Anonim PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE snapshot for Anonim—see how political shifts, economic trends, and tech disruption shape its outlook. Perfect for investors and planners, this preview teases deeper, actionable insights. Purchase the full analysis to access the complete, editable report instantly.

Political factors

Trade policy and tariffs

Arçelik’s footprint in about 145 countries exposes it to tariff swings, antidumping duties and divergent customs rules that can abruptly raise landed costs and compress margins. Changes in trade agreements (eg regional FTAs) shift pricing power and sourcing choices, sometimes making components subject to duties that add several percentage points to COGS. Proactive supply reconfiguration and dual-sourcing, plus close policy monitoring, are essential to protect margins.

Geopolitical risk exposure

Operations across Europe, Middle East, Africa and Asia face regional instability and logistics disruptions, exemplified by EU gas imports from Russia falling about 80% since 2022, pressuring energy-dependent supply chains. Sanctions and political tensions (over 40 jurisdictions with Russia-related measures by 2024) can constrain markets or suppliers. Scenario planning and diversified routes reduce concentration risk. Insurance and FX/commodity hedging supplement business continuity.

Home-country policy dynamics

As a Turkish multinational, Anonim is shaped by fiscal, monetary and industrial policy—Turkey's general government debt was about 39% of GDP in 2023 and macro policy drives financing costs and incentives. The 1995 EU customs union and modernization talks affect EU access while exports reached roughly USD 254 billion in 2023, supported by state export credit and incentives. Local content requirements in sectors like defense and autos steer manufacturing footprints, and public R&D spending was about 1.1% of GDP (2022), with government energy and YEKA renewables programs expanding capacity and competitiveness.

Public procurement and incentives

Public procurement and appliance-replacement subsidies in 2024–25 have shifted purchase timing and product mix, driving spikes in demand for high-efficiency models and concentrating orders around program windows; US and EU schemes reported double-digit year-on-year increases in efficient appliance sales. Tax credits (2024 IRA and EU national schemes) accelerated premium-model uptake, while incentive volatility forces manufacturers into agile production and inventory strategies. Strategic partnerships with authorities expanded market penetration through bulk procurement and voucher schemes.

- Procurement-driven demand peaks

- Tax credits -> faster premium adoption

- Volatility -> agile planning

- Authority partnerships -> wider reach

Regulatory harmonization and standards

Global appliance maker faces tariff sanctions and energy risks amid incentive-driven premium demand

Arçelik's presence in ~145 countries exposes it to tariff swings and 40+ sanctions-related measures (2024), raising landed costs. EU gas imports from Russia fell ~80% since 2022, heightening energy risk. Turkey's general government debt ~39% of GDP (2023) with exports ~$254bn (2023) shape financing and incentives. Procurement subsidies and 2024 IRA/EU credits accelerate premium appliance demand.

| Metric | Value | Implication |

|---|---|---|

| Market footprint | ~145 countries | Tariff/exposure |

| Sanctions (2024) | 40+ | Supply/market limits |

| EU gas | -80% since 2022 | Energy risk |

| Turkey debt | 39% GDP (2023) | Financing cost |

| Exports | $254bn (2023) | Export support |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Anonim across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to reflect market and regulatory dynamics; designed for executives, consultants, and entrepreneurs with forward-looking insights ready for reports and investor materials.

An Anonim PESTLE delivers a concise, visually segmented summary that can be dropped into presentations or shared across teams to simplify external risk discussions and speed decision-making. Editable notes let users tailor insights to region or business line for quick alignment in meetings.

Economic factors

Consumer demand cyclicality

Appliances are semi-durable purchases tied to housing cycles and disposable income; US housing starts were about 1.58 million in 2023, illustrating linkages that continued into 2024 as demand tracked construction and remodeling activity.

Economic downturns typically delay replacements while upcycles favor upgrades and premium features, and the global household appliance market was estimated near USD 330 billion in 2024, up modestly from 2023.

Targeted product mix, extended warranties and point-of-sale financing have been shown to stabilize volumes, and counter-seasonal categories such as small kitchen appliances help balance revenue across quarters.

FX volatility and inflation

Revenue and costs span multiple currencies—input imports and global sales—exposing Anonim to FX swings often in the 10–15% range and inflation running roughly 3–7% across key markets in 2024, pressuring margins and pricing. Hedging, local sourcing and index-linked contracts have reduced net exposure. Clear pricing architecture preserves brand equity while allowing pass-through where markets permit.

Commodity and logistics costs

Steel HRC averaged about $850/ton in 2024, copper roughly $9,000/ton and major thermoplastics near $1,200/ton, while Shanghai–LA 40ft spot freight averaged ~$1,800/FEU in 2024, driving COGS variability. Supply tightness or shocks quickly ripple through margins and inventory turns. Long-term contracts and design-to-cost practices blunt price swings. Nearshoring and larger inventory buffers have measurably improved resilience.

Interest rates and credit access

Consumer financing availability drives big-ticket demand; with US policy rates at 5.25–5.50% (mid‑2024/2025) and 30‑year mortgage averages near 6–7%, affordability and purchase timing compress. Higher rates raise working capital costs and can slow sell‑through, while flexible payment plans and BNPL keep volumes resilient during tight credit. A strong balance sheet and diversified funding reduce refinancing and interest risk for Anonim.

Emerging market growth

- Middle-class demand: 5–7% YoY sales growth in 2024

- Pricing: tiered SKUs + localized features

- Scale: distribution + service networks

- Risk: currency & policy volatility 2024–25

Global appliance maker faces tariff sanctions and energy risks amid incentive-driven premium demand

Appliance demand tracks housing starts (~1.58M US 2023), global market ~USD 330B (2024), and EM household growth ~5–7% (2024); FX swings 10–15% and input costs (steel $850/t, copper $9k/t) pressure margins; policy rates 5.25–5.50% and mortgages ~6–7% constrain affordability while financing and tiered SKUs mitigate risk.

| Metric | 2024 |

|---|---|

| US housing starts | 1.58M |

| Market size | USD 330B |

| FX volatility | 10–15% |

| Policy rate | 5.25–5.50% |

Preview Before You Purchase

Anonim PESTLE Analysis

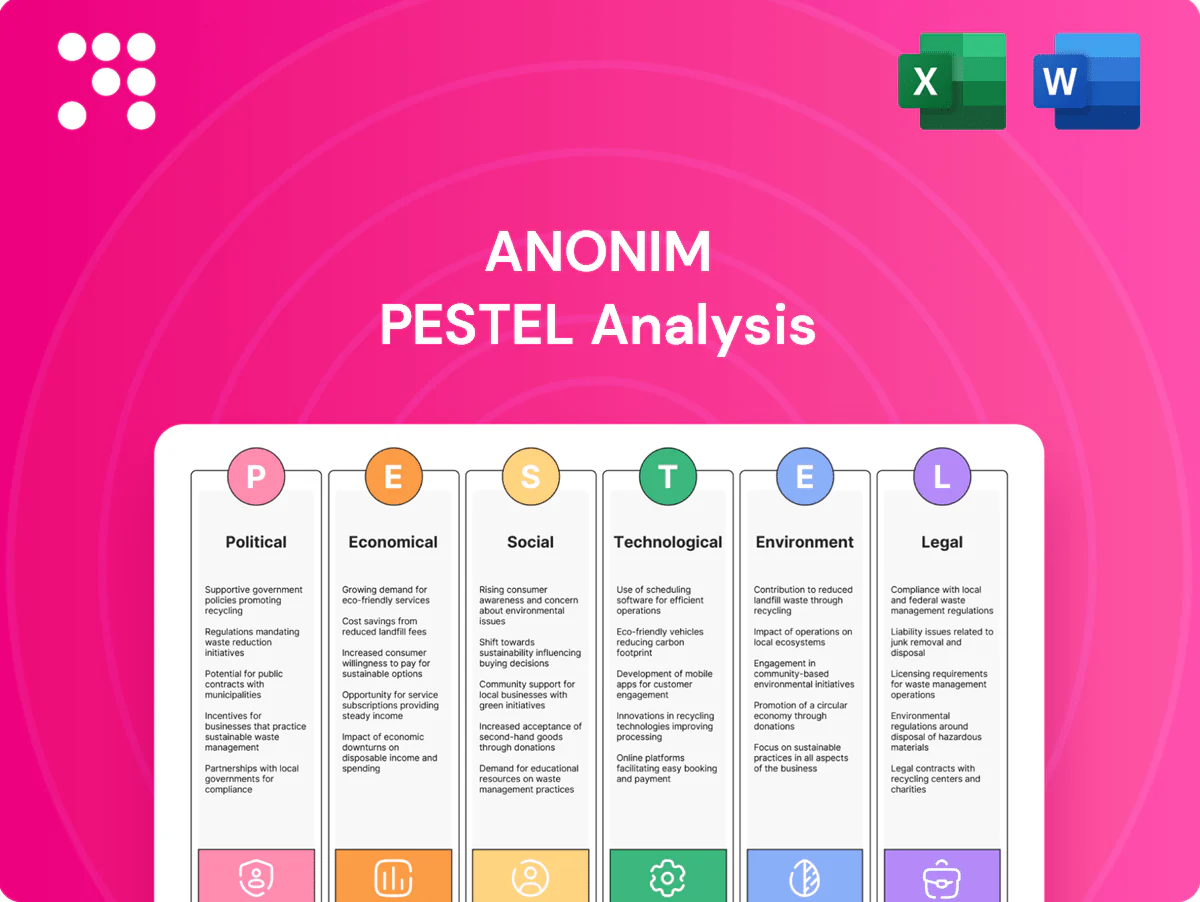

The preview shown here is the exact Anonim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown with no placeholders or surprises. After checkout you’ll instantly download this same finished document.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE snapshot for Anonim—see how political shifts, economic trends, and tech disruption shape its outlook. Perfect for investors and planners, this preview teases deeper, actionable insights. Purchase the full analysis to access the complete, editable report instantly.

Political factors

Trade policy and tariffs

Arçelik’s footprint in about 145 countries exposes it to tariff swings, antidumping duties and divergent customs rules that can abruptly raise landed costs and compress margins. Changes in trade agreements (eg regional FTAs) shift pricing power and sourcing choices, sometimes making components subject to duties that add several percentage points to COGS. Proactive supply reconfiguration and dual-sourcing, plus close policy monitoring, are essential to protect margins.

Geopolitical risk exposure

Operations across Europe, Middle East, Africa and Asia face regional instability and logistics disruptions, exemplified by EU gas imports from Russia falling about 80% since 2022, pressuring energy-dependent supply chains. Sanctions and political tensions (over 40 jurisdictions with Russia-related measures by 2024) can constrain markets or suppliers. Scenario planning and diversified routes reduce concentration risk. Insurance and FX/commodity hedging supplement business continuity.

Home-country policy dynamics

As a Turkish multinational, Anonim is shaped by fiscal, monetary and industrial policy—Turkey's general government debt was about 39% of GDP in 2023 and macro policy drives financing costs and incentives. The 1995 EU customs union and modernization talks affect EU access while exports reached roughly USD 254 billion in 2023, supported by state export credit and incentives. Local content requirements in sectors like defense and autos steer manufacturing footprints, and public R&D spending was about 1.1% of GDP (2022), with government energy and YEKA renewables programs expanding capacity and competitiveness.

Public procurement and incentives

Public procurement and appliance-replacement subsidies in 2024–25 have shifted purchase timing and product mix, driving spikes in demand for high-efficiency models and concentrating orders around program windows; US and EU schemes reported double-digit year-on-year increases in efficient appliance sales. Tax credits (2024 IRA and EU national schemes) accelerated premium-model uptake, while incentive volatility forces manufacturers into agile production and inventory strategies. Strategic partnerships with authorities expanded market penetration through bulk procurement and voucher schemes.

- Procurement-driven demand peaks

- Tax credits -> faster premium adoption

- Volatility -> agile planning

- Authority partnerships -> wider reach

Regulatory harmonization and standards

Global appliance maker faces tariff sanctions and energy risks amid incentive-driven premium demand

Arçelik's presence in ~145 countries exposes it to tariff swings and 40+ sanctions-related measures (2024), raising landed costs. EU gas imports from Russia fell ~80% since 2022, heightening energy risk. Turkey's general government debt ~39% of GDP (2023) with exports ~$254bn (2023) shape financing and incentives. Procurement subsidies and 2024 IRA/EU credits accelerate premium appliance demand.

| Metric | Value | Implication |

|---|---|---|

| Market footprint | ~145 countries | Tariff/exposure |

| Sanctions (2024) | 40+ | Supply/market limits |

| EU gas | -80% since 2022 | Energy risk |

| Turkey debt | 39% GDP (2023) | Financing cost |

| Exports | $254bn (2023) | Export support |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Anonim across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to reflect market and regulatory dynamics; designed for executives, consultants, and entrepreneurs with forward-looking insights ready for reports and investor materials.

An Anonim PESTLE delivers a concise, visually segmented summary that can be dropped into presentations or shared across teams to simplify external risk discussions and speed decision-making. Editable notes let users tailor insights to region or business line for quick alignment in meetings.

Economic factors

Consumer demand cyclicality

Appliances are semi-durable purchases tied to housing cycles and disposable income; US housing starts were about 1.58 million in 2023, illustrating linkages that continued into 2024 as demand tracked construction and remodeling activity.

Economic downturns typically delay replacements while upcycles favor upgrades and premium features, and the global household appliance market was estimated near USD 330 billion in 2024, up modestly from 2023.

Targeted product mix, extended warranties and point-of-sale financing have been shown to stabilize volumes, and counter-seasonal categories such as small kitchen appliances help balance revenue across quarters.

FX volatility and inflation

Revenue and costs span multiple currencies—input imports and global sales—exposing Anonim to FX swings often in the 10–15% range and inflation running roughly 3–7% across key markets in 2024, pressuring margins and pricing. Hedging, local sourcing and index-linked contracts have reduced net exposure. Clear pricing architecture preserves brand equity while allowing pass-through where markets permit.

Commodity and logistics costs

Steel HRC averaged about $850/ton in 2024, copper roughly $9,000/ton and major thermoplastics near $1,200/ton, while Shanghai–LA 40ft spot freight averaged ~$1,800/FEU in 2024, driving COGS variability. Supply tightness or shocks quickly ripple through margins and inventory turns. Long-term contracts and design-to-cost practices blunt price swings. Nearshoring and larger inventory buffers have measurably improved resilience.

Interest rates and credit access

Consumer financing availability drives big-ticket demand; with US policy rates at 5.25–5.50% (mid‑2024/2025) and 30‑year mortgage averages near 6–7%, affordability and purchase timing compress. Higher rates raise working capital costs and can slow sell‑through, while flexible payment plans and BNPL keep volumes resilient during tight credit. A strong balance sheet and diversified funding reduce refinancing and interest risk for Anonim.

Emerging market growth

- Middle-class demand: 5–7% YoY sales growth in 2024

- Pricing: tiered SKUs + localized features

- Scale: distribution + service networks

- Risk: currency & policy volatility 2024–25

Global appliance maker faces tariff sanctions and energy risks amid incentive-driven premium demand

Appliance demand tracks housing starts (~1.58M US 2023), global market ~USD 330B (2024), and EM household growth ~5–7% (2024); FX swings 10–15% and input costs (steel $850/t, copper $9k/t) pressure margins; policy rates 5.25–5.50% and mortgages ~6–7% constrain affordability while financing and tiered SKUs mitigate risk.

| Metric | 2024 |

|---|---|

| US housing starts | 1.58M |

| Market size | USD 330B |

| FX volatility | 10–15% |

| Policy rate | 5.25–5.50% |

Preview Before You Purchase

Anonim PESTLE Analysis

The preview shown here is the exact Anonim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown with no placeholders or surprises. After checkout you’ll instantly download this same finished document.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our concise PESTLE snapshot for Anonim—see how political shifts, economic trends, and tech disruption shape its outlook. Perfect for investors and planners, this preview teases deeper, actionable insights. Purchase the full analysis to access the complete, editable report instantly.

Political factors

Trade policy and tariffs

Arçelik’s footprint in about 145 countries exposes it to tariff swings, antidumping duties and divergent customs rules that can abruptly raise landed costs and compress margins. Changes in trade agreements (eg regional FTAs) shift pricing power and sourcing choices, sometimes making components subject to duties that add several percentage points to COGS. Proactive supply reconfiguration and dual-sourcing, plus close policy monitoring, are essential to protect margins.

Geopolitical risk exposure

Operations across Europe, Middle East, Africa and Asia face regional instability and logistics disruptions, exemplified by EU gas imports from Russia falling about 80% since 2022, pressuring energy-dependent supply chains. Sanctions and political tensions (over 40 jurisdictions with Russia-related measures by 2024) can constrain markets or suppliers. Scenario planning and diversified routes reduce concentration risk. Insurance and FX/commodity hedging supplement business continuity.

Home-country policy dynamics

As a Turkish multinational, Anonim is shaped by fiscal, monetary and industrial policy—Turkey's general government debt was about 39% of GDP in 2023 and macro policy drives financing costs and incentives. The 1995 EU customs union and modernization talks affect EU access while exports reached roughly USD 254 billion in 2023, supported by state export credit and incentives. Local content requirements in sectors like defense and autos steer manufacturing footprints, and public R&D spending was about 1.1% of GDP (2022), with government energy and YEKA renewables programs expanding capacity and competitiveness.

Public procurement and incentives

Public procurement and appliance-replacement subsidies in 2024–25 have shifted purchase timing and product mix, driving spikes in demand for high-efficiency models and concentrating orders around program windows; US and EU schemes reported double-digit year-on-year increases in efficient appliance sales. Tax credits (2024 IRA and EU national schemes) accelerated premium-model uptake, while incentive volatility forces manufacturers into agile production and inventory strategies. Strategic partnerships with authorities expanded market penetration through bulk procurement and voucher schemes.

- Procurement-driven demand peaks

- Tax credits -> faster premium adoption

- Volatility -> agile planning

- Authority partnerships -> wider reach

Regulatory harmonization and standards

Global appliance maker faces tariff sanctions and energy risks amid incentive-driven premium demand

Arçelik's presence in ~145 countries exposes it to tariff swings and 40+ sanctions-related measures (2024), raising landed costs. EU gas imports from Russia fell ~80% since 2022, heightening energy risk. Turkey's general government debt ~39% of GDP (2023) with exports ~$254bn (2023) shape financing and incentives. Procurement subsidies and 2024 IRA/EU credits accelerate premium appliance demand.

| Metric | Value | Implication |

|---|---|---|

| Market footprint | ~145 countries | Tariff/exposure |

| Sanctions (2024) | 40+ | Supply/market limits |

| EU gas | -80% since 2022 | Energy risk |

| Turkey debt | 39% GDP (2023) | Financing cost |

| Exports | $254bn (2023) | Export support |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Anonim across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and current trends to reflect market and regulatory dynamics; designed for executives, consultants, and entrepreneurs with forward-looking insights ready for reports and investor materials.

An Anonim PESTLE delivers a concise, visually segmented summary that can be dropped into presentations or shared across teams to simplify external risk discussions and speed decision-making. Editable notes let users tailor insights to region or business line for quick alignment in meetings.

Economic factors

Consumer demand cyclicality

Appliances are semi-durable purchases tied to housing cycles and disposable income; US housing starts were about 1.58 million in 2023, illustrating linkages that continued into 2024 as demand tracked construction and remodeling activity.

Economic downturns typically delay replacements while upcycles favor upgrades and premium features, and the global household appliance market was estimated near USD 330 billion in 2024, up modestly from 2023.

Targeted product mix, extended warranties and point-of-sale financing have been shown to stabilize volumes, and counter-seasonal categories such as small kitchen appliances help balance revenue across quarters.

FX volatility and inflation

Revenue and costs span multiple currencies—input imports and global sales—exposing Anonim to FX swings often in the 10–15% range and inflation running roughly 3–7% across key markets in 2024, pressuring margins and pricing. Hedging, local sourcing and index-linked contracts have reduced net exposure. Clear pricing architecture preserves brand equity while allowing pass-through where markets permit.

Commodity and logistics costs

Steel HRC averaged about $850/ton in 2024, copper roughly $9,000/ton and major thermoplastics near $1,200/ton, while Shanghai–LA 40ft spot freight averaged ~$1,800/FEU in 2024, driving COGS variability. Supply tightness or shocks quickly ripple through margins and inventory turns. Long-term contracts and design-to-cost practices blunt price swings. Nearshoring and larger inventory buffers have measurably improved resilience.

Interest rates and credit access

Consumer financing availability drives big-ticket demand; with US policy rates at 5.25–5.50% (mid‑2024/2025) and 30‑year mortgage averages near 6–7%, affordability and purchase timing compress. Higher rates raise working capital costs and can slow sell‑through, while flexible payment plans and BNPL keep volumes resilient during tight credit. A strong balance sheet and diversified funding reduce refinancing and interest risk for Anonim.

Emerging market growth

- Middle-class demand: 5–7% YoY sales growth in 2024

- Pricing: tiered SKUs + localized features

- Scale: distribution + service networks

- Risk: currency & policy volatility 2024–25

Global appliance maker faces tariff sanctions and energy risks amid incentive-driven premium demand

Appliance demand tracks housing starts (~1.58M US 2023), global market ~USD 330B (2024), and EM household growth ~5–7% (2024); FX swings 10–15% and input costs (steel $850/t, copper $9k/t) pressure margins; policy rates 5.25–5.50% and mortgages ~6–7% constrain affordability while financing and tiered SKUs mitigate risk.

| Metric | 2024 |

|---|---|

| US housing starts | 1.58M |

| Market size | USD 330B |

| FX volatility | 10–15% |

| Policy rate | 5.25–5.50% |

Preview Before You Purchase

Anonim PESTLE Analysis

The preview shown here is the exact Anonim PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown with no placeholders or surprises. After checkout you’ll instantly download this same finished document.