Ashtead Technology Porter's Five Forces Analysis

Don't Miss the Bigger Picture

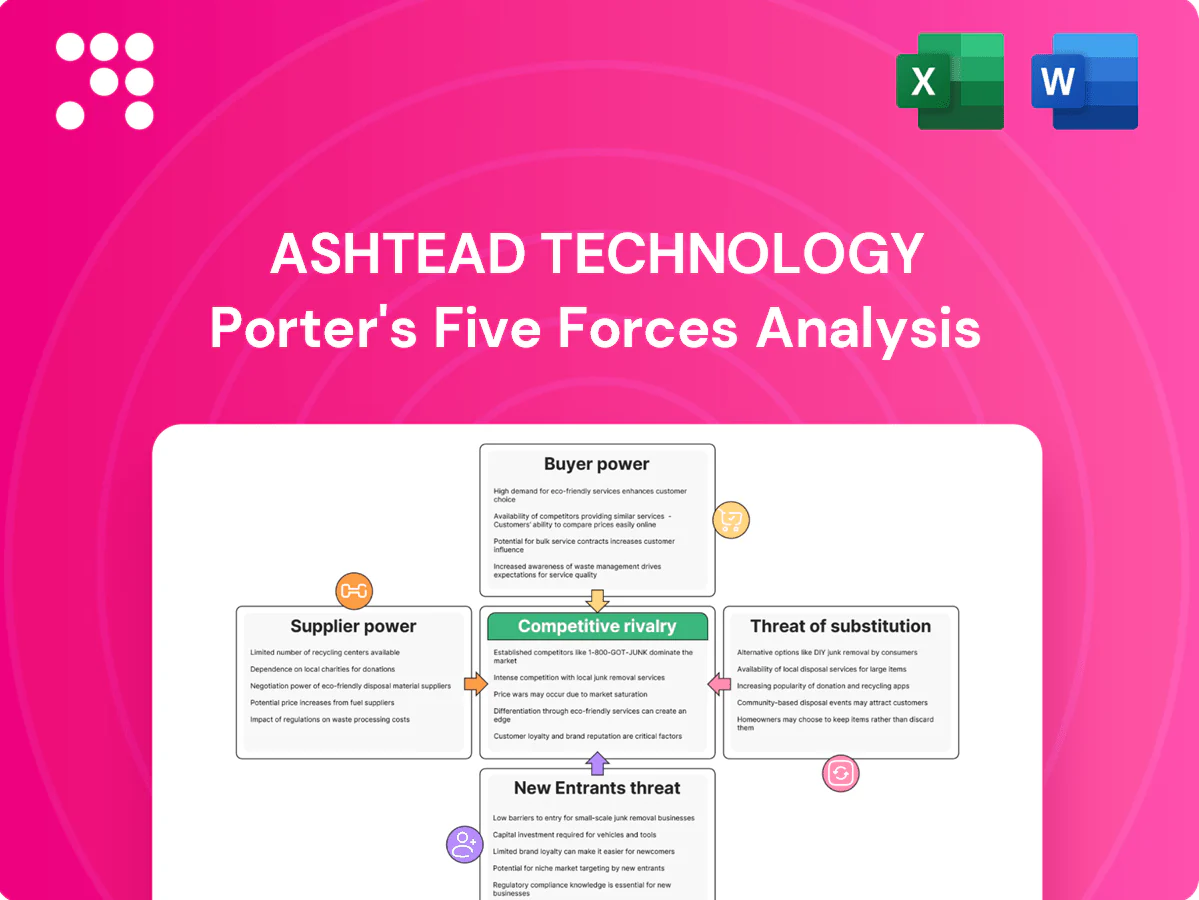

Ashtead Technology faces moderate supplier power, concentrated buyers in energy and infrastructure, and high competitive rivalry from niche rental specialists. Emerging technologies and substitutes present medium threats while regulatory barriers curb new entrants. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Specialized OEM concentration

Critical subsea sensors, acoustics, ROVs and positioning systems are sourced from a narrow set of specialized OEMs, concentrating supplier power and raising switching costs. Long qualification cycles and certification requirements entrench incumbents and slow alternative sourcing. This often produces tighter delivery terms and limited discounting for customers. Ashtead mitigates exposure by multi-sourcing where feasible and maintaining long-term OEM relationships.

Technology lock-in and IP

Proprietary interfaces and software ecosystems create switching frictions for Ashtead Technology, binding clients and increasing supplier leverage over upgrades and maintenance. As of 2024 Ashtead Technology operates within Ashtead Group (AHT.L), so compatibility with client fleets can lock the business to specific vendors. This elevates supplier bargaining power on pricing and support; negotiating portfolio agreements helps dilute that lock-in.

Lead-time and supply chain risk

Long lead times for subsea electronics and specialist semiconductors — often exceeding six months in 2024 for certain parts — amplify supplier control over Ashtead Technology. Geopolitics and logistics constraints have caused intermittent availability hits for time-critical projects. Expedited fees and allocation priorities can raise procurement costs materially, sometimes by up to 30%. Strategic inventory and in‑house refurbishment capacity help buffer this risk.

Aftermarket and spares control

OEMs often gatekeep spares, calibration and certifications, and mandatory OEM servicing can set pricing and scheduling, squeezing margins and causing delays that jeopardize typical SLA uptime targets above 95% for field clients. Ashtead Technology reduces this supplier power via in‑house workshops and accredited labs that lower lead times and restore control over pricing and delivery.

- OEM gatekeeping raises spare costs and scheduling risk

- Mandatory OEM service can impact >95% uptime SLAs

- In‑house workshops/accredited labs cut dependency

Countervailing buyer scale

Large end-clients influence OEM behavior through joint programs, and Ashtead can leverage client-backed standardization to extract better terms; Ashtead Group reported c.£5.9bn revenue in FY2024, boosting its bargaining credibility. Framework deals and volume commitments typically curb supplier pricing (often 5–15%), while collaboration on product roadmaps aligns incentives and reduces OEM hold-up risk.

- Client-backed standards: improved negotiation

- Frameworks: 5–15% price leverage

- Volume commitments: secure supply/discounts

- Roadmap collaboration: aligned incentives

Supplier leverage keeps lead times >6 months; expedite fees up to 30%, framework cuts 5–15%

Specialized OEM concentration, long qualification cycles and proprietary interfaces give suppliers meaningful leverage, raising switching costs and pricing pressure. In 2024 lead times exceeded six months for some subsea electronics, expedited fees rose up to 30% and Ashtead Group reported c.£5.9bn revenue, improving negotiation clout. In‑house workshops and framework deals (5–15% price leverage) partially offset supplier power.

| Metric | 2024 |

|---|---|

| Lead time | >6 months |

| Expedite cost | up to 30% |

| Ashtead Group rev | c.£5.9bn |

| Framework leverage | 5–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Ashtead Technology that uncovers competitive drivers, buyer and supplier power, barriers to entry, substitute threats and disruptive forces, providing strategic insights to gauge pricing influence, market entry risks and defensive levers for investors and management.

Clear one-sheet Porter's Five Forces for Ashtead Technology—instant strategic clarity to relieve analysis overload and speed decision-making. Customizable pressure levels and export-ready visuals (spider chart) make it easy to update with new data and drop straight into pitch decks or executive reports.

Customers Bargaining Power

Concentrated customer base

IOCs, NOCs, EPCs and tier-1 contractors control a concentrated pool of demand and drove over 60% of sector project spend in 2024, amplifying customer bargaining power. Tender-driven procurement in 2024 increased price sensitivity, forcing suppliers to match aggressive rates. Securing framework agreements now hinges on competitive pricing and tight service SLAs. Deep operational relationships and technical intimacy remain key to preserving margins.

Project cyclicality and budget scrutiny

Offshore project cyclicality and 2024 commodity swings (Brent ~85 USD/bbl) tighten buyer budgets, leading to capex gating and delayed campaign spend; customers push for cost cuts in downturns, driving rate compression and shorter commitments, often by 10–20% on dayrates; Ashtead Technology’s value-add services and digital inspection offerings help defend pricing and sustain utilization through cycles.

Switching costs and standardization

Equipment in the rental sector is partially standardized, reducing formal switching barriers for customers, but operational mobilization efficiencies and continuity of instrumentation data create practical stickiness.

Known reliability and historic calibration records raise effective switching costs, while Ashtead’s multi-region depot network leveraging over 1,150+ branches anchors customer preference.

Contractual performance KPIs and service SLAs further suppress churn by aligning uptime and measurement quality with client objectives.

Demand for integrated solutions

Clients increasingly demand one-stop rental, sales, calibration and personnel support; bundling cuts buyer transaction costs and shifts leverage to integrated providers. Ashtead can grow share-of-wallet by packaging services, reducing pure price comparisons and increasing stickiness; global equipment rental market ~USD 115bn in 2024 supports scale benefits.

- Bundles raise switching costs

- Share-of-wallet opportunity

- Tempered price-only competition

Compliance and uptime expectations

Strict HSE, third-party certification, and 2024-era uptime SLAs (commonly 99.5%+) raise buyer demands and contract scrutiny; financial penalties and service credits for downtime amplify customer leverage. Demonstrable reliability and rapid replacement response are key differentiators, while real-time, data-enabled monitoring increases trust and drives higher renewal propensity.

- HSE & certification pressure

- 99.5%+ uptime SLA expectation (2024)

- Downtime penalties strengthen buyer leverage

- Rapid replacement & telemetry = renewal driver

Over 60% buyer spend, Brent 85 USD/bbl squeeze dayrates

IOC/NOC/EPC concentration drove >60% of sector spend in 2024, increasing buyer leverage and tender-driven price sensitivity.

Brent ~85 USD/bbl in 2024 and offshore cyclicality led to capex gating, 10–20% dayrate compression and shorter commitments.

Ashtead’s 1,150+ branches, bundling, calibration records and 99.5%+ SLAs mitigate switching; global rental market ~USD 115bn (2024) supports scale.

| Metric | 2024 Value |

|---|---|

| Buyer spend concentration | >60% |

| Brent | ~85 USD/bbl |

| Dayrate pressure | 10–20% |

| Branches | 1,150+ |

| Market size | ~USD 115bn |

What You See Is What You Get

Ashtead Technology Porter's Five Forces Analysis

This preview is the exact Ashtead Technology Porter’s Five Forces analysis you’ll receive after purchase — professionally written, fully formatted, and ready for immediate download. No samples or placeholders, just the complete, final document for your use. Instant access upon payment.

Don't Miss the Bigger Picture

Ashtead Technology faces moderate supplier power, concentrated buyers in energy and infrastructure, and high competitive rivalry from niche rental specialists. Emerging technologies and substitutes present medium threats while regulatory barriers curb new entrants. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Specialized OEM concentration

Critical subsea sensors, acoustics, ROVs and positioning systems are sourced from a narrow set of specialized OEMs, concentrating supplier power and raising switching costs. Long qualification cycles and certification requirements entrench incumbents and slow alternative sourcing. This often produces tighter delivery terms and limited discounting for customers. Ashtead mitigates exposure by multi-sourcing where feasible and maintaining long-term OEM relationships.

Technology lock-in and IP

Proprietary interfaces and software ecosystems create switching frictions for Ashtead Technology, binding clients and increasing supplier leverage over upgrades and maintenance. As of 2024 Ashtead Technology operates within Ashtead Group (AHT.L), so compatibility with client fleets can lock the business to specific vendors. This elevates supplier bargaining power on pricing and support; negotiating portfolio agreements helps dilute that lock-in.

Lead-time and supply chain risk

Long lead times for subsea electronics and specialist semiconductors — often exceeding six months in 2024 for certain parts — amplify supplier control over Ashtead Technology. Geopolitics and logistics constraints have caused intermittent availability hits for time-critical projects. Expedited fees and allocation priorities can raise procurement costs materially, sometimes by up to 30%. Strategic inventory and in‑house refurbishment capacity help buffer this risk.

Aftermarket and spares control

OEMs often gatekeep spares, calibration and certifications, and mandatory OEM servicing can set pricing and scheduling, squeezing margins and causing delays that jeopardize typical SLA uptime targets above 95% for field clients. Ashtead Technology reduces this supplier power via in‑house workshops and accredited labs that lower lead times and restore control over pricing and delivery.

- OEM gatekeeping raises spare costs and scheduling risk

- Mandatory OEM service can impact >95% uptime SLAs

- In‑house workshops/accredited labs cut dependency

Countervailing buyer scale

Large end-clients influence OEM behavior through joint programs, and Ashtead can leverage client-backed standardization to extract better terms; Ashtead Group reported c.£5.9bn revenue in FY2024, boosting its bargaining credibility. Framework deals and volume commitments typically curb supplier pricing (often 5–15%), while collaboration on product roadmaps aligns incentives and reduces OEM hold-up risk.

- Client-backed standards: improved negotiation

- Frameworks: 5–15% price leverage

- Volume commitments: secure supply/discounts

- Roadmap collaboration: aligned incentives

Supplier leverage keeps lead times >6 months; expedite fees up to 30%, framework cuts 5–15%

Specialized OEM concentration, long qualification cycles and proprietary interfaces give suppliers meaningful leverage, raising switching costs and pricing pressure. In 2024 lead times exceeded six months for some subsea electronics, expedited fees rose up to 30% and Ashtead Group reported c.£5.9bn revenue, improving negotiation clout. In‑house workshops and framework deals (5–15% price leverage) partially offset supplier power.

| Metric | 2024 |

|---|---|

| Lead time | >6 months |

| Expedite cost | up to 30% |

| Ashtead Group rev | c.£5.9bn |

| Framework leverage | 5–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Ashtead Technology that uncovers competitive drivers, buyer and supplier power, barriers to entry, substitute threats and disruptive forces, providing strategic insights to gauge pricing influence, market entry risks and defensive levers for investors and management.

Clear one-sheet Porter's Five Forces for Ashtead Technology—instant strategic clarity to relieve analysis overload and speed decision-making. Customizable pressure levels and export-ready visuals (spider chart) make it easy to update with new data and drop straight into pitch decks or executive reports.

Customers Bargaining Power

Concentrated customer base

IOCs, NOCs, EPCs and tier-1 contractors control a concentrated pool of demand and drove over 60% of sector project spend in 2024, amplifying customer bargaining power. Tender-driven procurement in 2024 increased price sensitivity, forcing suppliers to match aggressive rates. Securing framework agreements now hinges on competitive pricing and tight service SLAs. Deep operational relationships and technical intimacy remain key to preserving margins.

Project cyclicality and budget scrutiny

Offshore project cyclicality and 2024 commodity swings (Brent ~85 USD/bbl) tighten buyer budgets, leading to capex gating and delayed campaign spend; customers push for cost cuts in downturns, driving rate compression and shorter commitments, often by 10–20% on dayrates; Ashtead Technology’s value-add services and digital inspection offerings help defend pricing and sustain utilization through cycles.

Switching costs and standardization

Equipment in the rental sector is partially standardized, reducing formal switching barriers for customers, but operational mobilization efficiencies and continuity of instrumentation data create practical stickiness.

Known reliability and historic calibration records raise effective switching costs, while Ashtead’s multi-region depot network leveraging over 1,150+ branches anchors customer preference.

Contractual performance KPIs and service SLAs further suppress churn by aligning uptime and measurement quality with client objectives.

Demand for integrated solutions

Clients increasingly demand one-stop rental, sales, calibration and personnel support; bundling cuts buyer transaction costs and shifts leverage to integrated providers. Ashtead can grow share-of-wallet by packaging services, reducing pure price comparisons and increasing stickiness; global equipment rental market ~USD 115bn in 2024 supports scale benefits.

- Bundles raise switching costs

- Share-of-wallet opportunity

- Tempered price-only competition

Compliance and uptime expectations

Strict HSE, third-party certification, and 2024-era uptime SLAs (commonly 99.5%+) raise buyer demands and contract scrutiny; financial penalties and service credits for downtime amplify customer leverage. Demonstrable reliability and rapid replacement response are key differentiators, while real-time, data-enabled monitoring increases trust and drives higher renewal propensity.

- HSE & certification pressure

- 99.5%+ uptime SLA expectation (2024)

- Downtime penalties strengthen buyer leverage

- Rapid replacement & telemetry = renewal driver

Over 60% buyer spend, Brent 85 USD/bbl squeeze dayrates

IOC/NOC/EPC concentration drove >60% of sector spend in 2024, increasing buyer leverage and tender-driven price sensitivity.

Brent ~85 USD/bbl in 2024 and offshore cyclicality led to capex gating, 10–20% dayrate compression and shorter commitments.

Ashtead’s 1,150+ branches, bundling, calibration records and 99.5%+ SLAs mitigate switching; global rental market ~USD 115bn (2024) supports scale.

| Metric | 2024 Value |

|---|---|

| Buyer spend concentration | >60% |

| Brent | ~85 USD/bbl |

| Dayrate pressure | 10–20% |

| Branches | 1,150+ |

| Market size | ~USD 115bn |

What You See Is What You Get

Ashtead Technology Porter's Five Forces Analysis

This preview is the exact Ashtead Technology Porter’s Five Forces analysis you’ll receive after purchase — professionally written, fully formatted, and ready for immediate download. No samples or placeholders, just the complete, final document for your use. Instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ashtead Technology faces moderate supplier power, concentrated buyers in energy and infrastructure, and high competitive rivalry from niche rental specialists. Emerging technologies and substitutes present medium threats while regulatory barriers curb new entrants. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Specialized OEM concentration

Critical subsea sensors, acoustics, ROVs and positioning systems are sourced from a narrow set of specialized OEMs, concentrating supplier power and raising switching costs. Long qualification cycles and certification requirements entrench incumbents and slow alternative sourcing. This often produces tighter delivery terms and limited discounting for customers. Ashtead mitigates exposure by multi-sourcing where feasible and maintaining long-term OEM relationships.

Technology lock-in and IP

Proprietary interfaces and software ecosystems create switching frictions for Ashtead Technology, binding clients and increasing supplier leverage over upgrades and maintenance. As of 2024 Ashtead Technology operates within Ashtead Group (AHT.L), so compatibility with client fleets can lock the business to specific vendors. This elevates supplier bargaining power on pricing and support; negotiating portfolio agreements helps dilute that lock-in.

Lead-time and supply chain risk

Long lead times for subsea electronics and specialist semiconductors — often exceeding six months in 2024 for certain parts — amplify supplier control over Ashtead Technology. Geopolitics and logistics constraints have caused intermittent availability hits for time-critical projects. Expedited fees and allocation priorities can raise procurement costs materially, sometimes by up to 30%. Strategic inventory and in‑house refurbishment capacity help buffer this risk.

Aftermarket and spares control

OEMs often gatekeep spares, calibration and certifications, and mandatory OEM servicing can set pricing and scheduling, squeezing margins and causing delays that jeopardize typical SLA uptime targets above 95% for field clients. Ashtead Technology reduces this supplier power via in‑house workshops and accredited labs that lower lead times and restore control over pricing and delivery.

- OEM gatekeeping raises spare costs and scheduling risk

- Mandatory OEM service can impact >95% uptime SLAs

- In‑house workshops/accredited labs cut dependency

Countervailing buyer scale

Large end-clients influence OEM behavior through joint programs, and Ashtead can leverage client-backed standardization to extract better terms; Ashtead Group reported c.£5.9bn revenue in FY2024, boosting its bargaining credibility. Framework deals and volume commitments typically curb supplier pricing (often 5–15%), while collaboration on product roadmaps aligns incentives and reduces OEM hold-up risk.

- Client-backed standards: improved negotiation

- Frameworks: 5–15% price leverage

- Volume commitments: secure supply/discounts

- Roadmap collaboration: aligned incentives

Supplier leverage keeps lead times >6 months; expedite fees up to 30%, framework cuts 5–15%

Specialized OEM concentration, long qualification cycles and proprietary interfaces give suppliers meaningful leverage, raising switching costs and pricing pressure. In 2024 lead times exceeded six months for some subsea electronics, expedited fees rose up to 30% and Ashtead Group reported c.£5.9bn revenue, improving negotiation clout. In‑house workshops and framework deals (5–15% price leverage) partially offset supplier power.

| Metric | 2024 |

|---|---|

| Lead time | >6 months |

| Expedite cost | up to 30% |

| Ashtead Group rev | c.£5.9bn |

| Framework leverage | 5–15% |

What is included in the product

Tailored Porter's Five Forces analysis for Ashtead Technology that uncovers competitive drivers, buyer and supplier power, barriers to entry, substitute threats and disruptive forces, providing strategic insights to gauge pricing influence, market entry risks and defensive levers for investors and management.

Clear one-sheet Porter's Five Forces for Ashtead Technology—instant strategic clarity to relieve analysis overload and speed decision-making. Customizable pressure levels and export-ready visuals (spider chart) make it easy to update with new data and drop straight into pitch decks or executive reports.

Customers Bargaining Power

Concentrated customer base

IOCs, NOCs, EPCs and tier-1 contractors control a concentrated pool of demand and drove over 60% of sector project spend in 2024, amplifying customer bargaining power. Tender-driven procurement in 2024 increased price sensitivity, forcing suppliers to match aggressive rates. Securing framework agreements now hinges on competitive pricing and tight service SLAs. Deep operational relationships and technical intimacy remain key to preserving margins.

Project cyclicality and budget scrutiny

Offshore project cyclicality and 2024 commodity swings (Brent ~85 USD/bbl) tighten buyer budgets, leading to capex gating and delayed campaign spend; customers push for cost cuts in downturns, driving rate compression and shorter commitments, often by 10–20% on dayrates; Ashtead Technology’s value-add services and digital inspection offerings help defend pricing and sustain utilization through cycles.

Switching costs and standardization

Equipment in the rental sector is partially standardized, reducing formal switching barriers for customers, but operational mobilization efficiencies and continuity of instrumentation data create practical stickiness.

Known reliability and historic calibration records raise effective switching costs, while Ashtead’s multi-region depot network leveraging over 1,150+ branches anchors customer preference.

Contractual performance KPIs and service SLAs further suppress churn by aligning uptime and measurement quality with client objectives.

Demand for integrated solutions

Clients increasingly demand one-stop rental, sales, calibration and personnel support; bundling cuts buyer transaction costs and shifts leverage to integrated providers. Ashtead can grow share-of-wallet by packaging services, reducing pure price comparisons and increasing stickiness; global equipment rental market ~USD 115bn in 2024 supports scale benefits.

- Bundles raise switching costs

- Share-of-wallet opportunity

- Tempered price-only competition

Compliance and uptime expectations

Strict HSE, third-party certification, and 2024-era uptime SLAs (commonly 99.5%+) raise buyer demands and contract scrutiny; financial penalties and service credits for downtime amplify customer leverage. Demonstrable reliability and rapid replacement response are key differentiators, while real-time, data-enabled monitoring increases trust and drives higher renewal propensity.

- HSE & certification pressure

- 99.5%+ uptime SLA expectation (2024)

- Downtime penalties strengthen buyer leverage

- Rapid replacement & telemetry = renewal driver

Over 60% buyer spend, Brent 85 USD/bbl squeeze dayrates

IOC/NOC/EPC concentration drove >60% of sector spend in 2024, increasing buyer leverage and tender-driven price sensitivity.

Brent ~85 USD/bbl in 2024 and offshore cyclicality led to capex gating, 10–20% dayrate compression and shorter commitments.

Ashtead’s 1,150+ branches, bundling, calibration records and 99.5%+ SLAs mitigate switching; global rental market ~USD 115bn (2024) supports scale.

| Metric | 2024 Value |

|---|---|

| Buyer spend concentration | >60% |

| Brent | ~85 USD/bbl |

| Dayrate pressure | 10–20% |

| Branches | 1,150+ |

| Market size | ~USD 115bn |

What You See Is What You Get

Ashtead Technology Porter's Five Forces Analysis

This preview is the exact Ashtead Technology Porter’s Five Forces analysis you’ll receive after purchase — professionally written, fully formatted, and ready for immediate download. No samples or placeholders, just the complete, final document for your use. Instant access upon payment.