Assertio Porter's Five Forces Analysis

Don't Miss the Bigger Picture

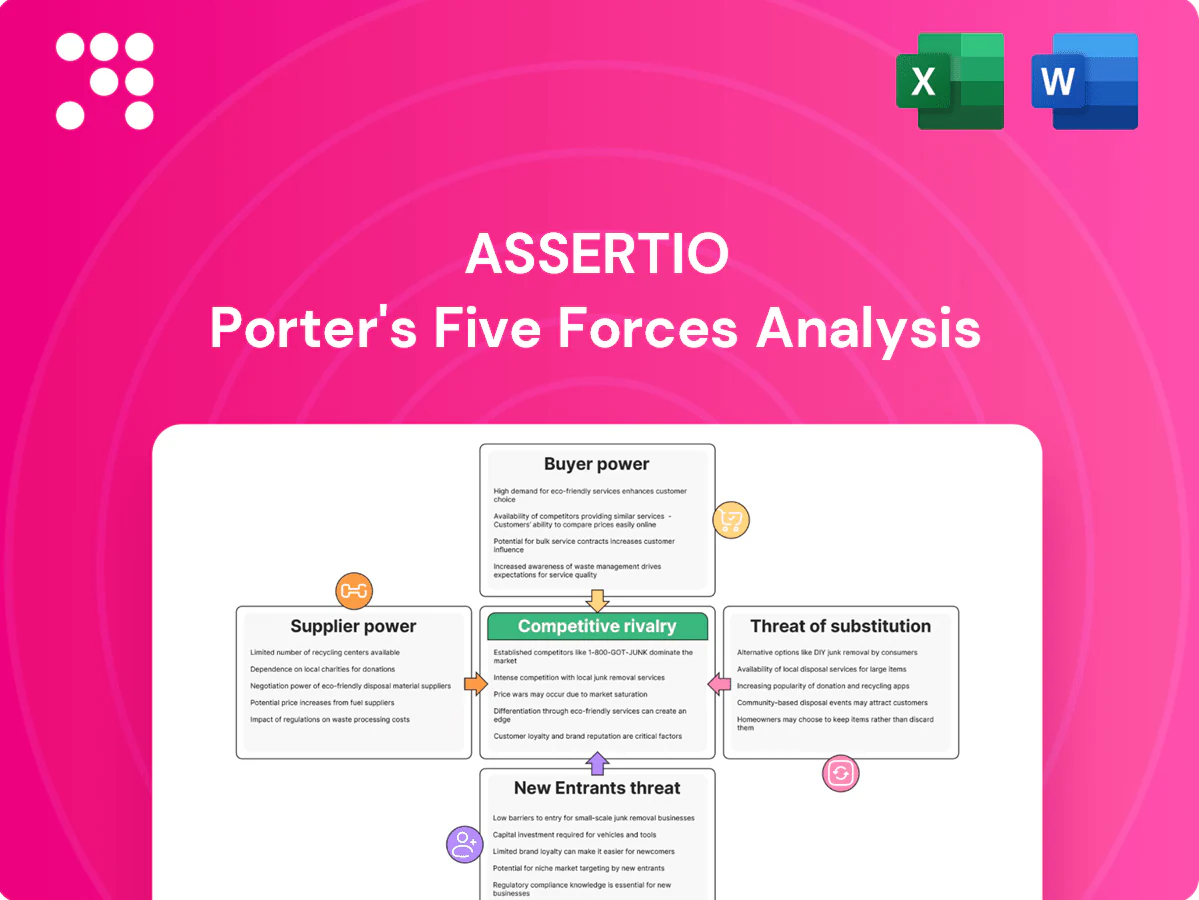

Assertio’s Porter's Five Forces snapshot highlights competitive intensity across suppliers, buyers, new entrants, substitutes, and rivalry, revealing pockets of margin pressure and opportunity. It synthesizes industry trends and regulatory impact on Assertio’s pricing power and innovation runway. Strategically relevant for investors and managers, it spots where Assertio can defend or expand its position. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated API and CMO base

As of 2024 Assertio relies on a concentrated set of API suppliers and CMOs, creating meaningful switching costs and supply-risk exposure. The limited pool of qualified specialty-pharma manufacturers increases bargaining leverage for CMOs. Dual sourcing remains feasible but is costly and time-consuming to implement. Any disruption to these partners can quickly affect service levels and Assertio’s pricing power.

Specialized inputs and quality compliance

High cGMP, FDA and EU quality standards in 2024 narrow vendor options, increasing supplier clout and bargaining power for Assertio. Compliance-driven audits and validations create switching costs that lock in supplier relationships and extend qualification cycles. Suppliers have been able to pass through inflation and rising compliance costs, forcing Assertio to balance strict quality assurance against cost containment pressures.

Licensing and royalty partners

In-licensed products impose milestone and royalty obligations that function as supplier leverage; industry royalty rates in 2024 typically ranged 5–20%, and milestone tranches often reach multiple millions. Originators can dictate contract terms and retain audit rights, creating asymmetric power. Renegotiation risk rises at lifecycle inflection points. Assertio’s diversified deal pipeline helps partially offset this supplier leverage.

Clinical, data, and packaging vendors

Clinical CROs, HEOR/data providers and specialized packagers supply differentiated, hard-to-substitute capabilities; vendor tacit knowledge on Assertio’s niche products creates switching frictions and specialist premiums. Assertio’s limited portfolio scale constrains volume discount leverage, while long-term contracts (common in 2024 CRO deals) stabilize supply but can lock in higher pricing.

Logistics and cold-chain dependencies

Special handling for cold-chain drugs concentrates distribution with a few distributors and 3PLs, so regulatory holds or capacity crunches can rapidly tighten supply; freight and temperature-control surcharges are frequently passed to manufacturers, while Assertio cushions risk via inventory buffers and service-level agreements to preserve continuity.

- concentrated 3PL reliance

- regulatory/capacity bottlenecks

- freight/temp costs shift to manufacturers

- mitigation: buffers + SLAs

Concentrated suppliers, strict cGMP/regulatory hurdles and high switching costs; use buffers, SLAs

Assertio faces high supplier leverage in 2024 due to concentrated API/CMO pools, stringent cGMP/FDA/EU requirements and costly switching/qualification. In‑licensed royalty ranges (5–20%) plus multi‑million milestones and long‑term CRO/3PL contracts amplify supplier bargaining power. Mitigations include inventory buffers, SLAs and diversified in‑licensing pipeline.

| Metric | 2024 |

|---|---|

| Royalty range | 5–20% |

| Milestone size | multi‑million USD |

| Contracts | long‑term common |

What is included in the product

Concise Porter's Five Forces assessment tailored to Assertio, highlighting competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and regulatory impacts on pricing and margins. Actionable insights identify disruptive threats and protective dynamics for strategic planning.

A concise one-sheet Porter's Five Forces for Assertio that clarifies competitive pressures at a glance. Customizable inputs and an instant radar view visualize threats and opportunities, simplifying boardroom decisions and slide-ready reporting.

Customers Bargaining Power

PBMs and payer formulary control

PBMs and three major payers control roughly 75–80% of U.S. prescription coverage, wielding leverage through prior authorization, step edits and rebate negotiations. Rebates commonly sit in the mid-20s percent of list price, driving a substantial gap between list and net price and compressing margins. Securing preferred tiering requires robust clinical evidence and contracting; non-preferred placement can rapidly divert volume to alternatives.

Group purchasing and wholesalers

GPOs aggregate purchasing for roughly 95% of US hospitals and large health systems, and the three major wholesalers (McKesson, AmerisourceBergen, Cardinal) together control about 85% of pharmaceutical distribution. Chargeback and administrative fee structures materially compress net pricing, while service-level penalties and return terms shift costs onto manufacturers. Assertio can trade broader distribution access for negotiated pricing concessions to maintain formulary placement.

Specialist prescribers

Neurology and pain specialists prioritize demonstrated efficacy, safety, and ease of use over headline price, with 68% of specialists in a 2024 therapeutic-area survey rating clinical outcomes as their top prescribing driver.

They remain responsive to payer restrictions and step-therapy rules, which in 2024 affected placement for roughly half of branded pain therapies on commercial formularies.

KOL advocacy can reduce buyer power locally by accelerating guideline uptake and regional prescribing patterns.

Targeted education and real-world evidence generation in 2024 supported sustained adoption and improved formulary positioning.

Hospitals and IDNs

Hospitals and IDNs exercise strong bargaining power: formulary committees prioritize cost-effectiveness and therapeutic interchange, and IDNs — managing roughly 50% of U.S. hospital beds in 2024 — can standardize protocols that limit brand flexibility. Contract wins or losses frequently produce step-change volume swings (often >20–30%), so value dossiers and real-world outcomes data are critical to secure access and pricing concessions.

- Formulary focus: cost-effectiveness

- IDN reach: ~50% U.S. beds (2024)

- Volume impact: contract swings >20–30%

- Must-have: value dossiers and outcomes data

Patient affordability dynamics

High out-of-pocket costs raise patient sensitivity to copay assistance and generics, pushing price-driven switches; patient support programs can blunt this buyer power but add commercial and R&D expense. Adherence tools (digital reminders, nurse outreach) boost perceived value and persistence, while sudden affordability shocks can trigger rapid demand erosion. Specialty drugs represent roughly 50% of US drug spend, amplifying stakes.

- High OOP sensitivity: increases generic/coupon usage

- Support programs: mitigate churn but raise costs

- Adherence tools: improve persistence and lifetime value

- Affordability shocks: risk quick demand decline; specialty drugs ~50% of spend

PBMs/GPOs/IDNs dominate access - rebates compress margins; outcomes and payer rules drive placements

PBMs/three payers control ~75–80% of US prescription coverage and use prior auth/step edits plus mid-20% rebates to compress margins. GPOs cover ~95% of hospitals; three wholesalers ~85% distribution, giving strong negotiating leverage. Specialists rate outcomes top driver (68%); payer rules affect ~50% branded pain placements and IDNs (~50% beds) can shift volume >20–30%.

| Counterparty | 2024 metric | Impact |

|---|---|---|

| PBMs/Payers | 75–80% coverage | Rebates mid-20% compress margins |

| GPOs/Hospitals | GPOs 95% / IDNs ~50% beds | Formulary control; >20–30% volume swings |

| Specialists | 68% prioritize outcomes | Clinical evidence drives tiering |

Full Version Awaits

Assertio Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Assertio you'll receive after purchase—fully formatted and ready to use. It contains the complete evaluation of competitive rivalry, buyer and supplier power, threats of entry and substitution. No samples or placeholders, instant download on payment.

Don't Miss the Bigger Picture

Assertio’s Porter's Five Forces snapshot highlights competitive intensity across suppliers, buyers, new entrants, substitutes, and rivalry, revealing pockets of margin pressure and opportunity. It synthesizes industry trends and regulatory impact on Assertio’s pricing power and innovation runway. Strategically relevant for investors and managers, it spots where Assertio can defend or expand its position. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated API and CMO base

As of 2024 Assertio relies on a concentrated set of API suppliers and CMOs, creating meaningful switching costs and supply-risk exposure. The limited pool of qualified specialty-pharma manufacturers increases bargaining leverage for CMOs. Dual sourcing remains feasible but is costly and time-consuming to implement. Any disruption to these partners can quickly affect service levels and Assertio’s pricing power.

Specialized inputs and quality compliance

High cGMP, FDA and EU quality standards in 2024 narrow vendor options, increasing supplier clout and bargaining power for Assertio. Compliance-driven audits and validations create switching costs that lock in supplier relationships and extend qualification cycles. Suppliers have been able to pass through inflation and rising compliance costs, forcing Assertio to balance strict quality assurance against cost containment pressures.

Licensing and royalty partners

In-licensed products impose milestone and royalty obligations that function as supplier leverage; industry royalty rates in 2024 typically ranged 5–20%, and milestone tranches often reach multiple millions. Originators can dictate contract terms and retain audit rights, creating asymmetric power. Renegotiation risk rises at lifecycle inflection points. Assertio’s diversified deal pipeline helps partially offset this supplier leverage.

Clinical, data, and packaging vendors

Clinical CROs, HEOR/data providers and specialized packagers supply differentiated, hard-to-substitute capabilities; vendor tacit knowledge on Assertio’s niche products creates switching frictions and specialist premiums. Assertio’s limited portfolio scale constrains volume discount leverage, while long-term contracts (common in 2024 CRO deals) stabilize supply but can lock in higher pricing.

Logistics and cold-chain dependencies

Special handling for cold-chain drugs concentrates distribution with a few distributors and 3PLs, so regulatory holds or capacity crunches can rapidly tighten supply; freight and temperature-control surcharges are frequently passed to manufacturers, while Assertio cushions risk via inventory buffers and service-level agreements to preserve continuity.

- concentrated 3PL reliance

- regulatory/capacity bottlenecks

- freight/temp costs shift to manufacturers

- mitigation: buffers + SLAs

Concentrated suppliers, strict cGMP/regulatory hurdles and high switching costs; use buffers, SLAs

Assertio faces high supplier leverage in 2024 due to concentrated API/CMO pools, stringent cGMP/FDA/EU requirements and costly switching/qualification. In‑licensed royalty ranges (5–20%) plus multi‑million milestones and long‑term CRO/3PL contracts amplify supplier bargaining power. Mitigations include inventory buffers, SLAs and diversified in‑licensing pipeline.

| Metric | 2024 |

|---|---|

| Royalty range | 5–20% |

| Milestone size | multi‑million USD |

| Contracts | long‑term common |

What is included in the product

Concise Porter's Five Forces assessment tailored to Assertio, highlighting competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and regulatory impacts on pricing and margins. Actionable insights identify disruptive threats and protective dynamics for strategic planning.

A concise one-sheet Porter's Five Forces for Assertio that clarifies competitive pressures at a glance. Customizable inputs and an instant radar view visualize threats and opportunities, simplifying boardroom decisions and slide-ready reporting.

Customers Bargaining Power

PBMs and payer formulary control

PBMs and three major payers control roughly 75–80% of U.S. prescription coverage, wielding leverage through prior authorization, step edits and rebate negotiations. Rebates commonly sit in the mid-20s percent of list price, driving a substantial gap between list and net price and compressing margins. Securing preferred tiering requires robust clinical evidence and contracting; non-preferred placement can rapidly divert volume to alternatives.

Group purchasing and wholesalers

GPOs aggregate purchasing for roughly 95% of US hospitals and large health systems, and the three major wholesalers (McKesson, AmerisourceBergen, Cardinal) together control about 85% of pharmaceutical distribution. Chargeback and administrative fee structures materially compress net pricing, while service-level penalties and return terms shift costs onto manufacturers. Assertio can trade broader distribution access for negotiated pricing concessions to maintain formulary placement.

Specialist prescribers

Neurology and pain specialists prioritize demonstrated efficacy, safety, and ease of use over headline price, with 68% of specialists in a 2024 therapeutic-area survey rating clinical outcomes as their top prescribing driver.

They remain responsive to payer restrictions and step-therapy rules, which in 2024 affected placement for roughly half of branded pain therapies on commercial formularies.

KOL advocacy can reduce buyer power locally by accelerating guideline uptake and regional prescribing patterns.

Targeted education and real-world evidence generation in 2024 supported sustained adoption and improved formulary positioning.

Hospitals and IDNs

Hospitals and IDNs exercise strong bargaining power: formulary committees prioritize cost-effectiveness and therapeutic interchange, and IDNs — managing roughly 50% of U.S. hospital beds in 2024 — can standardize protocols that limit brand flexibility. Contract wins or losses frequently produce step-change volume swings (often >20–30%), so value dossiers and real-world outcomes data are critical to secure access and pricing concessions.

- Formulary focus: cost-effectiveness

- IDN reach: ~50% U.S. beds (2024)

- Volume impact: contract swings >20–30%

- Must-have: value dossiers and outcomes data

Patient affordability dynamics

High out-of-pocket costs raise patient sensitivity to copay assistance and generics, pushing price-driven switches; patient support programs can blunt this buyer power but add commercial and R&D expense. Adherence tools (digital reminders, nurse outreach) boost perceived value and persistence, while sudden affordability shocks can trigger rapid demand erosion. Specialty drugs represent roughly 50% of US drug spend, amplifying stakes.

- High OOP sensitivity: increases generic/coupon usage

- Support programs: mitigate churn but raise costs

- Adherence tools: improve persistence and lifetime value

- Affordability shocks: risk quick demand decline; specialty drugs ~50% of spend

PBMs/GPOs/IDNs dominate access - rebates compress margins; outcomes and payer rules drive placements

PBMs/three payers control ~75–80% of US prescription coverage and use prior auth/step edits plus mid-20% rebates to compress margins. GPOs cover ~95% of hospitals; three wholesalers ~85% distribution, giving strong negotiating leverage. Specialists rate outcomes top driver (68%); payer rules affect ~50% branded pain placements and IDNs (~50% beds) can shift volume >20–30%.

| Counterparty | 2024 metric | Impact |

|---|---|---|

| PBMs/Payers | 75–80% coverage | Rebates mid-20% compress margins |

| GPOs/Hospitals | GPOs 95% / IDNs ~50% beds | Formulary control; >20–30% volume swings |

| Specialists | 68% prioritize outcomes | Clinical evidence drives tiering |

Full Version Awaits

Assertio Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Assertio you'll receive after purchase—fully formatted and ready to use. It contains the complete evaluation of competitive rivalry, buyer and supplier power, threats of entry and substitution. No samples or placeholders, instant download on payment.

Description

Don't Miss the Bigger Picture

Assertio’s Porter's Five Forces snapshot highlights competitive intensity across suppliers, buyers, new entrants, substitutes, and rivalry, revealing pockets of margin pressure and opportunity. It synthesizes industry trends and regulatory impact on Assertio’s pricing power and innovation runway. Strategically relevant for investors and managers, it spots where Assertio can defend or expand its position. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated API and CMO base

As of 2024 Assertio relies on a concentrated set of API suppliers and CMOs, creating meaningful switching costs and supply-risk exposure. The limited pool of qualified specialty-pharma manufacturers increases bargaining leverage for CMOs. Dual sourcing remains feasible but is costly and time-consuming to implement. Any disruption to these partners can quickly affect service levels and Assertio’s pricing power.

Specialized inputs and quality compliance

High cGMP, FDA and EU quality standards in 2024 narrow vendor options, increasing supplier clout and bargaining power for Assertio. Compliance-driven audits and validations create switching costs that lock in supplier relationships and extend qualification cycles. Suppliers have been able to pass through inflation and rising compliance costs, forcing Assertio to balance strict quality assurance against cost containment pressures.

Licensing and royalty partners

In-licensed products impose milestone and royalty obligations that function as supplier leverage; industry royalty rates in 2024 typically ranged 5–20%, and milestone tranches often reach multiple millions. Originators can dictate contract terms and retain audit rights, creating asymmetric power. Renegotiation risk rises at lifecycle inflection points. Assertio’s diversified deal pipeline helps partially offset this supplier leverage.

Clinical, data, and packaging vendors

Clinical CROs, HEOR/data providers and specialized packagers supply differentiated, hard-to-substitute capabilities; vendor tacit knowledge on Assertio’s niche products creates switching frictions and specialist premiums. Assertio’s limited portfolio scale constrains volume discount leverage, while long-term contracts (common in 2024 CRO deals) stabilize supply but can lock in higher pricing.

Logistics and cold-chain dependencies

Special handling for cold-chain drugs concentrates distribution with a few distributors and 3PLs, so regulatory holds or capacity crunches can rapidly tighten supply; freight and temperature-control surcharges are frequently passed to manufacturers, while Assertio cushions risk via inventory buffers and service-level agreements to preserve continuity.

- concentrated 3PL reliance

- regulatory/capacity bottlenecks

- freight/temp costs shift to manufacturers

- mitigation: buffers + SLAs

Concentrated suppliers, strict cGMP/regulatory hurdles and high switching costs; use buffers, SLAs

Assertio faces high supplier leverage in 2024 due to concentrated API/CMO pools, stringent cGMP/FDA/EU requirements and costly switching/qualification. In‑licensed royalty ranges (5–20%) plus multi‑million milestones and long‑term CRO/3PL contracts amplify supplier bargaining power. Mitigations include inventory buffers, SLAs and diversified in‑licensing pipeline.

| Metric | 2024 |

|---|---|

| Royalty range | 5–20% |

| Milestone size | multi‑million USD |

| Contracts | long‑term common |

What is included in the product

Concise Porter's Five Forces assessment tailored to Assertio, highlighting competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and regulatory impacts on pricing and margins. Actionable insights identify disruptive threats and protective dynamics for strategic planning.

A concise one-sheet Porter's Five Forces for Assertio that clarifies competitive pressures at a glance. Customizable inputs and an instant radar view visualize threats and opportunities, simplifying boardroom decisions and slide-ready reporting.

Customers Bargaining Power

PBMs and payer formulary control

PBMs and three major payers control roughly 75–80% of U.S. prescription coverage, wielding leverage through prior authorization, step edits and rebate negotiations. Rebates commonly sit in the mid-20s percent of list price, driving a substantial gap between list and net price and compressing margins. Securing preferred tiering requires robust clinical evidence and contracting; non-preferred placement can rapidly divert volume to alternatives.

Group purchasing and wholesalers

GPOs aggregate purchasing for roughly 95% of US hospitals and large health systems, and the three major wholesalers (McKesson, AmerisourceBergen, Cardinal) together control about 85% of pharmaceutical distribution. Chargeback and administrative fee structures materially compress net pricing, while service-level penalties and return terms shift costs onto manufacturers. Assertio can trade broader distribution access for negotiated pricing concessions to maintain formulary placement.

Specialist prescribers

Neurology and pain specialists prioritize demonstrated efficacy, safety, and ease of use over headline price, with 68% of specialists in a 2024 therapeutic-area survey rating clinical outcomes as their top prescribing driver.

They remain responsive to payer restrictions and step-therapy rules, which in 2024 affected placement for roughly half of branded pain therapies on commercial formularies.

KOL advocacy can reduce buyer power locally by accelerating guideline uptake and regional prescribing patterns.

Targeted education and real-world evidence generation in 2024 supported sustained adoption and improved formulary positioning.

Hospitals and IDNs

Hospitals and IDNs exercise strong bargaining power: formulary committees prioritize cost-effectiveness and therapeutic interchange, and IDNs — managing roughly 50% of U.S. hospital beds in 2024 — can standardize protocols that limit brand flexibility. Contract wins or losses frequently produce step-change volume swings (often >20–30%), so value dossiers and real-world outcomes data are critical to secure access and pricing concessions.

- Formulary focus: cost-effectiveness

- IDN reach: ~50% U.S. beds (2024)

- Volume impact: contract swings >20–30%

- Must-have: value dossiers and outcomes data

Patient affordability dynamics

High out-of-pocket costs raise patient sensitivity to copay assistance and generics, pushing price-driven switches; patient support programs can blunt this buyer power but add commercial and R&D expense. Adherence tools (digital reminders, nurse outreach) boost perceived value and persistence, while sudden affordability shocks can trigger rapid demand erosion. Specialty drugs represent roughly 50% of US drug spend, amplifying stakes.

- High OOP sensitivity: increases generic/coupon usage

- Support programs: mitigate churn but raise costs

- Adherence tools: improve persistence and lifetime value

- Affordability shocks: risk quick demand decline; specialty drugs ~50% of spend

PBMs/GPOs/IDNs dominate access - rebates compress margins; outcomes and payer rules drive placements

PBMs/three payers control ~75–80% of US prescription coverage and use prior auth/step edits plus mid-20% rebates to compress margins. GPOs cover ~95% of hospitals; three wholesalers ~85% distribution, giving strong negotiating leverage. Specialists rate outcomes top driver (68%); payer rules affect ~50% branded pain placements and IDNs (~50% beds) can shift volume >20–30%.

| Counterparty | 2024 metric | Impact |

|---|---|---|

| PBMs/Payers | 75–80% coverage | Rebates mid-20% compress margins |

| GPOs/Hospitals | GPOs 95% / IDNs ~50% beds | Formulary control; >20–30% volume swings |

| Specialists | 68% prioritize outcomes | Clinical evidence drives tiering |

Full Version Awaits

Assertio Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Assertio you'll receive after purchase—fully formatted and ready to use. It contains the complete evaluation of competitive rivalry, buyer and supplier power, threats of entry and substitution. No samples or placeholders, instant download on payment.