Ascent Industries Porter's Five Forces Analysis

Don't Miss the Bigger Picture

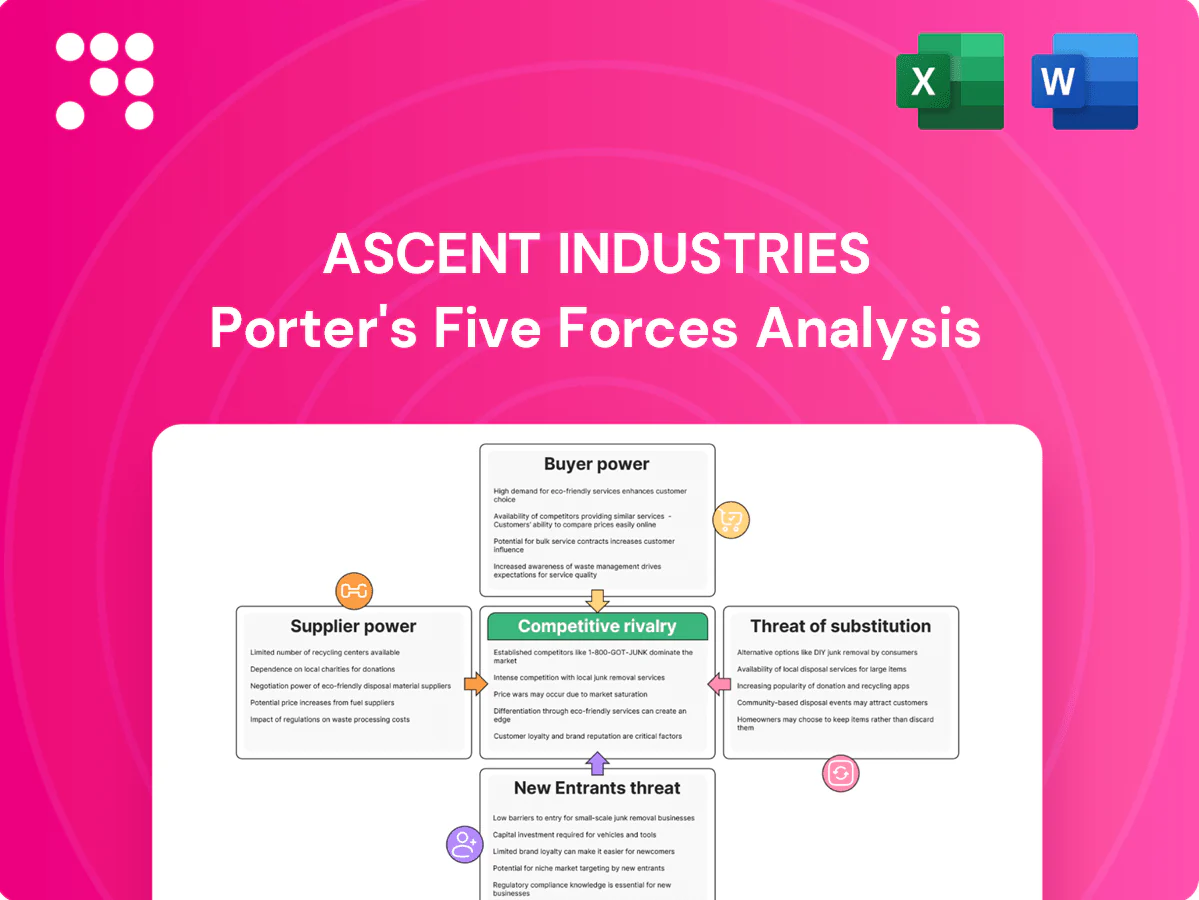

Ascent Industries faces intense competitive rivalry, evolving buyer power, concentrated supplier influence, and mounting substitute threats that could reshape margins and growth prospects. The threat of new entrants is moderated by capital and regulatory barriers, but innovation keeps pressure high. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ascent Industries’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented raw material sources

Ascent can multi-source steel coil, scrap, alloys and consumables from regional and global mills, tapping a supplier base that, per World Steel Association, includes over 2,000 producers worldwide to dilute single-supplier leverage. Fragmentation enables competitive bidding and hedging against outages, improving procurement flexibility. Specific grade and tight tolerance needs, however, narrow options for specialty products. Dual-qualifying suppliers preserves resilience and enforces price discipline.

Commodity price volatility

Input costs track global steel, energy and freight cycles, with steel spot swings ~25% in 2024, giving upstream mills significant leverage in tight markets. Index-linked contracts and hedging blunt shocks but do not prevent full pass-throughs, so volatility compresses margins on fixed-bid projects. Strategic inventory positioning and dynamic pricing proved critical to offset supplier-driven swings.

Quality and certification constraints

Infrastructure and energy end-markets demand certified inputs, and with roughly 1.2 million ISO 9001 certificates reported globally in 2024, switching costs for qualified mills are high. Suppliers holding rare metallurgy specs or niche certifications command price premiums and negotiation leverage. Qualification audits and approvals typically span 3–12 months, extending changeover timelines, so building a bench of pre-qualified sources materially reduces this supplier power.

Logistics and energy dependencies

Freight capacity shortages, port congestion and energy availability directly raise supplier delivery unreliability and costs; global container rates in 2024 averaged about 35% above 2019 levels and major port dwell times rose modestly versus 2022.

Mills located closer to Ascent plants or customers can extract location premia through lower last‑mile costs and faster replenishment.

Supply disruptions increase supplier bargaining power by creating lead‑time scarcity and price pass‑through.

Ascent's contracted transport agreements and route diversification reduce exposure and cap spot‑rate spikes.

- Freight rates: +35% vs 2019

- Port dwell times: higher vs 2022

- Energy costs: +~10% industrial 2024

- Mitigant: contracted transport, route diversity

Potential for upstream integration

Some peers vertically integrate into mini-mills and service centers, shifting supplier leverage toward captive upstream assets; electric-arc-furnace mills accounted for over 70% of U.S. steel output in 2024, underlining that trend. Ascent’s broad distribution footprint and scale let it negotiate volume-based rebates and allocate logistics to offset supplier bargaining. Multi-year offtake deals (commonly 3–7 years) trade committed volumes for price certainty, while joint grade/spec co-development raises mutual dependence and switching costs.

- Peers: mini-mill/service center integration — EAF >70% U.S. steel (2024)

- Ascent counter: scale + distribution → volume rebates/logistics leverage

- Contracts: 3–7 year offtake = price stability

- Co-development: deeper supplier lock-in

Multi-sourcing trims supplier leverage as 25% steel swings and +35% freight elevate upstream risk

Ascent dilutes supplier leverage via multi-sourcing and dual-qualifying suppliers but specialty grades retain supplier power. Steel spot swings ~25% in 2024 and freight +35% vs 2019 increase upstream leverage; EAFs >70% US output and 3–7 year offtakes give countervailing bargaining. Hedging, contracted transport and co‑development reduce pass‑through and changeover risk.

| Metric | 2024 value | Impact |

|---|---|---|

| Steel spot volatility | ~25% | High |

| Freight rates vs 2019 | +35% | Medium‑High |

| EAF share (US) | >70% | Reduces supplier power |

| Offtake length | 3–7 yrs | Mitigant |

What is included in the product

Tailored for Ascent Industries, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and emerging threats, delivering strategic insights and editable findings for investor materials, internal strategy decks, or academic work.

A one-sheet Porter's Five Forces for Ascent Industries that visualizes strategic pressure with an interactive spider chart and customizable force levels—ready to drop into decks, tweak for scenarios, and integrate into wider reports without macros.

Customers Bargaining Power

Large, sophisticated customers

EPCs, utilities and OEMs drive intense bidding that compresses supplier margins; 2024 procurement surveys report average bid discounts of 8–12% on repeat projects. High volume concentration—top buyers often represent 30–60% of supplier revenue—magnifies price and service pressure. Framework agreements trade 3–10% lower pricing for volume visibility, making relationship depth and KPI performance decisive in award decisions.

High price sensitivity in commoditized SKUs

Standard pipe, tube and common steel SKUs trade in highly transparent markets where buyers rapidly chase small price deltas; steel spot prices swung roughly 25% in 2024, amplifying churn risk. Buyers will switch suppliers for single-digit percentage savings, pressuring margins. Real-time quoting and inventory visibility can cut churn materially by improving responsiveness. Offering value-add services—processing, just-in-time delivery, technical support—is essential to defend margins.

Switching costs vary with customization

Custom fabrication, cut-to-length, and kitting raise switching costs through bespoke drawings, QA records, and fit-up standards, making vendor replacement operationally complex. As of 2024, supplier qualification cycles in energy and infrastructure commonly range 6–12 months, and certified supplier lists substantively slow vendor changes. Commodity items retain low switching costs, preserving buyer leverage, while bundled services increase lock-in and lifetime value.

Lead time and reliability as decision drivers

Projects penalize delays, so Ascent's reliable delivery often outweighs small price gaps; Gartner in 2024 reaffirmed OTIF as a primary procurement KPI. Buyers reward consistent OTIF and rapid replenishment with repeat orders; proximity and local stocking shrink alternatives while vendor-managed inventory embeds Ascent deeper into customer operations.

- OTIF importance: Gartner 2024

- Delays penalized: project contracts

- Proximity + stocking = switch cost

- VMI increases customer lock-in

Spec influence and design-in power

When buyers set specifications they commoditize supply and invite competitive bids. Early engineering engagement lets Ascent influence material choice and tolerances. Design assistance and technical support lock preferred positioning and reduce head-to-head price contests.

- Spec control: prevents pure commodity bidding

- Early-engage: shapes tolerances/materials

- Design-in: secures preferred supplier status

Buyers force 8-12% cuts; top buyers 30-60% revenue

Buyers (EPCs, utilities, OEMs) exert strong price pressure—2024 procurement surveys show repeat-project bid discounts of 8–12% and top buyers often account for 30–60% of supplier revenue. Transparent steel markets (spot swings ~25% in 2024) enable rapid switching for single-digit savings. Supplier qualification cycles run 6–12 months, while OTIF (Gartner 2024) and VMI increase lock-in.

| Metric | 2024 Value |

|---|---|

| Repeat bid discount | 8–12% |

| Top-buyer concentration | 30–60% |

| Steel spot volatility | ~25% |

| Qualification cycle | 6–12 months |

| Key KPI | OTIF (Gartner 2024) |

What You See Is What You Get

Ascent Industries Porter's Five Forces Analysis

This preview shows the exact Ascent Industries Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. It contains the complete forces assessment, supporting rationale, and actionable implications. What you see here is precisely what will be delivered upon payment.

Don't Miss the Bigger Picture

Ascent Industries faces intense competitive rivalry, evolving buyer power, concentrated supplier influence, and mounting substitute threats that could reshape margins and growth prospects. The threat of new entrants is moderated by capital and regulatory barriers, but innovation keeps pressure high. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ascent Industries’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented raw material sources

Ascent can multi-source steel coil, scrap, alloys and consumables from regional and global mills, tapping a supplier base that, per World Steel Association, includes over 2,000 producers worldwide to dilute single-supplier leverage. Fragmentation enables competitive bidding and hedging against outages, improving procurement flexibility. Specific grade and tight tolerance needs, however, narrow options for specialty products. Dual-qualifying suppliers preserves resilience and enforces price discipline.

Commodity price volatility

Input costs track global steel, energy and freight cycles, with steel spot swings ~25% in 2024, giving upstream mills significant leverage in tight markets. Index-linked contracts and hedging blunt shocks but do not prevent full pass-throughs, so volatility compresses margins on fixed-bid projects. Strategic inventory positioning and dynamic pricing proved critical to offset supplier-driven swings.

Quality and certification constraints

Infrastructure and energy end-markets demand certified inputs, and with roughly 1.2 million ISO 9001 certificates reported globally in 2024, switching costs for qualified mills are high. Suppliers holding rare metallurgy specs or niche certifications command price premiums and negotiation leverage. Qualification audits and approvals typically span 3–12 months, extending changeover timelines, so building a bench of pre-qualified sources materially reduces this supplier power.

Logistics and energy dependencies

Freight capacity shortages, port congestion and energy availability directly raise supplier delivery unreliability and costs; global container rates in 2024 averaged about 35% above 2019 levels and major port dwell times rose modestly versus 2022.

Mills located closer to Ascent plants or customers can extract location premia through lower last‑mile costs and faster replenishment.

Supply disruptions increase supplier bargaining power by creating lead‑time scarcity and price pass‑through.

Ascent's contracted transport agreements and route diversification reduce exposure and cap spot‑rate spikes.

- Freight rates: +35% vs 2019

- Port dwell times: higher vs 2022

- Energy costs: +~10% industrial 2024

- Mitigant: contracted transport, route diversity

Potential for upstream integration

Some peers vertically integrate into mini-mills and service centers, shifting supplier leverage toward captive upstream assets; electric-arc-furnace mills accounted for over 70% of U.S. steel output in 2024, underlining that trend. Ascent’s broad distribution footprint and scale let it negotiate volume-based rebates and allocate logistics to offset supplier bargaining. Multi-year offtake deals (commonly 3–7 years) trade committed volumes for price certainty, while joint grade/spec co-development raises mutual dependence and switching costs.

- Peers: mini-mill/service center integration — EAF >70% U.S. steel (2024)

- Ascent counter: scale + distribution → volume rebates/logistics leverage

- Contracts: 3–7 year offtake = price stability

- Co-development: deeper supplier lock-in

Multi-sourcing trims supplier leverage as 25% steel swings and +35% freight elevate upstream risk

Ascent dilutes supplier leverage via multi-sourcing and dual-qualifying suppliers but specialty grades retain supplier power. Steel spot swings ~25% in 2024 and freight +35% vs 2019 increase upstream leverage; EAFs >70% US output and 3–7 year offtakes give countervailing bargaining. Hedging, contracted transport and co‑development reduce pass‑through and changeover risk.

| Metric | 2024 value | Impact |

|---|---|---|

| Steel spot volatility | ~25% | High |

| Freight rates vs 2019 | +35% | Medium‑High |

| EAF share (US) | >70% | Reduces supplier power |

| Offtake length | 3–7 yrs | Mitigant |

What is included in the product

Tailored for Ascent Industries, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and emerging threats, delivering strategic insights and editable findings for investor materials, internal strategy decks, or academic work.

A one-sheet Porter's Five Forces for Ascent Industries that visualizes strategic pressure with an interactive spider chart and customizable force levels—ready to drop into decks, tweak for scenarios, and integrate into wider reports without macros.

Customers Bargaining Power

Large, sophisticated customers

EPCs, utilities and OEMs drive intense bidding that compresses supplier margins; 2024 procurement surveys report average bid discounts of 8–12% on repeat projects. High volume concentration—top buyers often represent 30–60% of supplier revenue—magnifies price and service pressure. Framework agreements trade 3–10% lower pricing for volume visibility, making relationship depth and KPI performance decisive in award decisions.

High price sensitivity in commoditized SKUs

Standard pipe, tube and common steel SKUs trade in highly transparent markets where buyers rapidly chase small price deltas; steel spot prices swung roughly 25% in 2024, amplifying churn risk. Buyers will switch suppliers for single-digit percentage savings, pressuring margins. Real-time quoting and inventory visibility can cut churn materially by improving responsiveness. Offering value-add services—processing, just-in-time delivery, technical support—is essential to defend margins.

Switching costs vary with customization

Custom fabrication, cut-to-length, and kitting raise switching costs through bespoke drawings, QA records, and fit-up standards, making vendor replacement operationally complex. As of 2024, supplier qualification cycles in energy and infrastructure commonly range 6–12 months, and certified supplier lists substantively slow vendor changes. Commodity items retain low switching costs, preserving buyer leverage, while bundled services increase lock-in and lifetime value.

Lead time and reliability as decision drivers

Projects penalize delays, so Ascent's reliable delivery often outweighs small price gaps; Gartner in 2024 reaffirmed OTIF as a primary procurement KPI. Buyers reward consistent OTIF and rapid replenishment with repeat orders; proximity and local stocking shrink alternatives while vendor-managed inventory embeds Ascent deeper into customer operations.

- OTIF importance: Gartner 2024

- Delays penalized: project contracts

- Proximity + stocking = switch cost

- VMI increases customer lock-in

Spec influence and design-in power

When buyers set specifications they commoditize supply and invite competitive bids. Early engineering engagement lets Ascent influence material choice and tolerances. Design assistance and technical support lock preferred positioning and reduce head-to-head price contests.

- Spec control: prevents pure commodity bidding

- Early-engage: shapes tolerances/materials

- Design-in: secures preferred supplier status

Buyers force 8-12% cuts; top buyers 30-60% revenue

Buyers (EPCs, utilities, OEMs) exert strong price pressure—2024 procurement surveys show repeat-project bid discounts of 8–12% and top buyers often account for 30–60% of supplier revenue. Transparent steel markets (spot swings ~25% in 2024) enable rapid switching for single-digit savings. Supplier qualification cycles run 6–12 months, while OTIF (Gartner 2024) and VMI increase lock-in.

| Metric | 2024 Value |

|---|---|

| Repeat bid discount | 8–12% |

| Top-buyer concentration | 30–60% |

| Steel spot volatility | ~25% |

| Qualification cycle | 6–12 months |

| Key KPI | OTIF (Gartner 2024) |

What You See Is What You Get

Ascent Industries Porter's Five Forces Analysis

This preview shows the exact Ascent Industries Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. It contains the complete forces assessment, supporting rationale, and actionable implications. What you see here is precisely what will be delivered upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ascent Industries faces intense competitive rivalry, evolving buyer power, concentrated supplier influence, and mounting substitute threats that could reshape margins and growth prospects. The threat of new entrants is moderated by capital and regulatory barriers, but innovation keeps pressure high. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ascent Industries’s competitive dynamics in detail.

Suppliers Bargaining Power

Fragmented raw material sources

Ascent can multi-source steel coil, scrap, alloys and consumables from regional and global mills, tapping a supplier base that, per World Steel Association, includes over 2,000 producers worldwide to dilute single-supplier leverage. Fragmentation enables competitive bidding and hedging against outages, improving procurement flexibility. Specific grade and tight tolerance needs, however, narrow options for specialty products. Dual-qualifying suppliers preserves resilience and enforces price discipline.

Commodity price volatility

Input costs track global steel, energy and freight cycles, with steel spot swings ~25% in 2024, giving upstream mills significant leverage in tight markets. Index-linked contracts and hedging blunt shocks but do not prevent full pass-throughs, so volatility compresses margins on fixed-bid projects. Strategic inventory positioning and dynamic pricing proved critical to offset supplier-driven swings.

Quality and certification constraints

Infrastructure and energy end-markets demand certified inputs, and with roughly 1.2 million ISO 9001 certificates reported globally in 2024, switching costs for qualified mills are high. Suppliers holding rare metallurgy specs or niche certifications command price premiums and negotiation leverage. Qualification audits and approvals typically span 3–12 months, extending changeover timelines, so building a bench of pre-qualified sources materially reduces this supplier power.

Logistics and energy dependencies

Freight capacity shortages, port congestion and energy availability directly raise supplier delivery unreliability and costs; global container rates in 2024 averaged about 35% above 2019 levels and major port dwell times rose modestly versus 2022.

Mills located closer to Ascent plants or customers can extract location premia through lower last‑mile costs and faster replenishment.

Supply disruptions increase supplier bargaining power by creating lead‑time scarcity and price pass‑through.

Ascent's contracted transport agreements and route diversification reduce exposure and cap spot‑rate spikes.

- Freight rates: +35% vs 2019

- Port dwell times: higher vs 2022

- Energy costs: +~10% industrial 2024

- Mitigant: contracted transport, route diversity

Potential for upstream integration

Some peers vertically integrate into mini-mills and service centers, shifting supplier leverage toward captive upstream assets; electric-arc-furnace mills accounted for over 70% of U.S. steel output in 2024, underlining that trend. Ascent’s broad distribution footprint and scale let it negotiate volume-based rebates and allocate logistics to offset supplier bargaining. Multi-year offtake deals (commonly 3–7 years) trade committed volumes for price certainty, while joint grade/spec co-development raises mutual dependence and switching costs.

- Peers: mini-mill/service center integration — EAF >70% U.S. steel (2024)

- Ascent counter: scale + distribution → volume rebates/logistics leverage

- Contracts: 3–7 year offtake = price stability

- Co-development: deeper supplier lock-in

Multi-sourcing trims supplier leverage as 25% steel swings and +35% freight elevate upstream risk

Ascent dilutes supplier leverage via multi-sourcing and dual-qualifying suppliers but specialty grades retain supplier power. Steel spot swings ~25% in 2024 and freight +35% vs 2019 increase upstream leverage; EAFs >70% US output and 3–7 year offtakes give countervailing bargaining. Hedging, contracted transport and co‑development reduce pass‑through and changeover risk.

| Metric | 2024 value | Impact |

|---|---|---|

| Steel spot volatility | ~25% | High |

| Freight rates vs 2019 | +35% | Medium‑High |

| EAF share (US) | >70% | Reduces supplier power |

| Offtake length | 3–7 yrs | Mitigant |

What is included in the product

Tailored for Ascent Industries, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and emerging threats, delivering strategic insights and editable findings for investor materials, internal strategy decks, or academic work.

A one-sheet Porter's Five Forces for Ascent Industries that visualizes strategic pressure with an interactive spider chart and customizable force levels—ready to drop into decks, tweak for scenarios, and integrate into wider reports without macros.

Customers Bargaining Power

Large, sophisticated customers

EPCs, utilities and OEMs drive intense bidding that compresses supplier margins; 2024 procurement surveys report average bid discounts of 8–12% on repeat projects. High volume concentration—top buyers often represent 30–60% of supplier revenue—magnifies price and service pressure. Framework agreements trade 3–10% lower pricing for volume visibility, making relationship depth and KPI performance decisive in award decisions.

High price sensitivity in commoditized SKUs

Standard pipe, tube and common steel SKUs trade in highly transparent markets where buyers rapidly chase small price deltas; steel spot prices swung roughly 25% in 2024, amplifying churn risk. Buyers will switch suppliers for single-digit percentage savings, pressuring margins. Real-time quoting and inventory visibility can cut churn materially by improving responsiveness. Offering value-add services—processing, just-in-time delivery, technical support—is essential to defend margins.

Switching costs vary with customization

Custom fabrication, cut-to-length, and kitting raise switching costs through bespoke drawings, QA records, and fit-up standards, making vendor replacement operationally complex. As of 2024, supplier qualification cycles in energy and infrastructure commonly range 6–12 months, and certified supplier lists substantively slow vendor changes. Commodity items retain low switching costs, preserving buyer leverage, while bundled services increase lock-in and lifetime value.

Lead time and reliability as decision drivers

Projects penalize delays, so Ascent's reliable delivery often outweighs small price gaps; Gartner in 2024 reaffirmed OTIF as a primary procurement KPI. Buyers reward consistent OTIF and rapid replenishment with repeat orders; proximity and local stocking shrink alternatives while vendor-managed inventory embeds Ascent deeper into customer operations.

- OTIF importance: Gartner 2024

- Delays penalized: project contracts

- Proximity + stocking = switch cost

- VMI increases customer lock-in

Spec influence and design-in power

When buyers set specifications they commoditize supply and invite competitive bids. Early engineering engagement lets Ascent influence material choice and tolerances. Design assistance and technical support lock preferred positioning and reduce head-to-head price contests.

- Spec control: prevents pure commodity bidding

- Early-engage: shapes tolerances/materials

- Design-in: secures preferred supplier status

Buyers force 8-12% cuts; top buyers 30-60% revenue

Buyers (EPCs, utilities, OEMs) exert strong price pressure—2024 procurement surveys show repeat-project bid discounts of 8–12% and top buyers often account for 30–60% of supplier revenue. Transparent steel markets (spot swings ~25% in 2024) enable rapid switching for single-digit savings. Supplier qualification cycles run 6–12 months, while OTIF (Gartner 2024) and VMI increase lock-in.

| Metric | 2024 Value |

|---|---|

| Repeat bid discount | 8–12% |

| Top-buyer concentration | 30–60% |

| Steel spot volatility | ~25% |

| Qualification cycle | 6–12 months |

| Key KPI | OTIF (Gartner 2024) |

What You See Is What You Get

Ascent Industries Porter's Five Forces Analysis

This preview shows the exact Ascent Industries Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for immediate download and use. It contains the complete forces assessment, supporting rationale, and actionable implications. What you see here is precisely what will be delivered upon payment.