Arco Construction Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

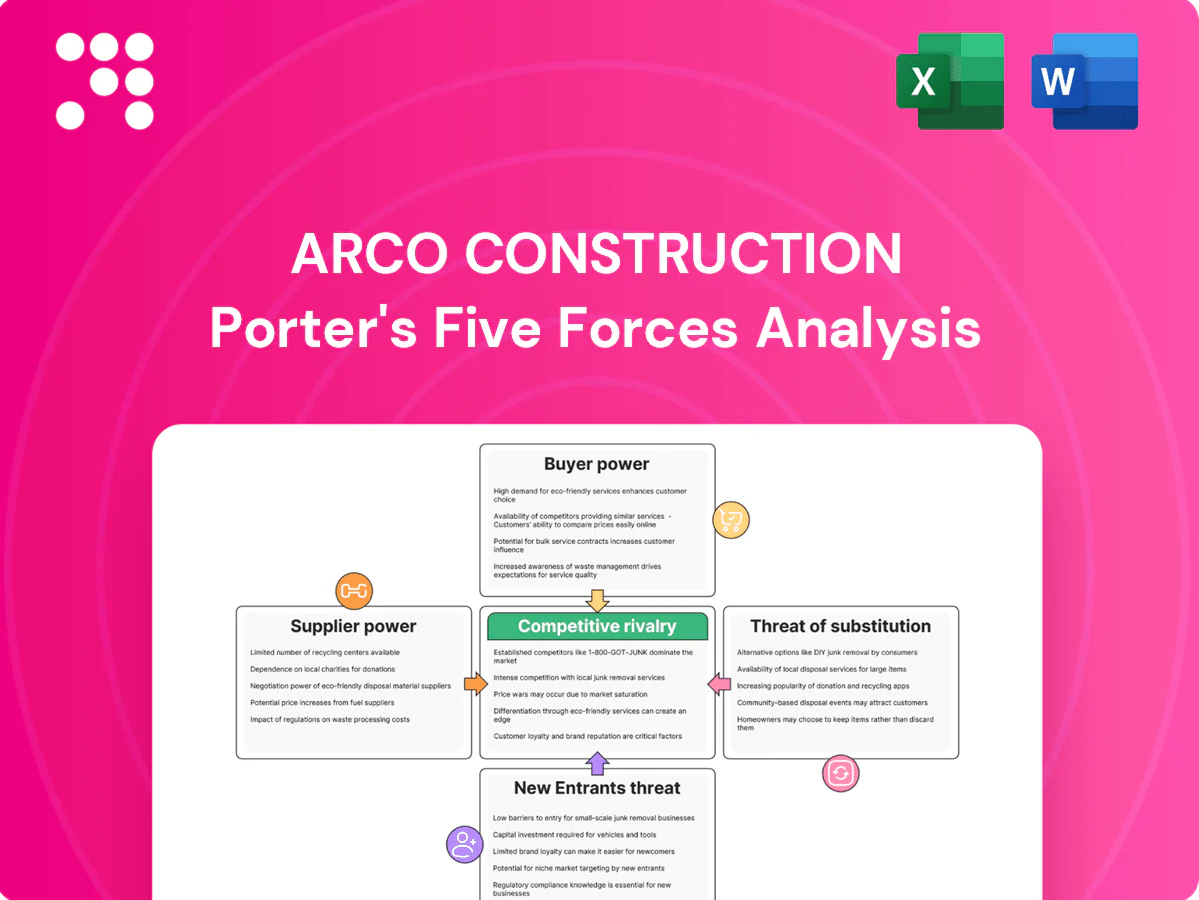

Arco Construction faces moderate buyer power, fragmented suppliers, and stiff rivalry from regional builders impacting margins. Potential new entrants and substitute materials pose emerging threats while regulatory hurdles shape project pipelines. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic recommendations tailored to Arco Construction.

Suppliers Bargaining Power

Specialized trades dependence

ARCO depends heavily on skilled subcontractors for MEP, concrete and specialty systems, concentrating supplier power where trade scarcity exists; construction employment exceeded pre‑pandemic levels in 2024 but skilled trades remain tight. Scarcity in these trades elevates bid prices and elongates schedules, increasing ARCO’s cost and timeline risk. Rigorous prequalification and long‑term partnering stabilize availability, while design‑build integration bundles scopes to reduce fragmentation and subcontractor leverage.

Key materials price volatility

Steel, concrete, lumber and HVAC equipment see cyclical price swings often ranging 10–30% historically, with 2024 still showing elevated volatility versus pre‑pandemic levels. Global supply shocks and freight swings (Baltic Dry Index history) can compress GMP margins by several percentage points on large projects. Early procurement and hedging clauses reduce exposure. Value engineering in design offsets cost spikes by optimizing material use.

OEM lead times and capacity

Elevators (20–30 weeks), medium-voltage switchgear (16–28 weeks) and rooftop units (8–20 weeks) commonly face extended 2024 lead times, making OEM capacity constraints a critical-path risk. ARCO’s front-loaded design enables submittals/releases earlier in the schedule. Alternate approvals add schedule flexibility and mitigate OEM bottlenecks.

Regional supplier concentration

Regional supplier concentration raises leverage where industrial and multifamily work clusters in major metros; about 3,600 ready‑mix plants nationwide (PCA, 2024) means local batch plants can command premium margins on tight jobs, while Arco can counter by sourcing multi‑region fabricators and planning logistics to pull from adjacent markets.

- Local batch plants: concentrated supply

- 3,600 ready‑mix plants (PCA 2024)

- Multi‑region vendors: increased competition

- Logistics planning: access adjacent markets

Contract terms and pass-through

Subcontractor risk-shift clauses materially lift Arco Construction bid pricing as subcontractors — supplying roughly 60–80% of direct trade value in 2024 — price contingency into quotes. Limited willingness to hold prices beyond short windows erodes revenue certainty. Escalation allowances and unit-rate schedules redistribute material and labour volatility, while clear scopes curtail change-order bargaining power.

- risk-shift

- price-hold

- escalation

- scope-clarity

Subcontractor concentration, material volatility and long lead times threaten GMP and schedule

ARCO faces concentrated supplier power: subcontractors supply 60–80% of direct trade value (2024) and skilled trades remain tight despite employment above pre‑pandemic levels. Material volatility (steel/concrete/lumber) historically 10–30% raises GMP risk; elevators 20–30w, switchgear 16–28w, RTUs 8–20w create critical‑path pressure. Mitigants: prequalification, early procurement, design‑build bundling.

| Item | 2024 metric | Impact |

|---|---|---|

| Subcontractor share | 60–80% | High price/schedule leverage |

| Ready‑mix plants | 3,600 (PCA 2024) | Local premium |

| Lead times | Elev 20–30w; SWG 16–28w; RTU 8–20w | Critical‑path risk |

| Material volatility | 10–30% | GMP margin compression |

What is included in the product

Tailored exclusively for Arco Construction, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and emerging threats shaping its pricing and profitability.

A concise one-sheet Porter's Five Forces for Arco Construction that highlights strategic pressures and relief points—ready to drop into decks; adjustable inputs let you model scenarios, reduce uncertainty, and speed confident decision-making.

Customers Bargaining Power

Sophisticated owner base

Industrial and commercial owners are experienced and highly price-sensitive, often benchmarking Arco against multiple design-builders on 2024 projects exceeding $100M. Transparent GMP and open-book models reduce scrutiny by providing line-item visibility and have been adopted across major tenders in 2024. Clear performance metrics—schedule adherence, cost variance, safety TRIR—and KPIs (targeted schedule adherence >90%) strengthen Arco’s credibility with sophisticated owners.

Project scale and pipeline

Large programs (typically >$5M) give buyers significant volume leverage, with 2024 procurement rounds commonly yielding 5–15% price concessions. Multi-site rollouts (10+ locations) increase demands for discounts and priority scheduling. ARCO can trade rate for continuity and predictability; master service agreements lock pipeline and stabilize margins.

Bid comparability

Owners solicit competitive proposals with standardized assumptions to enable bid comparability, driving price pressure when detailed alternates are included and often compressing margins; industry estimates in 2024 showed standardized bidding increased shortlisted bids by about 40%. Early collaboration shifts selection toward best value, with early contractor involvement reducing expected cost overruns by roughly 25% in 2024 studies. Differentiation in speed and delivery certainty breaks pure price comparisons and supports premium pricing for predictable schedules.

Switching costs and stage gates

Owners often switch pre-construction partners before final GMP, so low early-stage switching costs amplify buyer power; ARCO counters this with upfront design IP and permitting momentum that increase stickiness, while milestone-based commitments align incentives and reduce late-stage churn.

- Early switching: increases buyer leverage

- ARCO design IP: raises retention

- Permitting momentum: accelerates lock-in

- Milestones: align risks and payments

Performance guarantees

Owners push GMP/open-book; ECI trims overruns ~25%, delays >60%

Industrial owners are price-sensitive, benchmarking ARCO on 2024 projects >$100M; GMP/open-book models and KPIs (target schedule adherence >90%) increase scrutiny.

Large programs yield 5–15% concessions; standardized bids raised shortlisted bids ~40%, and early contractor involvement cut expected cost overruns ~25% in 2024.

Over 60% of projects faced delays in 2024, driving LDs; ARCO mitigates via IP, permitting momentum, QA/QC and documented buffers.

| Metric | 2024 Value |

|---|---|

| Benchmarked project size | >$100M |

| Typical price concession | 5–15% |

| Shortlisted bids ↑ | ~40% |

| ECI reduces overruns | ~25% |

| Projects with delays | >60% |

| Target schedule adherence | >90% |

Same Document Delivered

Arco Construction Porter's Five Forces Analysis

This preview shows the exact Arco Construction Porter’s Five Forces analysis you'll receive upon purchase—fully written, formatted, and ready to download. It assesses supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable, data-driven conclusions. No placeholders or samples—what you see is the final deliverable and will be available instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

Arco Construction faces moderate buyer power, fragmented suppliers, and stiff rivalry from regional builders impacting margins. Potential new entrants and substitute materials pose emerging threats while regulatory hurdles shape project pipelines. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic recommendations tailored to Arco Construction.

Suppliers Bargaining Power

Specialized trades dependence

ARCO depends heavily on skilled subcontractors for MEP, concrete and specialty systems, concentrating supplier power where trade scarcity exists; construction employment exceeded pre‑pandemic levels in 2024 but skilled trades remain tight. Scarcity in these trades elevates bid prices and elongates schedules, increasing ARCO’s cost and timeline risk. Rigorous prequalification and long‑term partnering stabilize availability, while design‑build integration bundles scopes to reduce fragmentation and subcontractor leverage.

Key materials price volatility

Steel, concrete, lumber and HVAC equipment see cyclical price swings often ranging 10–30% historically, with 2024 still showing elevated volatility versus pre‑pandemic levels. Global supply shocks and freight swings (Baltic Dry Index history) can compress GMP margins by several percentage points on large projects. Early procurement and hedging clauses reduce exposure. Value engineering in design offsets cost spikes by optimizing material use.

OEM lead times and capacity

Elevators (20–30 weeks), medium-voltage switchgear (16–28 weeks) and rooftop units (8–20 weeks) commonly face extended 2024 lead times, making OEM capacity constraints a critical-path risk. ARCO’s front-loaded design enables submittals/releases earlier in the schedule. Alternate approvals add schedule flexibility and mitigate OEM bottlenecks.

Regional supplier concentration

Regional supplier concentration raises leverage where industrial and multifamily work clusters in major metros; about 3,600 ready‑mix plants nationwide (PCA, 2024) means local batch plants can command premium margins on tight jobs, while Arco can counter by sourcing multi‑region fabricators and planning logistics to pull from adjacent markets.

- Local batch plants: concentrated supply

- 3,600 ready‑mix plants (PCA 2024)

- Multi‑region vendors: increased competition

- Logistics planning: access adjacent markets

Contract terms and pass-through

Subcontractor risk-shift clauses materially lift Arco Construction bid pricing as subcontractors — supplying roughly 60–80% of direct trade value in 2024 — price contingency into quotes. Limited willingness to hold prices beyond short windows erodes revenue certainty. Escalation allowances and unit-rate schedules redistribute material and labour volatility, while clear scopes curtail change-order bargaining power.

- risk-shift

- price-hold

- escalation

- scope-clarity

Subcontractor concentration, material volatility and long lead times threaten GMP and schedule

ARCO faces concentrated supplier power: subcontractors supply 60–80% of direct trade value (2024) and skilled trades remain tight despite employment above pre‑pandemic levels. Material volatility (steel/concrete/lumber) historically 10–30% raises GMP risk; elevators 20–30w, switchgear 16–28w, RTUs 8–20w create critical‑path pressure. Mitigants: prequalification, early procurement, design‑build bundling.

| Item | 2024 metric | Impact |

|---|---|---|

| Subcontractor share | 60–80% | High price/schedule leverage |

| Ready‑mix plants | 3,600 (PCA 2024) | Local premium |

| Lead times | Elev 20–30w; SWG 16–28w; RTU 8–20w | Critical‑path risk |

| Material volatility | 10–30% | GMP margin compression |

What is included in the product

Tailored exclusively for Arco Construction, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and emerging threats shaping its pricing and profitability.

A concise one-sheet Porter's Five Forces for Arco Construction that highlights strategic pressures and relief points—ready to drop into decks; adjustable inputs let you model scenarios, reduce uncertainty, and speed confident decision-making.

Customers Bargaining Power

Sophisticated owner base

Industrial and commercial owners are experienced and highly price-sensitive, often benchmarking Arco against multiple design-builders on 2024 projects exceeding $100M. Transparent GMP and open-book models reduce scrutiny by providing line-item visibility and have been adopted across major tenders in 2024. Clear performance metrics—schedule adherence, cost variance, safety TRIR—and KPIs (targeted schedule adherence >90%) strengthen Arco’s credibility with sophisticated owners.

Project scale and pipeline

Large programs (typically >$5M) give buyers significant volume leverage, with 2024 procurement rounds commonly yielding 5–15% price concessions. Multi-site rollouts (10+ locations) increase demands for discounts and priority scheduling. ARCO can trade rate for continuity and predictability; master service agreements lock pipeline and stabilize margins.

Bid comparability

Owners solicit competitive proposals with standardized assumptions to enable bid comparability, driving price pressure when detailed alternates are included and often compressing margins; industry estimates in 2024 showed standardized bidding increased shortlisted bids by about 40%. Early collaboration shifts selection toward best value, with early contractor involvement reducing expected cost overruns by roughly 25% in 2024 studies. Differentiation in speed and delivery certainty breaks pure price comparisons and supports premium pricing for predictable schedules.

Switching costs and stage gates

Owners often switch pre-construction partners before final GMP, so low early-stage switching costs amplify buyer power; ARCO counters this with upfront design IP and permitting momentum that increase stickiness, while milestone-based commitments align incentives and reduce late-stage churn.

- Early switching: increases buyer leverage

- ARCO design IP: raises retention

- Permitting momentum: accelerates lock-in

- Milestones: align risks and payments

Performance guarantees

Owners push GMP/open-book; ECI trims overruns ~25%, delays >60%

Industrial owners are price-sensitive, benchmarking ARCO on 2024 projects >$100M; GMP/open-book models and KPIs (target schedule adherence >90%) increase scrutiny.

Large programs yield 5–15% concessions; standardized bids raised shortlisted bids ~40%, and early contractor involvement cut expected cost overruns ~25% in 2024.

Over 60% of projects faced delays in 2024, driving LDs; ARCO mitigates via IP, permitting momentum, QA/QC and documented buffers.

| Metric | 2024 Value |

|---|---|

| Benchmarked project size | >$100M |

| Typical price concession | 5–15% |

| Shortlisted bids ↑ | ~40% |

| ECI reduces overruns | ~25% |

| Projects with delays | >60% |

| Target schedule adherence | >90% |

Same Document Delivered

Arco Construction Porter's Five Forces Analysis

This preview shows the exact Arco Construction Porter’s Five Forces analysis you'll receive upon purchase—fully written, formatted, and ready to download. It assesses supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable, data-driven conclusions. No placeholders or samples—what you see is the final deliverable and will be available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Arco Construction faces moderate buyer power, fragmented suppliers, and stiff rivalry from regional builders impacting margins. Potential new entrants and substitute materials pose emerging threats while regulatory hurdles shape project pipelines. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic recommendations tailored to Arco Construction.

Suppliers Bargaining Power

Specialized trades dependence

ARCO depends heavily on skilled subcontractors for MEP, concrete and specialty systems, concentrating supplier power where trade scarcity exists; construction employment exceeded pre‑pandemic levels in 2024 but skilled trades remain tight. Scarcity in these trades elevates bid prices and elongates schedules, increasing ARCO’s cost and timeline risk. Rigorous prequalification and long‑term partnering stabilize availability, while design‑build integration bundles scopes to reduce fragmentation and subcontractor leverage.

Key materials price volatility

Steel, concrete, lumber and HVAC equipment see cyclical price swings often ranging 10–30% historically, with 2024 still showing elevated volatility versus pre‑pandemic levels. Global supply shocks and freight swings (Baltic Dry Index history) can compress GMP margins by several percentage points on large projects. Early procurement and hedging clauses reduce exposure. Value engineering in design offsets cost spikes by optimizing material use.

OEM lead times and capacity

Elevators (20–30 weeks), medium-voltage switchgear (16–28 weeks) and rooftop units (8–20 weeks) commonly face extended 2024 lead times, making OEM capacity constraints a critical-path risk. ARCO’s front-loaded design enables submittals/releases earlier in the schedule. Alternate approvals add schedule flexibility and mitigate OEM bottlenecks.

Regional supplier concentration

Regional supplier concentration raises leverage where industrial and multifamily work clusters in major metros; about 3,600 ready‑mix plants nationwide (PCA, 2024) means local batch plants can command premium margins on tight jobs, while Arco can counter by sourcing multi‑region fabricators and planning logistics to pull from adjacent markets.

- Local batch plants: concentrated supply

- 3,600 ready‑mix plants (PCA 2024)

- Multi‑region vendors: increased competition

- Logistics planning: access adjacent markets

Contract terms and pass-through

Subcontractor risk-shift clauses materially lift Arco Construction bid pricing as subcontractors — supplying roughly 60–80% of direct trade value in 2024 — price contingency into quotes. Limited willingness to hold prices beyond short windows erodes revenue certainty. Escalation allowances and unit-rate schedules redistribute material and labour volatility, while clear scopes curtail change-order bargaining power.

- risk-shift

- price-hold

- escalation

- scope-clarity

Subcontractor concentration, material volatility and long lead times threaten GMP and schedule

ARCO faces concentrated supplier power: subcontractors supply 60–80% of direct trade value (2024) and skilled trades remain tight despite employment above pre‑pandemic levels. Material volatility (steel/concrete/lumber) historically 10–30% raises GMP risk; elevators 20–30w, switchgear 16–28w, RTUs 8–20w create critical‑path pressure. Mitigants: prequalification, early procurement, design‑build bundling.

| Item | 2024 metric | Impact |

|---|---|---|

| Subcontractor share | 60–80% | High price/schedule leverage |

| Ready‑mix plants | 3,600 (PCA 2024) | Local premium |

| Lead times | Elev 20–30w; SWG 16–28w; RTU 8–20w | Critical‑path risk |

| Material volatility | 10–30% | GMP margin compression |

What is included in the product

Tailored exclusively for Arco Construction, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and emerging threats shaping its pricing and profitability.

A concise one-sheet Porter's Five Forces for Arco Construction that highlights strategic pressures and relief points—ready to drop into decks; adjustable inputs let you model scenarios, reduce uncertainty, and speed confident decision-making.

Customers Bargaining Power

Sophisticated owner base

Industrial and commercial owners are experienced and highly price-sensitive, often benchmarking Arco against multiple design-builders on 2024 projects exceeding $100M. Transparent GMP and open-book models reduce scrutiny by providing line-item visibility and have been adopted across major tenders in 2024. Clear performance metrics—schedule adherence, cost variance, safety TRIR—and KPIs (targeted schedule adherence >90%) strengthen Arco’s credibility with sophisticated owners.

Project scale and pipeline

Large programs (typically >$5M) give buyers significant volume leverage, with 2024 procurement rounds commonly yielding 5–15% price concessions. Multi-site rollouts (10+ locations) increase demands for discounts and priority scheduling. ARCO can trade rate for continuity and predictability; master service agreements lock pipeline and stabilize margins.

Bid comparability

Owners solicit competitive proposals with standardized assumptions to enable bid comparability, driving price pressure when detailed alternates are included and often compressing margins; industry estimates in 2024 showed standardized bidding increased shortlisted bids by about 40%. Early collaboration shifts selection toward best value, with early contractor involvement reducing expected cost overruns by roughly 25% in 2024 studies. Differentiation in speed and delivery certainty breaks pure price comparisons and supports premium pricing for predictable schedules.

Switching costs and stage gates

Owners often switch pre-construction partners before final GMP, so low early-stage switching costs amplify buyer power; ARCO counters this with upfront design IP and permitting momentum that increase stickiness, while milestone-based commitments align incentives and reduce late-stage churn.

- Early switching: increases buyer leverage

- ARCO design IP: raises retention

- Permitting momentum: accelerates lock-in

- Milestones: align risks and payments

Performance guarantees

Owners push GMP/open-book; ECI trims overruns ~25%, delays >60%

Industrial owners are price-sensitive, benchmarking ARCO on 2024 projects >$100M; GMP/open-book models and KPIs (target schedule adherence >90%) increase scrutiny.

Large programs yield 5–15% concessions; standardized bids raised shortlisted bids ~40%, and early contractor involvement cut expected cost overruns ~25% in 2024.

Over 60% of projects faced delays in 2024, driving LDs; ARCO mitigates via IP, permitting momentum, QA/QC and documented buffers.

| Metric | 2024 Value |

|---|---|

| Benchmarked project size | >$100M |

| Typical price concession | 5–15% |

| Shortlisted bids ↑ | ~40% |

| ECI reduces overruns | ~25% |

| Projects with delays | >60% |

| Target schedule adherence | >90% |

Same Document Delivered

Arco Construction Porter's Five Forces Analysis

This preview shows the exact Arco Construction Porter’s Five Forces analysis you'll receive upon purchase—fully written, formatted, and ready to download. It assesses supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable, data-driven conclusions. No placeholders or samples—what you see is the final deliverable and will be available instantly after payment.