AsiaInfo Technologies Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

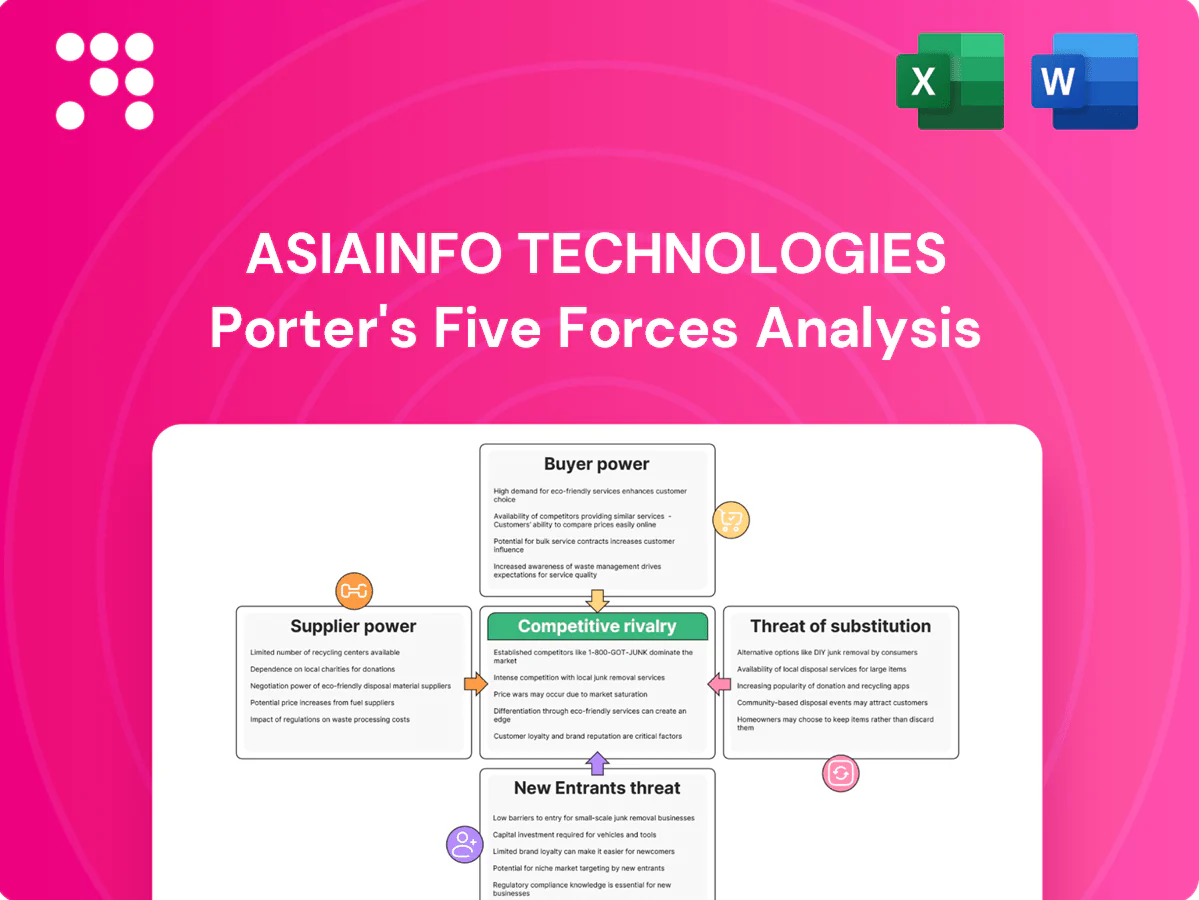

AsiaInfo Technologies faces moderate rivalry amid platform commoditization, rising buyer power from large telcos, and supplier leverage for specialized tech—while substitutes and regulatory shifts pose material threats; strategic positioning and barriers to entry remain mixed. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AsiaInfo’s competitive dynamics in detail.

Suppliers Bargaining Power

Dependence on hyperscale cloud and hardware

AsiaInfo’s deployments depend on a few hyperscalers—globally AWS ~32%, Azure ~23%, GCP ~11% (2024 estimates)—and in China Alibaba Cloud ~37%, Tencent ~22%, Huawei ~11%, concentrating supplier leverage and raising switching costs. Multi-cloud and on-prem architectures reduce dependency, while multi-year frame agreements stabilize pricing and supply.

Specialized AI/analytics toolchains

Core AsiaInfo products embed AI/ML frameworks, streaming engines and databases, creating licensing and technical lock-in that elevates supplier power and switching friction around optimized stacks. Open-source frameworks such as TensorFlow and PyTorch and in-house tuning mitigate exposure, while strategic vendor partnerships—often involving margin concessions—buy roadmap influence; IDC estimated global AI software spend at about $209B in 2024.

Telecom network equipment integrations

OSS/BSS must interoperate with RAN and core vendors, so compliance with proprietary interfaces keeps supplier leverage high and NEP certification cycles often add 6–12 months and incremental costs. AsiaInfo’s deep integration experience reduces integration risk but does not remove vendor influence. Industry moves to open APIs via TM Forum (850+ members) are gradually curbing supplier power.

Skilled talent and niche contractors

Highly skilled 5G, billing and data-engineering talent remains scarce, with ManpowerGroup's 2024 Talent Shortage Survey reporting 69% of employers struggling to fill roles, giving labor suppliers clear bargaining leverage; wage inflation and retention bonuses are pressuring margins and delivery schedules, while AsiaInfo’s scale, training programs and defined career pathways mitigate attrition and cost exposure, and nearshore/offshore resourcing diversifies the supply base.

- Scarcity: 69% talent shortage (ManpowerGroup 2024)

- Margin pressure: rising wages and retention bonuses

- Mitigant: AsiaInfo scale, training, career paths

- Resilience: nearshore/offshore diversification

Data sources and compliance tooling

Access to high-quality datasets and compliance tooling is concentrated: AWS, Microsoft Azure and Google Cloud held about 65% of global cloud IaaS market share in 2024, giving a few vendors outsized control. Strict telecom, finance and government regulations raise reliance on certified suppliers, shifting power during audits and contract renewals. Over time AsiaInfo lowering costs by building proprietary data pipelines will erode that leverage.

- Concentration: 65% IaaS share (AWS/MSFT/Google) 2024

- Regulatory reliance increases supplier power

- Proprietary pipelines reduce supplier leverage over time

High supplier power: cloud concentration and 69% 5G talent gap raise switching costs

Supplier power is high: global cloud concentration (AWS 32%, Azure 23%, GCP 11% 2024) and China hyperscalers (Alibaba 37%, Tencent 22%) raise switching costs and pricing leverage. Proprietary RAN/core interfaces and scarce 5G/data talent (69% shortage 2024) further strengthen suppliers, while AsiaInfo’s multi-cloud, proprietary pipelines and training reduce exposure over time.

| Metric | 2024 |

|---|---|

| Top 3 global IaaS share | 65% |

| AWS | 32% |

| Talent shortage | 69% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of new entrants and substitutes, and regulatory and technological disruptions shaping AsiaInfo Technologies’ industry position, with strategic insights on pricing, margins, and defensive opportunities.

A concise one-sheet Porter's Five Forces for AsiaInfo Technologies that instantly visualizes competitive pressure via a spider chart—customize force levels for shifting telecom software market dynamics and drop straight into decks or Excel dashboards without any complex macros.

Customers Bargaining Power

Concentrated Tier-1 telecom customers

Concentrated Tier-1 carriers—China Mobile, China Unicom and China Telecom—exert strong negotiation power over AsiaInfo given their combined ~1.66 billion mobile subscribers in 2024, representing a major revenue source. They demand customized features, stringent SLAs and price concessions; multi-year procurement cycles drive intense competitive bidding. AsiaInfo leverages incumbency and referenceability from long-term contracts to defend commercial terms.

High switching costs but rigorous RFPs

OSS/BSS replacements are risky and often multi-million-dollar endeavors, which lowers buyer propensity to switch; however, formal RFPs and proof-of-concepts in 2024 continue to force vendors to compete on demonstrable TCO and performance, enabling buyers to extract concessions. Strong migration tooling and modular architectures from vendors like AsiaInfo reduce buyer leverage by shortening timelines and lowering cost uncertainty.

Cross-vertical expansion with varied needs

Government, finance and energy clients have heterogeneous requirements and budgets, with AsiaInfo serving sectors that together sit within a $4.9 trillion global IT spend in 2024 (Gartner). Some buyers lack scale to negotiate aggressively while large public utilities and financial institutions impose strict compliance and price caps, creating mixed buyer power. Vertical-specific IP and accelerators lift AsiaInfo’s pricing stance by enabling premium, compliant solutions.

Preference for outcome-based contracts

Customers increasingly demand outcome- or usage-based pricing tied to KPIs, shifting performance risk to AsiaInfo and pressuring margins; clear value-realization frameworks enable premium pricing and justify higher TCV per deal. Robust SLAs, real-time analytics proofs and joint-governance clauses strengthen vendor negotiating leverage and reduce dispute costs.

- Outcome-based deals: higher client demand

- Risk shift: margin pressure

- Mitigation: value frameworks, SLAs, analytics

Demand for open architectures

Buyers increasingly demand open APIs to avoid vendor lock-in, a 2024 survey found 68% of telecom operators prioritize open architectures, boosting their leverage to compare vendors and swap components. AsiaInfo’s adherence to standards and open interfaces (e.g., cloud-native, 5G-friendly designs) builds trust and reduces bespoke one-offs. Marketplace ecosystems and network effects (platform reach growth >25% y/y in leading exchanges) can rebalance power toward buyers.

- Buyers: avoid lock-in, compare vendors

- AsiaInfo: standards reduce custom work

- Marketplaces: network effects shift power

Tier-1 carriers, open-API RFPs and outcome-based deals squeeze vendor margins

Concentrated Tier-1 carriers (≈1.66bn mobile subs in 2024) and large vertical clients exert high bargaining power, demanding SLAs, custom features and price concessions. OSS/BSS switch costs reduce churn but RFPs and POCs (68% of operators prioritize open APIs in 2024) restore buyer leverage. Outcome-based pricing and KPI-linked deals shift risk to AsiaInfo, pressuring margins.

| Metric | 2024 Value |

|---|---|

| Tier-1 mobile subs | ~1.66 billion |

| Global IT spend | $4.9 trillion (Gartner) |

| Operators prioritizing open APIs | 68% |

Preview Before You Purchase

AsiaInfo Technologies Porter's Five Forces Analysis

This Porter's Five Forces analysis of AsiaInfo Technologies is the professional, fully formatted strategic assessment you see here—covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. This preview is the exact document you'll receive instantly after purchase, ready for download and use with no placeholders or changes.

A Must-Have Tool for Decision-Makers

AsiaInfo Technologies faces moderate rivalry amid platform commoditization, rising buyer power from large telcos, and supplier leverage for specialized tech—while substitutes and regulatory shifts pose material threats; strategic positioning and barriers to entry remain mixed. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AsiaInfo’s competitive dynamics in detail.

Suppliers Bargaining Power

Dependence on hyperscale cloud and hardware

AsiaInfo’s deployments depend on a few hyperscalers—globally AWS ~32%, Azure ~23%, GCP ~11% (2024 estimates)—and in China Alibaba Cloud ~37%, Tencent ~22%, Huawei ~11%, concentrating supplier leverage and raising switching costs. Multi-cloud and on-prem architectures reduce dependency, while multi-year frame agreements stabilize pricing and supply.

Specialized AI/analytics toolchains

Core AsiaInfo products embed AI/ML frameworks, streaming engines and databases, creating licensing and technical lock-in that elevates supplier power and switching friction around optimized stacks. Open-source frameworks such as TensorFlow and PyTorch and in-house tuning mitigate exposure, while strategic vendor partnerships—often involving margin concessions—buy roadmap influence; IDC estimated global AI software spend at about $209B in 2024.

Telecom network equipment integrations

OSS/BSS must interoperate with RAN and core vendors, so compliance with proprietary interfaces keeps supplier leverage high and NEP certification cycles often add 6–12 months and incremental costs. AsiaInfo’s deep integration experience reduces integration risk but does not remove vendor influence. Industry moves to open APIs via TM Forum (850+ members) are gradually curbing supplier power.

Skilled talent and niche contractors

Highly skilled 5G, billing and data-engineering talent remains scarce, with ManpowerGroup's 2024 Talent Shortage Survey reporting 69% of employers struggling to fill roles, giving labor suppliers clear bargaining leverage; wage inflation and retention bonuses are pressuring margins and delivery schedules, while AsiaInfo’s scale, training programs and defined career pathways mitigate attrition and cost exposure, and nearshore/offshore resourcing diversifies the supply base.

- Scarcity: 69% talent shortage (ManpowerGroup 2024)

- Margin pressure: rising wages and retention bonuses

- Mitigant: AsiaInfo scale, training, career paths

- Resilience: nearshore/offshore diversification

Data sources and compliance tooling

Access to high-quality datasets and compliance tooling is concentrated: AWS, Microsoft Azure and Google Cloud held about 65% of global cloud IaaS market share in 2024, giving a few vendors outsized control. Strict telecom, finance and government regulations raise reliance on certified suppliers, shifting power during audits and contract renewals. Over time AsiaInfo lowering costs by building proprietary data pipelines will erode that leverage.

- Concentration: 65% IaaS share (AWS/MSFT/Google) 2024

- Regulatory reliance increases supplier power

- Proprietary pipelines reduce supplier leverage over time

High supplier power: cloud concentration and 69% 5G talent gap raise switching costs

Supplier power is high: global cloud concentration (AWS 32%, Azure 23%, GCP 11% 2024) and China hyperscalers (Alibaba 37%, Tencent 22%) raise switching costs and pricing leverage. Proprietary RAN/core interfaces and scarce 5G/data talent (69% shortage 2024) further strengthen suppliers, while AsiaInfo’s multi-cloud, proprietary pipelines and training reduce exposure over time.

| Metric | 2024 |

|---|---|

| Top 3 global IaaS share | 65% |

| AWS | 32% |

| Talent shortage | 69% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of new entrants and substitutes, and regulatory and technological disruptions shaping AsiaInfo Technologies’ industry position, with strategic insights on pricing, margins, and defensive opportunities.

A concise one-sheet Porter's Five Forces for AsiaInfo Technologies that instantly visualizes competitive pressure via a spider chart—customize force levels for shifting telecom software market dynamics and drop straight into decks or Excel dashboards without any complex macros.

Customers Bargaining Power

Concentrated Tier-1 telecom customers

Concentrated Tier-1 carriers—China Mobile, China Unicom and China Telecom—exert strong negotiation power over AsiaInfo given their combined ~1.66 billion mobile subscribers in 2024, representing a major revenue source. They demand customized features, stringent SLAs and price concessions; multi-year procurement cycles drive intense competitive bidding. AsiaInfo leverages incumbency and referenceability from long-term contracts to defend commercial terms.

High switching costs but rigorous RFPs

OSS/BSS replacements are risky and often multi-million-dollar endeavors, which lowers buyer propensity to switch; however, formal RFPs and proof-of-concepts in 2024 continue to force vendors to compete on demonstrable TCO and performance, enabling buyers to extract concessions. Strong migration tooling and modular architectures from vendors like AsiaInfo reduce buyer leverage by shortening timelines and lowering cost uncertainty.

Cross-vertical expansion with varied needs

Government, finance and energy clients have heterogeneous requirements and budgets, with AsiaInfo serving sectors that together sit within a $4.9 trillion global IT spend in 2024 (Gartner). Some buyers lack scale to negotiate aggressively while large public utilities and financial institutions impose strict compliance and price caps, creating mixed buyer power. Vertical-specific IP and accelerators lift AsiaInfo’s pricing stance by enabling premium, compliant solutions.

Preference for outcome-based contracts

Customers increasingly demand outcome- or usage-based pricing tied to KPIs, shifting performance risk to AsiaInfo and pressuring margins; clear value-realization frameworks enable premium pricing and justify higher TCV per deal. Robust SLAs, real-time analytics proofs and joint-governance clauses strengthen vendor negotiating leverage and reduce dispute costs.

- Outcome-based deals: higher client demand

- Risk shift: margin pressure

- Mitigation: value frameworks, SLAs, analytics

Demand for open architectures

Buyers increasingly demand open APIs to avoid vendor lock-in, a 2024 survey found 68% of telecom operators prioritize open architectures, boosting their leverage to compare vendors and swap components. AsiaInfo’s adherence to standards and open interfaces (e.g., cloud-native, 5G-friendly designs) builds trust and reduces bespoke one-offs. Marketplace ecosystems and network effects (platform reach growth >25% y/y in leading exchanges) can rebalance power toward buyers.

- Buyers: avoid lock-in, compare vendors

- AsiaInfo: standards reduce custom work

- Marketplaces: network effects shift power

Tier-1 carriers, open-API RFPs and outcome-based deals squeeze vendor margins

Concentrated Tier-1 carriers (≈1.66bn mobile subs in 2024) and large vertical clients exert high bargaining power, demanding SLAs, custom features and price concessions. OSS/BSS switch costs reduce churn but RFPs and POCs (68% of operators prioritize open APIs in 2024) restore buyer leverage. Outcome-based pricing and KPI-linked deals shift risk to AsiaInfo, pressuring margins.

| Metric | 2024 Value |

|---|---|

| Tier-1 mobile subs | ~1.66 billion |

| Global IT spend | $4.9 trillion (Gartner) |

| Operators prioritizing open APIs | 68% |

Preview Before You Purchase

AsiaInfo Technologies Porter's Five Forces Analysis

This Porter's Five Forces analysis of AsiaInfo Technologies is the professional, fully formatted strategic assessment you see here—covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. This preview is the exact document you'll receive instantly after purchase, ready for download and use with no placeholders or changes.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

AsiaInfo Technologies faces moderate rivalry amid platform commoditization, rising buyer power from large telcos, and supplier leverage for specialized tech—while substitutes and regulatory shifts pose material threats; strategic positioning and barriers to entry remain mixed. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AsiaInfo’s competitive dynamics in detail.

Suppliers Bargaining Power

Dependence on hyperscale cloud and hardware

AsiaInfo’s deployments depend on a few hyperscalers—globally AWS ~32%, Azure ~23%, GCP ~11% (2024 estimates)—and in China Alibaba Cloud ~37%, Tencent ~22%, Huawei ~11%, concentrating supplier leverage and raising switching costs. Multi-cloud and on-prem architectures reduce dependency, while multi-year frame agreements stabilize pricing and supply.

Specialized AI/analytics toolchains

Core AsiaInfo products embed AI/ML frameworks, streaming engines and databases, creating licensing and technical lock-in that elevates supplier power and switching friction around optimized stacks. Open-source frameworks such as TensorFlow and PyTorch and in-house tuning mitigate exposure, while strategic vendor partnerships—often involving margin concessions—buy roadmap influence; IDC estimated global AI software spend at about $209B in 2024.

Telecom network equipment integrations

OSS/BSS must interoperate with RAN and core vendors, so compliance with proprietary interfaces keeps supplier leverage high and NEP certification cycles often add 6–12 months and incremental costs. AsiaInfo’s deep integration experience reduces integration risk but does not remove vendor influence. Industry moves to open APIs via TM Forum (850+ members) are gradually curbing supplier power.

Skilled talent and niche contractors

Highly skilled 5G, billing and data-engineering talent remains scarce, with ManpowerGroup's 2024 Talent Shortage Survey reporting 69% of employers struggling to fill roles, giving labor suppliers clear bargaining leverage; wage inflation and retention bonuses are pressuring margins and delivery schedules, while AsiaInfo’s scale, training programs and defined career pathways mitigate attrition and cost exposure, and nearshore/offshore resourcing diversifies the supply base.

- Scarcity: 69% talent shortage (ManpowerGroup 2024)

- Margin pressure: rising wages and retention bonuses

- Mitigant: AsiaInfo scale, training, career paths

- Resilience: nearshore/offshore diversification

Data sources and compliance tooling

Access to high-quality datasets and compliance tooling is concentrated: AWS, Microsoft Azure and Google Cloud held about 65% of global cloud IaaS market share in 2024, giving a few vendors outsized control. Strict telecom, finance and government regulations raise reliance on certified suppliers, shifting power during audits and contract renewals. Over time AsiaInfo lowering costs by building proprietary data pipelines will erode that leverage.

- Concentration: 65% IaaS share (AWS/MSFT/Google) 2024

- Regulatory reliance increases supplier power

- Proprietary pipelines reduce supplier leverage over time

High supplier power: cloud concentration and 69% 5G talent gap raise switching costs

Supplier power is high: global cloud concentration (AWS 32%, Azure 23%, GCP 11% 2024) and China hyperscalers (Alibaba 37%, Tencent 22%) raise switching costs and pricing leverage. Proprietary RAN/core interfaces and scarce 5G/data talent (69% shortage 2024) further strengthen suppliers, while AsiaInfo’s multi-cloud, proprietary pipelines and training reduce exposure over time.

| Metric | 2024 |

|---|---|

| Top 3 global IaaS share | 65% |

| AWS | 32% |

| Talent shortage | 69% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of new entrants and substitutes, and regulatory and technological disruptions shaping AsiaInfo Technologies’ industry position, with strategic insights on pricing, margins, and defensive opportunities.

A concise one-sheet Porter's Five Forces for AsiaInfo Technologies that instantly visualizes competitive pressure via a spider chart—customize force levels for shifting telecom software market dynamics and drop straight into decks or Excel dashboards without any complex macros.

Customers Bargaining Power

Concentrated Tier-1 telecom customers

Concentrated Tier-1 carriers—China Mobile, China Unicom and China Telecom—exert strong negotiation power over AsiaInfo given their combined ~1.66 billion mobile subscribers in 2024, representing a major revenue source. They demand customized features, stringent SLAs and price concessions; multi-year procurement cycles drive intense competitive bidding. AsiaInfo leverages incumbency and referenceability from long-term contracts to defend commercial terms.

High switching costs but rigorous RFPs

OSS/BSS replacements are risky and often multi-million-dollar endeavors, which lowers buyer propensity to switch; however, formal RFPs and proof-of-concepts in 2024 continue to force vendors to compete on demonstrable TCO and performance, enabling buyers to extract concessions. Strong migration tooling and modular architectures from vendors like AsiaInfo reduce buyer leverage by shortening timelines and lowering cost uncertainty.

Cross-vertical expansion with varied needs

Government, finance and energy clients have heterogeneous requirements and budgets, with AsiaInfo serving sectors that together sit within a $4.9 trillion global IT spend in 2024 (Gartner). Some buyers lack scale to negotiate aggressively while large public utilities and financial institutions impose strict compliance and price caps, creating mixed buyer power. Vertical-specific IP and accelerators lift AsiaInfo’s pricing stance by enabling premium, compliant solutions.

Preference for outcome-based contracts

Customers increasingly demand outcome- or usage-based pricing tied to KPIs, shifting performance risk to AsiaInfo and pressuring margins; clear value-realization frameworks enable premium pricing and justify higher TCV per deal. Robust SLAs, real-time analytics proofs and joint-governance clauses strengthen vendor negotiating leverage and reduce dispute costs.

- Outcome-based deals: higher client demand

- Risk shift: margin pressure

- Mitigation: value frameworks, SLAs, analytics

Demand for open architectures

Buyers increasingly demand open APIs to avoid vendor lock-in, a 2024 survey found 68% of telecom operators prioritize open architectures, boosting their leverage to compare vendors and swap components. AsiaInfo’s adherence to standards and open interfaces (e.g., cloud-native, 5G-friendly designs) builds trust and reduces bespoke one-offs. Marketplace ecosystems and network effects (platform reach growth >25% y/y in leading exchanges) can rebalance power toward buyers.

- Buyers: avoid lock-in, compare vendors

- AsiaInfo: standards reduce custom work

- Marketplaces: network effects shift power

Tier-1 carriers, open-API RFPs and outcome-based deals squeeze vendor margins

Concentrated Tier-1 carriers (≈1.66bn mobile subs in 2024) and large vertical clients exert high bargaining power, demanding SLAs, custom features and price concessions. OSS/BSS switch costs reduce churn but RFPs and POCs (68% of operators prioritize open APIs in 2024) restore buyer leverage. Outcome-based pricing and KPI-linked deals shift risk to AsiaInfo, pressuring margins.

| Metric | 2024 Value |

|---|---|

| Tier-1 mobile subs | ~1.66 billion |

| Global IT spend | $4.9 trillion (Gartner) |

| Operators prioritizing open APIs | 68% |

Preview Before You Purchase

AsiaInfo Technologies Porter's Five Forces Analysis

This Porter's Five Forces analysis of AsiaInfo Technologies is the professional, fully formatted strategic assessment you see here—covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. This preview is the exact document you'll receive instantly after purchase, ready for download and use with no placeholders or changes.