Ascom Porter's Five Forces Analysis

Don't Miss the Bigger Picture

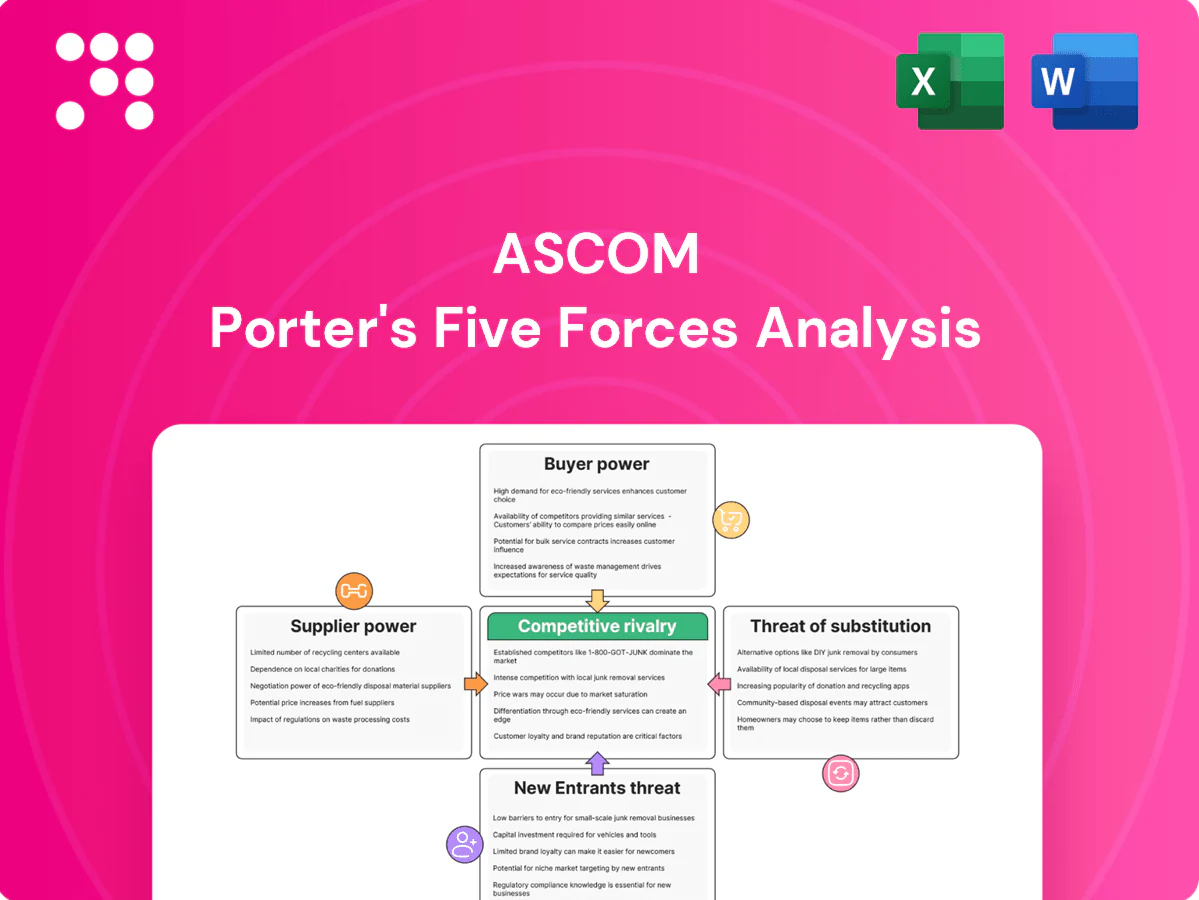

Ascom faces moderate buyer power, niche supplier dependencies, and intense rivalry in healthcare communications, with emerging substitutes and selective entry barriers shaping its outlook. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ascom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized radio and sensor components

Ascom depends on niche RF modules, sensors and low-power chipsets with few qualified vendors, concentrating supply and raising switching costs and lead times.

Vendors offering unique specs or medical/industrial certifications therefore gain pricing and delivery leverage over Ascom.

Dual-sourcing and design-for-alternatives reduce this supplier power but cannot fully eliminate certification and integration barriers.

Proprietary software and middleware dependencies

Proprietary software and middleware dependencies give suppliers outsized leverage over Ascom because core platforms rely on third‑party libraries, OSes, or licensed middleware, and in 2024 vendors still control upgrades, security patches and roadmap access. This control creates lock‑in and pricing power that can increase TCO and margin pressure. Negotiating enterprise agreements and pushing open standards reduces that supplier risk.

Wireless infrastructure and certification partners

Compliance with healthcare, RF and safety standards relies on accredited labs; ILAC membership exceeded 100 economies in 2024, highlighting limited official accreditation capacity that can create bottlenecks and premium testing pricing. Certification schedules often dictate product launch timing, so Ascom mitigates risk via strategic partnerships and early booking of lab slots to smooth timelines and costs.

Contract manufacturers and EMS providers

Contract manufacturers and EMS providers with ruggedized device and base-station expertise command leverage: global EMS revenue reached about $575 billion in 2024 and capacity utilization spikes above 85% during supply shortages, allowing preferential component allocation to higher‑margin customers.

Quality yields and NPI throughput directly affect Ascom margins; lower yields raise COGS while fast NPI secures launch windows. Long‑term volume commitments win priority and 1–3% better pricing or allocation in constrained periods.

- EMS market 2024 ~ $575B

- Utilization >85% in shortages

- NPI throughput and yields drive margins

- Long‑term commits → priority + ~1–3% better terms

Cloud and cybersecurity vendors

Ascom’s software and managed services rely on cloud and cybersecurity vendors, with market concentration high (2024 market shares: AWS ~33%, Microsoft Azure ~23%, Google Cloud ~11%), which gives suppliers pricing leverage; usage-based pricing and added compliance tooling can materially raise OPEX. Data residency and healthcare regulations increase switching friction, while multi-cloud architectures and strengthened internal security teams help rebalance supplier power.

- High cloud concentration: AWS/Azure/GCP ~33%/23%/11% (2024)

- Usage-based billing increases OPEX risk

- Data residency and healthcare compliance raise switching costs

- Multi-cloud + internal security reduce supplier leverage

Supply risk: EMS >85%, AWS 33% — dual‑source, multi‑cloud

Ascom faces concentrated suppliers for RF modules, certified testing and EMS, giving vendors pricing and allocation leverage; EMS market ~ $575B (2024) and utilization spikes >85% tighten access. Cloud concentration (AWS 33%, Azure 23%, GCP 11% in 2024) raises OPEX and switching friction for healthcare workloads. Mitigations: dual‑sourcing, long‑term commits (≈1–3% better terms), multi‑cloud and early certification bookings.

| Metric | 2024 |

|---|---|

| EMS market | $575B |

| EMS utilization | >85% (shortages) |

| Cloud share | AWS 33% / AZ 23% / GCP 11% |

| ILAC membership | >100 economies |

| Long‑term commit benefit | ≈1–3% better terms |

What is included in the product

Tailored Porter's Five Forces analysis for Ascom that uncovers key drivers of competition, customer influence, supplier power, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Practical insights support strategic decisions, investor materials, and editable reports for business planning and internal strategy.

Concise Porter's Five Forces for Ascom—crystal-clear force ratings and a radar chart to pinpoint competitive pain points, prioritize strategic responses, and drop straight into decks or dashboards.

Customers Bargaining Power

Large hospital systems and GPOs

Large health networks and GPOs aggregate demand and negotiate aggressively, with leading U.S. GPOs collectively managing over $200 billion in annual purchasing (2024), driving strong leverage for volume discounts, extended warranties and integration services. Vendor lists and tender processes intensify price pressure, so demonstrating total cost-of-ownership savings is critical to offset pure price focus.

High switching and integration costs

Once deployed, Ascom workflows embed across clinical units and EHRs, creating switching costs that industry reports in 2024 place commonly in the $500k–$5M range and materially reduce buyer churn. Buyers still extract concessions—renewal negotiations typically yield 5–10% price reductions—while demanding higher service and bespoke terms. Strong SLA performance (>90% uptime/response metrics) preserves pricing integrity and limits discount pressure.

Demand for interoperability and open APIs

Customers demand seamless integration with EHRs, nurse call, RTLS and alarm systems, driven by 21st Century Cures Act API requirements and near-universal EHR adoption (about 96% of US acute hospitals by 2024). Failure to interoperate leads to price pressure or outright disqualification; buyers require proofs, certifications and reference sites. Investing in certified connectors and standards demonstrably raises win rates and reduces price erosion.

Outcome-based procurement focus

Global tendering and long sales cycles

Public hospitals run formal RFPs with strict scoring matrices and budget caps; in 2024 many tenders exceed 12 months, which advantages incumbents, compresses margins and lets buyers leverage competing bids to extract discounts.

- Incumbent retention: higher win rates for current suppliers

- Sales cycle: tenders commonly >12 months (2024)

- Margin pressure: frequent price concessions

- Mitigation: early stakeholder mapping and clear solution differentiation

GPO leverage >$200B and 96% EHR adoption lock incumbents, compressing margins

Large GPOs drive leverage (>$200B purchasing, 2024), buyers push 5–10% renewal discounts; switching costs (reported $500k–$5M) and >90% SLA uptime defend pricing. EHR integration is critical (96% US acute hospital adoption, 2024); tenders commonly exceed 12 months, favoring incumbents and compressing margins.

| Metric | 2024 Value |

|---|---|

| GPO purchasing | $200B+ |

| EHR adoption (US acute) | 96% |

| Switching cost range | $500k–$5M |

| Renewal discounts | 5–10% |

| Tender length | >12 months |

What You See Is What You Get

Ascom Porter's Five Forces Analysis

You're looking at the actual Ascom Porter's Five Forces Analysis document. This preview is the exact file you'll receive immediately after purchase—fully formatted, complete and ready to use. No mockups or placeholders; once you buy you'll get instant access to this precise deliverable for your analysis and decision-making.

Don't Miss the Bigger Picture

Ascom faces moderate buyer power, niche supplier dependencies, and intense rivalry in healthcare communications, with emerging substitutes and selective entry barriers shaping its outlook. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ascom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized radio and sensor components

Ascom depends on niche RF modules, sensors and low-power chipsets with few qualified vendors, concentrating supply and raising switching costs and lead times.

Vendors offering unique specs or medical/industrial certifications therefore gain pricing and delivery leverage over Ascom.

Dual-sourcing and design-for-alternatives reduce this supplier power but cannot fully eliminate certification and integration barriers.

Proprietary software and middleware dependencies

Proprietary software and middleware dependencies give suppliers outsized leverage over Ascom because core platforms rely on third‑party libraries, OSes, or licensed middleware, and in 2024 vendors still control upgrades, security patches and roadmap access. This control creates lock‑in and pricing power that can increase TCO and margin pressure. Negotiating enterprise agreements and pushing open standards reduces that supplier risk.

Wireless infrastructure and certification partners

Compliance with healthcare, RF and safety standards relies on accredited labs; ILAC membership exceeded 100 economies in 2024, highlighting limited official accreditation capacity that can create bottlenecks and premium testing pricing. Certification schedules often dictate product launch timing, so Ascom mitigates risk via strategic partnerships and early booking of lab slots to smooth timelines and costs.

Contract manufacturers and EMS providers

Contract manufacturers and EMS providers with ruggedized device and base-station expertise command leverage: global EMS revenue reached about $575 billion in 2024 and capacity utilization spikes above 85% during supply shortages, allowing preferential component allocation to higher‑margin customers.

Quality yields and NPI throughput directly affect Ascom margins; lower yields raise COGS while fast NPI secures launch windows. Long‑term volume commitments win priority and 1–3% better pricing or allocation in constrained periods.

- EMS market 2024 ~ $575B

- Utilization >85% in shortages

- NPI throughput and yields drive margins

- Long‑term commits → priority + ~1–3% better terms

Cloud and cybersecurity vendors

Ascom’s software and managed services rely on cloud and cybersecurity vendors, with market concentration high (2024 market shares: AWS ~33%, Microsoft Azure ~23%, Google Cloud ~11%), which gives suppliers pricing leverage; usage-based pricing and added compliance tooling can materially raise OPEX. Data residency and healthcare regulations increase switching friction, while multi-cloud architectures and strengthened internal security teams help rebalance supplier power.

- High cloud concentration: AWS/Azure/GCP ~33%/23%/11% (2024)

- Usage-based billing increases OPEX risk

- Data residency and healthcare compliance raise switching costs

- Multi-cloud + internal security reduce supplier leverage

Supply risk: EMS >85%, AWS 33% — dual‑source, multi‑cloud

Ascom faces concentrated suppliers for RF modules, certified testing and EMS, giving vendors pricing and allocation leverage; EMS market ~ $575B (2024) and utilization spikes >85% tighten access. Cloud concentration (AWS 33%, Azure 23%, GCP 11% in 2024) raises OPEX and switching friction for healthcare workloads. Mitigations: dual‑sourcing, long‑term commits (≈1–3% better terms), multi‑cloud and early certification bookings.

| Metric | 2024 |

|---|---|

| EMS market | $575B |

| EMS utilization | >85% (shortages) |

| Cloud share | AWS 33% / AZ 23% / GCP 11% |

| ILAC membership | >100 economies |

| Long‑term commit benefit | ≈1–3% better terms |

What is included in the product

Tailored Porter's Five Forces analysis for Ascom that uncovers key drivers of competition, customer influence, supplier power, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Practical insights support strategic decisions, investor materials, and editable reports for business planning and internal strategy.

Concise Porter's Five Forces for Ascom—crystal-clear force ratings and a radar chart to pinpoint competitive pain points, prioritize strategic responses, and drop straight into decks or dashboards.

Customers Bargaining Power

Large hospital systems and GPOs

Large health networks and GPOs aggregate demand and negotiate aggressively, with leading U.S. GPOs collectively managing over $200 billion in annual purchasing (2024), driving strong leverage for volume discounts, extended warranties and integration services. Vendor lists and tender processes intensify price pressure, so demonstrating total cost-of-ownership savings is critical to offset pure price focus.

High switching and integration costs

Once deployed, Ascom workflows embed across clinical units and EHRs, creating switching costs that industry reports in 2024 place commonly in the $500k–$5M range and materially reduce buyer churn. Buyers still extract concessions—renewal negotiations typically yield 5–10% price reductions—while demanding higher service and bespoke terms. Strong SLA performance (>90% uptime/response metrics) preserves pricing integrity and limits discount pressure.

Demand for interoperability and open APIs

Customers demand seamless integration with EHRs, nurse call, RTLS and alarm systems, driven by 21st Century Cures Act API requirements and near-universal EHR adoption (about 96% of US acute hospitals by 2024). Failure to interoperate leads to price pressure or outright disqualification; buyers require proofs, certifications and reference sites. Investing in certified connectors and standards demonstrably raises win rates and reduces price erosion.

Outcome-based procurement focus

Global tendering and long sales cycles

Public hospitals run formal RFPs with strict scoring matrices and budget caps; in 2024 many tenders exceed 12 months, which advantages incumbents, compresses margins and lets buyers leverage competing bids to extract discounts.

- Incumbent retention: higher win rates for current suppliers

- Sales cycle: tenders commonly >12 months (2024)

- Margin pressure: frequent price concessions

- Mitigation: early stakeholder mapping and clear solution differentiation

GPO leverage >$200B and 96% EHR adoption lock incumbents, compressing margins

Large GPOs drive leverage (>$200B purchasing, 2024), buyers push 5–10% renewal discounts; switching costs (reported $500k–$5M) and >90% SLA uptime defend pricing. EHR integration is critical (96% US acute hospital adoption, 2024); tenders commonly exceed 12 months, favoring incumbents and compressing margins.

| Metric | 2024 Value |

|---|---|

| GPO purchasing | $200B+ |

| EHR adoption (US acute) | 96% |

| Switching cost range | $500k–$5M |

| Renewal discounts | 5–10% |

| Tender length | >12 months |

What You See Is What You Get

Ascom Porter's Five Forces Analysis

You're looking at the actual Ascom Porter's Five Forces Analysis document. This preview is the exact file you'll receive immediately after purchase—fully formatted, complete and ready to use. No mockups or placeholders; once you buy you'll get instant access to this precise deliverable for your analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ascom faces moderate buyer power, niche supplier dependencies, and intense rivalry in healthcare communications, with emerging substitutes and selective entry barriers shaping its outlook. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Ascom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized radio and sensor components

Ascom depends on niche RF modules, sensors and low-power chipsets with few qualified vendors, concentrating supply and raising switching costs and lead times.

Vendors offering unique specs or medical/industrial certifications therefore gain pricing and delivery leverage over Ascom.

Dual-sourcing and design-for-alternatives reduce this supplier power but cannot fully eliminate certification and integration barriers.

Proprietary software and middleware dependencies

Proprietary software and middleware dependencies give suppliers outsized leverage over Ascom because core platforms rely on third‑party libraries, OSes, or licensed middleware, and in 2024 vendors still control upgrades, security patches and roadmap access. This control creates lock‑in and pricing power that can increase TCO and margin pressure. Negotiating enterprise agreements and pushing open standards reduces that supplier risk.

Wireless infrastructure and certification partners

Compliance with healthcare, RF and safety standards relies on accredited labs; ILAC membership exceeded 100 economies in 2024, highlighting limited official accreditation capacity that can create bottlenecks and premium testing pricing. Certification schedules often dictate product launch timing, so Ascom mitigates risk via strategic partnerships and early booking of lab slots to smooth timelines and costs.

Contract manufacturers and EMS providers

Contract manufacturers and EMS providers with ruggedized device and base-station expertise command leverage: global EMS revenue reached about $575 billion in 2024 and capacity utilization spikes above 85% during supply shortages, allowing preferential component allocation to higher‑margin customers.

Quality yields and NPI throughput directly affect Ascom margins; lower yields raise COGS while fast NPI secures launch windows. Long‑term volume commitments win priority and 1–3% better pricing or allocation in constrained periods.

- EMS market 2024 ~ $575B

- Utilization >85% in shortages

- NPI throughput and yields drive margins

- Long‑term commits → priority + ~1–3% better terms

Cloud and cybersecurity vendors

Ascom’s software and managed services rely on cloud and cybersecurity vendors, with market concentration high (2024 market shares: AWS ~33%, Microsoft Azure ~23%, Google Cloud ~11%), which gives suppliers pricing leverage; usage-based pricing and added compliance tooling can materially raise OPEX. Data residency and healthcare regulations increase switching friction, while multi-cloud architectures and strengthened internal security teams help rebalance supplier power.

- High cloud concentration: AWS/Azure/GCP ~33%/23%/11% (2024)

- Usage-based billing increases OPEX risk

- Data residency and healthcare compliance raise switching costs

- Multi-cloud + internal security reduce supplier leverage

Supply risk: EMS >85%, AWS 33% — dual‑source, multi‑cloud

Ascom faces concentrated suppliers for RF modules, certified testing and EMS, giving vendors pricing and allocation leverage; EMS market ~ $575B (2024) and utilization spikes >85% tighten access. Cloud concentration (AWS 33%, Azure 23%, GCP 11% in 2024) raises OPEX and switching friction for healthcare workloads. Mitigations: dual‑sourcing, long‑term commits (≈1–3% better terms), multi‑cloud and early certification bookings.

| Metric | 2024 |

|---|---|

| EMS market | $575B |

| EMS utilization | >85% (shortages) |

| Cloud share | AWS 33% / AZ 23% / GCP 11% |

| ILAC membership | >100 economies |

| Long‑term commit benefit | ≈1–3% better terms |

What is included in the product

Tailored Porter's Five Forces analysis for Ascom that uncovers key drivers of competition, customer influence, supplier power, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Practical insights support strategic decisions, investor materials, and editable reports for business planning and internal strategy.

Concise Porter's Five Forces for Ascom—crystal-clear force ratings and a radar chart to pinpoint competitive pain points, prioritize strategic responses, and drop straight into decks or dashboards.

Customers Bargaining Power

Large hospital systems and GPOs

Large health networks and GPOs aggregate demand and negotiate aggressively, with leading U.S. GPOs collectively managing over $200 billion in annual purchasing (2024), driving strong leverage for volume discounts, extended warranties and integration services. Vendor lists and tender processes intensify price pressure, so demonstrating total cost-of-ownership savings is critical to offset pure price focus.

High switching and integration costs

Once deployed, Ascom workflows embed across clinical units and EHRs, creating switching costs that industry reports in 2024 place commonly in the $500k–$5M range and materially reduce buyer churn. Buyers still extract concessions—renewal negotiations typically yield 5–10% price reductions—while demanding higher service and bespoke terms. Strong SLA performance (>90% uptime/response metrics) preserves pricing integrity and limits discount pressure.

Demand for interoperability and open APIs

Customers demand seamless integration with EHRs, nurse call, RTLS and alarm systems, driven by 21st Century Cures Act API requirements and near-universal EHR adoption (about 96% of US acute hospitals by 2024). Failure to interoperate leads to price pressure or outright disqualification; buyers require proofs, certifications and reference sites. Investing in certified connectors and standards demonstrably raises win rates and reduces price erosion.

Outcome-based procurement focus

Global tendering and long sales cycles

Public hospitals run formal RFPs with strict scoring matrices and budget caps; in 2024 many tenders exceed 12 months, which advantages incumbents, compresses margins and lets buyers leverage competing bids to extract discounts.

- Incumbent retention: higher win rates for current suppliers

- Sales cycle: tenders commonly >12 months (2024)

- Margin pressure: frequent price concessions

- Mitigation: early stakeholder mapping and clear solution differentiation

GPO leverage >$200B and 96% EHR adoption lock incumbents, compressing margins

Large GPOs drive leverage (>$200B purchasing, 2024), buyers push 5–10% renewal discounts; switching costs (reported $500k–$5M) and >90% SLA uptime defend pricing. EHR integration is critical (96% US acute hospital adoption, 2024); tenders commonly exceed 12 months, favoring incumbents and compressing margins.

| Metric | 2024 Value |

|---|---|

| GPO purchasing | $200B+ |

| EHR adoption (US acute) | 96% |

| Switching cost range | $500k–$5M |

| Renewal discounts | 5–10% |

| Tender length | >12 months |

What You See Is What You Get

Ascom Porter's Five Forces Analysis

You're looking at the actual Ascom Porter's Five Forces Analysis document. This preview is the exact file you'll receive immediately after purchase—fully formatted, complete and ready to use. No mockups or placeholders; once you buy you'll get instant access to this precise deliverable for your analysis and decision-making.