ArcelorMittal PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Get a strategic advantage with our concise PESTLE analysis of ArcelorMittal—revealing how political regulations, commodity cycles, and decarbonization trends will shape future performance. Ideal for investors and strategists, it's fully editable and actionable. Buy the full report to access deep-dive insights and ready-to-use slides.

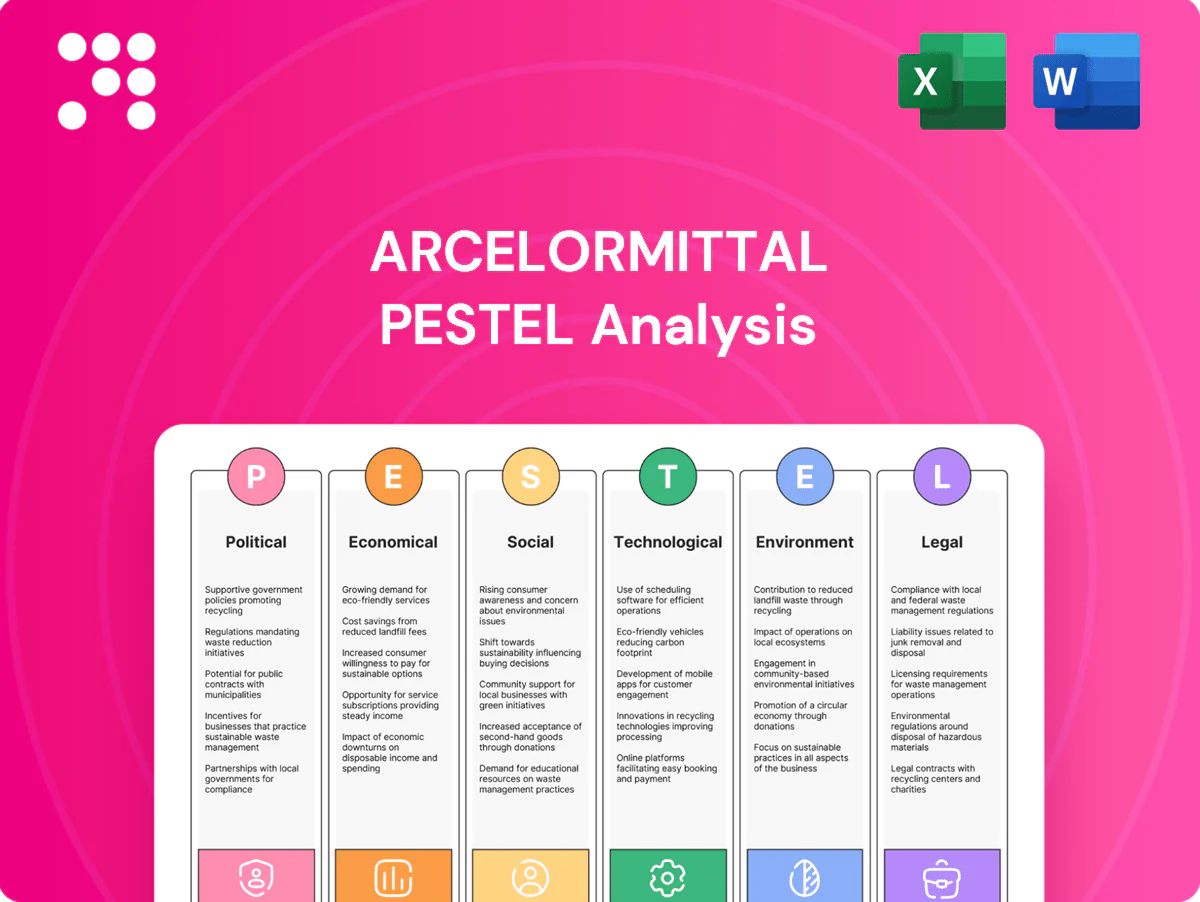

Political factors

Trade policy shifts

Steel trade measures—tariffs, quotas and anti‑dumping duties—can shift flows and prices overnight; US Section 232 tariffs remain at 25% on many steel lines. EU CBAM enters full application in 2026, altering import parity and cost pass‑through. ArcelorMittal, active in 60+ countries with ~150,000 employees, must optimize sourcing and capacity allocation and use proactive lobbying and scenario planning to mitigate volatility.

Geopolitical exposure

Operations and sales span over 60 countries and a commercial footprint in about 160 countries, exposing ArcelorMittal to conflicts, sanctions and regime shifts in key markets. Disruptions to iron ore, coking coal and energy supply chains increase costs and lead times, as seen in 2022–24 commodity volatility. Political risk insurance and diversified logistics networks are critical mitigation. A balanced portfolio across Americas, Europe, Africa and Asia reduces geographic concentration risk.

Industrial policy & subsidies

Governments are channeling major support into green steel, hydrogen and reshoring: the US Inflation Reduction Act commits roughly $369 billion to clean energy incentives and Europe has mobilized multi-billion-euro IPCEI and Green Deal support for low-carbon industry. Accessing grants, tax credits and low-cost financing can materially lift project IRRs. Policy strings such as local-content and job-creation requirements shape siting and supplier choices, so early capture of supportive programs strengthens ArcelorMittal’s competitive positioning.

Resource nationalism

Resource nationalism—e.g., tighter mining licences, higher royalties or export curbs—can compress upstream margins and force changes in internal transfer pricing; world crude steel production was 1,832 Mt in 2024 (World Steel Association), underscoring feedstock importance. Stable community relations and formal benefit-sharing lower permit and social-risk shocks. Alternative feedstock strategies hedge sudden policy shifts.

- Host policy tightening

- Upstream margin pressure

- Transfer-pricing impact

- Community agreements reduce risk

- Feedstock diversification hedge

Energy security policy

- Power price caps reduce short-term volatility but can raise long-term investment risk

- Gas allocation limits can increase feedstock costs; energy ~15–25% of costs

- Long-term PPAs (10–15 years) support decarbonization compliance

- Grid upgrades + renewable build-outs (EU ~42–45% by 2030) enable electrification

Tariffs, CBAM & energy policy force steel majors to retool sourcing across 60+

Political risks—trade measures (US 25% Section 232), CBAM (EU full 2026) and sanctions reshape flows and margins; ArcelorMittal must flex sourcing across 60+ countries. State support (US IRA ~$369bn; EU IPCEI) and local‑content rules drive project economics. Energy policy and resource nationalism (2024 crude steel 1,832 Mt) materially affect costs and siting.

| Factor | Key metric | Impact |

|---|---|---|

| Trade | US 25% tariffs | Price/margin shock |

| Green policy | IRA ~$369bn; CBAM 2026 | Capex subsidy opportunity |

| Energy | Energy 15–25% costs; EU renewables 42–45% by 2030 | Electrification value |

What is included in the product

Explores how external macro-environmental factors uniquely affect ArcelorMittal across Political, Economic, Social, Technological, Environmental and Legal dimensions; data-backed, regionally relevant analysis designed to help executives, consultants and investors identify threats, opportunities and actionable, forward-looking strategies.

Concise, visually segmented PESTLE summary of ArcelorMittal highlighting regulatory, market, environmental and geopolitical risks for quick meeting use; editable notes and export‑ready format for slides, Excel and tablets to align teams and support strategic planning.

Economic factors

Steel demand cycles

Automotive, construction and machinery cycles drive ArcelorMittal's volume and mix, with global crude steel output at 1,878.5 Mt in 2023 (Worldsteel) underpinning demand patterns. Large public programs — US Bipartisan Infrastructure Law ($1.2tn) and green stimulus — can offset private slowdowns. Order books and PMIs (manufacturing PMIs around 50 in 2024) and housing starts guide capacity planning. Flexible production lines allow rapid downtime cuts and product-mix shifts.

Commodity price volatility

Commodity swings in iron ore, coking coal, scrap and energy drive large margin volatility for ArcelorMittal, with raw materials representing roughly half of steel production cash costs. Vertical integration — owned mines in Canada and Brazil and captive coal assets — buffers but does not eliminate exposure to spot spikes. Dynamic pricing, index-linked contracts and hedging have reduced EBITDA volatility in recent years. Optimizing raw-material mix (blast-furnace vs scrap/EAF feed) preserves competitiveness.

Interest rates & financing

Rising policy rates (US Fed funds ~5.25-5.50% mid-2025) lift capex hurdle rates, making green-steel projects harder to justify on IRR alone. ArcelorMittal’s strong balance sheet (net debt ~€4.3bn end-2024) and ~€1.0bn of green bond issuance help lower its WACC and preserve project economics. Access to export credit agencies and longer-tenor facilities improves funding tenor, while macro shifts tighten refinancing windows.

FX and inflation

Multi-currency revenues and costs expose ArcelorMittal to translation and transaction risks, prompting active currency hedges and reliance on natural offsets across EUR, USD, BRL and INR cashflows; inflation raises labor, refractory and maintenance costs, pressuring margins; pricing clauses, surcharges and indexation in contracts are used to recover input inflation.

- FX hedging: active

- Key currencies: EUR/USD/BRL/INR

- Inflation pressure: labor, refractory, maintenance

- Mitigants: pricing clauses, surcharges, natural offsets

Customer mix & premiums

Auto and packaging contracts command value-added premiums but require tight specs and traceability; ArcelorMittal highlights specialty coated and electrical steels as higher-margin lines supporting resilience amid cyclical demand. Construction remains volume-driven and price-sensitive, pressuring margins in flat products. As of 2024 ArcelorMittal targets a 25% CO2 intensity reduction by 2030, making green-steel premiums likely to emerge as standards tighten.

- Auto/packaging: quality-driven premiums, higher margin

- Construction: volume-led, price-sensitive

- Shift: coated/electrical steels = resilience

- Green steel: premium potential as 2030 decarbonization targets tighten

Tariffs, CBAM & energy policy force steel majors to retool sourcing across 60+

Automotive/construction cycles and 2023 global crude steel 1,878.5 Mt drive volumes; US $1.2tn infrastructure and green stimulus support demand. Raw materials (≈50% cash costs) and iron-ore/coal swings create margin volatility; ArcelorMittal net debt ≈€4.3bn (end-2024). FX (EUR/USD/BRL/INR) and inflation raise input costs; pricing clauses and hedges mitigate.

| Metric | Value |

|---|---|

| Steel output 2023 | 1,878.5 Mt |

| Net debt | ≈€4.3bn (end-2024) |

| Fed funds (mid-2025) | 5.25–5.50% |

| Raw-materials share | ≈50% cash costs |

Full Version Awaits

ArcelorMittal PESTLE Analysis

The preview shown here is the exact ArcelorMittal PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with the same layout, data and insights visible in the preview. No placeholders or teasers—this is the final, downloadable file delivered immediately after payment.

Your Shortcut to Market Insight Starts Here

Get a strategic advantage with our concise PESTLE analysis of ArcelorMittal—revealing how political regulations, commodity cycles, and decarbonization trends will shape future performance. Ideal for investors and strategists, it's fully editable and actionable. Buy the full report to access deep-dive insights and ready-to-use slides.

Political factors

Trade policy shifts

Steel trade measures—tariffs, quotas and anti‑dumping duties—can shift flows and prices overnight; US Section 232 tariffs remain at 25% on many steel lines. EU CBAM enters full application in 2026, altering import parity and cost pass‑through. ArcelorMittal, active in 60+ countries with ~150,000 employees, must optimize sourcing and capacity allocation and use proactive lobbying and scenario planning to mitigate volatility.

Geopolitical exposure

Operations and sales span over 60 countries and a commercial footprint in about 160 countries, exposing ArcelorMittal to conflicts, sanctions and regime shifts in key markets. Disruptions to iron ore, coking coal and energy supply chains increase costs and lead times, as seen in 2022–24 commodity volatility. Political risk insurance and diversified logistics networks are critical mitigation. A balanced portfolio across Americas, Europe, Africa and Asia reduces geographic concentration risk.

Industrial policy & subsidies

Governments are channeling major support into green steel, hydrogen and reshoring: the US Inflation Reduction Act commits roughly $369 billion to clean energy incentives and Europe has mobilized multi-billion-euro IPCEI and Green Deal support for low-carbon industry. Accessing grants, tax credits and low-cost financing can materially lift project IRRs. Policy strings such as local-content and job-creation requirements shape siting and supplier choices, so early capture of supportive programs strengthens ArcelorMittal’s competitive positioning.

Resource nationalism

Resource nationalism—e.g., tighter mining licences, higher royalties or export curbs—can compress upstream margins and force changes in internal transfer pricing; world crude steel production was 1,832 Mt in 2024 (World Steel Association), underscoring feedstock importance. Stable community relations and formal benefit-sharing lower permit and social-risk shocks. Alternative feedstock strategies hedge sudden policy shifts.

- Host policy tightening

- Upstream margin pressure

- Transfer-pricing impact

- Community agreements reduce risk

- Feedstock diversification hedge

Energy security policy

- Power price caps reduce short-term volatility but can raise long-term investment risk

- Gas allocation limits can increase feedstock costs; energy ~15–25% of costs

- Long-term PPAs (10–15 years) support decarbonization compliance

- Grid upgrades + renewable build-outs (EU ~42–45% by 2030) enable electrification

Tariffs, CBAM & energy policy force steel majors to retool sourcing across 60+

Political risks—trade measures (US 25% Section 232), CBAM (EU full 2026) and sanctions reshape flows and margins; ArcelorMittal must flex sourcing across 60+ countries. State support (US IRA ~$369bn; EU IPCEI) and local‑content rules drive project economics. Energy policy and resource nationalism (2024 crude steel 1,832 Mt) materially affect costs and siting.

| Factor | Key metric | Impact |

|---|---|---|

| Trade | US 25% tariffs | Price/margin shock |

| Green policy | IRA ~$369bn; CBAM 2026 | Capex subsidy opportunity |

| Energy | Energy 15–25% costs; EU renewables 42–45% by 2030 | Electrification value |

What is included in the product

Explores how external macro-environmental factors uniquely affect ArcelorMittal across Political, Economic, Social, Technological, Environmental and Legal dimensions; data-backed, regionally relevant analysis designed to help executives, consultants and investors identify threats, opportunities and actionable, forward-looking strategies.

Concise, visually segmented PESTLE summary of ArcelorMittal highlighting regulatory, market, environmental and geopolitical risks for quick meeting use; editable notes and export‑ready format for slides, Excel and tablets to align teams and support strategic planning.

Economic factors

Steel demand cycles

Automotive, construction and machinery cycles drive ArcelorMittal's volume and mix, with global crude steel output at 1,878.5 Mt in 2023 (Worldsteel) underpinning demand patterns. Large public programs — US Bipartisan Infrastructure Law ($1.2tn) and green stimulus — can offset private slowdowns. Order books and PMIs (manufacturing PMIs around 50 in 2024) and housing starts guide capacity planning. Flexible production lines allow rapid downtime cuts and product-mix shifts.

Commodity price volatility

Commodity swings in iron ore, coking coal, scrap and energy drive large margin volatility for ArcelorMittal, with raw materials representing roughly half of steel production cash costs. Vertical integration — owned mines in Canada and Brazil and captive coal assets — buffers but does not eliminate exposure to spot spikes. Dynamic pricing, index-linked contracts and hedging have reduced EBITDA volatility in recent years. Optimizing raw-material mix (blast-furnace vs scrap/EAF feed) preserves competitiveness.

Interest rates & financing

Rising policy rates (US Fed funds ~5.25-5.50% mid-2025) lift capex hurdle rates, making green-steel projects harder to justify on IRR alone. ArcelorMittal’s strong balance sheet (net debt ~€4.3bn end-2024) and ~€1.0bn of green bond issuance help lower its WACC and preserve project economics. Access to export credit agencies and longer-tenor facilities improves funding tenor, while macro shifts tighten refinancing windows.

FX and inflation

Multi-currency revenues and costs expose ArcelorMittal to translation and transaction risks, prompting active currency hedges and reliance on natural offsets across EUR, USD, BRL and INR cashflows; inflation raises labor, refractory and maintenance costs, pressuring margins; pricing clauses, surcharges and indexation in contracts are used to recover input inflation.

- FX hedging: active

- Key currencies: EUR/USD/BRL/INR

- Inflation pressure: labor, refractory, maintenance

- Mitigants: pricing clauses, surcharges, natural offsets

Customer mix & premiums

Auto and packaging contracts command value-added premiums but require tight specs and traceability; ArcelorMittal highlights specialty coated and electrical steels as higher-margin lines supporting resilience amid cyclical demand. Construction remains volume-driven and price-sensitive, pressuring margins in flat products. As of 2024 ArcelorMittal targets a 25% CO2 intensity reduction by 2030, making green-steel premiums likely to emerge as standards tighten.

- Auto/packaging: quality-driven premiums, higher margin

- Construction: volume-led, price-sensitive

- Shift: coated/electrical steels = resilience

- Green steel: premium potential as 2030 decarbonization targets tighten

Tariffs, CBAM & energy policy force steel majors to retool sourcing across 60+

Automotive/construction cycles and 2023 global crude steel 1,878.5 Mt drive volumes; US $1.2tn infrastructure and green stimulus support demand. Raw materials (≈50% cash costs) and iron-ore/coal swings create margin volatility; ArcelorMittal net debt ≈€4.3bn (end-2024). FX (EUR/USD/BRL/INR) and inflation raise input costs; pricing clauses and hedges mitigate.

| Metric | Value |

|---|---|

| Steel output 2023 | 1,878.5 Mt |

| Net debt | ≈€4.3bn (end-2024) |

| Fed funds (mid-2025) | 5.25–5.50% |

| Raw-materials share | ≈50% cash costs |

Full Version Awaits

ArcelorMittal PESTLE Analysis

The preview shown here is the exact ArcelorMittal PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with the same layout, data and insights visible in the preview. No placeholders or teasers—this is the final, downloadable file delivered immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Get a strategic advantage with our concise PESTLE analysis of ArcelorMittal—revealing how political regulations, commodity cycles, and decarbonization trends will shape future performance. Ideal for investors and strategists, it's fully editable and actionable. Buy the full report to access deep-dive insights and ready-to-use slides.

Political factors

Trade policy shifts

Steel trade measures—tariffs, quotas and anti‑dumping duties—can shift flows and prices overnight; US Section 232 tariffs remain at 25% on many steel lines. EU CBAM enters full application in 2026, altering import parity and cost pass‑through. ArcelorMittal, active in 60+ countries with ~150,000 employees, must optimize sourcing and capacity allocation and use proactive lobbying and scenario planning to mitigate volatility.

Geopolitical exposure

Operations and sales span over 60 countries and a commercial footprint in about 160 countries, exposing ArcelorMittal to conflicts, sanctions and regime shifts in key markets. Disruptions to iron ore, coking coal and energy supply chains increase costs and lead times, as seen in 2022–24 commodity volatility. Political risk insurance and diversified logistics networks are critical mitigation. A balanced portfolio across Americas, Europe, Africa and Asia reduces geographic concentration risk.

Industrial policy & subsidies

Governments are channeling major support into green steel, hydrogen and reshoring: the US Inflation Reduction Act commits roughly $369 billion to clean energy incentives and Europe has mobilized multi-billion-euro IPCEI and Green Deal support for low-carbon industry. Accessing grants, tax credits and low-cost financing can materially lift project IRRs. Policy strings such as local-content and job-creation requirements shape siting and supplier choices, so early capture of supportive programs strengthens ArcelorMittal’s competitive positioning.

Resource nationalism

Resource nationalism—e.g., tighter mining licences, higher royalties or export curbs—can compress upstream margins and force changes in internal transfer pricing; world crude steel production was 1,832 Mt in 2024 (World Steel Association), underscoring feedstock importance. Stable community relations and formal benefit-sharing lower permit and social-risk shocks. Alternative feedstock strategies hedge sudden policy shifts.

- Host policy tightening

- Upstream margin pressure

- Transfer-pricing impact

- Community agreements reduce risk

- Feedstock diversification hedge

Energy security policy

- Power price caps reduce short-term volatility but can raise long-term investment risk

- Gas allocation limits can increase feedstock costs; energy ~15–25% of costs

- Long-term PPAs (10–15 years) support decarbonization compliance

- Grid upgrades + renewable build-outs (EU ~42–45% by 2030) enable electrification

Tariffs, CBAM & energy policy force steel majors to retool sourcing across 60+

Political risks—trade measures (US 25% Section 232), CBAM (EU full 2026) and sanctions reshape flows and margins; ArcelorMittal must flex sourcing across 60+ countries. State support (US IRA ~$369bn; EU IPCEI) and local‑content rules drive project economics. Energy policy and resource nationalism (2024 crude steel 1,832 Mt) materially affect costs and siting.

| Factor | Key metric | Impact |

|---|---|---|

| Trade | US 25% tariffs | Price/margin shock |

| Green policy | IRA ~$369bn; CBAM 2026 | Capex subsidy opportunity |

| Energy | Energy 15–25% costs; EU renewables 42–45% by 2030 | Electrification value |

What is included in the product

Explores how external macro-environmental factors uniquely affect ArcelorMittal across Political, Economic, Social, Technological, Environmental and Legal dimensions; data-backed, regionally relevant analysis designed to help executives, consultants and investors identify threats, opportunities and actionable, forward-looking strategies.

Concise, visually segmented PESTLE summary of ArcelorMittal highlighting regulatory, market, environmental and geopolitical risks for quick meeting use; editable notes and export‑ready format for slides, Excel and tablets to align teams and support strategic planning.

Economic factors

Steel demand cycles

Automotive, construction and machinery cycles drive ArcelorMittal's volume and mix, with global crude steel output at 1,878.5 Mt in 2023 (Worldsteel) underpinning demand patterns. Large public programs — US Bipartisan Infrastructure Law ($1.2tn) and green stimulus — can offset private slowdowns. Order books and PMIs (manufacturing PMIs around 50 in 2024) and housing starts guide capacity planning. Flexible production lines allow rapid downtime cuts and product-mix shifts.

Commodity price volatility

Commodity swings in iron ore, coking coal, scrap and energy drive large margin volatility for ArcelorMittal, with raw materials representing roughly half of steel production cash costs. Vertical integration — owned mines in Canada and Brazil and captive coal assets — buffers but does not eliminate exposure to spot spikes. Dynamic pricing, index-linked contracts and hedging have reduced EBITDA volatility in recent years. Optimizing raw-material mix (blast-furnace vs scrap/EAF feed) preserves competitiveness.

Interest rates & financing

Rising policy rates (US Fed funds ~5.25-5.50% mid-2025) lift capex hurdle rates, making green-steel projects harder to justify on IRR alone. ArcelorMittal’s strong balance sheet (net debt ~€4.3bn end-2024) and ~€1.0bn of green bond issuance help lower its WACC and preserve project economics. Access to export credit agencies and longer-tenor facilities improves funding tenor, while macro shifts tighten refinancing windows.

FX and inflation

Multi-currency revenues and costs expose ArcelorMittal to translation and transaction risks, prompting active currency hedges and reliance on natural offsets across EUR, USD, BRL and INR cashflows; inflation raises labor, refractory and maintenance costs, pressuring margins; pricing clauses, surcharges and indexation in contracts are used to recover input inflation.

- FX hedging: active

- Key currencies: EUR/USD/BRL/INR

- Inflation pressure: labor, refractory, maintenance

- Mitigants: pricing clauses, surcharges, natural offsets

Customer mix & premiums

Auto and packaging contracts command value-added premiums but require tight specs and traceability; ArcelorMittal highlights specialty coated and electrical steels as higher-margin lines supporting resilience amid cyclical demand. Construction remains volume-driven and price-sensitive, pressuring margins in flat products. As of 2024 ArcelorMittal targets a 25% CO2 intensity reduction by 2030, making green-steel premiums likely to emerge as standards tighten.

- Auto/packaging: quality-driven premiums, higher margin

- Construction: volume-led, price-sensitive

- Shift: coated/electrical steels = resilience

- Green steel: premium potential as 2030 decarbonization targets tighten

Tariffs, CBAM & energy policy force steel majors to retool sourcing across 60+

Automotive/construction cycles and 2023 global crude steel 1,878.5 Mt drive volumes; US $1.2tn infrastructure and green stimulus support demand. Raw materials (≈50% cash costs) and iron-ore/coal swings create margin volatility; ArcelorMittal net debt ≈€4.3bn (end-2024). FX (EUR/USD/BRL/INR) and inflation raise input costs; pricing clauses and hedges mitigate.

| Metric | Value |

|---|---|

| Steel output 2023 | 1,878.5 Mt |

| Net debt | ≈€4.3bn (end-2024) |

| Fed funds (mid-2025) | 5.25–5.50% |

| Raw-materials share | ≈50% cash costs |

Full Version Awaits

ArcelorMittal PESTLE Analysis

The preview shown here is the exact ArcelorMittal PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with the same layout, data and insights visible in the preview. No placeholders or teasers—this is the final, downloadable file delivered immediately after payment.