Arcus Biosciences Porter's Five Forces Analysis

From Overview to Strategy Blueprint

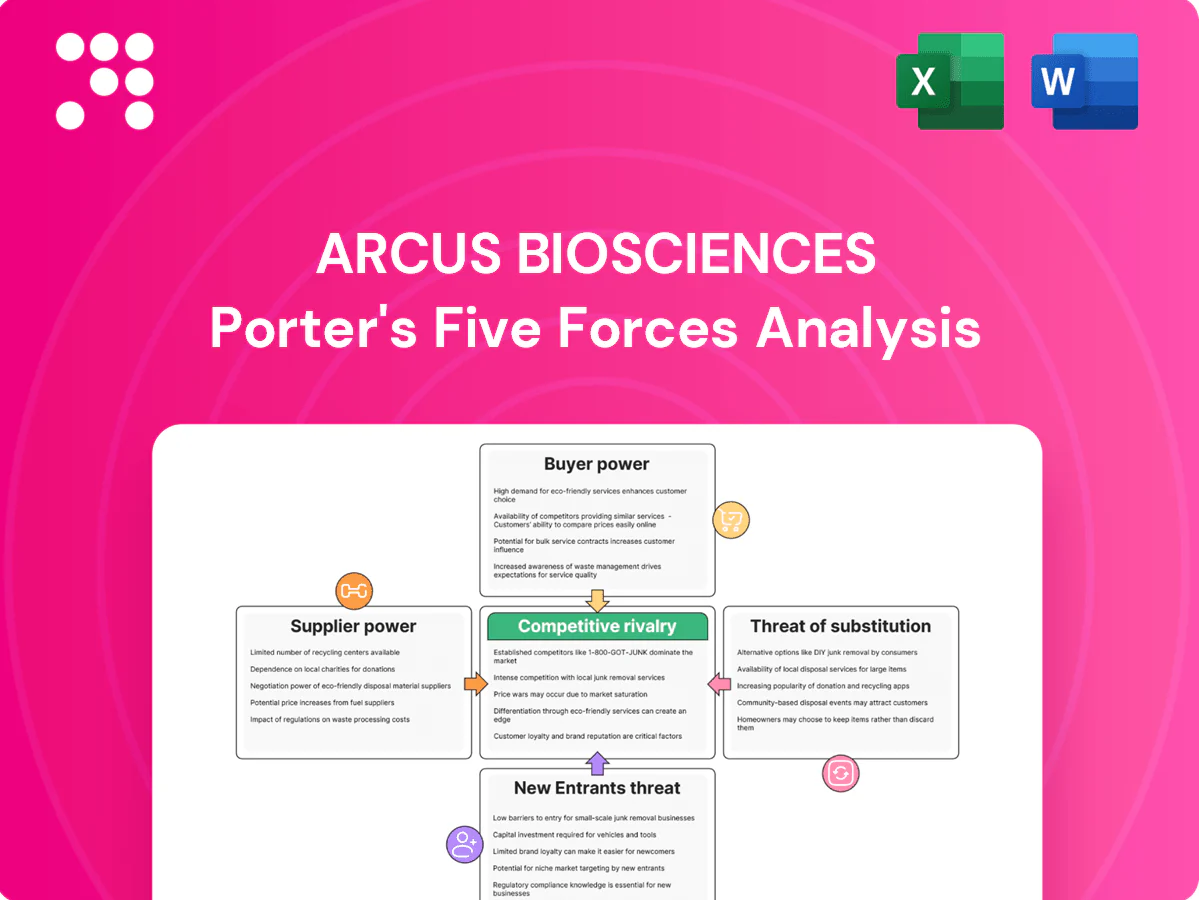

Arcus Biosciences faces high competitive rivalry from big pharma and biotech peers, moderate buyer power from payers, and supplier/partner leverage in specialized biologics manufacturing; threats from new entrants and substitutes are tempered by R&D complexity and pipeline differentiation, though regulatory and capital risks persist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arcus Biosciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated CRO/CMO reliance

Arcus relies on a limited pool of high-quality CROs/CMOs for complex biologics and small molecules; the global CRO/CMO market was roughly $65 billion in 2024, reflecting concentrated capacity. Capacity constraints or quality issues can delay trials and raise costs, with tech transfers often taking 6–12 months and costing millions. This concentration elevates supplier bargaining power and execution risk for Arcus.

Specialized biologics inputs

Proprietary cell lines, single-use bioreactors and GMP-grade reagents remain concentrated among a few suppliers, giving them pricing leverage. Lead times and qualification often exceed 12 weeks, amplifying supplier bargaining power and tightening terms. Industry up-cycles have produced acute scarcity and allocation; Arcus must dual-source and carry safety stock, increasing operating costs and working capital needs.

Cutting-edge diagnostics and assays

Biomarker testing, next-generation sequencing and companion diagnostics are now essential to immunotherapy trials, with the FDA having approved more than 40 companion diagnostics since 2014, concentrating supplier influence. Assay IP and platform lock-in (NGS panels, proprietary bioinformatics) increase switching costs, while custom assay validation adds time and regulatory burden that entrenches vendors. Co-development deals reduce upfront risk but create multi-year dependency through shared validation and revenue-sharing terms.

Skilled talent and KOL networks

Experienced immuno-oncology scientists, clinical operations staff, and KOLs remain scarce, with 2024 industry surveys reporting majority-facing recruitment challenges; compensation inflation and retention packages have risen markedly, squeezing R&D budgets and favoring the supplier labor market. Site relationships and investigator mindshare can reprioritize trial schedules, and talent scarcity increases supplier leverage over timelines and cost.

- Talent scarcity: higher bargaining power

- Compensation inflation: raises retention costs

- Site/KOL influence: shifts trial priority

Data, software, and AI platforms

Analytics, safety databases and eClinical systems are mission-critical for Arcus, and 21 CFR Part 11 remained an active FDA compliance requirement in 2024, raising validation and audit trail obligations that increase switching costs. Vendor ecosystems and limited data portability create technical stickiness, enabling suppliers of validated AI and software platforms to negotiate premium pricing and long-term contracts.

- Mission-critical: analytics, safety, eClinical

- Compliance: 21 CFR Part 11 (2024) increases validation costs

- Stickiness: vendor ecosystems limit portability

- Pricing power: validated platforms secure premium contracts

Concentrated CRO/CMO and NGS suppliers squeeze costs; $65B market pressure

Arcus faces elevated supplier power from concentrated CRO/CMO capacity, GMP reagent vendors, and diagnostic/NGS platform providers; the global CRO/CMO market was roughly $65 billion in 2024. Proprietary assays, validation timelines and 21 CFR Part 11 compliance raise switching costs. Talent and site/KOL scarcity further tighten timelines and increase costs.

| Supplier Type | Concentration / 2024 metric |

|---|---|

| CRO/CMO | $65B global market (2024) |

| Companion diagnostics/NGS | >40 FDA approvals since 2014 |

| Regulatory/software | 21 CFR Part 11 (2024) compliance |

What is included in the product

Tailored Porter's Five Forces analysis of Arcus Biosciences uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic barriers that shape its pricing, R&D positioning, and long-term profitability.

A concise, Arcus-specific Porter's Five Forces one-sheet that clarifies competitive pressures and therapeutic-pipeline risks for fast decision-making; customizable inputs and radar visualization make it easy to update scenarios and drop straight into pitch decks or executive reports.

Customers Bargaining Power

Payers demand clear value

Payers and HTA bodies demand robust overall survival, progression-free survival and quality-of-life gains to justify premium pricing for Arcus products. Comparator selection and ICER thresholds—commonly $100,000–$150,000 per QALY in the US and £20,000–£30,000 per QALY for NICE—set reimbursement ceilings. Major HTAs and insurers increasingly require post-approval real-world evidence, strengthening payer leverage in price and access negotiations.

Oncologists and centers influence uptake

Treatment guidelines and formulary committees gate clinical adoption and payer coverage, shaping uptake of Arcus assets; class-wide IO sales topped roughly $40 billion in 2024, reinforcing committee scrutiny. Physician preference for simplicity and manageable toxicity often tips choices among similar IOs. Academic centers demand compelling Phase III data and trial access. Post-approval this translates into meaningful buyer leverage on price and volume.

Pharma partners as pivotal buyers

As a clinical-stage company, Arcus routinely monetizes programs via licensing, co-development, or co-promotion agreements, leaving commercial upside subject to partner terms. Large pharma buyers extract leverage to push down upfronts, tether milestones to stringent endpoints, and restrict territories and indications. Because partners can walk away when data are marginal, Arcus faces concentrated buyer power that compresses deal economics and negotiation leverage.

Patients and advocacy groups

Patients and advocacy groups, though indirect buyers for Arcus Biosciences, shape trial design and access programs by pressuring for compassionate use and broader enrollment criteria, which raises development costs and can extend timelines; patient-reported outcomes increasingly affect payer and prescriber decisions, amplifying their indirect bargaining power.

- Influence: trial design & access

- Pressure: compassionate use, inclusive criteria

- Impact: costs and timelines

- Voice: patient-reported outcomes sway payers/prescribers

Hospital systems and GPOs

Hospital value analysis committees and GPOs, used by about 75% of US hospitals, push for protocol preferences and discounts that constrain pricing; GPO-negotiated discounts commonly range 20–30% for high-cost therapies. Site-administered oncology drugs face buy-and-bill economics scrutiny, with formulary and budget-impact models often delaying adoption by 6–12 months, reducing launch uptake and negotiating leverage for Arcus.

- GPO share ~75%

- Typical GPO discounts 20–30%

- Formulary decision lag 6–12 months

- Buy-and-bill scrutiny lowers pricing power

Payers, HTAs and GPOs squeeze pricing and access via ICER thresholds and GPO discounts

Payers, HTAs and GPOs exert strong leverage over Arcus through ICER thresholds (US $100–150k/QALY; NICE £20–30k/QALY), growing RWE demands and formulary gatekeeping. Large pharma partners and hospital buying groups compress deal economics and pricing (GPOs cover ~75% of US hospitals; typical discounts 20–30%). Physician and patient outcome preferences further constrain uptake and access.

| Metric | 2024 Value |

|---|---|

| IO class sales | $40B |

| GPO hospital share | ~75% |

| GPO discounts | 20–30% |

| Formulary lag | 6–12 months |

Full Version Awaits

Arcus Biosciences Porter's Five Forces Analysis

This Porter's Five Forces analysis for Arcus Biosciences evaluates competitive rivalry, supplier and buyer power, barriers to entry, and threats from substitutes, with clear strategic implications for oncology-focused biotech positioning. This preview is the exact, fully formatted document you’ll receive instantly after purchase.

From Overview to Strategy Blueprint

Arcus Biosciences faces high competitive rivalry from big pharma and biotech peers, moderate buyer power from payers, and supplier/partner leverage in specialized biologics manufacturing; threats from new entrants and substitutes are tempered by R&D complexity and pipeline differentiation, though regulatory and capital risks persist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arcus Biosciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated CRO/CMO reliance

Arcus relies on a limited pool of high-quality CROs/CMOs for complex biologics and small molecules; the global CRO/CMO market was roughly $65 billion in 2024, reflecting concentrated capacity. Capacity constraints or quality issues can delay trials and raise costs, with tech transfers often taking 6–12 months and costing millions. This concentration elevates supplier bargaining power and execution risk for Arcus.

Specialized biologics inputs

Proprietary cell lines, single-use bioreactors and GMP-grade reagents remain concentrated among a few suppliers, giving them pricing leverage. Lead times and qualification often exceed 12 weeks, amplifying supplier bargaining power and tightening terms. Industry up-cycles have produced acute scarcity and allocation; Arcus must dual-source and carry safety stock, increasing operating costs and working capital needs.

Cutting-edge diagnostics and assays

Biomarker testing, next-generation sequencing and companion diagnostics are now essential to immunotherapy trials, with the FDA having approved more than 40 companion diagnostics since 2014, concentrating supplier influence. Assay IP and platform lock-in (NGS panels, proprietary bioinformatics) increase switching costs, while custom assay validation adds time and regulatory burden that entrenches vendors. Co-development deals reduce upfront risk but create multi-year dependency through shared validation and revenue-sharing terms.

Skilled talent and KOL networks

Experienced immuno-oncology scientists, clinical operations staff, and KOLs remain scarce, with 2024 industry surveys reporting majority-facing recruitment challenges; compensation inflation and retention packages have risen markedly, squeezing R&D budgets and favoring the supplier labor market. Site relationships and investigator mindshare can reprioritize trial schedules, and talent scarcity increases supplier leverage over timelines and cost.

- Talent scarcity: higher bargaining power

- Compensation inflation: raises retention costs

- Site/KOL influence: shifts trial priority

Data, software, and AI platforms

Analytics, safety databases and eClinical systems are mission-critical for Arcus, and 21 CFR Part 11 remained an active FDA compliance requirement in 2024, raising validation and audit trail obligations that increase switching costs. Vendor ecosystems and limited data portability create technical stickiness, enabling suppliers of validated AI and software platforms to negotiate premium pricing and long-term contracts.

- Mission-critical: analytics, safety, eClinical

- Compliance: 21 CFR Part 11 (2024) increases validation costs

- Stickiness: vendor ecosystems limit portability

- Pricing power: validated platforms secure premium contracts

Concentrated CRO/CMO and NGS suppliers squeeze costs; $65B market pressure

Arcus faces elevated supplier power from concentrated CRO/CMO capacity, GMP reagent vendors, and diagnostic/NGS platform providers; the global CRO/CMO market was roughly $65 billion in 2024. Proprietary assays, validation timelines and 21 CFR Part 11 compliance raise switching costs. Talent and site/KOL scarcity further tighten timelines and increase costs.

| Supplier Type | Concentration / 2024 metric |

|---|---|

| CRO/CMO | $65B global market (2024) |

| Companion diagnostics/NGS | >40 FDA approvals since 2014 |

| Regulatory/software | 21 CFR Part 11 (2024) compliance |

What is included in the product

Tailored Porter's Five Forces analysis of Arcus Biosciences uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic barriers that shape its pricing, R&D positioning, and long-term profitability.

A concise, Arcus-specific Porter's Five Forces one-sheet that clarifies competitive pressures and therapeutic-pipeline risks for fast decision-making; customizable inputs and radar visualization make it easy to update scenarios and drop straight into pitch decks or executive reports.

Customers Bargaining Power

Payers demand clear value

Payers and HTA bodies demand robust overall survival, progression-free survival and quality-of-life gains to justify premium pricing for Arcus products. Comparator selection and ICER thresholds—commonly $100,000–$150,000 per QALY in the US and £20,000–£30,000 per QALY for NICE—set reimbursement ceilings. Major HTAs and insurers increasingly require post-approval real-world evidence, strengthening payer leverage in price and access negotiations.

Oncologists and centers influence uptake

Treatment guidelines and formulary committees gate clinical adoption and payer coverage, shaping uptake of Arcus assets; class-wide IO sales topped roughly $40 billion in 2024, reinforcing committee scrutiny. Physician preference for simplicity and manageable toxicity often tips choices among similar IOs. Academic centers demand compelling Phase III data and trial access. Post-approval this translates into meaningful buyer leverage on price and volume.

Pharma partners as pivotal buyers

As a clinical-stage company, Arcus routinely monetizes programs via licensing, co-development, or co-promotion agreements, leaving commercial upside subject to partner terms. Large pharma buyers extract leverage to push down upfronts, tether milestones to stringent endpoints, and restrict territories and indications. Because partners can walk away when data are marginal, Arcus faces concentrated buyer power that compresses deal economics and negotiation leverage.

Patients and advocacy groups

Patients and advocacy groups, though indirect buyers for Arcus Biosciences, shape trial design and access programs by pressuring for compassionate use and broader enrollment criteria, which raises development costs and can extend timelines; patient-reported outcomes increasingly affect payer and prescriber decisions, amplifying their indirect bargaining power.

- Influence: trial design & access

- Pressure: compassionate use, inclusive criteria

- Impact: costs and timelines

- Voice: patient-reported outcomes sway payers/prescribers

Hospital systems and GPOs

Hospital value analysis committees and GPOs, used by about 75% of US hospitals, push for protocol preferences and discounts that constrain pricing; GPO-negotiated discounts commonly range 20–30% for high-cost therapies. Site-administered oncology drugs face buy-and-bill economics scrutiny, with formulary and budget-impact models often delaying adoption by 6–12 months, reducing launch uptake and negotiating leverage for Arcus.

- GPO share ~75%

- Typical GPO discounts 20–30%

- Formulary decision lag 6–12 months

- Buy-and-bill scrutiny lowers pricing power

Payers, HTAs and GPOs squeeze pricing and access via ICER thresholds and GPO discounts

Payers, HTAs and GPOs exert strong leverage over Arcus through ICER thresholds (US $100–150k/QALY; NICE £20–30k/QALY), growing RWE demands and formulary gatekeeping. Large pharma partners and hospital buying groups compress deal economics and pricing (GPOs cover ~75% of US hospitals; typical discounts 20–30%). Physician and patient outcome preferences further constrain uptake and access.

| Metric | 2024 Value |

|---|---|

| IO class sales | $40B |

| GPO hospital share | ~75% |

| GPO discounts | 20–30% |

| Formulary lag | 6–12 months |

Full Version Awaits

Arcus Biosciences Porter's Five Forces Analysis

This Porter's Five Forces analysis for Arcus Biosciences evaluates competitive rivalry, supplier and buyer power, barriers to entry, and threats from substitutes, with clear strategic implications for oncology-focused biotech positioning. This preview is the exact, fully formatted document you’ll receive instantly after purchase.

Description

From Overview to Strategy Blueprint

Arcus Biosciences faces high competitive rivalry from big pharma and biotech peers, moderate buyer power from payers, and supplier/partner leverage in specialized biologics manufacturing; threats from new entrants and substitutes are tempered by R&D complexity and pipeline differentiation, though regulatory and capital risks persist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arcus Biosciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated CRO/CMO reliance

Arcus relies on a limited pool of high-quality CROs/CMOs for complex biologics and small molecules; the global CRO/CMO market was roughly $65 billion in 2024, reflecting concentrated capacity. Capacity constraints or quality issues can delay trials and raise costs, with tech transfers often taking 6–12 months and costing millions. This concentration elevates supplier bargaining power and execution risk for Arcus.

Specialized biologics inputs

Proprietary cell lines, single-use bioreactors and GMP-grade reagents remain concentrated among a few suppliers, giving them pricing leverage. Lead times and qualification often exceed 12 weeks, amplifying supplier bargaining power and tightening terms. Industry up-cycles have produced acute scarcity and allocation; Arcus must dual-source and carry safety stock, increasing operating costs and working capital needs.

Cutting-edge diagnostics and assays

Biomarker testing, next-generation sequencing and companion diagnostics are now essential to immunotherapy trials, with the FDA having approved more than 40 companion diagnostics since 2014, concentrating supplier influence. Assay IP and platform lock-in (NGS panels, proprietary bioinformatics) increase switching costs, while custom assay validation adds time and regulatory burden that entrenches vendors. Co-development deals reduce upfront risk but create multi-year dependency through shared validation and revenue-sharing terms.

Skilled talent and KOL networks

Experienced immuno-oncology scientists, clinical operations staff, and KOLs remain scarce, with 2024 industry surveys reporting majority-facing recruitment challenges; compensation inflation and retention packages have risen markedly, squeezing R&D budgets and favoring the supplier labor market. Site relationships and investigator mindshare can reprioritize trial schedules, and talent scarcity increases supplier leverage over timelines and cost.

- Talent scarcity: higher bargaining power

- Compensation inflation: raises retention costs

- Site/KOL influence: shifts trial priority

Data, software, and AI platforms

Analytics, safety databases and eClinical systems are mission-critical for Arcus, and 21 CFR Part 11 remained an active FDA compliance requirement in 2024, raising validation and audit trail obligations that increase switching costs. Vendor ecosystems and limited data portability create technical stickiness, enabling suppliers of validated AI and software platforms to negotiate premium pricing and long-term contracts.

- Mission-critical: analytics, safety, eClinical

- Compliance: 21 CFR Part 11 (2024) increases validation costs

- Stickiness: vendor ecosystems limit portability

- Pricing power: validated platforms secure premium contracts

Concentrated CRO/CMO and NGS suppliers squeeze costs; $65B market pressure

Arcus faces elevated supplier power from concentrated CRO/CMO capacity, GMP reagent vendors, and diagnostic/NGS platform providers; the global CRO/CMO market was roughly $65 billion in 2024. Proprietary assays, validation timelines and 21 CFR Part 11 compliance raise switching costs. Talent and site/KOL scarcity further tighten timelines and increase costs.

| Supplier Type | Concentration / 2024 metric |

|---|---|

| CRO/CMO | $65B global market (2024) |

| Companion diagnostics/NGS | >40 FDA approvals since 2014 |

| Regulatory/software | 21 CFR Part 11 (2024) compliance |

What is included in the product

Tailored Porter's Five Forces analysis of Arcus Biosciences uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic barriers that shape its pricing, R&D positioning, and long-term profitability.

A concise, Arcus-specific Porter's Five Forces one-sheet that clarifies competitive pressures and therapeutic-pipeline risks for fast decision-making; customizable inputs and radar visualization make it easy to update scenarios and drop straight into pitch decks or executive reports.

Customers Bargaining Power

Payers demand clear value

Payers and HTA bodies demand robust overall survival, progression-free survival and quality-of-life gains to justify premium pricing for Arcus products. Comparator selection and ICER thresholds—commonly $100,000–$150,000 per QALY in the US and £20,000–£30,000 per QALY for NICE—set reimbursement ceilings. Major HTAs and insurers increasingly require post-approval real-world evidence, strengthening payer leverage in price and access negotiations.

Oncologists and centers influence uptake

Treatment guidelines and formulary committees gate clinical adoption and payer coverage, shaping uptake of Arcus assets; class-wide IO sales topped roughly $40 billion in 2024, reinforcing committee scrutiny. Physician preference for simplicity and manageable toxicity often tips choices among similar IOs. Academic centers demand compelling Phase III data and trial access. Post-approval this translates into meaningful buyer leverage on price and volume.

Pharma partners as pivotal buyers

As a clinical-stage company, Arcus routinely monetizes programs via licensing, co-development, or co-promotion agreements, leaving commercial upside subject to partner terms. Large pharma buyers extract leverage to push down upfronts, tether milestones to stringent endpoints, and restrict territories and indications. Because partners can walk away when data are marginal, Arcus faces concentrated buyer power that compresses deal economics and negotiation leverage.

Patients and advocacy groups

Patients and advocacy groups, though indirect buyers for Arcus Biosciences, shape trial design and access programs by pressuring for compassionate use and broader enrollment criteria, which raises development costs and can extend timelines; patient-reported outcomes increasingly affect payer and prescriber decisions, amplifying their indirect bargaining power.

- Influence: trial design & access

- Pressure: compassionate use, inclusive criteria

- Impact: costs and timelines

- Voice: patient-reported outcomes sway payers/prescribers

Hospital systems and GPOs

Hospital value analysis committees and GPOs, used by about 75% of US hospitals, push for protocol preferences and discounts that constrain pricing; GPO-negotiated discounts commonly range 20–30% for high-cost therapies. Site-administered oncology drugs face buy-and-bill economics scrutiny, with formulary and budget-impact models often delaying adoption by 6–12 months, reducing launch uptake and negotiating leverage for Arcus.

- GPO share ~75%

- Typical GPO discounts 20–30%

- Formulary decision lag 6–12 months

- Buy-and-bill scrutiny lowers pricing power

Payers, HTAs and GPOs squeeze pricing and access via ICER thresholds and GPO discounts

Payers, HTAs and GPOs exert strong leverage over Arcus through ICER thresholds (US $100–150k/QALY; NICE £20–30k/QALY), growing RWE demands and formulary gatekeeping. Large pharma partners and hospital buying groups compress deal economics and pricing (GPOs cover ~75% of US hospitals; typical discounts 20–30%). Physician and patient outcome preferences further constrain uptake and access.

| Metric | 2024 Value |

|---|---|

| IO class sales | $40B |

| GPO hospital share | ~75% |

| GPO discounts | 20–30% |

| Formulary lag | 6–12 months |

Full Version Awaits

Arcus Biosciences Porter's Five Forces Analysis

This Porter's Five Forces analysis for Arcus Biosciences evaluates competitive rivalry, supplier and buyer power, barriers to entry, and threats from substitutes, with clear strategic implications for oncology-focused biotech positioning. This preview is the exact, fully formatted document you’ll receive instantly after purchase.