Arca Continental Porter's Five Forces Analysis

From Overview to Strategy Blueprint

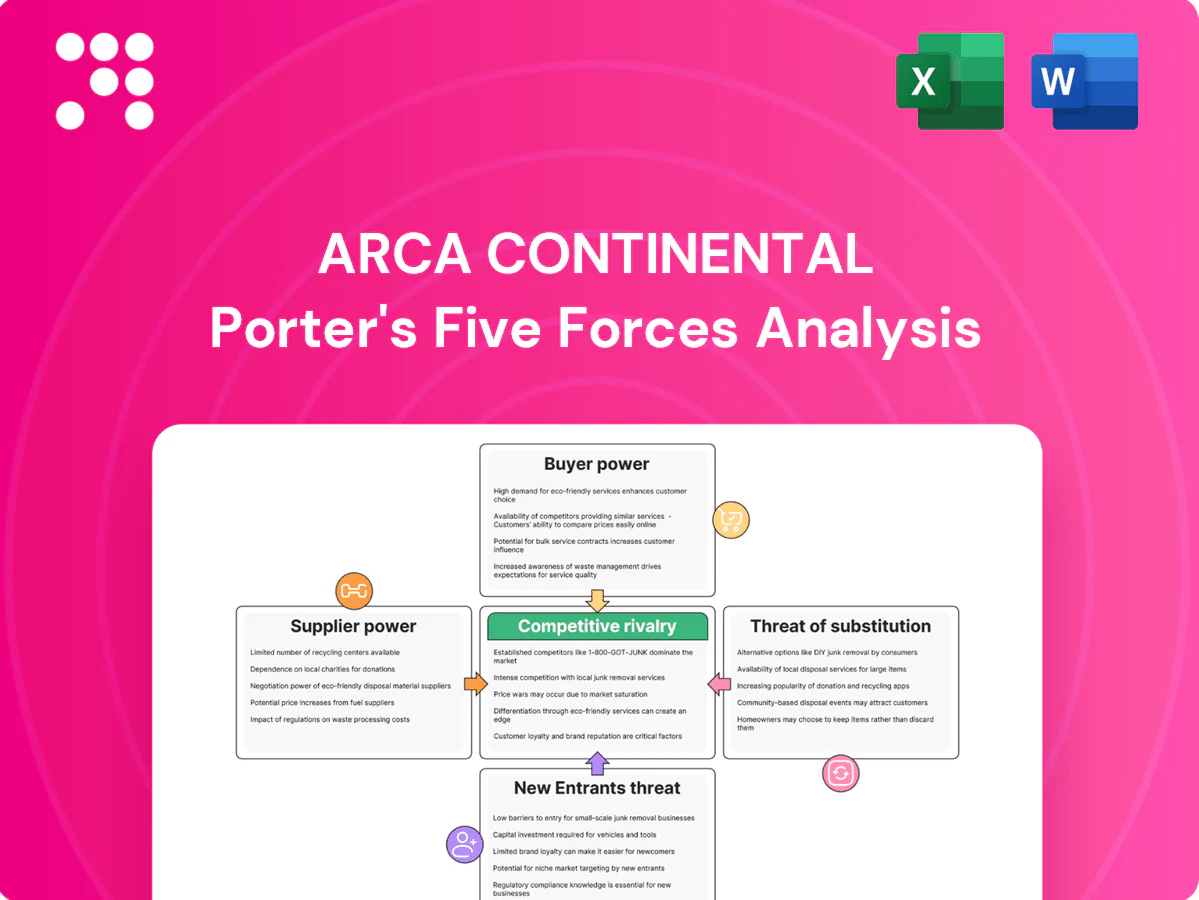

Arca Continental faces moderate buyer power and intense rivalry across beverages and packaging, with supplier leverage and capital intensity raising entry barriers while regional substitutes create niche risks. Strategic scale and distribution are key defenses, yet margin pressure persists. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arca Continental’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrate dependence on The Coca‑Cola Company

Arca Continental relies on Coca‑Cola Company concentrate under long‑term bottling agreements, giving the licensor notable leverage over pricing and quality standards. Formula or concentrate price adjustments are contractually passed through and directly affect Arca Continental margins. Performance clauses and marketing fund requirements further reinforce supplier power. Diversification into snacks and non‑cola beverages only partially offsets this dependence.

Commodity inputs: sugar, PET resin, aluminum

Key inputs—sugar, PET resin and aluminum—trade globally and remained volatile in 2024 (ICE raw sugar ~0.20 USD/lb, PET resin ~1,100 USD/ton, LME aluminum ~2,300 USD/ton), enabling upstream suppliers to pass through spikes. Limited substitution (PET vs glass/can) is constrained by packaging lines and consumer preferences. Hedging reduces short-term swings but cannot remove structural cost pressure. Local LatAm sugar policies and tariffs can amplify supplier leverage.

Packaging and equipment OEM concentration

Bottling lines, coolers and closures are sourced from a concentrated set of OEMs, creating switching costs and lock‑in as Coca‑Cola technical standards narrow vendor options; spare parts scarcity and strict maintenance schedules further strengthen OEM bargaining power, although Arca Continental’s regional scale (operations across six countries) allows it to secure volume discounts and better payment terms in 2024.

Logistics, CO2, and water treatment inputs

Logistics, industrial gases and water‑treatment chemicals are critical, time‑sensitive inputs; maritime shipping accounts for roughly 2.9% of global CO2 emissions and EU ETS carbon averaged about €88/ton in 2024, raising input cost exposure. Regional bottlenecks and fuel spikes (diesel volatility) amplify supplier pricing power; multi‑sourcing and captive fleets mitigate but do not eliminate disruptions across Ecuador, Peru, Argentina, Mexico and the U.S. Southwest.

Water access and regulatory permissions

Water is a critical input for Arca Continental, treated as an effective supplier due to local permits and community expectations; scarcity or regulatory shifts can tighten access and raise costs, forcing operational adjustments and capital spending on treatment and reuse.

- Supplier role: water access tied to permits and social license

- Risk drivers: basin stress and drought variability

- Mitigation: compliance, investments in reuse and community engagement

Licensor leverage and volatile inputs raise supplier power and pass‑through risk

Arca Continental’s dependence on Coca‑Cola concentrate and long‑term bottling terms gives the licensor strong pricing and quality leverage. Key inputs were volatile in 2024 (raw sugar ~0.20 USD/lb, PET resin ~1,100 USD/ton, aluminum ~2,300 USD/ton), raising pass‑through risk. Water permits, OEM lock‑in and logistics constraints further elevate supplier power despite scale and hedging.

| Metric | 2024 value |

|---|---|

| Coca‑Cola dependence | High |

| Raw sugar | ~0.20 USD/lb |

| PET resin | ~1,100 USD/ton |

| Aluminum | ~2,300 USD/ton |

| EU ETS | ~€88/ton |

What is included in the product

Tailored Porter's Five Forces analysis for Arca Continental identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory impacts. Highlights key drivers of pricing, margins, and market entry barriers, plus emerging disruptive threats to its beverage and bottling operations.

A concise, one-sheet Porter's Five Forces analysis for Arca Continental that pinpoints key competitive pressures, suggests strategic responses, and is ready to drop into decks for fast decision-making.

Customers Bargaining Power

Modern trade consolidation

Large retailers and convenience chains such as Walmart de México (≈2,700 stores) and OXXO (over 21,000 outlets) exert strong bargaining power, negotiating hard on price, terms and promotions and leveraging shelf space and sales data. Arca Continental offsets this with a broad brand portfolio and extensive cold‑equipment placements to secure visibility and impulse purchases. Concentrated buyers still extract concessions through rebates and co‑funded marketing.

Fragmented traditional trade

Numerous small shops and horeca accounts dilute individual bargaining power despite collectively representing a large channel for Arca Continental; the company reports serving roughly 1.2 million points of sale across its territories in 2024. These outlets are price sensitive and require frequent deliveries, raising distribution and service costs by an estimated 10–12% of logistics spend. Arca’s direct-store-delivery model — covering about 70% of on-premise outlets — strengthens its control through guaranteed cold availability and credit terms, while targeted loyalty programs drive repeat purchases and account for an estimated 25% of incremental channel sales.

End-consumer health sensitivity

Consumers readily switch across beverage categories driven by price, sugar content and perceived wellness, making demand elastic; over 50 jurisdictions had sugar-sweetened beverage taxes by 2024. Sugar taxes amplify elasticity—Mexico’s 1 peso/liter (~10%) levy produced 6–12% declines in purchases. Arca must tailor pack sizes, reformulations and zero-sugar SKUs while using promotions and affordability packs to mitigate churn.

Private label and local brands

Retailers push private‑label water and juices to pressure pricing, while regional local brands compete on taste and cost; Arca Continental’s Coca‑Cola trademark and extensive distribution mitigate but do not remove these alternatives.

- Retailer leverage: private‑label pressure

- Local brands: regional taste advantage

- Arca: strong brand + wide reach

- Category mix: water more exposed than Coca‑Cola

Contract terms and exclusivity

Contracted cold-equipment placements and exclusivity deals materially reduce outlet switching by locking shelf and cooler space, though buyers continue to push on placement fees and planogram terms; compliance monitoring raises operating costs but helps preserve pricing integrity. Enforcement varies across national legal frameworks, affecting the practical strength of exclusivity.

- Exclusivity: lowers outlet churn

- Negotiation: placements and planograms remain contested

- Monitoring: compliance adds cost but protects margins

- Legal: enforceability differs by country

Retailer power; distributor: ≈1.2M POS, DSD ≈70%, logistics +10–12%, tax −6–12%

Large retailers (Walmart de México ≈2,700 stores) and OXXO (≈21,000 outlets) exert strong price and placement leverage; Arca mitigates with Coca‑Cola brands, cold‑equipment exclusivity and rebates. Arca serves ≈1.2M points of sale, uses DSD for ≈70% of on‑premise outlets, and faces logistics uplift (~10–12%). Sugar taxes (~10%) raise elasticity (6–12% purchase drops), prompting reformulations and affordability packs.

| Metric | Value |

|---|---|

| Retailer footprint | Walmart ≈2,700; OXXO ≈21,000 |

| Points of sale | ≈1.2M |

| DSD coverage | ≈70% |

| Logistics impact | 10–12% |

| Sugar tax effect | ≈10% tax → 6–12% drop |

Full Version Awaits

Arca Continental Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Arca Continental you’ll receive. It’s the full, professionally formatted document—no placeholders or samples. Purchase grants instant access to this identical file, ready for download and use.

From Overview to Strategy Blueprint

Arca Continental faces moderate buyer power and intense rivalry across beverages and packaging, with supplier leverage and capital intensity raising entry barriers while regional substitutes create niche risks. Strategic scale and distribution are key defenses, yet margin pressure persists. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arca Continental’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrate dependence on The Coca‑Cola Company

Arca Continental relies on Coca‑Cola Company concentrate under long‑term bottling agreements, giving the licensor notable leverage over pricing and quality standards. Formula or concentrate price adjustments are contractually passed through and directly affect Arca Continental margins. Performance clauses and marketing fund requirements further reinforce supplier power. Diversification into snacks and non‑cola beverages only partially offsets this dependence.

Commodity inputs: sugar, PET resin, aluminum

Key inputs—sugar, PET resin and aluminum—trade globally and remained volatile in 2024 (ICE raw sugar ~0.20 USD/lb, PET resin ~1,100 USD/ton, LME aluminum ~2,300 USD/ton), enabling upstream suppliers to pass through spikes. Limited substitution (PET vs glass/can) is constrained by packaging lines and consumer preferences. Hedging reduces short-term swings but cannot remove structural cost pressure. Local LatAm sugar policies and tariffs can amplify supplier leverage.

Packaging and equipment OEM concentration

Bottling lines, coolers and closures are sourced from a concentrated set of OEMs, creating switching costs and lock‑in as Coca‑Cola technical standards narrow vendor options; spare parts scarcity and strict maintenance schedules further strengthen OEM bargaining power, although Arca Continental’s regional scale (operations across six countries) allows it to secure volume discounts and better payment terms in 2024.

Logistics, CO2, and water treatment inputs

Logistics, industrial gases and water‑treatment chemicals are critical, time‑sensitive inputs; maritime shipping accounts for roughly 2.9% of global CO2 emissions and EU ETS carbon averaged about €88/ton in 2024, raising input cost exposure. Regional bottlenecks and fuel spikes (diesel volatility) amplify supplier pricing power; multi‑sourcing and captive fleets mitigate but do not eliminate disruptions across Ecuador, Peru, Argentina, Mexico and the U.S. Southwest.

Water access and regulatory permissions

Water is a critical input for Arca Continental, treated as an effective supplier due to local permits and community expectations; scarcity or regulatory shifts can tighten access and raise costs, forcing operational adjustments and capital spending on treatment and reuse.

- Supplier role: water access tied to permits and social license

- Risk drivers: basin stress and drought variability

- Mitigation: compliance, investments in reuse and community engagement

Licensor leverage and volatile inputs raise supplier power and pass‑through risk

Arca Continental’s dependence on Coca‑Cola concentrate and long‑term bottling terms gives the licensor strong pricing and quality leverage. Key inputs were volatile in 2024 (raw sugar ~0.20 USD/lb, PET resin ~1,100 USD/ton, aluminum ~2,300 USD/ton), raising pass‑through risk. Water permits, OEM lock‑in and logistics constraints further elevate supplier power despite scale and hedging.

| Metric | 2024 value |

|---|---|

| Coca‑Cola dependence | High |

| Raw sugar | ~0.20 USD/lb |

| PET resin | ~1,100 USD/ton |

| Aluminum | ~2,300 USD/ton |

| EU ETS | ~€88/ton |

What is included in the product

Tailored Porter's Five Forces analysis for Arca Continental identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory impacts. Highlights key drivers of pricing, margins, and market entry barriers, plus emerging disruptive threats to its beverage and bottling operations.

A concise, one-sheet Porter's Five Forces analysis for Arca Continental that pinpoints key competitive pressures, suggests strategic responses, and is ready to drop into decks for fast decision-making.

Customers Bargaining Power

Modern trade consolidation

Large retailers and convenience chains such as Walmart de México (≈2,700 stores) and OXXO (over 21,000 outlets) exert strong bargaining power, negotiating hard on price, terms and promotions and leveraging shelf space and sales data. Arca Continental offsets this with a broad brand portfolio and extensive cold‑equipment placements to secure visibility and impulse purchases. Concentrated buyers still extract concessions through rebates and co‑funded marketing.

Fragmented traditional trade

Numerous small shops and horeca accounts dilute individual bargaining power despite collectively representing a large channel for Arca Continental; the company reports serving roughly 1.2 million points of sale across its territories in 2024. These outlets are price sensitive and require frequent deliveries, raising distribution and service costs by an estimated 10–12% of logistics spend. Arca’s direct-store-delivery model — covering about 70% of on-premise outlets — strengthens its control through guaranteed cold availability and credit terms, while targeted loyalty programs drive repeat purchases and account for an estimated 25% of incremental channel sales.

End-consumer health sensitivity

Consumers readily switch across beverage categories driven by price, sugar content and perceived wellness, making demand elastic; over 50 jurisdictions had sugar-sweetened beverage taxes by 2024. Sugar taxes amplify elasticity—Mexico’s 1 peso/liter (~10%) levy produced 6–12% declines in purchases. Arca must tailor pack sizes, reformulations and zero-sugar SKUs while using promotions and affordability packs to mitigate churn.

Private label and local brands

Retailers push private‑label water and juices to pressure pricing, while regional local brands compete on taste and cost; Arca Continental’s Coca‑Cola trademark and extensive distribution mitigate but do not remove these alternatives.

- Retailer leverage: private‑label pressure

- Local brands: regional taste advantage

- Arca: strong brand + wide reach

- Category mix: water more exposed than Coca‑Cola

Contract terms and exclusivity

Contracted cold-equipment placements and exclusivity deals materially reduce outlet switching by locking shelf and cooler space, though buyers continue to push on placement fees and planogram terms; compliance monitoring raises operating costs but helps preserve pricing integrity. Enforcement varies across national legal frameworks, affecting the practical strength of exclusivity.

- Exclusivity: lowers outlet churn

- Negotiation: placements and planograms remain contested

- Monitoring: compliance adds cost but protects margins

- Legal: enforceability differs by country

Retailer power; distributor: ≈1.2M POS, DSD ≈70%, logistics +10–12%, tax −6–12%

Large retailers (Walmart de México ≈2,700 stores) and OXXO (≈21,000 outlets) exert strong price and placement leverage; Arca mitigates with Coca‑Cola brands, cold‑equipment exclusivity and rebates. Arca serves ≈1.2M points of sale, uses DSD for ≈70% of on‑premise outlets, and faces logistics uplift (~10–12%). Sugar taxes (~10%) raise elasticity (6–12% purchase drops), prompting reformulations and affordability packs.

| Metric | Value |

|---|---|

| Retailer footprint | Walmart ≈2,700; OXXO ≈21,000 |

| Points of sale | ≈1.2M |

| DSD coverage | ≈70% |

| Logistics impact | 10–12% |

| Sugar tax effect | ≈10% tax → 6–12% drop |

Full Version Awaits

Arca Continental Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Arca Continental you’ll receive. It’s the full, professionally formatted document—no placeholders or samples. Purchase grants instant access to this identical file, ready for download and use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Arca Continental faces moderate buyer power and intense rivalry across beverages and packaging, with supplier leverage and capital intensity raising entry barriers while regional substitutes create niche risks. Strategic scale and distribution are key defenses, yet margin pressure persists. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arca Continental’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrate dependence on The Coca‑Cola Company

Arca Continental relies on Coca‑Cola Company concentrate under long‑term bottling agreements, giving the licensor notable leverage over pricing and quality standards. Formula or concentrate price adjustments are contractually passed through and directly affect Arca Continental margins. Performance clauses and marketing fund requirements further reinforce supplier power. Diversification into snacks and non‑cola beverages only partially offsets this dependence.

Commodity inputs: sugar, PET resin, aluminum

Key inputs—sugar, PET resin and aluminum—trade globally and remained volatile in 2024 (ICE raw sugar ~0.20 USD/lb, PET resin ~1,100 USD/ton, LME aluminum ~2,300 USD/ton), enabling upstream suppliers to pass through spikes. Limited substitution (PET vs glass/can) is constrained by packaging lines and consumer preferences. Hedging reduces short-term swings but cannot remove structural cost pressure. Local LatAm sugar policies and tariffs can amplify supplier leverage.

Packaging and equipment OEM concentration

Bottling lines, coolers and closures are sourced from a concentrated set of OEMs, creating switching costs and lock‑in as Coca‑Cola technical standards narrow vendor options; spare parts scarcity and strict maintenance schedules further strengthen OEM bargaining power, although Arca Continental’s regional scale (operations across six countries) allows it to secure volume discounts and better payment terms in 2024.

Logistics, CO2, and water treatment inputs

Logistics, industrial gases and water‑treatment chemicals are critical, time‑sensitive inputs; maritime shipping accounts for roughly 2.9% of global CO2 emissions and EU ETS carbon averaged about €88/ton in 2024, raising input cost exposure. Regional bottlenecks and fuel spikes (diesel volatility) amplify supplier pricing power; multi‑sourcing and captive fleets mitigate but do not eliminate disruptions across Ecuador, Peru, Argentina, Mexico and the U.S. Southwest.

Water access and regulatory permissions

Water is a critical input for Arca Continental, treated as an effective supplier due to local permits and community expectations; scarcity or regulatory shifts can tighten access and raise costs, forcing operational adjustments and capital spending on treatment and reuse.

- Supplier role: water access tied to permits and social license

- Risk drivers: basin stress and drought variability

- Mitigation: compliance, investments in reuse and community engagement

Licensor leverage and volatile inputs raise supplier power and pass‑through risk

Arca Continental’s dependence on Coca‑Cola concentrate and long‑term bottling terms gives the licensor strong pricing and quality leverage. Key inputs were volatile in 2024 (raw sugar ~0.20 USD/lb, PET resin ~1,100 USD/ton, aluminum ~2,300 USD/ton), raising pass‑through risk. Water permits, OEM lock‑in and logistics constraints further elevate supplier power despite scale and hedging.

| Metric | 2024 value |

|---|---|

| Coca‑Cola dependence | High |

| Raw sugar | ~0.20 USD/lb |

| PET resin | ~1,100 USD/ton |

| Aluminum | ~2,300 USD/ton |

| EU ETS | ~€88/ton |

What is included in the product

Tailored Porter's Five Forces analysis for Arca Continental identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory impacts. Highlights key drivers of pricing, margins, and market entry barriers, plus emerging disruptive threats to its beverage and bottling operations.

A concise, one-sheet Porter's Five Forces analysis for Arca Continental that pinpoints key competitive pressures, suggests strategic responses, and is ready to drop into decks for fast decision-making.

Customers Bargaining Power

Modern trade consolidation

Large retailers and convenience chains such as Walmart de México (≈2,700 stores) and OXXO (over 21,000 outlets) exert strong bargaining power, negotiating hard on price, terms and promotions and leveraging shelf space and sales data. Arca Continental offsets this with a broad brand portfolio and extensive cold‑equipment placements to secure visibility and impulse purchases. Concentrated buyers still extract concessions through rebates and co‑funded marketing.

Fragmented traditional trade

Numerous small shops and horeca accounts dilute individual bargaining power despite collectively representing a large channel for Arca Continental; the company reports serving roughly 1.2 million points of sale across its territories in 2024. These outlets are price sensitive and require frequent deliveries, raising distribution and service costs by an estimated 10–12% of logistics spend. Arca’s direct-store-delivery model — covering about 70% of on-premise outlets — strengthens its control through guaranteed cold availability and credit terms, while targeted loyalty programs drive repeat purchases and account for an estimated 25% of incremental channel sales.

End-consumer health sensitivity

Consumers readily switch across beverage categories driven by price, sugar content and perceived wellness, making demand elastic; over 50 jurisdictions had sugar-sweetened beverage taxes by 2024. Sugar taxes amplify elasticity—Mexico’s 1 peso/liter (~10%) levy produced 6–12% declines in purchases. Arca must tailor pack sizes, reformulations and zero-sugar SKUs while using promotions and affordability packs to mitigate churn.

Private label and local brands

Retailers push private‑label water and juices to pressure pricing, while regional local brands compete on taste and cost; Arca Continental’s Coca‑Cola trademark and extensive distribution mitigate but do not remove these alternatives.

- Retailer leverage: private‑label pressure

- Local brands: regional taste advantage

- Arca: strong brand + wide reach

- Category mix: water more exposed than Coca‑Cola

Contract terms and exclusivity

Contracted cold-equipment placements and exclusivity deals materially reduce outlet switching by locking shelf and cooler space, though buyers continue to push on placement fees and planogram terms; compliance monitoring raises operating costs but helps preserve pricing integrity. Enforcement varies across national legal frameworks, affecting the practical strength of exclusivity.

- Exclusivity: lowers outlet churn

- Negotiation: placements and planograms remain contested

- Monitoring: compliance adds cost but protects margins

- Legal: enforceability differs by country

Retailer power; distributor: ≈1.2M POS, DSD ≈70%, logistics +10–12%, tax −6–12%

Large retailers (Walmart de México ≈2,700 stores) and OXXO (≈21,000 outlets) exert strong price and placement leverage; Arca mitigates with Coca‑Cola brands, cold‑equipment exclusivity and rebates. Arca serves ≈1.2M points of sale, uses DSD for ≈70% of on‑premise outlets, and faces logistics uplift (~10–12%). Sugar taxes (~10%) raise elasticity (6–12% purchase drops), prompting reformulations and affordability packs.

| Metric | Value |

|---|---|

| Retailer footprint | Walmart ≈2,700; OXXO ≈21,000 |

| Points of sale | ≈1.2M |

| DSD coverage | ≈70% |

| Logistics impact | 10–12% |

| Sugar tax effect | ≈10% tax → 6–12% drop |

Full Version Awaits

Arca Continental Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Arca Continental you’ll receive. It’s the full, professionally formatted document—no placeholders or samples. Purchase grants instant access to this identical file, ready for download and use.