Arcadis Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

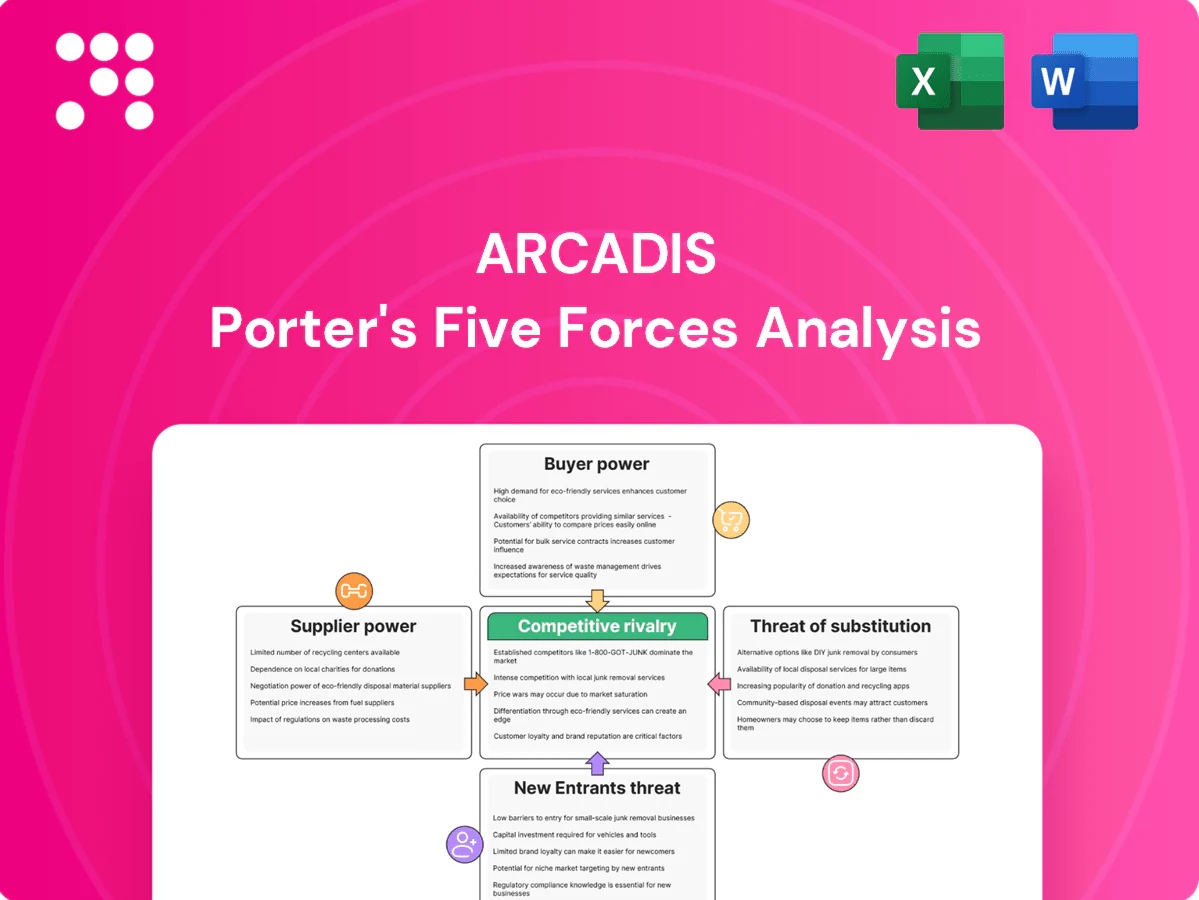

Arcadis’s Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory pressures shaping its performance. This brief overview teases force-by-force implications for strategy and investment decisions. Unlock the full Porter’s Five Forces Analysis to access detailed ratings, visuals, and actionable insights tailored to Arcadis.

Suppliers Bargaining Power

Specialized talent scarcity

Arcadis depends on highly qualified engineers, planners and environmental scientists and employed about 27,000 professionals in 2024, making talent scarcity a key supplier power driver. Tight supply in many markets has driven salary inflation (around 6% in professional services in 2024) and higher retention costs, increasing labor bargaining power. Niche accreditations and local licensing limit substitutes, while graduate pipelines and global mobility partially mitigate these pressures.

Proprietary software and data

Core tools like BIM, GIS and digital-twin platforms create switching costs and training burdens; the global BIM market was about $8 billion in 2024, underscoring vendor influence. Vendors can raise license fees or change terms, squeezing project margins and timelines. Interoperability limits lock workflows into ecosystems, while negotiating enterprise licenses and adopting open standards such as IFC (buildingSMART) mitigates dependency.

Specialist subcontractors

Environmental labs, geotech drillers, surveyors and permitting experts remained capacity-constrained, with industry surveys reporting ~60% of projects affected by specialist supplier constraints in 2024, which boosts their rate-setting and scheduling power on tight programs. Their local knowledge and certified quality lower substitutability and increase switching costs. Arcadis and peers mitigate exposure via preferred-supplier agreements and multi-vendor panels to spread risk.

Materials and field services volatility

Though Arcadis is advisory-led, programs requiring procurement oversight and field services face materials volatility; supply shocks for testing kits and sensors have in past cycles extended lead times by 20–30%, raising delivery risk for project schedules and margins.

Vendors often prioritize large-volume buyers, tightening availability; Arcadis reported c.28,000 staff and ~€3.0bn revenue in 2023, so forward planning and inventory buffers are used to stabilize supply and protect delivery.

- Supply shocks: testing kits/sensors → lead times +20–30%

- Vendor priority: favors high-volume buyers → tighter access

- Mitigation: forward planning, inventory buffers, procurement oversight

- Scale: Arcadis ~28,000 staff, ~€3.0bn revenue (2023)

Regulatory and certification gatekeepers

Regulatory and certification bodies function as suppliers to Arcadis by controlling access to permits, accredited methodologies and official data, so approval requirements can directly constrain project timelines and scope. Rule changes or permitting delays increase their bargaining power, raising compliance costs and schedule risk. Early engagement and demonstrated compliance expertise reduce Arcadis exposure and negotiation friction.

- Access: permits and accredited methods controlled by approved bodies

- Leverage: delays or rule changes raise supplier power

- Mitigation: early engagement and compliance expertise lower risk

Scarce talent (27,000) and 6% salary inflation amplify supplier power

Arcadis faces strong supplier power from scarce talent (27,000 professionals in 2024) and 6% salary inflation in professional services (2024), plus specialist vendors affecting ~60% of projects. Digital tool vendors (global BIM market ~$8bn in 2024) and supply shocks (testing kits/sensors lead times +20–30%) raise costs and scheduling risk. Mitigations: panels, enterprise licenses, early regulatory engagement.

| Metric | 2023/2024 |

|---|---|

| Staff | 27,000 (2024) |

| Revenue | ~€3.0bn (2023) |

| Salary inflation | ~6% (2024) |

| BIM market | ~$8bn (2024) |

| Projects affected | ~60% (2024) |

| Lead-time shocks | +20–30% |

What is included in the product

Profiles Arcadis’s competitive landscape using Porter’s Five Forces to reveal rivalry intensity, supplier and buyer power, entry barriers, and substitute threats, highlighting disruptive trends and strategic levers to protect market position.

A clear, one-sheet Porter's Five Forces for Arcadis—visual spider chart with customizable pressure levels, no macros, and a clean layout ready to drop into pitch decks, dashboards or reports to instantly relieve strategic analysis bottlenecks.

Customers Bargaining Power

Public sector RFP dominance

Public sector RFP dominance forces competitive tenders that standardize scope and compress fees; public procurement represents roughly 10–15% of GDP globally and about 14% in the EU (European Commission). Transparent scoring and framework agreements increase substitutability and allow buyers to enforce capped rates across multi-year programs, so differentiation must shift from hourly rates to demonstrable value and outcomes.

Large private developers’ leverage

Large private developers bundle repeat projects to extract volume discounts (commonly 5–10%) and impose stringent SLAs, forcing suppliers into tighter margins. They routinely multi-source — keeping bid mark-ups low and compressing contractor gross margins to single digits. Performance clauses and liquidated damages (often 0.1–0.3% of contract value per day) shift failure risk onto suppliers. Deep relationships and integrated offerings, however, permit premium pricing and longer-term frameworks.

Professionalized procurement

Buyers at Arcadis increasingly use data-driven vendor scorecards, e-auctions and rate benchmarking, with e-auctions commonly delivering 5–15% realized savings by 2024, raising price sensitivity and reducing information asymmetry.

Switching ease among top peers

With 250 companies on ENRs Top 250 Global Contractors (2024), clients can rotate providers with limited onboarding cost; standardized deliverables and interoperable formats like IFC and COBie lower technical barriers. Past performance and reputation help but rarely fully lock in clients. Embedding digital twins and O&M insights increases operational stickiness and lifetime revenue capture.

- ENR Top 250 (2024): 250 peers

- Interoperable formats: IFC, COBie

- Switching cost: low due to standardization

- Stickiness lever: digital twins/O&M data

Outcome-based contracting

Clients increasingly tie fees to sustainability, schedule and permitting milestones, shifting execution risk to consultants and compressing margins; KPIs give buyers control of withhold/bonus structures, raising the need for robust risk management and crystal-clear scope to protect profitability.

- Outcome-based contracts raise client leverage

- KPIs enable buyer-controlled withholds/bonuses

- Robust risk allocation and scope clarity essential

Procurement leverage compresses margins: e-auctions 5-15% savings; high substitutability

Public procurement (~14% of EU GDP) and standardized RFPs boost buyer leverage; e-auctions yielded 5–15% savings by 2024, raising price sensitivity. Large developers extract 5–10% volume discounts and enforce SLAs/liquidated damages, compressing margins. Low switching costs (250 ENR peers, interoperable IFC/COBie) increase substitutability, while digital twins/O&M data create limited stickiness.

| Metric | Value (2024) |

|---|---|

| EU public procurement | ~14% GDP |

| E-auction savings | 5–15% |

| ENR Top 250 peers | 250 |

Full Version Awaits

Arcadis Porter's Five Forces Analysis

This preview shows the exact Arcadis Porter's Five Forces Analysis you’ll receive after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file for your strategic review and decision-making.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Arcadis’s Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory pressures shaping its performance. This brief overview teases force-by-force implications for strategy and investment decisions. Unlock the full Porter’s Five Forces Analysis to access detailed ratings, visuals, and actionable insights tailored to Arcadis.

Suppliers Bargaining Power

Specialized talent scarcity

Arcadis depends on highly qualified engineers, planners and environmental scientists and employed about 27,000 professionals in 2024, making talent scarcity a key supplier power driver. Tight supply in many markets has driven salary inflation (around 6% in professional services in 2024) and higher retention costs, increasing labor bargaining power. Niche accreditations and local licensing limit substitutes, while graduate pipelines and global mobility partially mitigate these pressures.

Proprietary software and data

Core tools like BIM, GIS and digital-twin platforms create switching costs and training burdens; the global BIM market was about $8 billion in 2024, underscoring vendor influence. Vendors can raise license fees or change terms, squeezing project margins and timelines. Interoperability limits lock workflows into ecosystems, while negotiating enterprise licenses and adopting open standards such as IFC (buildingSMART) mitigates dependency.

Specialist subcontractors

Environmental labs, geotech drillers, surveyors and permitting experts remained capacity-constrained, with industry surveys reporting ~60% of projects affected by specialist supplier constraints in 2024, which boosts their rate-setting and scheduling power on tight programs. Their local knowledge and certified quality lower substitutability and increase switching costs. Arcadis and peers mitigate exposure via preferred-supplier agreements and multi-vendor panels to spread risk.

Materials and field services volatility

Though Arcadis is advisory-led, programs requiring procurement oversight and field services face materials volatility; supply shocks for testing kits and sensors have in past cycles extended lead times by 20–30%, raising delivery risk for project schedules and margins.

Vendors often prioritize large-volume buyers, tightening availability; Arcadis reported c.28,000 staff and ~€3.0bn revenue in 2023, so forward planning and inventory buffers are used to stabilize supply and protect delivery.

- Supply shocks: testing kits/sensors → lead times +20–30%

- Vendor priority: favors high-volume buyers → tighter access

- Mitigation: forward planning, inventory buffers, procurement oversight

- Scale: Arcadis ~28,000 staff, ~€3.0bn revenue (2023)

Regulatory and certification gatekeepers

Regulatory and certification bodies function as suppliers to Arcadis by controlling access to permits, accredited methodologies and official data, so approval requirements can directly constrain project timelines and scope. Rule changes or permitting delays increase their bargaining power, raising compliance costs and schedule risk. Early engagement and demonstrated compliance expertise reduce Arcadis exposure and negotiation friction.

- Access: permits and accredited methods controlled by approved bodies

- Leverage: delays or rule changes raise supplier power

- Mitigation: early engagement and compliance expertise lower risk

Scarce talent (27,000) and 6% salary inflation amplify supplier power

Arcadis faces strong supplier power from scarce talent (27,000 professionals in 2024) and 6% salary inflation in professional services (2024), plus specialist vendors affecting ~60% of projects. Digital tool vendors (global BIM market ~$8bn in 2024) and supply shocks (testing kits/sensors lead times +20–30%) raise costs and scheduling risk. Mitigations: panels, enterprise licenses, early regulatory engagement.

| Metric | 2023/2024 |

|---|---|

| Staff | 27,000 (2024) |

| Revenue | ~€3.0bn (2023) |

| Salary inflation | ~6% (2024) |

| BIM market | ~$8bn (2024) |

| Projects affected | ~60% (2024) |

| Lead-time shocks | +20–30% |

What is included in the product

Profiles Arcadis’s competitive landscape using Porter’s Five Forces to reveal rivalry intensity, supplier and buyer power, entry barriers, and substitute threats, highlighting disruptive trends and strategic levers to protect market position.

A clear, one-sheet Porter's Five Forces for Arcadis—visual spider chart with customizable pressure levels, no macros, and a clean layout ready to drop into pitch decks, dashboards or reports to instantly relieve strategic analysis bottlenecks.

Customers Bargaining Power

Public sector RFP dominance

Public sector RFP dominance forces competitive tenders that standardize scope and compress fees; public procurement represents roughly 10–15% of GDP globally and about 14% in the EU (European Commission). Transparent scoring and framework agreements increase substitutability and allow buyers to enforce capped rates across multi-year programs, so differentiation must shift from hourly rates to demonstrable value and outcomes.

Large private developers’ leverage

Large private developers bundle repeat projects to extract volume discounts (commonly 5–10%) and impose stringent SLAs, forcing suppliers into tighter margins. They routinely multi-source — keeping bid mark-ups low and compressing contractor gross margins to single digits. Performance clauses and liquidated damages (often 0.1–0.3% of contract value per day) shift failure risk onto suppliers. Deep relationships and integrated offerings, however, permit premium pricing and longer-term frameworks.

Professionalized procurement

Buyers at Arcadis increasingly use data-driven vendor scorecards, e-auctions and rate benchmarking, with e-auctions commonly delivering 5–15% realized savings by 2024, raising price sensitivity and reducing information asymmetry.

Switching ease among top peers

With 250 companies on ENRs Top 250 Global Contractors (2024), clients can rotate providers with limited onboarding cost; standardized deliverables and interoperable formats like IFC and COBie lower technical barriers. Past performance and reputation help but rarely fully lock in clients. Embedding digital twins and O&M insights increases operational stickiness and lifetime revenue capture.

- ENR Top 250 (2024): 250 peers

- Interoperable formats: IFC, COBie

- Switching cost: low due to standardization

- Stickiness lever: digital twins/O&M data

Outcome-based contracting

Clients increasingly tie fees to sustainability, schedule and permitting milestones, shifting execution risk to consultants and compressing margins; KPIs give buyers control of withhold/bonus structures, raising the need for robust risk management and crystal-clear scope to protect profitability.

- Outcome-based contracts raise client leverage

- KPIs enable buyer-controlled withholds/bonuses

- Robust risk allocation and scope clarity essential

Procurement leverage compresses margins: e-auctions 5-15% savings; high substitutability

Public procurement (~14% of EU GDP) and standardized RFPs boost buyer leverage; e-auctions yielded 5–15% savings by 2024, raising price sensitivity. Large developers extract 5–10% volume discounts and enforce SLAs/liquidated damages, compressing margins. Low switching costs (250 ENR peers, interoperable IFC/COBie) increase substitutability, while digital twins/O&M data create limited stickiness.

| Metric | Value (2024) |

|---|---|

| EU public procurement | ~14% GDP |

| E-auction savings | 5–15% |

| ENR Top 250 peers | 250 |

Full Version Awaits

Arcadis Porter's Five Forces Analysis

This preview shows the exact Arcadis Porter's Five Forces Analysis you’ll receive after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file for your strategic review and decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Arcadis’s Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory pressures shaping its performance. This brief overview teases force-by-force implications for strategy and investment decisions. Unlock the full Porter’s Five Forces Analysis to access detailed ratings, visuals, and actionable insights tailored to Arcadis.

Suppliers Bargaining Power

Specialized talent scarcity

Arcadis depends on highly qualified engineers, planners and environmental scientists and employed about 27,000 professionals in 2024, making talent scarcity a key supplier power driver. Tight supply in many markets has driven salary inflation (around 6% in professional services in 2024) and higher retention costs, increasing labor bargaining power. Niche accreditations and local licensing limit substitutes, while graduate pipelines and global mobility partially mitigate these pressures.

Proprietary software and data

Core tools like BIM, GIS and digital-twin platforms create switching costs and training burdens; the global BIM market was about $8 billion in 2024, underscoring vendor influence. Vendors can raise license fees or change terms, squeezing project margins and timelines. Interoperability limits lock workflows into ecosystems, while negotiating enterprise licenses and adopting open standards such as IFC (buildingSMART) mitigates dependency.

Specialist subcontractors

Environmental labs, geotech drillers, surveyors and permitting experts remained capacity-constrained, with industry surveys reporting ~60% of projects affected by specialist supplier constraints in 2024, which boosts their rate-setting and scheduling power on tight programs. Their local knowledge and certified quality lower substitutability and increase switching costs. Arcadis and peers mitigate exposure via preferred-supplier agreements and multi-vendor panels to spread risk.

Materials and field services volatility

Though Arcadis is advisory-led, programs requiring procurement oversight and field services face materials volatility; supply shocks for testing kits and sensors have in past cycles extended lead times by 20–30%, raising delivery risk for project schedules and margins.

Vendors often prioritize large-volume buyers, tightening availability; Arcadis reported c.28,000 staff and ~€3.0bn revenue in 2023, so forward planning and inventory buffers are used to stabilize supply and protect delivery.

- Supply shocks: testing kits/sensors → lead times +20–30%

- Vendor priority: favors high-volume buyers → tighter access

- Mitigation: forward planning, inventory buffers, procurement oversight

- Scale: Arcadis ~28,000 staff, ~€3.0bn revenue (2023)

Regulatory and certification gatekeepers

Regulatory and certification bodies function as suppliers to Arcadis by controlling access to permits, accredited methodologies and official data, so approval requirements can directly constrain project timelines and scope. Rule changes or permitting delays increase their bargaining power, raising compliance costs and schedule risk. Early engagement and demonstrated compliance expertise reduce Arcadis exposure and negotiation friction.

- Access: permits and accredited methods controlled by approved bodies

- Leverage: delays or rule changes raise supplier power

- Mitigation: early engagement and compliance expertise lower risk

Scarce talent (27,000) and 6% salary inflation amplify supplier power

Arcadis faces strong supplier power from scarce talent (27,000 professionals in 2024) and 6% salary inflation in professional services (2024), plus specialist vendors affecting ~60% of projects. Digital tool vendors (global BIM market ~$8bn in 2024) and supply shocks (testing kits/sensors lead times +20–30%) raise costs and scheduling risk. Mitigations: panels, enterprise licenses, early regulatory engagement.

| Metric | 2023/2024 |

|---|---|

| Staff | 27,000 (2024) |

| Revenue | ~€3.0bn (2023) |

| Salary inflation | ~6% (2024) |

| BIM market | ~$8bn (2024) |

| Projects affected | ~60% (2024) |

| Lead-time shocks | +20–30% |

What is included in the product

Profiles Arcadis’s competitive landscape using Porter’s Five Forces to reveal rivalry intensity, supplier and buyer power, entry barriers, and substitute threats, highlighting disruptive trends and strategic levers to protect market position.

A clear, one-sheet Porter's Five Forces for Arcadis—visual spider chart with customizable pressure levels, no macros, and a clean layout ready to drop into pitch decks, dashboards or reports to instantly relieve strategic analysis bottlenecks.

Customers Bargaining Power

Public sector RFP dominance

Public sector RFP dominance forces competitive tenders that standardize scope and compress fees; public procurement represents roughly 10–15% of GDP globally and about 14% in the EU (European Commission). Transparent scoring and framework agreements increase substitutability and allow buyers to enforce capped rates across multi-year programs, so differentiation must shift from hourly rates to demonstrable value and outcomes.

Large private developers’ leverage

Large private developers bundle repeat projects to extract volume discounts (commonly 5–10%) and impose stringent SLAs, forcing suppliers into tighter margins. They routinely multi-source — keeping bid mark-ups low and compressing contractor gross margins to single digits. Performance clauses and liquidated damages (often 0.1–0.3% of contract value per day) shift failure risk onto suppliers. Deep relationships and integrated offerings, however, permit premium pricing and longer-term frameworks.

Professionalized procurement

Buyers at Arcadis increasingly use data-driven vendor scorecards, e-auctions and rate benchmarking, with e-auctions commonly delivering 5–15% realized savings by 2024, raising price sensitivity and reducing information asymmetry.

Switching ease among top peers

With 250 companies on ENRs Top 250 Global Contractors (2024), clients can rotate providers with limited onboarding cost; standardized deliverables and interoperable formats like IFC and COBie lower technical barriers. Past performance and reputation help but rarely fully lock in clients. Embedding digital twins and O&M insights increases operational stickiness and lifetime revenue capture.

- ENR Top 250 (2024): 250 peers

- Interoperable formats: IFC, COBie

- Switching cost: low due to standardization

- Stickiness lever: digital twins/O&M data

Outcome-based contracting

Clients increasingly tie fees to sustainability, schedule and permitting milestones, shifting execution risk to consultants and compressing margins; KPIs give buyers control of withhold/bonus structures, raising the need for robust risk management and crystal-clear scope to protect profitability.

- Outcome-based contracts raise client leverage

- KPIs enable buyer-controlled withholds/bonuses

- Robust risk allocation and scope clarity essential

Procurement leverage compresses margins: e-auctions 5-15% savings; high substitutability

Public procurement (~14% of EU GDP) and standardized RFPs boost buyer leverage; e-auctions yielded 5–15% savings by 2024, raising price sensitivity. Large developers extract 5–10% volume discounts and enforce SLAs/liquidated damages, compressing margins. Low switching costs (250 ENR peers, interoperable IFC/COBie) increase substitutability, while digital twins/O&M data create limited stickiness.

| Metric | Value (2024) |

|---|---|

| EU public procurement | ~14% GDP |

| E-auction savings | 5–15% |

| ENR Top 250 peers | 250 |

Full Version Awaits

Arcadis Porter's Five Forces Analysis

This preview shows the exact Arcadis Porter's Five Forces Analysis you’ll receive after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file for your strategic review and decision-making.