Arcland Sakamoto Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

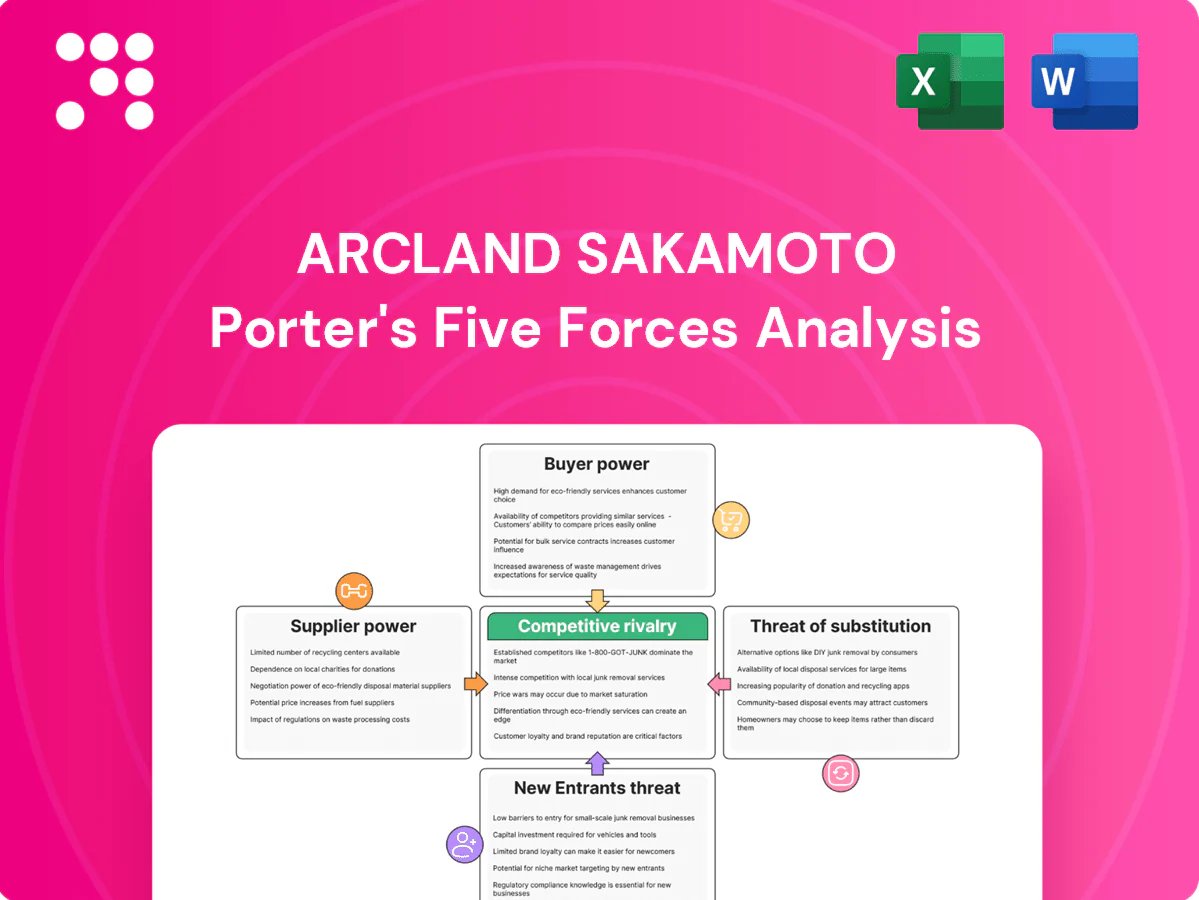

Arcland Sakamoto faces moderate supplier leverage, stiff retail competition, and evolving substitute threats that together shape its margin outlook and strategic priorities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arcland Sakamoto’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier mix

Arcland Sakamoto sources from tool makers, hardware manufacturers, garden inputs, pet food firms and FMCG suppliers, creating a diverse supplier mix that reduces single-source dependence. Fragmentation across fasteners, gardening and household lines tempers supplier leverage and enables competitive sourcing. Certain categories remain concentrated, requiring focused category management and strategic partnerships. The retailer’s multi-format footprint supports cross-category negotiation to balance supplier power.

Branded tools concentration

Branded power-tool and premium hardware markets are concentrated in Japan and globally, with Makita, Koki/Hikoki and Bosch/DeWalt collectively estimated to hold over 50% of Japan’s branded power-tool sales, strengthening supplier bargaining power. Professional buyers often specify brands, reducing retailer switching and raising margin pressure on Arcland Sakamoto. Volume commitments and co-marketing deals can secure price and promotional concessions, while private-label expansion (now ~10–15% of some retailers’ tool assortments) helps offset brand concentration.

Private label and OEM

Private-label consumables and basic tools reduce Arcland Sakamoto’s reliance on national brands by allowing control over costs and assortment, while OEM sourcing and tiered private assortments create clear pricing anchors that protect margins. These strategies raise switching costs for shoppers attached to the retailer’s brands and support higher gross margins. Sustaining this edge requires ongoing investment in quality control and supplier development to avoid reputational risk.

Import, FX, and commodity exposure

Imported inventory exposes Arcland Sakamoto to yen moves (USD/JPY averaged about 148 in 2024) and freight-rate swings, increasing supplier leverage; categories tied to steel, lumber and chemicals see direct commodity pass-throughs to costs. Long-term supply contracts and FX hedging reduce but do not eliminate spikes. Dual-sourcing and regional diversification cut single-supplier shocks.

- USD/JPY ≈148 (2024)

- High commodity pass-through for steel/lumber/chemicals

- Hedging/contracts mitigate but not remove risk

- Dual-sourcing/regional spread lowers supplier power

Logistics and availability

Just-in-time expectations and seasonal peaks for gardening and typhoon preparation make reliable supplier logistics critical, elevating bargaining power for suppliers who can guarantee on-time delivery during tight windows.

Retailer distribution center capabilities and data sharing (sales velocity, inventory positions) can secure priority allocations, while joint demand planning with key suppliers reduces stockouts and rebalances power asymmetry.

- suppliers with superior logistics gain leverage

- dc capability and data sharing secure priority

- joint demand planning lowers stockouts

Moderate supplier power — branded tools ≈ 50%, hedging softens risk

Supplier power is moderate: diversified sourcing reduces single-source risk, but branded power-tool concentration (Makita, Koki/Hikoki, Bosch ~50% of Japan) and commodity-linked categories raise leverage. Private-label (≈10–15%) and OEM tiers soften pressure; long-term contracts, FX hedging (USD/JPY ≈148 in 2024) and DC/data sharing mitigate risks.

| Metric | Value |

|---|---|

| Branded power-tool share | ~50% |

| Private-label share | 10–15% |

| USD/JPY (2024) | ≈148 |

| Commodity exposure | High (steel/lumber/chem) |

| Mitigants | Hedging, contracts, dual-sourcing |

What is included in the product

Tailored Five Forces analysis for Arcland Sakamoto that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, and barriers deterring new entrants. Identifies disruptive threats, substitutes, and strategic positions to protect market share—ready for inclusion in investor materials or strategy decks.

A clear, one-sheet summary of Arcland Sakamoto's five competitive forces—ideal for quick strategic decisions, investor briefings, and pinpointing which pressures to alleviate first.

Customers Bargaining Power

Fragmented DIY demand

Individual DIY shoppers are numerous and typically low-volume, which limits their collective bargaining power. Frequent impulse and convenience buys in small baskets reduce price sensitivity and increase margin resilience. Clear merchandising and in-store advice shift focus from price to solution value. Loyalty programs capture repeat spend and behavioral data to further soften customer price pressure.

Professional buyer leverage

Contractors and trades purchase in high volumes, expect bulk pricing and can switch suppliers for better terms, raising their bargaining power against Arcland Sakamoto. Their sensitivity to brand and immediate availability amplifies leverage, pressuring margins. Trade desks, extended credit terms and job-site delivery help lock in accounts. Value-added services such as technical support and bulk logistics reduce churn despite persistent price pressure.

High price transparency

High price transparency on platforms like Amazon and Rakuten (Japan e‑commerce penetration ~13% in 2024) strengthens customer bargaining power as branded SKUs are easily compared; many shoppers showroom in-store then buy online if price gaps persist. Dynamic pricing and platform‑exclusive SKUs obscure direct comparability, while click‑and‑collect and rapid fulfillment preserve enough convenience to retain on‑premise sales.

Cross-category basket effects

Customers bundle tools, consumables and household goods, diluting price sensitivity on single SKUs while promotions on traffic drivers (e.g., seasonal discounts) shape overall basket margin; in-store services and project guidance raise perceived value and willingness to pay; broad assortment reduces multi-stop shopping, strengthening buyer dependence on Arcland Sakamoto.

Switching costs are modest

Alternative chains and e-commerce are widely available across Japan’s urban areas—convenience store density remains high (about 56,000 stores nationwide as of 2023), and online retail penetration rose materially into 2024, keeping routine-item switching costs low and strengthening buyer power.

Service differentiation, extended warranties, and installation support by Arcland Sakamoto can raise stickiness for higher-ticket purchases, while private-label ranges create mild lock-in for repeat buyers.

- Low switching costs for routine items

- High urban channel availability (~56,000 convenience stores, 2023)

- Service/warranty/installation increase retention

- Private-label mildly reduces churn

Contractors pressure prices; Japan's low switching costs meet loyalty and private-label stickiness

Individual DIY buyers are low-volume with limited bargaining power; contractors buy bulk and exert stronger price pressure. High price transparency (Japan e‑commerce penetration ~13% in 2024) and ~56,000 convenience stores (2023) keep switching costs low, while loyalty, services and private‑label raise stickiness for higher‑ticket sales.

| Metric | Value |

|---|---|

| Japan e‑commerce penetration (2024) | ~13% |

| Convenience stores (2023) | ~56,000 |

| Urbanization (approx.) | ~91% |

Same Document Delivered

Arcland Sakamoto Porter's Five Forces Analysis

This preview shows the exact Arcland Sakamoto Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The report provides a concise evaluation of competitive rivalry, supplier and buyer power, and threats of entrants and substitutes, plus strategic implications tailored to Arcland Sakamoto. It's fully formatted and ready to download and use upon payment.

A Must-Have Tool for Decision-Makers

Arcland Sakamoto faces moderate supplier leverage, stiff retail competition, and evolving substitute threats that together shape its margin outlook and strategic priorities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arcland Sakamoto’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier mix

Arcland Sakamoto sources from tool makers, hardware manufacturers, garden inputs, pet food firms and FMCG suppliers, creating a diverse supplier mix that reduces single-source dependence. Fragmentation across fasteners, gardening and household lines tempers supplier leverage and enables competitive sourcing. Certain categories remain concentrated, requiring focused category management and strategic partnerships. The retailer’s multi-format footprint supports cross-category negotiation to balance supplier power.

Branded tools concentration

Branded power-tool and premium hardware markets are concentrated in Japan and globally, with Makita, Koki/Hikoki and Bosch/DeWalt collectively estimated to hold over 50% of Japan’s branded power-tool sales, strengthening supplier bargaining power. Professional buyers often specify brands, reducing retailer switching and raising margin pressure on Arcland Sakamoto. Volume commitments and co-marketing deals can secure price and promotional concessions, while private-label expansion (now ~10–15% of some retailers’ tool assortments) helps offset brand concentration.

Private label and OEM

Private-label consumables and basic tools reduce Arcland Sakamoto’s reliance on national brands by allowing control over costs and assortment, while OEM sourcing and tiered private assortments create clear pricing anchors that protect margins. These strategies raise switching costs for shoppers attached to the retailer’s brands and support higher gross margins. Sustaining this edge requires ongoing investment in quality control and supplier development to avoid reputational risk.

Import, FX, and commodity exposure

Imported inventory exposes Arcland Sakamoto to yen moves (USD/JPY averaged about 148 in 2024) and freight-rate swings, increasing supplier leverage; categories tied to steel, lumber and chemicals see direct commodity pass-throughs to costs. Long-term supply contracts and FX hedging reduce but do not eliminate spikes. Dual-sourcing and regional diversification cut single-supplier shocks.

- USD/JPY ≈148 (2024)

- High commodity pass-through for steel/lumber/chemicals

- Hedging/contracts mitigate but not remove risk

- Dual-sourcing/regional spread lowers supplier power

Logistics and availability

Just-in-time expectations and seasonal peaks for gardening and typhoon preparation make reliable supplier logistics critical, elevating bargaining power for suppliers who can guarantee on-time delivery during tight windows.

Retailer distribution center capabilities and data sharing (sales velocity, inventory positions) can secure priority allocations, while joint demand planning with key suppliers reduces stockouts and rebalances power asymmetry.

- suppliers with superior logistics gain leverage

- dc capability and data sharing secure priority

- joint demand planning lowers stockouts

Moderate supplier power — branded tools ≈ 50%, hedging softens risk

Supplier power is moderate: diversified sourcing reduces single-source risk, but branded power-tool concentration (Makita, Koki/Hikoki, Bosch ~50% of Japan) and commodity-linked categories raise leverage. Private-label (≈10–15%) and OEM tiers soften pressure; long-term contracts, FX hedging (USD/JPY ≈148 in 2024) and DC/data sharing mitigate risks.

| Metric | Value |

|---|---|

| Branded power-tool share | ~50% |

| Private-label share | 10–15% |

| USD/JPY (2024) | ≈148 |

| Commodity exposure | High (steel/lumber/chem) |

| Mitigants | Hedging, contracts, dual-sourcing |

What is included in the product

Tailored Five Forces analysis for Arcland Sakamoto that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, and barriers deterring new entrants. Identifies disruptive threats, substitutes, and strategic positions to protect market share—ready for inclusion in investor materials or strategy decks.

A clear, one-sheet summary of Arcland Sakamoto's five competitive forces—ideal for quick strategic decisions, investor briefings, and pinpointing which pressures to alleviate first.

Customers Bargaining Power

Fragmented DIY demand

Individual DIY shoppers are numerous and typically low-volume, which limits their collective bargaining power. Frequent impulse and convenience buys in small baskets reduce price sensitivity and increase margin resilience. Clear merchandising and in-store advice shift focus from price to solution value. Loyalty programs capture repeat spend and behavioral data to further soften customer price pressure.

Professional buyer leverage

Contractors and trades purchase in high volumes, expect bulk pricing and can switch suppliers for better terms, raising their bargaining power against Arcland Sakamoto. Their sensitivity to brand and immediate availability amplifies leverage, pressuring margins. Trade desks, extended credit terms and job-site delivery help lock in accounts. Value-added services such as technical support and bulk logistics reduce churn despite persistent price pressure.

High price transparency

High price transparency on platforms like Amazon and Rakuten (Japan e‑commerce penetration ~13% in 2024) strengthens customer bargaining power as branded SKUs are easily compared; many shoppers showroom in-store then buy online if price gaps persist. Dynamic pricing and platform‑exclusive SKUs obscure direct comparability, while click‑and‑collect and rapid fulfillment preserve enough convenience to retain on‑premise sales.

Cross-category basket effects

Customers bundle tools, consumables and household goods, diluting price sensitivity on single SKUs while promotions on traffic drivers (e.g., seasonal discounts) shape overall basket margin; in-store services and project guidance raise perceived value and willingness to pay; broad assortment reduces multi-stop shopping, strengthening buyer dependence on Arcland Sakamoto.

Switching costs are modest

Alternative chains and e-commerce are widely available across Japan’s urban areas—convenience store density remains high (about 56,000 stores nationwide as of 2023), and online retail penetration rose materially into 2024, keeping routine-item switching costs low and strengthening buyer power.

Service differentiation, extended warranties, and installation support by Arcland Sakamoto can raise stickiness for higher-ticket purchases, while private-label ranges create mild lock-in for repeat buyers.

- Low switching costs for routine items

- High urban channel availability (~56,000 convenience stores, 2023)

- Service/warranty/installation increase retention

- Private-label mildly reduces churn

Contractors pressure prices; Japan's low switching costs meet loyalty and private-label stickiness

Individual DIY buyers are low-volume with limited bargaining power; contractors buy bulk and exert stronger price pressure. High price transparency (Japan e‑commerce penetration ~13% in 2024) and ~56,000 convenience stores (2023) keep switching costs low, while loyalty, services and private‑label raise stickiness for higher‑ticket sales.

| Metric | Value |

|---|---|

| Japan e‑commerce penetration (2024) | ~13% |

| Convenience stores (2023) | ~56,000 |

| Urbanization (approx.) | ~91% |

Same Document Delivered

Arcland Sakamoto Porter's Five Forces Analysis

This preview shows the exact Arcland Sakamoto Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The report provides a concise evaluation of competitive rivalry, supplier and buyer power, and threats of entrants and substitutes, plus strategic implications tailored to Arcland Sakamoto. It's fully formatted and ready to download and use upon payment.

Description

A Must-Have Tool for Decision-Makers

Arcland Sakamoto faces moderate supplier leverage, stiff retail competition, and evolving substitute threats that together shape its margin outlook and strategic priorities. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arcland Sakamoto’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier mix

Arcland Sakamoto sources from tool makers, hardware manufacturers, garden inputs, pet food firms and FMCG suppliers, creating a diverse supplier mix that reduces single-source dependence. Fragmentation across fasteners, gardening and household lines tempers supplier leverage and enables competitive sourcing. Certain categories remain concentrated, requiring focused category management and strategic partnerships. The retailer’s multi-format footprint supports cross-category negotiation to balance supplier power.

Branded tools concentration

Branded power-tool and premium hardware markets are concentrated in Japan and globally, with Makita, Koki/Hikoki and Bosch/DeWalt collectively estimated to hold over 50% of Japan’s branded power-tool sales, strengthening supplier bargaining power. Professional buyers often specify brands, reducing retailer switching and raising margin pressure on Arcland Sakamoto. Volume commitments and co-marketing deals can secure price and promotional concessions, while private-label expansion (now ~10–15% of some retailers’ tool assortments) helps offset brand concentration.

Private label and OEM

Private-label consumables and basic tools reduce Arcland Sakamoto’s reliance on national brands by allowing control over costs and assortment, while OEM sourcing and tiered private assortments create clear pricing anchors that protect margins. These strategies raise switching costs for shoppers attached to the retailer’s brands and support higher gross margins. Sustaining this edge requires ongoing investment in quality control and supplier development to avoid reputational risk.

Import, FX, and commodity exposure

Imported inventory exposes Arcland Sakamoto to yen moves (USD/JPY averaged about 148 in 2024) and freight-rate swings, increasing supplier leverage; categories tied to steel, lumber and chemicals see direct commodity pass-throughs to costs. Long-term supply contracts and FX hedging reduce but do not eliminate spikes. Dual-sourcing and regional diversification cut single-supplier shocks.

- USD/JPY ≈148 (2024)

- High commodity pass-through for steel/lumber/chemicals

- Hedging/contracts mitigate but not remove risk

- Dual-sourcing/regional spread lowers supplier power

Logistics and availability

Just-in-time expectations and seasonal peaks for gardening and typhoon preparation make reliable supplier logistics critical, elevating bargaining power for suppliers who can guarantee on-time delivery during tight windows.

Retailer distribution center capabilities and data sharing (sales velocity, inventory positions) can secure priority allocations, while joint demand planning with key suppliers reduces stockouts and rebalances power asymmetry.

- suppliers with superior logistics gain leverage

- dc capability and data sharing secure priority

- joint demand planning lowers stockouts

Moderate supplier power — branded tools ≈ 50%, hedging softens risk

Supplier power is moderate: diversified sourcing reduces single-source risk, but branded power-tool concentration (Makita, Koki/Hikoki, Bosch ~50% of Japan) and commodity-linked categories raise leverage. Private-label (≈10–15%) and OEM tiers soften pressure; long-term contracts, FX hedging (USD/JPY ≈148 in 2024) and DC/data sharing mitigate risks.

| Metric | Value |

|---|---|

| Branded power-tool share | ~50% |

| Private-label share | 10–15% |

| USD/JPY (2024) | ≈148 |

| Commodity exposure | High (steel/lumber/chem) |

| Mitigants | Hedging, contracts, dual-sourcing |

What is included in the product

Tailored Five Forces analysis for Arcland Sakamoto that uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, and barriers deterring new entrants. Identifies disruptive threats, substitutes, and strategic positions to protect market share—ready for inclusion in investor materials or strategy decks.

A clear, one-sheet summary of Arcland Sakamoto's five competitive forces—ideal for quick strategic decisions, investor briefings, and pinpointing which pressures to alleviate first.

Customers Bargaining Power

Fragmented DIY demand

Individual DIY shoppers are numerous and typically low-volume, which limits their collective bargaining power. Frequent impulse and convenience buys in small baskets reduce price sensitivity and increase margin resilience. Clear merchandising and in-store advice shift focus from price to solution value. Loyalty programs capture repeat spend and behavioral data to further soften customer price pressure.

Professional buyer leverage

Contractors and trades purchase in high volumes, expect bulk pricing and can switch suppliers for better terms, raising their bargaining power against Arcland Sakamoto. Their sensitivity to brand and immediate availability amplifies leverage, pressuring margins. Trade desks, extended credit terms and job-site delivery help lock in accounts. Value-added services such as technical support and bulk logistics reduce churn despite persistent price pressure.

High price transparency

High price transparency on platforms like Amazon and Rakuten (Japan e‑commerce penetration ~13% in 2024) strengthens customer bargaining power as branded SKUs are easily compared; many shoppers showroom in-store then buy online if price gaps persist. Dynamic pricing and platform‑exclusive SKUs obscure direct comparability, while click‑and‑collect and rapid fulfillment preserve enough convenience to retain on‑premise sales.

Cross-category basket effects

Customers bundle tools, consumables and household goods, diluting price sensitivity on single SKUs while promotions on traffic drivers (e.g., seasonal discounts) shape overall basket margin; in-store services and project guidance raise perceived value and willingness to pay; broad assortment reduces multi-stop shopping, strengthening buyer dependence on Arcland Sakamoto.

Switching costs are modest

Alternative chains and e-commerce are widely available across Japan’s urban areas—convenience store density remains high (about 56,000 stores nationwide as of 2023), and online retail penetration rose materially into 2024, keeping routine-item switching costs low and strengthening buyer power.

Service differentiation, extended warranties, and installation support by Arcland Sakamoto can raise stickiness for higher-ticket purchases, while private-label ranges create mild lock-in for repeat buyers.

- Low switching costs for routine items

- High urban channel availability (~56,000 convenience stores, 2023)

- Service/warranty/installation increase retention

- Private-label mildly reduces churn

Contractors pressure prices; Japan's low switching costs meet loyalty and private-label stickiness

Individual DIY buyers are low-volume with limited bargaining power; contractors buy bulk and exert stronger price pressure. High price transparency (Japan e‑commerce penetration ~13% in 2024) and ~56,000 convenience stores (2023) keep switching costs low, while loyalty, services and private‑label raise stickiness for higher‑ticket sales.

| Metric | Value |

|---|---|

| Japan e‑commerce penetration (2024) | ~13% |

| Convenience stores (2023) | ~56,000 |

| Urbanization (approx.) | ~91% |

Same Document Delivered

Arcland Sakamoto Porter's Five Forces Analysis

This preview shows the exact Arcland Sakamoto Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The report provides a concise evaluation of competitive rivalry, supplier and buyer power, and threats of entrants and substitutes, plus strategic implications tailored to Arcland Sakamoto. It's fully formatted and ready to download and use upon payment.