Asics Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

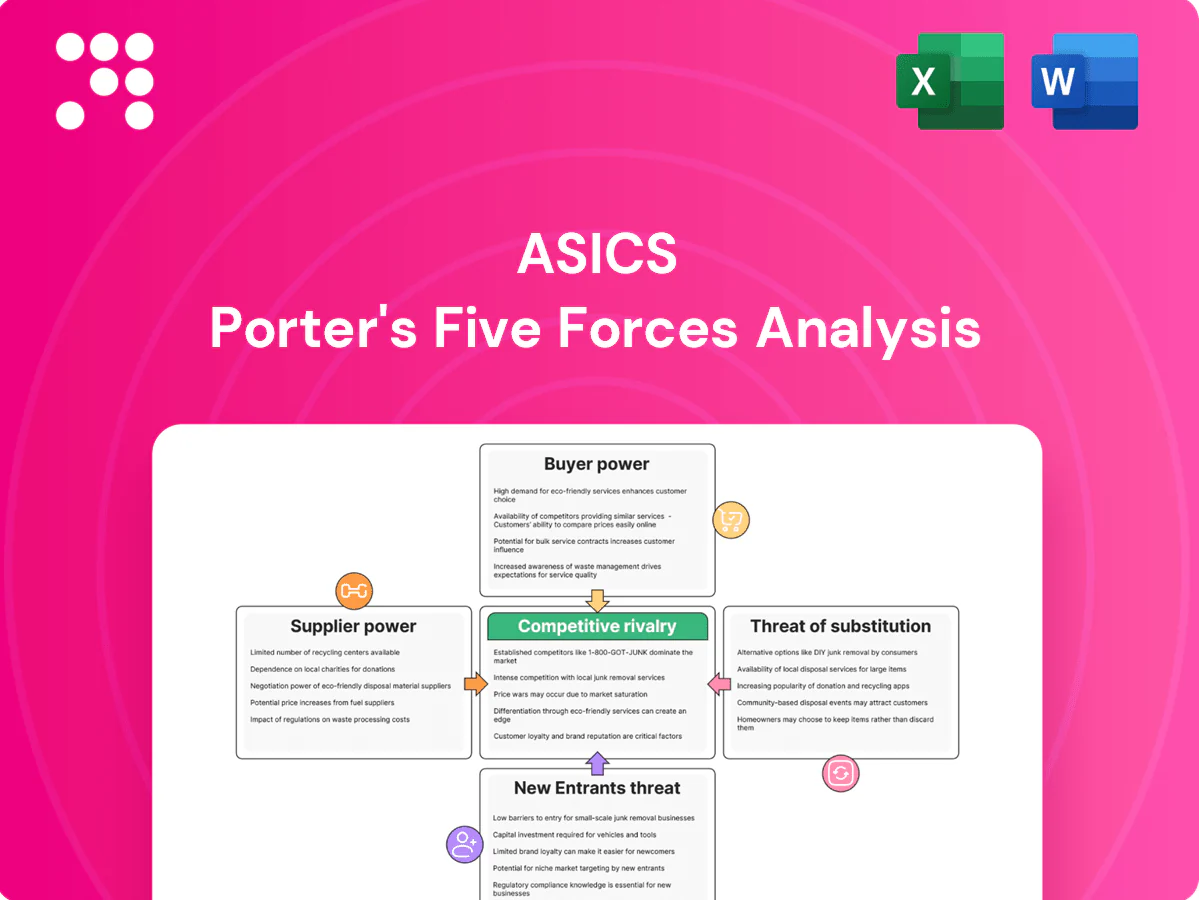

Asics faces intense rivalry from global sportswear giants, moderate supplier power, rising substitute threats from athleisure brands, and steady buyer expectations for innovation and sustainability. This snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Asics’s competitive dynamics, market pressures, and strategic advantages in detail. Get force-by-force ratings, visuals, and actionable implications to inform investment or strategy.

Suppliers Bargaining Power

Specialized performance materials

ASICS depends on a limited pool of qualified suppliers for advanced foams, gels, carbon plates, technical meshes and rubber compounds, giving suppliers moderate leverage—heightened during innovation waves when adoption spikes. Long qualification cycles raise switching costs and delay product rollouts. ASICS counters with multi-sourcing and longer-term contracts; in FY2024 ASICS reported consolidated net sales of 452.7 billion JPY, supporting sustained supplier partnerships.

Contract manufacturing concentration

Production is largely outsourced to contract manufacturers in Asia, where capable athletic-shoe factories are limited, giving vendors with tooling know-how and process quality leverage to bargain for better terms. ASICS mitigates this through vendor diversification and volume commitments across suppliers. Nonetheless, rapid reallocation of complex models remains difficult, sustaining short-term supplier power.

ESG and compliance constraints

Rising labor, environmental and traceability standards shrink ASICS’ approved supplier base, letting compliant partners demand price premiums or stricter terms; ASICS’ brand standards and supplier Code of Conduct limit easy switching and raise switching costs. Over time ASICS’ supplier development programs aim to broaden the pool and normalize costs through training and capacity investments.

Logistics and input volatility

Logistics and input volatility—rising freight, currency swings, and spikes in oil-based foams and rubber—increase supplier leverage as vendors pass costs through and squeeze ASICS margins; ASICS mitigates with hedging, buffer inventory and 2024 near-shoring pilots, but abrupt shocks still tilt power to suppliers.

- Freight/currency/commodity pass-through

- Hedging & buffer inventory

- 2024 near-shoring pilots

- Sudden shocks favor suppliers

Co-development and mutual dependence

Joint R&D on midsole compounds and last designs creates integration that tempers unilateral supplier power by aligning technical roadmaps and lowering opportunism; ASICS’ emphasis on proprietary GEL and FF technologies (supporting global revenue around ≈JPY 380bn in FY2023) reinforces mutual dependence while raising switching costs.

Footwear leader with 452.7 bn JPY FY2024 sales faces moderate supplier power

ASICS faces moderate supplier power: specialized materials, long qualification cycles and concentration in Asian contract factories raise switching costs; FY2024 consolidated net sales 452.7 billion JPY supports long-term contracts. Compliance costs, logistics volatility and limited factory capacity give suppliers leverage despite multi-sourcing, hedging and 2024 near-shoring pilots.

| Metric | Value |

|---|---|

| Net sales FY2024 | 452.7 bn JPY |

| Global revenue approx FY2023 | ≈380 bn JPY |

What is included in the product

Uncovers key drivers of competition for Asics—evaluating rivalry, supplier and buyer power, threats from substitutes and new entrants—and their impact on pricing and profitability. Identifies disruptive forces, emerging threats, and protective market dynamics; fully editable for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces for ASICS that highlights competitive pressures and relieves decision paralysis—customizable for shifting market trends and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Fragmented consumers, price sensitivity

End consumers for ASICS are highly fragmented, limiting individual bargaining power, but frequent promotions and online price transparency have increased price sensitivity; ASICS reported net sales of JPY 538.6 billion in FY2024, pressuring margins. ASICS defends pricing through product differentiation and tiered pricing across performance and lifestyle lines. Loyalty programs and fit/technology education (run clinics, digital gait analysis) reduce churn and support retention.

Wholesale retailers’ leverage

Wholesale retailers — sporting goods chains and specialty run shops — shape assortment, pricing and shelf space, and their ability to switch brands gives them strong negotiating leverage; ASICS reported net sales of ¥360.1 billion in FY2023, using sell-through data, MAP policies and exclusive SKUs to protect margin and placement. Despite these measures, large accounts can still demand better terms and concessions on price, promotion and lead times.

Growing DTC reduces dependence

ASICS’ expansion of e-commerce and owned stores has pushed DTC to roughly 30–35% of sales by 2024, strengthening direct customer data and relationships and reducing dependence on powerful wholesale partners.

DTC gives ASICS greater pricing control and enables personalized offers and product assortments using first‑party data, lowering customer bargaining leverage.

To fully capture these benefits ASICS must continue investing in logistics, fulfillment and CX—areas management cites as priorities to sustain digital growth.

Product differentiation tempers power

Asics product differentiation—GEL cushioning and stability lines—reduces direct comparability, making core runners prioritize fit and injury prevention over price; hero models therefore show lower price elasticity. Casual buyers remain more price-driven, keeping overall customer bargaining power mixed. Brand heritage and performance tech sustain premium positioning despite discount competition.

- Core runners: value feel/fit

- Hero models: lower elasticity

- Casual segment: price-sensitive

High information availability

Reviews, wear tests, and social media (Instagram ~2 billion MAUs in 2024) make ASICS product performance and deals highly visible, accelerating discovery across channels.

Informed customers can cross-shop across brands within minutes, raising switching ease and bargaining power and pressuring margins.

ASICS offsets this through community tactics—try-on events, run clubs, and brand ambassadors—to maintain trust and reduce churn.

- Visible reviews: higher switching

- 2B IG users (2024): broad reach

- Community events: retention

DTC to 30-35% boosts pricing, net sales JPY 538.6bn

End consumers are fragmented and price-sensitive amid promotions; ASICS reported net sales JPY 538.6 billion in FY2024, pressuring margins. DTC growth to ~30–35% by 2024 strengthens pricing control and first‑party data. Wholesale buyers retain strong leverage (wholesale sales ¥360.1bn FY2023) but ASICS offsets via product differentiation (GEL/hero models) and community retention tactics.

| Metric | Value |

|---|---|

| Net sales FY2024 | JPY 538.6bn |

| DTC share 2024 | 30–35% |

| Wholesale sales FY2023 | ¥360.1bn |

| Instagram reach 2024 | ~2.0B MAUs |

Preview Before You Purchase

Asics Porter's Five Forces Analysis

This preview shows the exact Asics Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted and ready for download and use the moment you buy, containing supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry insights. You're viewing the final file—instant access upon payment.

A Must-Have Tool for Decision-Makers

Asics faces intense rivalry from global sportswear giants, moderate supplier power, rising substitute threats from athleisure brands, and steady buyer expectations for innovation and sustainability. This snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Asics’s competitive dynamics, market pressures, and strategic advantages in detail. Get force-by-force ratings, visuals, and actionable implications to inform investment or strategy.

Suppliers Bargaining Power

Specialized performance materials

ASICS depends on a limited pool of qualified suppliers for advanced foams, gels, carbon plates, technical meshes and rubber compounds, giving suppliers moderate leverage—heightened during innovation waves when adoption spikes. Long qualification cycles raise switching costs and delay product rollouts. ASICS counters with multi-sourcing and longer-term contracts; in FY2024 ASICS reported consolidated net sales of 452.7 billion JPY, supporting sustained supplier partnerships.

Contract manufacturing concentration

Production is largely outsourced to contract manufacturers in Asia, where capable athletic-shoe factories are limited, giving vendors with tooling know-how and process quality leverage to bargain for better terms. ASICS mitigates this through vendor diversification and volume commitments across suppliers. Nonetheless, rapid reallocation of complex models remains difficult, sustaining short-term supplier power.

ESG and compliance constraints

Rising labor, environmental and traceability standards shrink ASICS’ approved supplier base, letting compliant partners demand price premiums or stricter terms; ASICS’ brand standards and supplier Code of Conduct limit easy switching and raise switching costs. Over time ASICS’ supplier development programs aim to broaden the pool and normalize costs through training and capacity investments.

Logistics and input volatility

Logistics and input volatility—rising freight, currency swings, and spikes in oil-based foams and rubber—increase supplier leverage as vendors pass costs through and squeeze ASICS margins; ASICS mitigates with hedging, buffer inventory and 2024 near-shoring pilots, but abrupt shocks still tilt power to suppliers.

- Freight/currency/commodity pass-through

- Hedging & buffer inventory

- 2024 near-shoring pilots

- Sudden shocks favor suppliers

Co-development and mutual dependence

Joint R&D on midsole compounds and last designs creates integration that tempers unilateral supplier power by aligning technical roadmaps and lowering opportunism; ASICS’ emphasis on proprietary GEL and FF technologies (supporting global revenue around ≈JPY 380bn in FY2023) reinforces mutual dependence while raising switching costs.

Footwear leader with 452.7 bn JPY FY2024 sales faces moderate supplier power

ASICS faces moderate supplier power: specialized materials, long qualification cycles and concentration in Asian contract factories raise switching costs; FY2024 consolidated net sales 452.7 billion JPY supports long-term contracts. Compliance costs, logistics volatility and limited factory capacity give suppliers leverage despite multi-sourcing, hedging and 2024 near-shoring pilots.

| Metric | Value |

|---|---|

| Net sales FY2024 | 452.7 bn JPY |

| Global revenue approx FY2023 | ≈380 bn JPY |

What is included in the product

Uncovers key drivers of competition for Asics—evaluating rivalry, supplier and buyer power, threats from substitutes and new entrants—and their impact on pricing and profitability. Identifies disruptive forces, emerging threats, and protective market dynamics; fully editable for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces for ASICS that highlights competitive pressures and relieves decision paralysis—customizable for shifting market trends and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Fragmented consumers, price sensitivity

End consumers for ASICS are highly fragmented, limiting individual bargaining power, but frequent promotions and online price transparency have increased price sensitivity; ASICS reported net sales of JPY 538.6 billion in FY2024, pressuring margins. ASICS defends pricing through product differentiation and tiered pricing across performance and lifestyle lines. Loyalty programs and fit/technology education (run clinics, digital gait analysis) reduce churn and support retention.

Wholesale retailers’ leverage

Wholesale retailers — sporting goods chains and specialty run shops — shape assortment, pricing and shelf space, and their ability to switch brands gives them strong negotiating leverage; ASICS reported net sales of ¥360.1 billion in FY2023, using sell-through data, MAP policies and exclusive SKUs to protect margin and placement. Despite these measures, large accounts can still demand better terms and concessions on price, promotion and lead times.

Growing DTC reduces dependence

ASICS’ expansion of e-commerce and owned stores has pushed DTC to roughly 30–35% of sales by 2024, strengthening direct customer data and relationships and reducing dependence on powerful wholesale partners.

DTC gives ASICS greater pricing control and enables personalized offers and product assortments using first‑party data, lowering customer bargaining leverage.

To fully capture these benefits ASICS must continue investing in logistics, fulfillment and CX—areas management cites as priorities to sustain digital growth.

Product differentiation tempers power

Asics product differentiation—GEL cushioning and stability lines—reduces direct comparability, making core runners prioritize fit and injury prevention over price; hero models therefore show lower price elasticity. Casual buyers remain more price-driven, keeping overall customer bargaining power mixed. Brand heritage and performance tech sustain premium positioning despite discount competition.

- Core runners: value feel/fit

- Hero models: lower elasticity

- Casual segment: price-sensitive

High information availability

Reviews, wear tests, and social media (Instagram ~2 billion MAUs in 2024) make ASICS product performance and deals highly visible, accelerating discovery across channels.

Informed customers can cross-shop across brands within minutes, raising switching ease and bargaining power and pressuring margins.

ASICS offsets this through community tactics—try-on events, run clubs, and brand ambassadors—to maintain trust and reduce churn.

- Visible reviews: higher switching

- 2B IG users (2024): broad reach

- Community events: retention

DTC to 30-35% boosts pricing, net sales JPY 538.6bn

End consumers are fragmented and price-sensitive amid promotions; ASICS reported net sales JPY 538.6 billion in FY2024, pressuring margins. DTC growth to ~30–35% by 2024 strengthens pricing control and first‑party data. Wholesale buyers retain strong leverage (wholesale sales ¥360.1bn FY2023) but ASICS offsets via product differentiation (GEL/hero models) and community retention tactics.

| Metric | Value |

|---|---|

| Net sales FY2024 | JPY 538.6bn |

| DTC share 2024 | 30–35% |

| Wholesale sales FY2023 | ¥360.1bn |

| Instagram reach 2024 | ~2.0B MAUs |

Preview Before You Purchase

Asics Porter's Five Forces Analysis

This preview shows the exact Asics Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted and ready for download and use the moment you buy, containing supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry insights. You're viewing the final file—instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Asics faces intense rivalry from global sportswear giants, moderate supplier power, rising substitute threats from athleisure brands, and steady buyer expectations for innovation and sustainability. This snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Asics’s competitive dynamics, market pressures, and strategic advantages in detail. Get force-by-force ratings, visuals, and actionable implications to inform investment or strategy.

Suppliers Bargaining Power

Specialized performance materials

ASICS depends on a limited pool of qualified suppliers for advanced foams, gels, carbon plates, technical meshes and rubber compounds, giving suppliers moderate leverage—heightened during innovation waves when adoption spikes. Long qualification cycles raise switching costs and delay product rollouts. ASICS counters with multi-sourcing and longer-term contracts; in FY2024 ASICS reported consolidated net sales of 452.7 billion JPY, supporting sustained supplier partnerships.

Contract manufacturing concentration

Production is largely outsourced to contract manufacturers in Asia, where capable athletic-shoe factories are limited, giving vendors with tooling know-how and process quality leverage to bargain for better terms. ASICS mitigates this through vendor diversification and volume commitments across suppliers. Nonetheless, rapid reallocation of complex models remains difficult, sustaining short-term supplier power.

ESG and compliance constraints

Rising labor, environmental and traceability standards shrink ASICS’ approved supplier base, letting compliant partners demand price premiums or stricter terms; ASICS’ brand standards and supplier Code of Conduct limit easy switching and raise switching costs. Over time ASICS’ supplier development programs aim to broaden the pool and normalize costs through training and capacity investments.

Logistics and input volatility

Logistics and input volatility—rising freight, currency swings, and spikes in oil-based foams and rubber—increase supplier leverage as vendors pass costs through and squeeze ASICS margins; ASICS mitigates with hedging, buffer inventory and 2024 near-shoring pilots, but abrupt shocks still tilt power to suppliers.

- Freight/currency/commodity pass-through

- Hedging & buffer inventory

- 2024 near-shoring pilots

- Sudden shocks favor suppliers

Co-development and mutual dependence

Joint R&D on midsole compounds and last designs creates integration that tempers unilateral supplier power by aligning technical roadmaps and lowering opportunism; ASICS’ emphasis on proprietary GEL and FF technologies (supporting global revenue around ≈JPY 380bn in FY2023) reinforces mutual dependence while raising switching costs.

Footwear leader with 452.7 bn JPY FY2024 sales faces moderate supplier power

ASICS faces moderate supplier power: specialized materials, long qualification cycles and concentration in Asian contract factories raise switching costs; FY2024 consolidated net sales 452.7 billion JPY supports long-term contracts. Compliance costs, logistics volatility and limited factory capacity give suppliers leverage despite multi-sourcing, hedging and 2024 near-shoring pilots.

| Metric | Value |

|---|---|

| Net sales FY2024 | 452.7 bn JPY |

| Global revenue approx FY2023 | ≈380 bn JPY |

What is included in the product

Uncovers key drivers of competition for Asics—evaluating rivalry, supplier and buyer power, threats from substitutes and new entrants—and their impact on pricing and profitability. Identifies disruptive forces, emerging threats, and protective market dynamics; fully editable for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces for ASICS that highlights competitive pressures and relieves decision paralysis—customizable for shifting market trends and ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Fragmented consumers, price sensitivity

End consumers for ASICS are highly fragmented, limiting individual bargaining power, but frequent promotions and online price transparency have increased price sensitivity; ASICS reported net sales of JPY 538.6 billion in FY2024, pressuring margins. ASICS defends pricing through product differentiation and tiered pricing across performance and lifestyle lines. Loyalty programs and fit/technology education (run clinics, digital gait analysis) reduce churn and support retention.

Wholesale retailers’ leverage

Wholesale retailers — sporting goods chains and specialty run shops — shape assortment, pricing and shelf space, and their ability to switch brands gives them strong negotiating leverage; ASICS reported net sales of ¥360.1 billion in FY2023, using sell-through data, MAP policies and exclusive SKUs to protect margin and placement. Despite these measures, large accounts can still demand better terms and concessions on price, promotion and lead times.

Growing DTC reduces dependence

ASICS’ expansion of e-commerce and owned stores has pushed DTC to roughly 30–35% of sales by 2024, strengthening direct customer data and relationships and reducing dependence on powerful wholesale partners.

DTC gives ASICS greater pricing control and enables personalized offers and product assortments using first‑party data, lowering customer bargaining leverage.

To fully capture these benefits ASICS must continue investing in logistics, fulfillment and CX—areas management cites as priorities to sustain digital growth.

Product differentiation tempers power

Asics product differentiation—GEL cushioning and stability lines—reduces direct comparability, making core runners prioritize fit and injury prevention over price; hero models therefore show lower price elasticity. Casual buyers remain more price-driven, keeping overall customer bargaining power mixed. Brand heritage and performance tech sustain premium positioning despite discount competition.

- Core runners: value feel/fit

- Hero models: lower elasticity

- Casual segment: price-sensitive

High information availability

Reviews, wear tests, and social media (Instagram ~2 billion MAUs in 2024) make ASICS product performance and deals highly visible, accelerating discovery across channels.

Informed customers can cross-shop across brands within minutes, raising switching ease and bargaining power and pressuring margins.

ASICS offsets this through community tactics—try-on events, run clubs, and brand ambassadors—to maintain trust and reduce churn.

- Visible reviews: higher switching

- 2B IG users (2024): broad reach

- Community events: retention

DTC to 30-35% boosts pricing, net sales JPY 538.6bn

End consumers are fragmented and price-sensitive amid promotions; ASICS reported net sales JPY 538.6 billion in FY2024, pressuring margins. DTC growth to ~30–35% by 2024 strengthens pricing control and first‑party data. Wholesale buyers retain strong leverage (wholesale sales ¥360.1bn FY2023) but ASICS offsets via product differentiation (GEL/hero models) and community retention tactics.

| Metric | Value |

|---|---|

| Net sales FY2024 | JPY 538.6bn |

| DTC share 2024 | 30–35% |

| Wholesale sales FY2023 | ¥360.1bn |

| Instagram reach 2024 | ~2.0B MAUs |

Preview Before You Purchase

Asics Porter's Five Forces Analysis

This preview shows the exact Asics Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted and ready for download and use the moment you buy, containing supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry insights. You're viewing the final file—instant access upon payment.