Comprehensive Porter’s Five Forces analysis of ARB Corp, assessing competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and identifying strategic levers and disruptive risks that influence pricing, margins and market share.

A concise one-sheet Porter's Five Forces for ARB Corp that maps supplier/customer power, rivalry and entry/substitution threats with customizable pressure levels and an instant spider chart—copy-ready for decks, integrates into Excel dashboards and speeds strategic decisions.

Customers Bargaining Power

Diverse customer mix

Customers span retail 4x4 enthusiasts, fleets, mining, government and export dealers, and ARB exports to over 100 countries, diluting single-buyer risk. Fragmented retail buyers have limited individual power, while fleet tendering and large mining contracts increase buyer leverage. ARB’s company stores and dealer network reduce channel dependence. A shift toward fleet sales in 2024 would raise average buyer power and contract pressure.

High information transparency

High information transparency lets ~90% of buyers consult online reviews and forums (2024), making price-performance comparisons and cross-shopping between ARB, Ironman 4x4, TJM, Rhino-Rack and global brands routine. This visibility raises price sensitivity, especially in commoditized accessories like roof racks and recovery gear. ARB’s strong brand equity and warranty offerings, cited frequently in reviews, help blunt pure price-based switching.

Product differentiation and switching costs

ARB’s proprietary products like Air Locker and engineered bull bars create perceived switching costs by fitting specific vehicle architectures and supporting integrated accessory ecosystems, which raises customer lock-in and reduces bargaining leverage.

For commoditised lines such as roof racks, auxiliary lights and camping gear, switching is easier and customer price sensitivity increases, elevating bargaining power in those segments.

Bundled fitment services and point-of-sale finance offers lower buyers’ effective price resistance and friction for switching, further diminishing customer bargaining power for core, high-margin accessories.

After-sales and installer influence

After-sales fitment quality and nationwide service are critical for safety-critical parts, so installers and dealers often steer buyer choice and reduce direct end-user bargaining; ARB (ASX: ARB) leverages a mix of company and franchised stores to capture margin and influence demand. Service SLAs and warranties in FY2024 reinforced loyalty, shifting competition from price to reliability.

- Installers drive choice

- Nationwide service = safety trust

- ARB retail footprint captures margin

- SLAs/warranties reduce price haggling

Macro sensitivity and discretionary spend

Accessories are partly discretionary and cyclical, increasing discount pressure in downturns as households curb non-essentials; with Australia’s CPI around 4% in 2024, buyers tightened spend and negotiated harder when fuel and living-cost pressures rose. Premium 4x4 buyers remain less elastic but still seek value, while targeted financing and promotions in 2024 helped stabilise conversions without deep blanket price cuts.

- Discretionary mix raises price sensitivity

- Higher fuel/CPI in 2024 boosted buyer leverage

- Premium segment: lower elasticity, higher value-seeking

- Financing/promotions reduce need for deep discounts

Exports to >100 countries; ~90% consult online, increasing price sensitivity

Customers range from fragmented retail 4x4 buyers to fleets/mining/government; exports >100 countries dilute single-buyer risk while large tenders increase leverage. About 90% consult online in 2024, raising price sensitivity though ARB’s brand, warranties and proprietary items increase switching costs. Commoditised lines carry higher buyer power; FY2024 SLAs/stores reduce direct bargaining amid ~4% CPI.

| Metric | 2024 | Impact |

|---|---|---|

| Online research | ~90% | Higher price sensitivity |

| Exports | >100 countries | Lower single-buyer risk |

| Australia CPI | ~4% | Increased negotiation |

Preview Before You Purchase

ARB Corp Porter's Five Forces Analysis

This preview shows the exact ARB Corp Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no mockups. It is the fully formatted, ready-to-use document covering competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants. Instant download upon payment; the content is identical to what you see here.