Arteria Networks Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Arteria Networks faces moderate competitive intensity driven by specialized network services, rising buyer bargaining power, and selective supplier influence, while scale and tech investment deter new entrants. Substitute threats are emerging from cloud-native equivalents. Strategic positioning hinges on innovation and partner leverage. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated network equipment vendors

Core fiber and routing gear is concentrated among a few global OEMs (Cisco, Huawei, Nokia, Juniper), giving suppliers leverage on price and lead times and raising certification/interoperability switching costs; Cisco alone reported about $62 billion revenue in FY2024, illustrating vendor scale. Arteria can mitigate via multi-vendor strategies, framework agreements and standardized interfaces, but advanced feature dependencies still risk roadmap lock-in.

Access to ducts, poles, and rights-of-way

Permitting bodies and utility pole owners control critical passive infrastructure, giving suppliers strong leverage; make-ready work for pole attachments commonly takes 3–12 months and can cost thousands of dollars per attachment. Limited alternatives in dense urban areas further strengthen supplier bargaining power, while long-term leases and regulatory constraints raise operating costs and slow deployment. Master access agreements help secure access but are often negotiated on terms unfavorable to network builders.

Wholesale fiber and backhaul providers

Where Arteria leases capacity, wholesale fiber and backhaul carriers can exert significant pricing power, especially on constrained routes. Dependency rises if only one or two routes provide required latency or diversity, increasing switching costs and outage risk. Term commitments and volume tiers commonly lower unit costs. Building owned routes remains capital-intensive; a single subsea cable often costs between 200 million and 500 million.

Data center and IX operators

Carrier-neutral data centers and IXs are critical for peering and enterprise hosting; operators like Equinix maintain 240+ global facilities (2024), concentrating demand in scarce prime metros where landlords command higher cross-connect and space fees. Long-term colocation contracts (commonly 3–10 years) restrict Arteria’s flexibility, while diversifying across facilities reduces supplier risk but raises operational complexity and capex.

- Concentration: prime metros scarce

- Fees: higher cross-connect/space pricing

- Contracts: 3–10 year lock-ins

- Diversification: lowers exposure, raises complexity

Cloud and software stack partners

Cloud and software stack partners (SD-WAN, security, cloud interconnect) shape bundled enterprise offers; the SD-WAN market reached about 3.5B in 2024 and global public cloud spend hit ~620B in 2024, giving vendors pricing leverage. Certification and revenue-share clauses (commonly 5–15% channel splits) compress Arteria margins, while deep integration raises switching costs and migration timelines by ~30–40%.

- multi-cloud 92% (2024)

- SD-WAN market 3.5B (2024)

- cloud spend ~620B (2024)

- channel splits 5–15%

Suppliers wield pricing power: routing and colocation vendors plus carriers control network costs

Suppliers hold strong leverage: core routing vendors (Cisco ~$62B FY2024) and Equinix (240+ facilities in 2024) concentrate hardware and colocation pricing; permitting/pole owners and wholesale carriers control essential passive routes (make-ready 3–12 months, thousands $; subsea build $200–500M). Cloud/SD-WAN vendors (SD-WAN $3.5B, cloud ~$620B in 2024) add pricing and integration lock‑in risk.

| Item | 2024 Data |

|---|---|

| Cisco revenue | $62B |

| Equinix facilities | 240+ |

| SD‑WAN market | $3.5B |

| Cloud spend | $620B |

What is included in the product

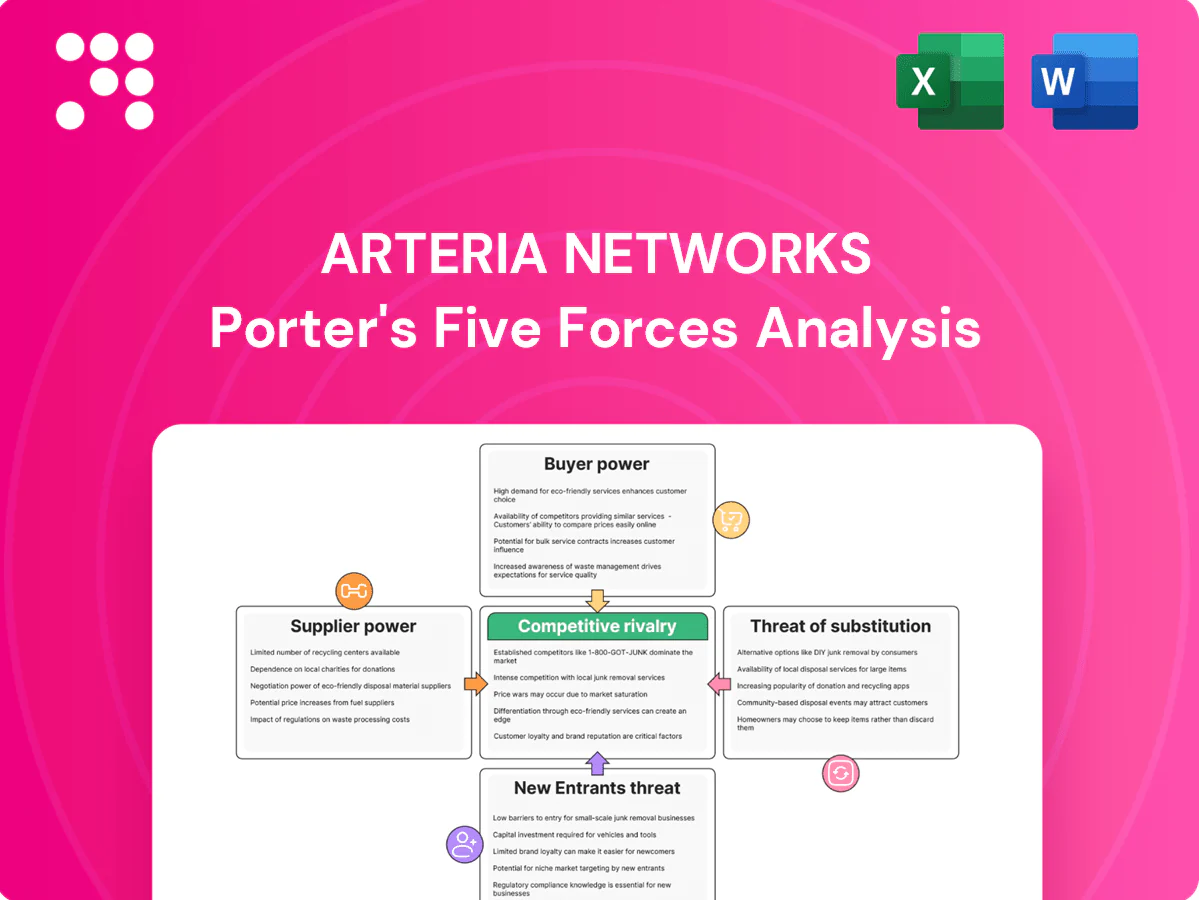

Tailored Porter's Five Forces analysis for Arteria Networks uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, plus disruptive and regulatory risks affecting pricing and profitability.

Clear one-sheet Porter's Five Forces for Arteria Networks—instantly highlights competitive pressures and relieves decision fatigue. Customize force levels, swap in your data, and drop the radar chart straight into pitch decks or reports for fast, board-ready insight.

Customers Bargaining Power

Enterprise clients with formal RFPs

Enterprise clients using formal RFPs run competitive tenders that intensify price pressure, with many contracts exceeding $1M and procurement cycles of 3–5 years. They demand bespoke SLAs, redundancy and financial penalties, shifting operational and financial risk to providers. Large contract size gives buyers clear negotiation leverage, and multi-year deals frequently trade lower unit pricing for volume or commitment guarantees.

Condominium associations and property managers

Condominium associations and property managers consolidate many end-users—typically buildings of 50–200+ units—creating concentrated buying power that lets a single contract sway thousands of subscribers. Building-wide agreements are often decided on small price or service differentials, making sales sensitive to marginal offers and SLAs. Churn risk is episodic at contract renewal, while bulk rates and amenity integration (concierge Wi‑Fi, managed services) materially increase lock-in and lifetime value.

Price transparency and service comparability

Published speeds and SLAs (commonly 99.9%–99.999% uptime targets in 2024) make vendor benchmarking straightforward, increasing buyer leverage and enabling rapid solicitation of counteroffers. Rapid comparisons drive price pressure, but Arteria can soften pure price focus through proven reliability, white‑glove support, and enterprise security certifications. Time‑limited trials and proof‑of‑performance reports support premium pricing by demonstrating measurable delivery.

Switching costs vary by segment

Enterprises face higher switching costs from reconfiguration, downtime risk and retraining; IP porting often requires 24–72 hours and redoing security policies can take weeks, raising friction for business clients.

Residential users can switch more easily where in-building infrastructure is open-access; contract break fees—commonly one to three months' charges—further deter churn.

- Enterprise: high reconfiguration, downtime, retraining

- IP porting: 24–72 hours; security policy rebuilds take weeks

- Residential: low if open-access

- Contract fees: typically 1–3 months' charges

Multi-homing and redundancy strategies

Many enterprises now dual-home with two ISPs, and Gartner 2024 reports about 60% of large organizations use multi-homing, diluting single-provider lock-in and keeping pricing pressure persistent at renewals. Providers must win on performance metrics and incident history—SLAs, mean time to repair, and latency reports increasingly decide deals. Offering value-added services (managed security, analytics) can raise share-of-wallet despite redundancy strategies.

- Multi-homing prevalence: ~60% (Gartner 2024)

- Renewal pricing pressure: persistent across enterprise renewals

- Competitive differentiators: SLA, MTTR, latency, incident history

- Upsell levers: managed services, security, analytics

Enterprise buyers squeeze margins; multi-homing and long cycles force value-adds like security SLAs

Buyers exert strong leverage: large enterprise RFPs (many >$1M, 3–5yr cycles) and building-wide condo contracts compress margins. Multi-homing (~60% of large orgs, Gartner 2024) sustains price pressure despite switching frictions (IP porting 24–72h, security rework weeks). Value-adds (managed security, SLAs 99.9–99.999% in 2024) are key to defend pricing.

| Metric | Value |

|---|---|

| Enterprise deal size | >$1M |

| Procurement cycle | 3–5 yrs |

| Multi-homing | ~60% (Gartner 2024) |

| IP porting | 24–72 h |

Full Version Awaits

Arteria Networks Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It contains a full Porter's Five Forces analysis of Arteria Networks covering supplier and buyer power, competitive rivalry, threat of new entrants, and substitute products, with evidence-based assessment. The file is fully formatted and ready to download the moment you buy. Use it for strategic planning, valuation, or investor briefing.

From Overview to Strategy Blueprint

Arteria Networks faces moderate competitive intensity driven by specialized network services, rising buyer bargaining power, and selective supplier influence, while scale and tech investment deter new entrants. Substitute threats are emerging from cloud-native equivalents. Strategic positioning hinges on innovation and partner leverage. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated network equipment vendors

Core fiber and routing gear is concentrated among a few global OEMs (Cisco, Huawei, Nokia, Juniper), giving suppliers leverage on price and lead times and raising certification/interoperability switching costs; Cisco alone reported about $62 billion revenue in FY2024, illustrating vendor scale. Arteria can mitigate via multi-vendor strategies, framework agreements and standardized interfaces, but advanced feature dependencies still risk roadmap lock-in.

Access to ducts, poles, and rights-of-way

Permitting bodies and utility pole owners control critical passive infrastructure, giving suppliers strong leverage; make-ready work for pole attachments commonly takes 3–12 months and can cost thousands of dollars per attachment. Limited alternatives in dense urban areas further strengthen supplier bargaining power, while long-term leases and regulatory constraints raise operating costs and slow deployment. Master access agreements help secure access but are often negotiated on terms unfavorable to network builders.

Wholesale fiber and backhaul providers

Where Arteria leases capacity, wholesale fiber and backhaul carriers can exert significant pricing power, especially on constrained routes. Dependency rises if only one or two routes provide required latency or diversity, increasing switching costs and outage risk. Term commitments and volume tiers commonly lower unit costs. Building owned routes remains capital-intensive; a single subsea cable often costs between 200 million and 500 million.

Data center and IX operators

Carrier-neutral data centers and IXs are critical for peering and enterprise hosting; operators like Equinix maintain 240+ global facilities (2024), concentrating demand in scarce prime metros where landlords command higher cross-connect and space fees. Long-term colocation contracts (commonly 3–10 years) restrict Arteria’s flexibility, while diversifying across facilities reduces supplier risk but raises operational complexity and capex.

- Concentration: prime metros scarce

- Fees: higher cross-connect/space pricing

- Contracts: 3–10 year lock-ins

- Diversification: lowers exposure, raises complexity

Cloud and software stack partners

Cloud and software stack partners (SD-WAN, security, cloud interconnect) shape bundled enterprise offers; the SD-WAN market reached about 3.5B in 2024 and global public cloud spend hit ~620B in 2024, giving vendors pricing leverage. Certification and revenue-share clauses (commonly 5–15% channel splits) compress Arteria margins, while deep integration raises switching costs and migration timelines by ~30–40%.

- multi-cloud 92% (2024)

- SD-WAN market 3.5B (2024)

- cloud spend ~620B (2024)

- channel splits 5–15%

Suppliers wield pricing power: routing and colocation vendors plus carriers control network costs

Suppliers hold strong leverage: core routing vendors (Cisco ~$62B FY2024) and Equinix (240+ facilities in 2024) concentrate hardware and colocation pricing; permitting/pole owners and wholesale carriers control essential passive routes (make-ready 3–12 months, thousands $; subsea build $200–500M). Cloud/SD-WAN vendors (SD-WAN $3.5B, cloud ~$620B in 2024) add pricing and integration lock‑in risk.

| Item | 2024 Data |

|---|---|

| Cisco revenue | $62B |

| Equinix facilities | 240+ |

| SD‑WAN market | $3.5B |

| Cloud spend | $620B |

What is included in the product

Tailored Porter's Five Forces analysis for Arteria Networks uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, plus disruptive and regulatory risks affecting pricing and profitability.

Clear one-sheet Porter's Five Forces for Arteria Networks—instantly highlights competitive pressures and relieves decision fatigue. Customize force levels, swap in your data, and drop the radar chart straight into pitch decks or reports for fast, board-ready insight.

Customers Bargaining Power

Enterprise clients with formal RFPs

Enterprise clients using formal RFPs run competitive tenders that intensify price pressure, with many contracts exceeding $1M and procurement cycles of 3–5 years. They demand bespoke SLAs, redundancy and financial penalties, shifting operational and financial risk to providers. Large contract size gives buyers clear negotiation leverage, and multi-year deals frequently trade lower unit pricing for volume or commitment guarantees.

Condominium associations and property managers

Condominium associations and property managers consolidate many end-users—typically buildings of 50–200+ units—creating concentrated buying power that lets a single contract sway thousands of subscribers. Building-wide agreements are often decided on small price or service differentials, making sales sensitive to marginal offers and SLAs. Churn risk is episodic at contract renewal, while bulk rates and amenity integration (concierge Wi‑Fi, managed services) materially increase lock-in and lifetime value.

Price transparency and service comparability

Published speeds and SLAs (commonly 99.9%–99.999% uptime targets in 2024) make vendor benchmarking straightforward, increasing buyer leverage and enabling rapid solicitation of counteroffers. Rapid comparisons drive price pressure, but Arteria can soften pure price focus through proven reliability, white‑glove support, and enterprise security certifications. Time‑limited trials and proof‑of‑performance reports support premium pricing by demonstrating measurable delivery.

Switching costs vary by segment

Enterprises face higher switching costs from reconfiguration, downtime risk and retraining; IP porting often requires 24–72 hours and redoing security policies can take weeks, raising friction for business clients.

Residential users can switch more easily where in-building infrastructure is open-access; contract break fees—commonly one to three months' charges—further deter churn.

- Enterprise: high reconfiguration, downtime, retraining

- IP porting: 24–72 hours; security policy rebuilds take weeks

- Residential: low if open-access

- Contract fees: typically 1–3 months' charges

Multi-homing and redundancy strategies

Many enterprises now dual-home with two ISPs, and Gartner 2024 reports about 60% of large organizations use multi-homing, diluting single-provider lock-in and keeping pricing pressure persistent at renewals. Providers must win on performance metrics and incident history—SLAs, mean time to repair, and latency reports increasingly decide deals. Offering value-added services (managed security, analytics) can raise share-of-wallet despite redundancy strategies.

- Multi-homing prevalence: ~60% (Gartner 2024)

- Renewal pricing pressure: persistent across enterprise renewals

- Competitive differentiators: SLA, MTTR, latency, incident history

- Upsell levers: managed services, security, analytics

Enterprise buyers squeeze margins; multi-homing and long cycles force value-adds like security SLAs

Buyers exert strong leverage: large enterprise RFPs (many >$1M, 3–5yr cycles) and building-wide condo contracts compress margins. Multi-homing (~60% of large orgs, Gartner 2024) sustains price pressure despite switching frictions (IP porting 24–72h, security rework weeks). Value-adds (managed security, SLAs 99.9–99.999% in 2024) are key to defend pricing.

| Metric | Value |

|---|---|

| Enterprise deal size | >$1M |

| Procurement cycle | 3–5 yrs |

| Multi-homing | ~60% (Gartner 2024) |

| IP porting | 24–72 h |

Full Version Awaits

Arteria Networks Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It contains a full Porter's Five Forces analysis of Arteria Networks covering supplier and buyer power, competitive rivalry, threat of new entrants, and substitute products, with evidence-based assessment. The file is fully formatted and ready to download the moment you buy. Use it for strategic planning, valuation, or investor briefing.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Arteria Networks faces moderate competitive intensity driven by specialized network services, rising buyer bargaining power, and selective supplier influence, while scale and tech investment deter new entrants. Substitute threats are emerging from cloud-native equivalents. Strategic positioning hinges on innovation and partner leverage. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated network equipment vendors

Core fiber and routing gear is concentrated among a few global OEMs (Cisco, Huawei, Nokia, Juniper), giving suppliers leverage on price and lead times and raising certification/interoperability switching costs; Cisco alone reported about $62 billion revenue in FY2024, illustrating vendor scale. Arteria can mitigate via multi-vendor strategies, framework agreements and standardized interfaces, but advanced feature dependencies still risk roadmap lock-in.

Access to ducts, poles, and rights-of-way

Permitting bodies and utility pole owners control critical passive infrastructure, giving suppliers strong leverage; make-ready work for pole attachments commonly takes 3–12 months and can cost thousands of dollars per attachment. Limited alternatives in dense urban areas further strengthen supplier bargaining power, while long-term leases and regulatory constraints raise operating costs and slow deployment. Master access agreements help secure access but are often negotiated on terms unfavorable to network builders.

Wholesale fiber and backhaul providers

Where Arteria leases capacity, wholesale fiber and backhaul carriers can exert significant pricing power, especially on constrained routes. Dependency rises if only one or two routes provide required latency or diversity, increasing switching costs and outage risk. Term commitments and volume tiers commonly lower unit costs. Building owned routes remains capital-intensive; a single subsea cable often costs between 200 million and 500 million.

Data center and IX operators

Carrier-neutral data centers and IXs are critical for peering and enterprise hosting; operators like Equinix maintain 240+ global facilities (2024), concentrating demand in scarce prime metros where landlords command higher cross-connect and space fees. Long-term colocation contracts (commonly 3–10 years) restrict Arteria’s flexibility, while diversifying across facilities reduces supplier risk but raises operational complexity and capex.

- Concentration: prime metros scarce

- Fees: higher cross-connect/space pricing

- Contracts: 3–10 year lock-ins

- Diversification: lowers exposure, raises complexity

Cloud and software stack partners

Cloud and software stack partners (SD-WAN, security, cloud interconnect) shape bundled enterprise offers; the SD-WAN market reached about 3.5B in 2024 and global public cloud spend hit ~620B in 2024, giving vendors pricing leverage. Certification and revenue-share clauses (commonly 5–15% channel splits) compress Arteria margins, while deep integration raises switching costs and migration timelines by ~30–40%.

- multi-cloud 92% (2024)

- SD-WAN market 3.5B (2024)

- cloud spend ~620B (2024)

- channel splits 5–15%

Suppliers wield pricing power: routing and colocation vendors plus carriers control network costs

Suppliers hold strong leverage: core routing vendors (Cisco ~$62B FY2024) and Equinix (240+ facilities in 2024) concentrate hardware and colocation pricing; permitting/pole owners and wholesale carriers control essential passive routes (make-ready 3–12 months, thousands $; subsea build $200–500M). Cloud/SD-WAN vendors (SD-WAN $3.5B, cloud ~$620B in 2024) add pricing and integration lock‑in risk.

| Item | 2024 Data |

|---|---|

| Cisco revenue | $62B |

| Equinix facilities | 240+ |

| SD‑WAN market | $3.5B |

| Cloud spend | $620B |

What is included in the product

Tailored Porter's Five Forces analysis for Arteria Networks uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, plus disruptive and regulatory risks affecting pricing and profitability.

Clear one-sheet Porter's Five Forces for Arteria Networks—instantly highlights competitive pressures and relieves decision fatigue. Customize force levels, swap in your data, and drop the radar chart straight into pitch decks or reports for fast, board-ready insight.

Customers Bargaining Power

Enterprise clients with formal RFPs

Enterprise clients using formal RFPs run competitive tenders that intensify price pressure, with many contracts exceeding $1M and procurement cycles of 3–5 years. They demand bespoke SLAs, redundancy and financial penalties, shifting operational and financial risk to providers. Large contract size gives buyers clear negotiation leverage, and multi-year deals frequently trade lower unit pricing for volume or commitment guarantees.

Condominium associations and property managers

Condominium associations and property managers consolidate many end-users—typically buildings of 50–200+ units—creating concentrated buying power that lets a single contract sway thousands of subscribers. Building-wide agreements are often decided on small price or service differentials, making sales sensitive to marginal offers and SLAs. Churn risk is episodic at contract renewal, while bulk rates and amenity integration (concierge Wi‑Fi, managed services) materially increase lock-in and lifetime value.

Price transparency and service comparability

Published speeds and SLAs (commonly 99.9%–99.999% uptime targets in 2024) make vendor benchmarking straightforward, increasing buyer leverage and enabling rapid solicitation of counteroffers. Rapid comparisons drive price pressure, but Arteria can soften pure price focus through proven reliability, white‑glove support, and enterprise security certifications. Time‑limited trials and proof‑of‑performance reports support premium pricing by demonstrating measurable delivery.

Switching costs vary by segment

Enterprises face higher switching costs from reconfiguration, downtime risk and retraining; IP porting often requires 24–72 hours and redoing security policies can take weeks, raising friction for business clients.

Residential users can switch more easily where in-building infrastructure is open-access; contract break fees—commonly one to three months' charges—further deter churn.

- Enterprise: high reconfiguration, downtime, retraining

- IP porting: 24–72 hours; security policy rebuilds take weeks

- Residential: low if open-access

- Contract fees: typically 1–3 months' charges

Multi-homing and redundancy strategies

Many enterprises now dual-home with two ISPs, and Gartner 2024 reports about 60% of large organizations use multi-homing, diluting single-provider lock-in and keeping pricing pressure persistent at renewals. Providers must win on performance metrics and incident history—SLAs, mean time to repair, and latency reports increasingly decide deals. Offering value-added services (managed security, analytics) can raise share-of-wallet despite redundancy strategies.

- Multi-homing prevalence: ~60% (Gartner 2024)

- Renewal pricing pressure: persistent across enterprise renewals

- Competitive differentiators: SLA, MTTR, latency, incident history

- Upsell levers: managed services, security, analytics

Enterprise buyers squeeze margins; multi-homing and long cycles force value-adds like security SLAs

Buyers exert strong leverage: large enterprise RFPs (many >$1M, 3–5yr cycles) and building-wide condo contracts compress margins. Multi-homing (~60% of large orgs, Gartner 2024) sustains price pressure despite switching frictions (IP porting 24–72h, security rework weeks). Value-adds (managed security, SLAs 99.9–99.999% in 2024) are key to defend pricing.

| Metric | Value |

|---|---|

| Enterprise deal size | >$1M |

| Procurement cycle | 3–5 yrs |

| Multi-homing | ~60% (Gartner 2024) |

| IP porting | 24–72 h |

Full Version Awaits

Arteria Networks Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It contains a full Porter's Five Forces analysis of Arteria Networks covering supplier and buyer power, competitive rivalry, threat of new entrants, and substitute products, with evidence-based assessment. The file is fully formatted and ready to download the moment you buy. Use it for strategic planning, valuation, or investor briefing.