Ashtead Technology PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our PESTLE analysis of Ashtead Technology—three concise, evidence-backed views on political, economic and technological forces shaping growth. Ideal for investors and strategists, it highlights regulatory risks, market drivers and sustainability trends. Purchase the full report to access detailed, downloadable insights and actionable recommendations.

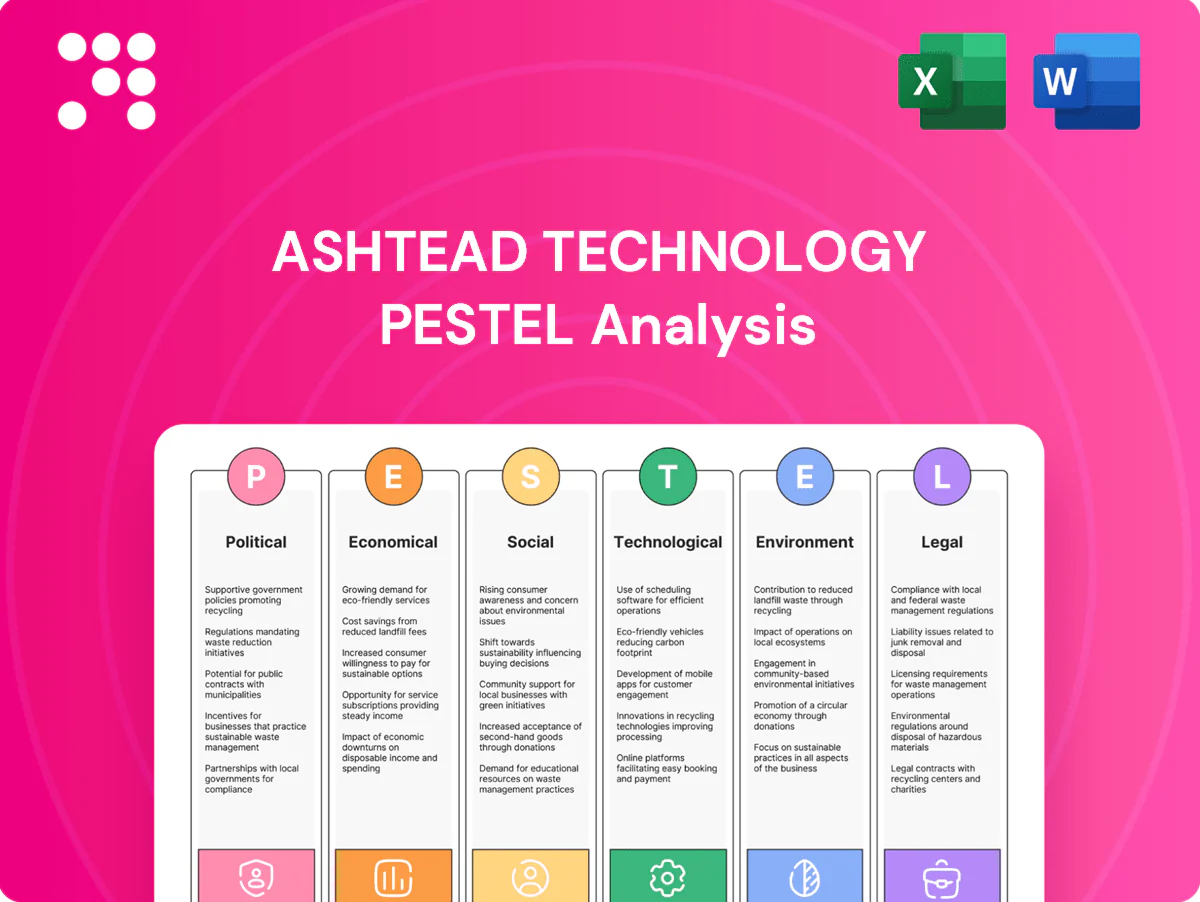

Political factors

Energy policy direction and subsidies

Government prioritization of offshore wind — UK target 50 GW by 2030 — and low‑carbon projects shapes Ashtead Technology’s project pipeline and rental demand. Subsidies and tax credits such as the US IRA’s up to 30% ITC accelerate inspections and installations. Policy reversals or auction delays create utilization gaps. Ashtead must align inventory and services to incentives in key basins.

Geopolitical stability and maritime security

Regional tensions, piracy and naval incidents—exemplified by Red Sea attacks since Oct 2023—have forced vessel rerouting adding 10–14 days and war-risk insurance spikes up to 300%, disrupting offshore access and timelines. Sanctions and export controls (eg EU/US restrictions since 2014, expanded 2022) limit equipment deployment to sanctioned jurisdictions. Ashtead Technology reduces concentration risk via diversified geography and flexible logistics.

Local content and nationalization pressures

Many jurisdictions — over 40 countries as of 2024 — enforce offshore local content rules, affecting hiring, partnerships, inventory placement and service delivery for Ashtead Technology. Compliance can raise operating costs by an estimated 5–15% but enhances market access and stakeholder relations. Strategic JV structures and localized bases can boost bid competitiveness, sometimes improving win rates by up to 20% in regional tenders.

Decommissioning mandates and stewardship

Governments are tightening end-of-life obligations for oil and gas assets, with UK North Sea decommissioning liabilities estimated at over £70 billion to 2050, creating sustained demand for survey and cutting equipment through clearer timelines and funding mechanisms. Policy uncertainty can still delay scope release and cash flows, so Ashtead can market itself as a compliance enabler to operators.

- Regulatory tightening: sustained equipment demand

- Funding clarity: supports multiyear contracts

- Policy risk: potential project delays

- Strategic position: compliance enabler

Trade policies, tariffs, and customs regimes

Tariffs and customs delays on subsea components materially extend turnaround times and squeeze margins, while temporary import regimes such as ATA carnets and bonded warehouses are essential to maintain fleet mobility; regulatory shifts risk stranding specialized assets, so proactive trade planning and equipment standardization reduce cross-border friction.

- Tariffs and delays increase operating costs and downtime

- ATA carnets/bonded warehousing critical for rapid redeployment

- Regulatory change can immobilize specialized kit

- Standardization and trade planning mitigate risk

UK 50 GW by 2030 and US 30% ITC boost offshore demand; Red Sea risks add delays

Government targets (UK 50 GW by 2030) and incentives (US IRA up to 30% ITC) drive rental demand and inspections, while policy reversals or auction delays can create utilization gaps. Geopolitical risks (Red Sea attacks since Oct 2023 adding 10–14 days; war‑risk premiums + up to 300%) and sanctions restrict deployment. Local content (>40 countries by 2024) and UK decommissioning liabilities (>£70bn to 2050) shape costs and long‑term demand.

| Metric | Value |

|---|---|

| UK offshore target | 50 GW by 2030 |

| US IRA credit | Up to 30% ITC |

| Red Sea impact | +10–14 days; war‑risk + up to 300% |

| Local content | >40 countries (2024) |

| North Sea decommissioning | £>70bn to 2050 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Ashtead Technology, with data-driven, region- and industry-specific insights and forward-looking scenarios. Designed for executives and investors to identify threats, opportunities and strategic priorities.

A concise, visually segmented PESTLE summary for Ashtead Technology that’s easy to drop into presentations, share across teams, and annotate with region-specific notes—streamlining external risk discussions and strategic planning.

Economic factors

Hydrocarbon price cycles and CAPEX

Brent crude averaged about 86 USD/bbl in 2024, driving stronger offshore FIDs, inspection campaigns and maintenance budgets while global oil and gas capex rose to roughly 420 billion USD in 2024; higher prices stimulated construction and life-extension surveys, whereas downturns push clients to defer nonessential work and cut costs, making Ashtead Technology’s rental flexibility attractive to capex-light strategies across cycles.

Offshore wind build-out and grid economics

Offshore wind LCOE has fallen roughly 30% since 2015, driving installations where wholesale power prices (European day‑ahead averages ~€60–€120/MWh in 2024) make projects bankable. Interconnection bottlenecks and auction undersubscription in parts of Europe in 2023–24 have delayed build schedules. Maturing floating wind technology and a growing project pipeline open deeper-water markets ideal for subsea expertise. Ashtead can leverage cross-sector rental equipment demand across fixed and floating wind.

Inflation, FX, and interest rates

Input cost inflation and tighter credit have pushed project hurdle rates higher, squeezing returns for capital-intensive subsea work; central-bank policy rates have been around 5.25% in recent cycles, keeping borrowing expensive. FX volatility alters margins on multinational contracts and the economics of deployed assets across USD/GBP/EUR. Higher interest rates raise client financing costs and Ashtead’s fleet renewal expense; hedging and contract price indexation are used to protect margins.

Supply chain capacity and vessel availability

Supply chain constraints in construction vessels, ROV crews and critical components can gate project starts; industry data showed offshore vessel utilization remained elevated through 2023–2024, pressuring availability and driving day-rate spikes up to ~30% in peak windows, shifting budgets and schedules. Early engagement and framework agreements secure access in peak seasons while Ashtead Technology’s broad inventory shortens client lead times.

- Vessel/crew scarcity: gates project starts

- Day-rate spikes: ~30% pressure on budgets

- Early engagement: secures peak access

- Inventory breadth: reduces client lead times

Client consolidation and procurement power

Client consolidation among operators and service firms concentrates buying power, driving larger framework agreements that enforce standardized pricing and performance KPIs, which compress margins for suppliers. This environment favors reliable, scalable partners like Ashtead Technology that can meet uniform KPIs across regions. Demonstrable, data-backed performance increases contract renewal and share-of-wallet with consolidated clients.

- Concentration: stronger buyer leverage

- Standardization: pricing and KPI pressure

- Opportunity: rewards scalable, reliable vendors

- Data: performance metrics boost renewals

UK 50 GW by 2030 and US 30% ITC boost offshore demand; Red Sea risks add delays

Brent ~86 USD/bbl in 2024 boosted offshore FIDs and maintenance spend while global oil & gas capex reached ~420 bn USD, favouring rental over capex-heavy models. Offshore wind LCOE down ~30% since 2015 with EU day‑ahead ~€60–€120/MWh in 2024, expanding subsea opportunity. Higher policy rates (~5.25%) and input inflation raise project hurdle rates and client financing costs; vessel/crew scarcity lifts peak day‑rates ~30%.

| Metric | Value |

|---|---|

| Brent 2024 | 86 USD/bbl |

| O&G capex 2024 | 420 bn USD |

| EU power 2024 | €60–€120/MWh |

| Policy rate | ~5.25% |

| Peak day‑rate spike | ~30% |

Full Version Awaits

Ashtead Technology PESTLE Analysis

The preview shown here is the exact Ashtead Technology PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the layout, content, and structure visible here are the final file delivered instantly after checkout. Use it immediately for research, presentations, or strategic planning.

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our PESTLE analysis of Ashtead Technology—three concise, evidence-backed views on political, economic and technological forces shaping growth. Ideal for investors and strategists, it highlights regulatory risks, market drivers and sustainability trends. Purchase the full report to access detailed, downloadable insights and actionable recommendations.

Political factors

Energy policy direction and subsidies

Government prioritization of offshore wind — UK target 50 GW by 2030 — and low‑carbon projects shapes Ashtead Technology’s project pipeline and rental demand. Subsidies and tax credits such as the US IRA’s up to 30% ITC accelerate inspections and installations. Policy reversals or auction delays create utilization gaps. Ashtead must align inventory and services to incentives in key basins.

Geopolitical stability and maritime security

Regional tensions, piracy and naval incidents—exemplified by Red Sea attacks since Oct 2023—have forced vessel rerouting adding 10–14 days and war-risk insurance spikes up to 300%, disrupting offshore access and timelines. Sanctions and export controls (eg EU/US restrictions since 2014, expanded 2022) limit equipment deployment to sanctioned jurisdictions. Ashtead Technology reduces concentration risk via diversified geography and flexible logistics.

Local content and nationalization pressures

Many jurisdictions — over 40 countries as of 2024 — enforce offshore local content rules, affecting hiring, partnerships, inventory placement and service delivery for Ashtead Technology. Compliance can raise operating costs by an estimated 5–15% but enhances market access and stakeholder relations. Strategic JV structures and localized bases can boost bid competitiveness, sometimes improving win rates by up to 20% in regional tenders.

Decommissioning mandates and stewardship

Governments are tightening end-of-life obligations for oil and gas assets, with UK North Sea decommissioning liabilities estimated at over £70 billion to 2050, creating sustained demand for survey and cutting equipment through clearer timelines and funding mechanisms. Policy uncertainty can still delay scope release and cash flows, so Ashtead can market itself as a compliance enabler to operators.

- Regulatory tightening: sustained equipment demand

- Funding clarity: supports multiyear contracts

- Policy risk: potential project delays

- Strategic position: compliance enabler

Trade policies, tariffs, and customs regimes

Tariffs and customs delays on subsea components materially extend turnaround times and squeeze margins, while temporary import regimes such as ATA carnets and bonded warehouses are essential to maintain fleet mobility; regulatory shifts risk stranding specialized assets, so proactive trade planning and equipment standardization reduce cross-border friction.

- Tariffs and delays increase operating costs and downtime

- ATA carnets/bonded warehousing critical for rapid redeployment

- Regulatory change can immobilize specialized kit

- Standardization and trade planning mitigate risk

UK 50 GW by 2030 and US 30% ITC boost offshore demand; Red Sea risks add delays

Government targets (UK 50 GW by 2030) and incentives (US IRA up to 30% ITC) drive rental demand and inspections, while policy reversals or auction delays can create utilization gaps. Geopolitical risks (Red Sea attacks since Oct 2023 adding 10–14 days; war‑risk premiums + up to 300%) and sanctions restrict deployment. Local content (>40 countries by 2024) and UK decommissioning liabilities (>£70bn to 2050) shape costs and long‑term demand.

| Metric | Value |

|---|---|

| UK offshore target | 50 GW by 2030 |

| US IRA credit | Up to 30% ITC |

| Red Sea impact | +10–14 days; war‑risk + up to 300% |

| Local content | >40 countries (2024) |

| North Sea decommissioning | £>70bn to 2050 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Ashtead Technology, with data-driven, region- and industry-specific insights and forward-looking scenarios. Designed for executives and investors to identify threats, opportunities and strategic priorities.

A concise, visually segmented PESTLE summary for Ashtead Technology that’s easy to drop into presentations, share across teams, and annotate with region-specific notes—streamlining external risk discussions and strategic planning.

Economic factors

Hydrocarbon price cycles and CAPEX

Brent crude averaged about 86 USD/bbl in 2024, driving stronger offshore FIDs, inspection campaigns and maintenance budgets while global oil and gas capex rose to roughly 420 billion USD in 2024; higher prices stimulated construction and life-extension surveys, whereas downturns push clients to defer nonessential work and cut costs, making Ashtead Technology’s rental flexibility attractive to capex-light strategies across cycles.

Offshore wind build-out and grid economics

Offshore wind LCOE has fallen roughly 30% since 2015, driving installations where wholesale power prices (European day‑ahead averages ~€60–€120/MWh in 2024) make projects bankable. Interconnection bottlenecks and auction undersubscription in parts of Europe in 2023–24 have delayed build schedules. Maturing floating wind technology and a growing project pipeline open deeper-water markets ideal for subsea expertise. Ashtead can leverage cross-sector rental equipment demand across fixed and floating wind.

Inflation, FX, and interest rates

Input cost inflation and tighter credit have pushed project hurdle rates higher, squeezing returns for capital-intensive subsea work; central-bank policy rates have been around 5.25% in recent cycles, keeping borrowing expensive. FX volatility alters margins on multinational contracts and the economics of deployed assets across USD/GBP/EUR. Higher interest rates raise client financing costs and Ashtead’s fleet renewal expense; hedging and contract price indexation are used to protect margins.

Supply chain capacity and vessel availability

Supply chain constraints in construction vessels, ROV crews and critical components can gate project starts; industry data showed offshore vessel utilization remained elevated through 2023–2024, pressuring availability and driving day-rate spikes up to ~30% in peak windows, shifting budgets and schedules. Early engagement and framework agreements secure access in peak seasons while Ashtead Technology’s broad inventory shortens client lead times.

- Vessel/crew scarcity: gates project starts

- Day-rate spikes: ~30% pressure on budgets

- Early engagement: secures peak access

- Inventory breadth: reduces client lead times

Client consolidation and procurement power

Client consolidation among operators and service firms concentrates buying power, driving larger framework agreements that enforce standardized pricing and performance KPIs, which compress margins for suppliers. This environment favors reliable, scalable partners like Ashtead Technology that can meet uniform KPIs across regions. Demonstrable, data-backed performance increases contract renewal and share-of-wallet with consolidated clients.

- Concentration: stronger buyer leverage

- Standardization: pricing and KPI pressure

- Opportunity: rewards scalable, reliable vendors

- Data: performance metrics boost renewals

UK 50 GW by 2030 and US 30% ITC boost offshore demand; Red Sea risks add delays

Brent ~86 USD/bbl in 2024 boosted offshore FIDs and maintenance spend while global oil & gas capex reached ~420 bn USD, favouring rental over capex-heavy models. Offshore wind LCOE down ~30% since 2015 with EU day‑ahead ~€60–€120/MWh in 2024, expanding subsea opportunity. Higher policy rates (~5.25%) and input inflation raise project hurdle rates and client financing costs; vessel/crew scarcity lifts peak day‑rates ~30%.

| Metric | Value |

|---|---|

| Brent 2024 | 86 USD/bbl |

| O&G capex 2024 | 420 bn USD |

| EU power 2024 | €60–€120/MWh |

| Policy rate | ~5.25% |

| Peak day‑rate spike | ~30% |

Full Version Awaits

Ashtead Technology PESTLE Analysis

The preview shown here is the exact Ashtead Technology PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the layout, content, and structure visible here are the final file delivered instantly after checkout. Use it immediately for research, presentations, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our PESTLE analysis of Ashtead Technology—three concise, evidence-backed views on political, economic and technological forces shaping growth. Ideal for investors and strategists, it highlights regulatory risks, market drivers and sustainability trends. Purchase the full report to access detailed, downloadable insights and actionable recommendations.

Political factors

Energy policy direction and subsidies

Government prioritization of offshore wind — UK target 50 GW by 2030 — and low‑carbon projects shapes Ashtead Technology’s project pipeline and rental demand. Subsidies and tax credits such as the US IRA’s up to 30% ITC accelerate inspections and installations. Policy reversals or auction delays create utilization gaps. Ashtead must align inventory and services to incentives in key basins.

Geopolitical stability and maritime security

Regional tensions, piracy and naval incidents—exemplified by Red Sea attacks since Oct 2023—have forced vessel rerouting adding 10–14 days and war-risk insurance spikes up to 300%, disrupting offshore access and timelines. Sanctions and export controls (eg EU/US restrictions since 2014, expanded 2022) limit equipment deployment to sanctioned jurisdictions. Ashtead Technology reduces concentration risk via diversified geography and flexible logistics.

Local content and nationalization pressures

Many jurisdictions — over 40 countries as of 2024 — enforce offshore local content rules, affecting hiring, partnerships, inventory placement and service delivery for Ashtead Technology. Compliance can raise operating costs by an estimated 5–15% but enhances market access and stakeholder relations. Strategic JV structures and localized bases can boost bid competitiveness, sometimes improving win rates by up to 20% in regional tenders.

Decommissioning mandates and stewardship

Governments are tightening end-of-life obligations for oil and gas assets, with UK North Sea decommissioning liabilities estimated at over £70 billion to 2050, creating sustained demand for survey and cutting equipment through clearer timelines and funding mechanisms. Policy uncertainty can still delay scope release and cash flows, so Ashtead can market itself as a compliance enabler to operators.

- Regulatory tightening: sustained equipment demand

- Funding clarity: supports multiyear contracts

- Policy risk: potential project delays

- Strategic position: compliance enabler

Trade policies, tariffs, and customs regimes

Tariffs and customs delays on subsea components materially extend turnaround times and squeeze margins, while temporary import regimes such as ATA carnets and bonded warehouses are essential to maintain fleet mobility; regulatory shifts risk stranding specialized assets, so proactive trade planning and equipment standardization reduce cross-border friction.

- Tariffs and delays increase operating costs and downtime

- ATA carnets/bonded warehousing critical for rapid redeployment

- Regulatory change can immobilize specialized kit

- Standardization and trade planning mitigate risk

UK 50 GW by 2030 and US 30% ITC boost offshore demand; Red Sea risks add delays

Government targets (UK 50 GW by 2030) and incentives (US IRA up to 30% ITC) drive rental demand and inspections, while policy reversals or auction delays can create utilization gaps. Geopolitical risks (Red Sea attacks since Oct 2023 adding 10–14 days; war‑risk premiums + up to 300%) and sanctions restrict deployment. Local content (>40 countries by 2024) and UK decommissioning liabilities (>£70bn to 2050) shape costs and long‑term demand.

| Metric | Value |

|---|---|

| UK offshore target | 50 GW by 2030 |

| US IRA credit | Up to 30% ITC |

| Red Sea impact | +10–14 days; war‑risk + up to 300% |

| Local content | >40 countries (2024) |

| North Sea decommissioning | £>70bn to 2050 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Ashtead Technology, with data-driven, region- and industry-specific insights and forward-looking scenarios. Designed for executives and investors to identify threats, opportunities and strategic priorities.

A concise, visually segmented PESTLE summary for Ashtead Technology that’s easy to drop into presentations, share across teams, and annotate with region-specific notes—streamlining external risk discussions and strategic planning.

Economic factors

Hydrocarbon price cycles and CAPEX

Brent crude averaged about 86 USD/bbl in 2024, driving stronger offshore FIDs, inspection campaigns and maintenance budgets while global oil and gas capex rose to roughly 420 billion USD in 2024; higher prices stimulated construction and life-extension surveys, whereas downturns push clients to defer nonessential work and cut costs, making Ashtead Technology’s rental flexibility attractive to capex-light strategies across cycles.

Offshore wind build-out and grid economics

Offshore wind LCOE has fallen roughly 30% since 2015, driving installations where wholesale power prices (European day‑ahead averages ~€60–€120/MWh in 2024) make projects bankable. Interconnection bottlenecks and auction undersubscription in parts of Europe in 2023–24 have delayed build schedules. Maturing floating wind technology and a growing project pipeline open deeper-water markets ideal for subsea expertise. Ashtead can leverage cross-sector rental equipment demand across fixed and floating wind.

Inflation, FX, and interest rates

Input cost inflation and tighter credit have pushed project hurdle rates higher, squeezing returns for capital-intensive subsea work; central-bank policy rates have been around 5.25% in recent cycles, keeping borrowing expensive. FX volatility alters margins on multinational contracts and the economics of deployed assets across USD/GBP/EUR. Higher interest rates raise client financing costs and Ashtead’s fleet renewal expense; hedging and contract price indexation are used to protect margins.

Supply chain capacity and vessel availability

Supply chain constraints in construction vessels, ROV crews and critical components can gate project starts; industry data showed offshore vessel utilization remained elevated through 2023–2024, pressuring availability and driving day-rate spikes up to ~30% in peak windows, shifting budgets and schedules. Early engagement and framework agreements secure access in peak seasons while Ashtead Technology’s broad inventory shortens client lead times.

- Vessel/crew scarcity: gates project starts

- Day-rate spikes: ~30% pressure on budgets

- Early engagement: secures peak access

- Inventory breadth: reduces client lead times

Client consolidation and procurement power

Client consolidation among operators and service firms concentrates buying power, driving larger framework agreements that enforce standardized pricing and performance KPIs, which compress margins for suppliers. This environment favors reliable, scalable partners like Ashtead Technology that can meet uniform KPIs across regions. Demonstrable, data-backed performance increases contract renewal and share-of-wallet with consolidated clients.

- Concentration: stronger buyer leverage

- Standardization: pricing and KPI pressure

- Opportunity: rewards scalable, reliable vendors

- Data: performance metrics boost renewals

UK 50 GW by 2030 and US 30% ITC boost offshore demand; Red Sea risks add delays

Brent ~86 USD/bbl in 2024 boosted offshore FIDs and maintenance spend while global oil & gas capex reached ~420 bn USD, favouring rental over capex-heavy models. Offshore wind LCOE down ~30% since 2015 with EU day‑ahead ~€60–€120/MWh in 2024, expanding subsea opportunity. Higher policy rates (~5.25%) and input inflation raise project hurdle rates and client financing costs; vessel/crew scarcity lifts peak day‑rates ~30%.

| Metric | Value |

|---|---|

| Brent 2024 | 86 USD/bbl |

| O&G capex 2024 | 420 bn USD |

| EU power 2024 | €60–€120/MWh |

| Policy rate | ~5.25% |

| Peak day‑rate spike | ~30% |

Full Version Awaits

Ashtead Technology PESTLE Analysis

The preview shown here is the exact Ashtead Technology PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; the layout, content, and structure visible here are the final file delivered instantly after checkout. Use it immediately for research, presentations, or strategic planning.